•

•

How to Open a GBP Account for a UAE Company with UK Sort Code

If you run a UAE company and bill clients in the UK, you've probably hit this wall already: your client wants to pay by bank transfer, but your only option is a SWIFT wire. That means fees on their end, delays on yours, and sometimes a polite request to "sort out a UK account."

UK buyers are used to paying locally — sort code, account number, done. A GBP account for UAE company with a real UK sort code removes that friction. Your UAE business gets UK payment details. Your UK clients pay the same way they pay anyone else.

What is a GBP account for a UAE company with a UK sort code?

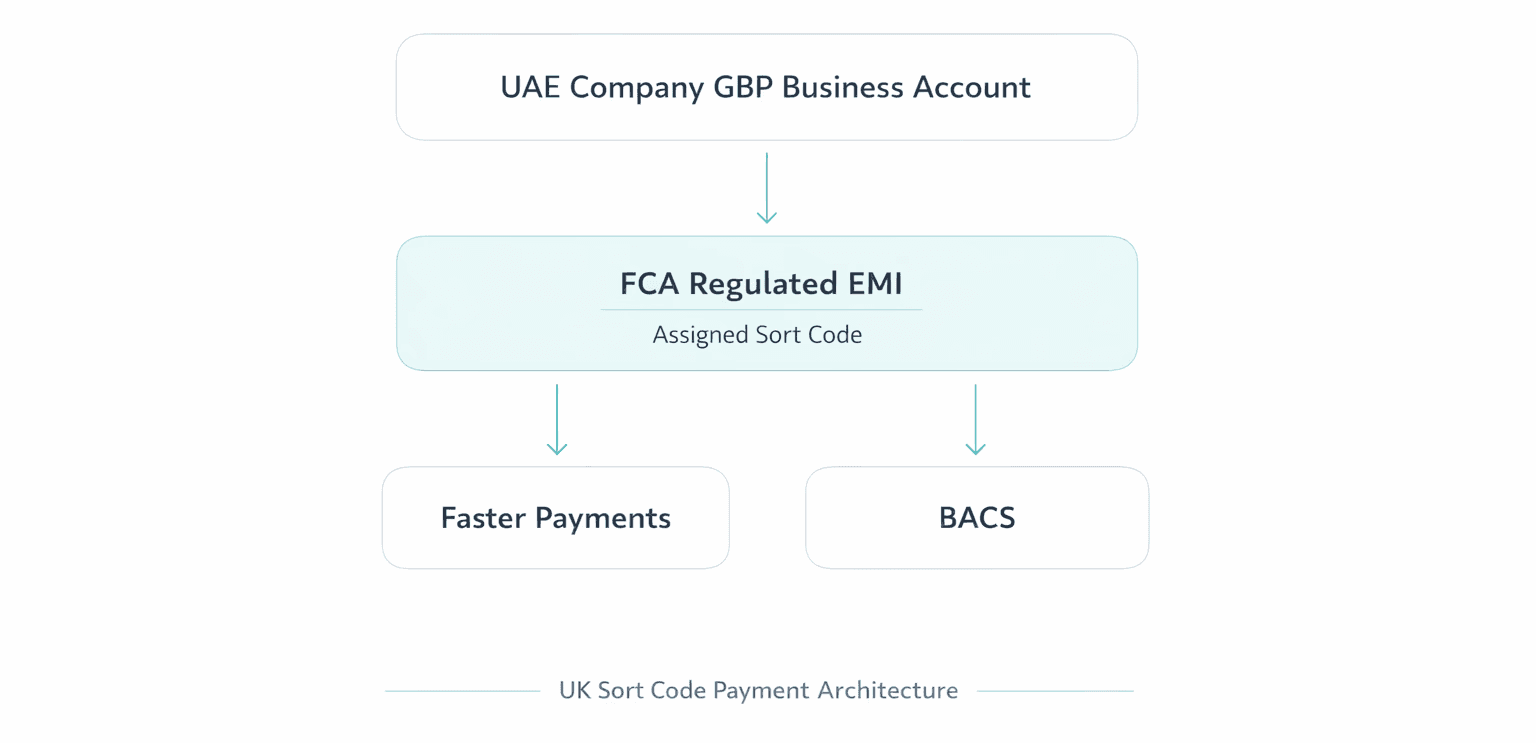

A GBP account for a UAE company with a UK sort code is a UK domestic payment account issued by an FCA-authorised Electronic Money Institution allowing non-UK businesses to receive GBP via Faster Payments, BACS, or CHAPS.

Key Takeaways

A UAE-registered company can open a GBP account with a real UK sort code — without a physical UK office or UK-resident director.

FCA-authorised Electronic Money Institutions (EMIs) provide access to UK local payment rails, including Faster Payments, BACS, and CHAPS.

UAE companies receive an actual UK account number and sort code, enabling UK clients to pay locally with no international wire fees.

The onboarding process is compliance-driven: expect KYC, AML screening, and documentation of business structure and ownership.

EMI accounts operate under FCA safeguarding rules — client funds are held separately from the institution's own capital.

Preparation matters: incomplete documentation or unclear ownership structures are the most common causes of rejection or delay.

Why UAE Businesses Need a UK Payment Account with a GBP Sort Code

A UK payment account for UAE company means the entire transaction stays inside the UK banking system — no international routing, no correspondent bank hops, no wire fees for either side.

Without local GBP details, receiving via SWIFT means the UK client pays a wire fee, the transfer hops through one or more correspondent banks, and settlement takes one to four business days. With a local account, funds arrive via Faster Payments in minutes, or via BACS within two working days.

UAE company GBP bank details issued through an FCA EMI are indistinguishable from a domestic business account on the client's end. They see a sort code and account number, pay through their normal banking app, and you receive clean sterling.

Where this matters most:

A UAE SaaS company billing UK subscribers monthly — local details reduce failed payments and invoice back-and-forth.

A UAE exporter waiting on payment from UK buyers — Faster Payments settlement is far more predictable than SWIFT.

A UAE freelancer or agency with UK clients — proper UK bank details simply look more professional.

Can a UAE Company Open a GBP Account in the UK?

Yes — but not through a traditional UK high street bank. If you've already tried Barclays or HSBC and been turned away, that's expected.

Traditional UK banks (Barclays, HSBC, NatWest, Lloyds) typically want UK-resident directors, a UK-registered entity, or physical presence in the country. Offshore structures get declined regularly, onboarding takes weeks or months, and minimum balance requirements can be significant.

FCA-authorised EMIs work differently. Authorised by the Financial Conduct Authority to issue e-money and provide payment services, they assess applications on what your business actually does — not where your directors live. You can verify any EMI's status on the FCA Financial Services Register.

One important distinction: bank deposits are covered by the Financial Services Compensation Scheme (FSCS) up to £85,000. EMI accounts use safeguarding instead — client funds are held in a segregated account at an authorised credit institution, ring-fenced from the EMI's own capital. If the EMI fails, those funds are returned to clients first. Different mechanism, but meaningful protection.

EMI vs UK High Street Bank vs Digital Providers: Full Comparison

Not all GBP account options are equal for a UAE-registered business. Here's how the main provider types compare across the criteria that matter most.

Criteria | UK High Street Bank | Wise Business | Airwallex | FCA EMI (e.g. EQWIRE) |

|---|---|---|---|---|

UK presence required | Usually yes | No | No | No |

UK director required | Often yes | No | No | No |

Eligibility for UAE entities | Rare / difficult | Yes | Yes | Yes |

Onboarding timeline | 4–12 weeks | 1–5 days | 3–10 days | 5–15 business days |

UK sort code issued | Yes (branch account) | Yes (local details) | Yes (local details) | Yes (EMI sort code) |

Payment rails | Faster Payments, BACS, CHAPS | Faster Payments, BACS | Faster Payments, BACS | Faster Payments, BACS, CHAPS |

Fund protection | FSCS up to £85,000 | Safeguarding (FCA) | Safeguarding (FCA/ASIC) | Safeguarding (FCA) |

FX margin | 2–4% | ~0.4–1.5% | ~0.5–1% | Competitive / transparent |

Multi-currency support | Limited | Yes (50+ currencies) | Yes (60+ currencies) | Yes |

Typical approval odds for UAE cos. | Low | High | High | High (compliance-dependent) |

Business account features | Full banking suite | Payments focused | Payments + treasury | Payments + FX |

Minimum balance | Often £10,000+ | None | None | None / low |

Traditional UK banks are a structural mismatch for UAE entities — it's not just red tape. Digital providers and FCA-authorised EMIs are built for international businesses from the ground up. The real differences between them come down to FX pricing, compliance depth, and how much payment infrastructure you need.

How Does a UAE Registered Business Get a UK Sort Code?

A GBP sort code for UAE registered business is issued by an FCA-authorised EMI connected to UK payment schemes. The mechanics are simple once you understand the model.

EMIs participate in Faster Payments, BACS, or CHAPS either directly or through a sponsoring bank. When the EMI onboards your business, it assigns you a dedicated UK account number paired with its sort code. Payments sent to those credentials route through the EMI's scheme account and credit to your wallet in real time.

The account number is real — not a virtual IBAN or redirect. It's a legitimate local sterling account that accepts domestic UK transfers. This is how a UAE holding company can obtain a GBP sort code via an FCA-authorised EMI account without needing a direct UK banking relationship.

The one caveat: the sort code belongs to the EMI, not a named UK bank branch. For most use cases — receiving payments, paying UK suppliers — this makes no difference. It's only worth double-checking if a specific counterparty requires a named high street bank account.

Step-by-Step: Open a GBP Account for a UAE-Registered Business via UK FCA EMI

The process is compliance-driven but not complicated. Go in prepared and it moves quickly.

Step 1 – Confirm Eligibility

Check that your business structure and activity fall within what the EMI accepts. Most providers work with UAE free zone entities (DIFC, ADGM, JAFZA, DMCC, and others) and mainland UAE companies. Core eligibility criteria:

A valid UAE trade licence with a clearly defined business activity

Identifiable Ultimate Beneficial Owners (UBOs) holding 25% or more of shares

Legitimate cross-border commercial activity

No adverse history with financial regulators or sanctions lists

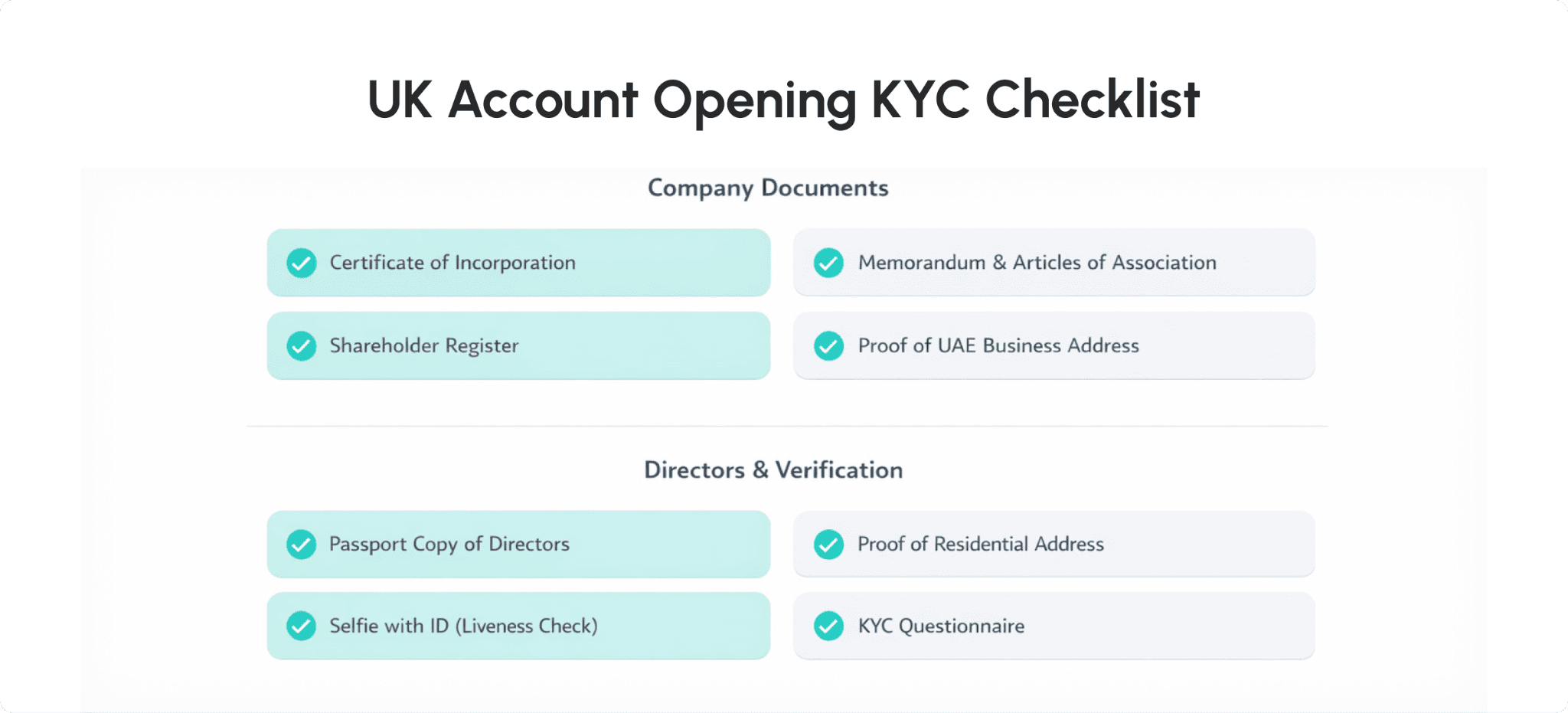

Step 2 – Submit KYC & Compliance Documents

Know Your Customer (KYC) documentation typically includes:

Certificate of Incorporation and Memorandum of Association

Trade licence (current, activity classification visible)

Shareholder register and corporate structure chart

Certified ID for all directors and UBOs (passport, proof of address)

Recent bank statements or proof of existing financial operations

Evidence of business activity (contracts, invoices, website, client list)

If your structure involves holding companies or multiple corporate layers, prepare a clear ownership chart tracing all the way to the natural persons who ultimately own the business — before you apply, not during.

Step 3 – Account Review & Compliance Checks

The EMI's compliance team runs AML screening against sanctions lists and PEP databases, a risk assessment based on your business model and expected volumes, and verification of your corporate structure. This typically takes two to ten business days. The most common reason it drags is slow responses from the applicant — reply quickly to any follow-up questions.

Step 4 – Receive Your UK Account Number & Sort Code

Once approved, you receive your UK account number and sort code. Use them immediately for Faster Payments, BACS, and CHAPS transfers. For UAE entities with clean structures and complete documentation, the full process runs five to fifteen business days end to end.

GBP Account for Offshore Company Without UK Office

Not having a UK office is not a problem with EMIs. Traditional banks used physical presence as a risk shortcut. EMIs don't.

A GBP account for offshore company without UK office is evaluated on business substance, ownership transparency, source of funds, and the compliance profile of your directors and UBOs. If those four things check out, the absence of a UK address is irrelevant.

Rejections typically come from: no demonstrable business activity, an ownership structure that obscures who's in control, activities in higher-risk sectors (unlicensed crypto, certain commodities, remittance), or documentation that's incomplete or inconsistently certified. The fix is preparation — get your ownership chart documented, ensure beneficial owners have current certified ID, and have something concrete that shows the business is real.

How to Receive GBP Payments as a UAE-Registered Company

Once your account is live, the process is exactly what you'd hope. Here's how to receive GBP payments as a UAE-registered company in practice:

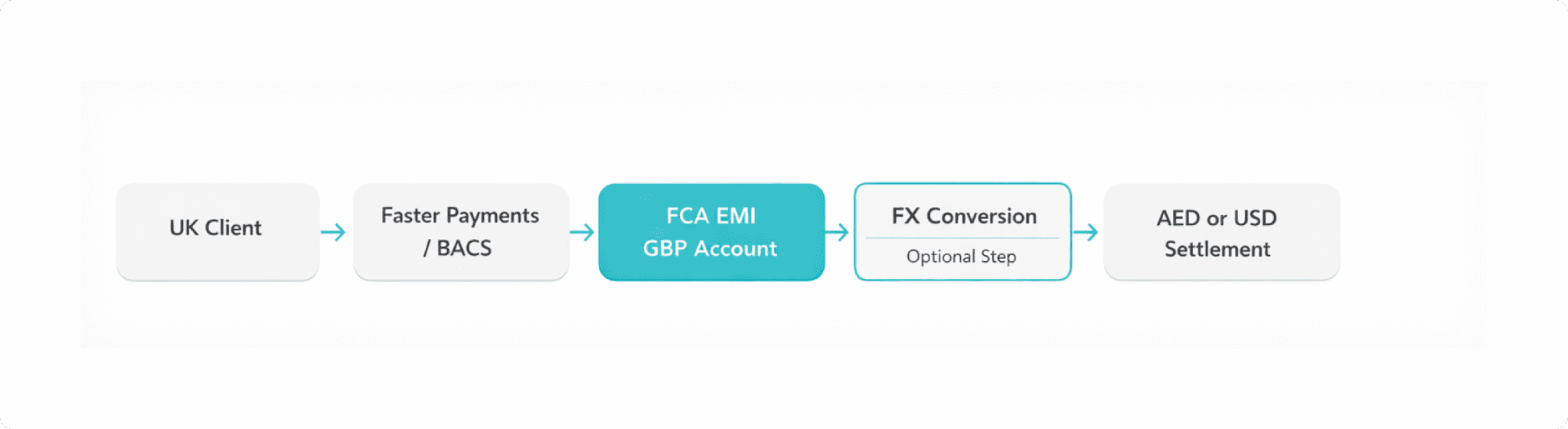

Issue your GBP invoice with the UK sort code and account number as payment details.

Your UK client makes a standard domestic bank transfer from their normal banking app.

Funds move via Faster Payments (within two hours) or BACS (two working days).

Sterling lands in your safeguarded EMI account.

Hold in GBP, convert to AED or another currency, or transfer out — your choice.

The operational benefits: no SWIFT fees for either party, same-day or near-instant settlement via Faster Payments, predictable settlement windows for working capital planning, and full flexibility on when you convert to AED or USD.

Compliance, FCA Regulation & Safeguarding Explained

The Financial Conduct Authority regulates EMIs under the Electronic Money Regulations 2011. FCA authorisation requires capital adequacy, robust AML and KYC programmes, and full safeguarding of client funds.

Safeguarding means 100% of your balance must be held in a segregated account at an authorised credit institution — separate from the EMI's own money, and returned to clients first if the EMI fails. Unlike FSCS protection (capped at £85,000), safeguarding covers your full balance. The mechanism differs, but the protection is real.

FCA-regulated EMIs are under ongoing supervision and reporting requirements. That's a meaningful baseline when deciding who to trust with your business funds.

Operational Advantages for Growing International Businesses

Most UAE businesses operating internationally aren't just dealing in GBP. EUR from European clients, USD from US contracts, AED domestically — managing these through accounts plugged into local payment rails in each market is cleaner and cheaper than routing everything through SWIFT.

Each SWIFT hop adds cost and uncertainty. A multi-currency setup with local account details in key markets lets you collect locally, hold in the currencies you need, and convert when the timing makes sense. Providers like Airwallex and Wise Business have built exactly this model for international SMBs. EQWIRE's infrastructure supports the same approach, including UK sterling accounts with full local payment rail access.

Open a GBP Account for Your UAE Company

Get UK payment details with a real sort code and receive GBP from UK clients through local payment rails.

Common Challenges UAE Companies Face When Opening a UK Payment Account

Most problems here are predictable — and avoidable.

Account rejections usually trace back to high-risk business categories, sanctions exposure in the ownership chain, or a business model that can't be documented. Incomplete KYC is the most preventable cause of delay — missing UBO ID, an expired trade licence, or no proof of actual operations will stall any application. Misunderstanding the EMI model catches some applicants off guard: no overdrafts, no chequebooks, no FSCS protection. Set expectations before you start. Unclear ownership structures — nominee shareholders, multi-layer holdcos, trust arrangements — need detailed documentation to pass KYC, and that can't be rushed. Finally, check payment limits before you onboard, not after — most EMIs apply transaction and balance ceilings that scale with your verification tier.

Conclusion

Getting a GBP account for UAE company with a genuine UK sort code is straightforward once you're on the right path. FCA-authorised EMIs give UAE-registered businesses full access to UK local payment rails — no UK office, no UK-resident directors, no UK incorporation required.

The process works: your EMI connects to Faster Payments and BACS, issues you a real sort code and account number, and your UK clients pay you like any local supplier. What determines how fast it goes is how prepared you are — clean ownership documentation, current KYC materials, clear evidence of real business operations.

For UAE businesses billing UK clients in SaaS, export, professional services, or e-commerce, local sterling account details are the difference between getting paid quickly and chasing wires.

FAQs

Can a UAE company open a GBP account in the UK?

Yes. A UAE company can open a GBP account in the UK through FCA-authorised Electronic Money Institutions. Traditional banks typically require UK residency or physical presence, but regulated EMIs assess applications on business activity, ownership transparency, and compliance profile. A UK office is not a requirement.

How does a UAE registered business get a UK sort code?

A UAE registered business gets a UK sort code through an FCA-authorised EMI connected to UK payment schemes such as Faster Payments or BACS. The EMI assigns a dedicated UK account number and sort code to each verified business client. Payments settle exactly as they would for any domestic UK account.

How long does it take to get a UK sort code for a UAE business?

For straightforward applications with complete documentation, the process typically takes five to fifteen business days. Complex ownership structures or incomplete documentation will extend this. Responding quickly to compliance queries is the fastest way to speed things up.

What documents are required for a UK payment account for UAE company?

You'll need the UAE trade licence, certificate of incorporation, memorandum of association, shareholder register, a corporate structure chart, certified ID for all directors and UBOs holding 25% or more, recent bank statements, and evidence of business operations. Complex structures may require additional supporting materials.

Are EMI accounts safe for holding business funds?

FCA-authorised EMIs must safeguard 100% of client funds in segregated accounts at authorised credit institutions, ring-fenced from the EMI's own capital. Funds are protected in the event of insolvency — unlike FSCS, safeguarding covers your full balance rather than a capped amount, but operates through a distinct legal mechanism.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)