•

•

GBP Faster Payments for Offshore Companies: Same-Day Settlement Guide

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

A UK customer pays an invoice immediately — yet the offshore company receiving the payment waits two or three days for the money to arrive.

The delay isn't the client's fault. It's the SWIFT correspondent banking system: a chain of intermediary banks, each adding processing time and fees before funds reach the intended recipient. For a company registered in Hong Kong, Cyprus, or the British Virgin Islands billing UK clients regularly, that friction compounds into a persistent cash flow problem.

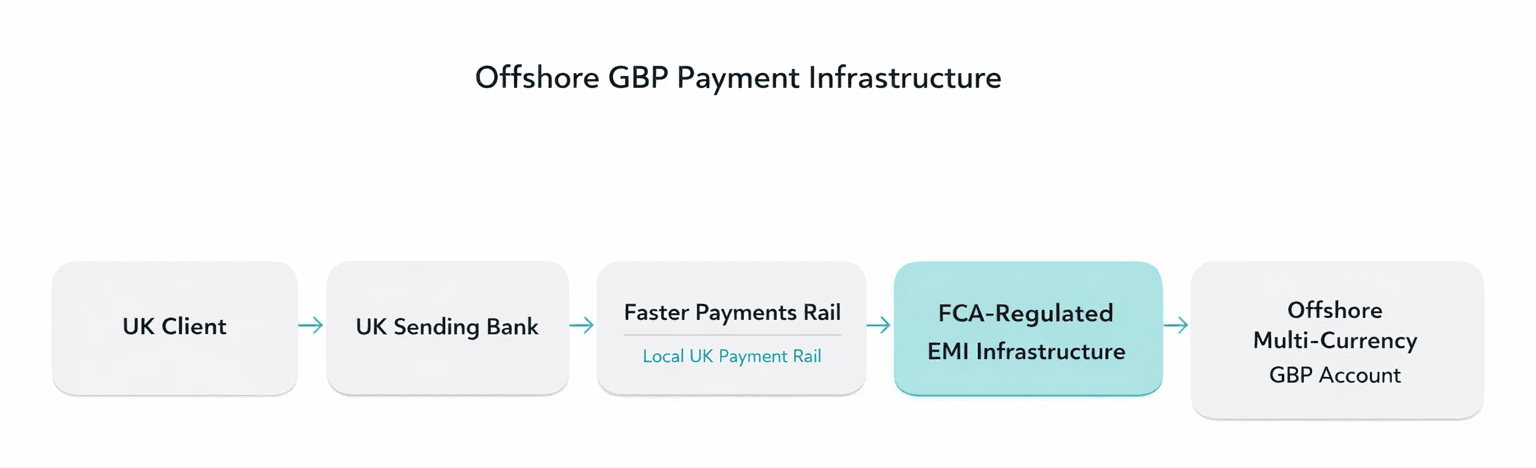

GBP Faster Payments for offshore company structures solves this directly. Non-UK entities can receive GBP payments internationally using a virtual GBP account — UK local account details for a foreign business, including a dedicated sort code and account number issued by an FCA-regulated intermediary — without a UK-resident company or a UK bank account for a non-resident company. Payments settle the same day via the domestic Faster Payments rail, bypassing SWIFT entirely.

Key Takeaways

GBP Faster Payments is the UK's real-time domestic payment scheme — near-instant settlement within seconds, up to £1 million per transaction.

Offshore companies cannot access Faster Payments directly through UK high-street banks due to compliance and residency requirements.

on-UK businesses gain access to Faster Payments for offshore company UK use through FCA-regulated EMIs via a sponsor bank model, receiving a virtual GBP account with a dedicated UK sort code and account number.

Settles on a T+0 basis: an offshore company receive GBP same day UK clients send the transfer — removing the need for 1–3 day SWIFT settlement delays.

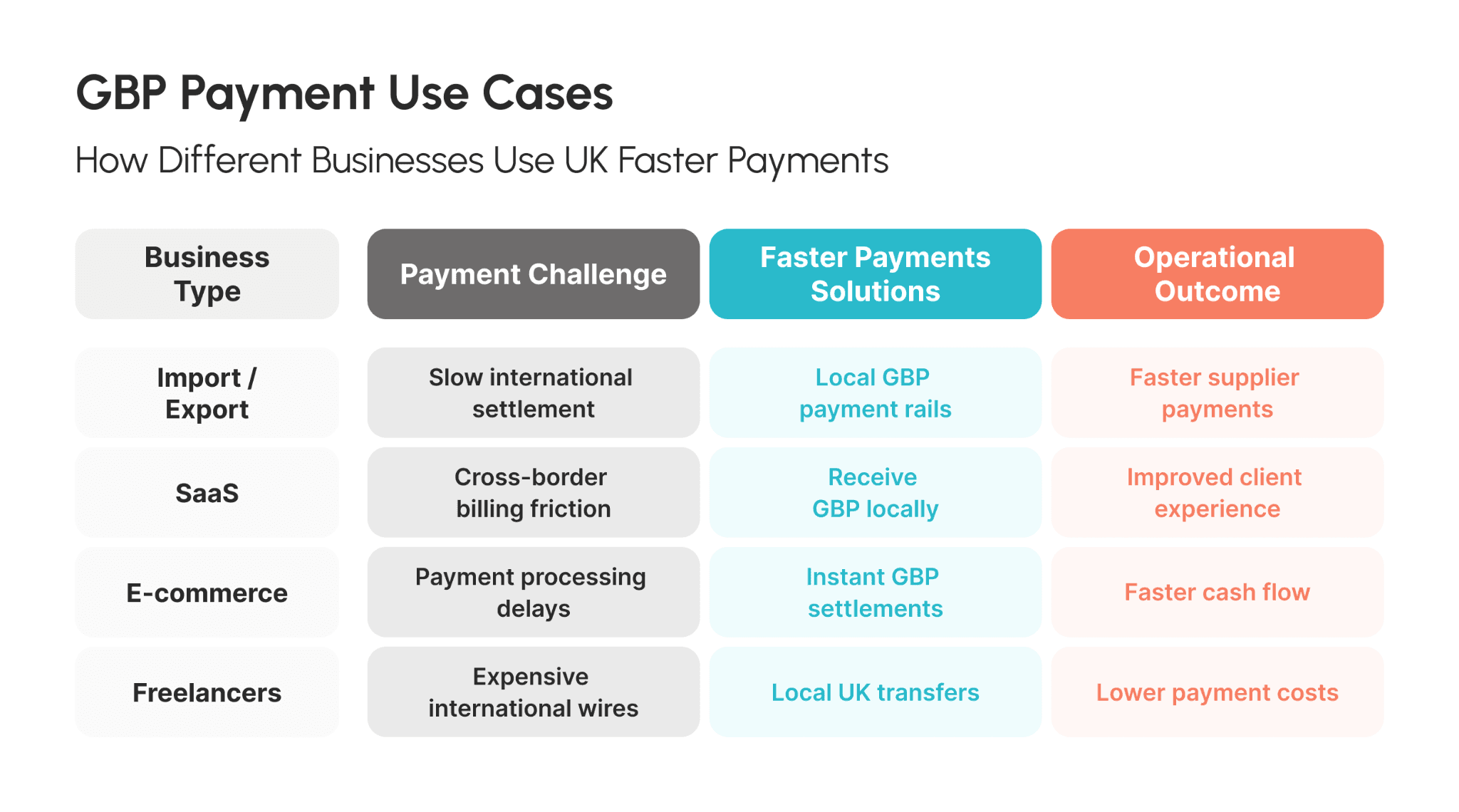

Potential use cases: import/export companies, SaaS providers, online retailers, and individual freelancers with UK clients.

Key selection criteria: FCA status, Faster Payments Scheme, currencies accepted, and offshore regulatory capabilities.

What Is UK Faster Payments (FPS) and How Do Offshore Companies Use It?

The Faster Payment Service (FPS), also referred to as the UK's real-time interbank payment system, is operated by Pay.UK and regulated by the Payment Systems Regulator (PSR). The Faster Payment Service was established in 2008 and has been reported to process over four billion transactions with a total value exceeding £3 trillion on an annual basis, based on statistics provided by Pay.UK.

Definition: FPS is a domestic payment system in the UK, which allows for the transfer of funds between connected UK accounts on a near-instant basis, 24/7, and is regulated as a designated payment system by the PSR.

The scheme runs 24/7 including weekends and bank holidays. The Faster Payments limit UK scheme rules allow up to £1 million per transaction, as documented in Pay.UK's scheme rules, though individual banks often apply lower thresholds. For offshore businesses using an EMI-issued account, the applicable limit is determined by the EMI's sponsor bank arrangement.

How Faster Payments Compares to CHAPS and BACS

Scheme | Speed | Cost | Limit | Best For |

|---|---|---|---|---|

Faster Payments | Seconds to 2 hours | Low | Up to £1 million (scheme maximum; institution limits vary) | Everyday transfers, supplier payments |

CHAPS | Same day (cut-off applies) | Higher | No formal limit | High-value, property settlements |

BACS | 3 working days | Very low | No formal limit | Bulk payroll, direct debits |

For cross-border GBP collection, Faster Payments offers the optimal balance of speed and cost. Faster Payments T+0 settlement for non-UK registered company use is the key operational benefit — enabling same-day GBP settlement offshore company structures otherwise unable to access UK domestic rails.

Can a Non-UK Company Receive GBP via Faster Payments?

Not directly — but access is achievable through the right intermediary.

The most common question is how offshore company accesses Faster Payments without a UK bank account. A non-UK company cannot join the scheme without a UK banking licence, but it can open a virtual GBP account with an FCA-regulated EMI and receive GBP from UK clients as if it held a standard UK business account. This is how UK Faster Payments access non-UK business structures achieve same-day GBP settlement in practice.

High street banks in the UK have stringent KYC and AML procedures, which have made it difficult for offshore companies to maintain traditional business bank accounts. The difficulties encountered are related to disclosing beneficial ownership, sources of funds, and monitoring transactions. The trend of de-risking offshore companies is recognized and documented by the Financial Action Task Force (FATF), which is endorsed by the FCA. The banks have started to view offshore companies as high risk.

The Alternative: FCA-Regulated EMIs and the Sponsor Bank Model

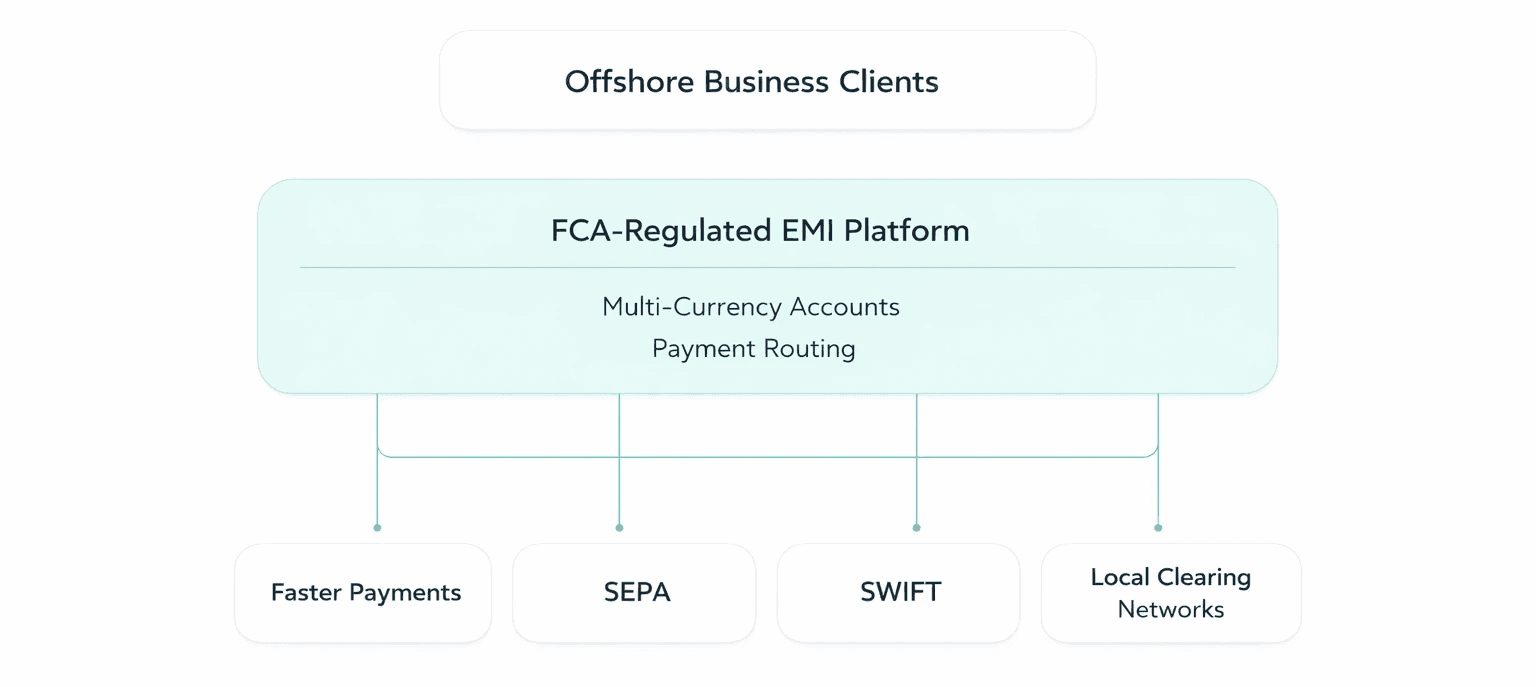

Electronic Money Institutions (EMIs) that are authorised by the FCA are issued a license under the Electronic Money Regulations 2011 to issue electronic money, hold client money in safeguarded accounts, and connect to domestic payment rails without a banking license. What is the key difference in the comparison of an EMI account and a bank account? Client money is safeguarded in segregated accounts under the Electronic Money Regulations 2011, which is sufficient protection for GBP collection. Verify any EMI's FCA status on the FCA Financial Services Register.

Most EMIs access Faster Payments via a sponsor bank model — a direct scheme participant that sponsors the EMI's payment rail access. A non-UK business can open a multi-currency account with such an EMI and obtain a UK sort code for a non-UK company, which works in exactly the same way as a normal UK business account and thus enables a business to receive GBP without a UK company or banking relationship. This is the mechanism through which an offshore business receive GBP via UK Faster Payments network rails — delivering same-day GBP T+0 settlement for offshore registered business via UK EMI, without any direct UK banking relationship. Client money is held in segregated accounts in accordance with the Electronic Money Regulations 2011.

How Offshore Companies Receive GBP Using Faster Payments

The offshore company onboards with an FCA-authorised EMI that provides UK payment rail access.

The platform issues a virtual GBP account — a dedicated UK sort code and account number in the company's name.

UK clients initiate standard bank transfers to that account — no SWIFT/BIC, no international payment form.

Funds settle through the Faster Payments infrastructure — typically within seconds to minutes.

The company holds, converts, or withdraws the GBP balance as needed.

The result is T+0 settlement: funds are typically available the same day, with no correspondent delays or intermediary deductions — compared to 1–3 business days and fee leakage via SWIFT.

Faster Payments | SWIFT International Transfer | |

|---|---|---|

Settlement | Seconds to 2 hours (T+0) | 1–3 business days |

Cost | Near-zero, no intermediary deductions | £15–30 sender fee (typical; varies by institution) + correspondent charges |

Infrastructure | Domestic UK rail | Global correspondent banking network |

Account needed | UK sort code via EMI | Foreign bank account |

Availability | 24/7 including weekends | Business days, cut-off times apply |

Benefits of Faster Payments Access for Offshore Businesses

Same-day settlement (T+0) is the primary advantage. A UK client sending £10,000 via Faster Payments typically pays a few pence to a few pounds; a comparable SWIFT transfer commonly costs £15–30 at origin, with further correspondent bank deductions reducing the amount received (exact fees vary by institution and route).

From the UK client's perspective, the experience is identical to paying any domestic supplier — sort code, account number, no SWIFT/BIC required. This removes friction and reduces payment errors. For businesses on net-30 or net-60 terms, predictable T+0 settlement improves FX conversion timing and cash flow visibility.

Why Offshore Companies Cannot Open UK Bank Accounts Easily

Under the Money Laundering Regulations 2017, UK banks must conduct enhanced due diligence (EDD) on offshore entities — verifying UBOs, source-of-funds, and ongoing transactions. This compliance cost typically exceeds the commercial return, driving most high-street banks to decline offshore applications outright.

Jurisdiction | Typical UK Bank Stance | Reason |

|---|---|---|

British Virgin Islands | Usually declined | Higher-risk offshore centre |

Cayman Islands | Usually declined | FATF-monitored jurisdiction history |

Cyprus | Case-by-case | EU jurisdiction, offshore structures scrutinised |

Hong Kong | Case-by-case | Increased scrutiny post-2020 |

UAE | Possible with full documentation | EDD required |

Seychelles | Usually declined | Common shell company jurisdiction |

Stances reflect general market practice based on FATF guidance on de-risking and FCA supervisory expectations. Individual bank decisions vary; this table is indicative, not exhaustive.

A legally incorporated offshore company with genuine trading activity can still be declined — the issue is bank risk appetite and compliance economics, not legality. FCA-regulated EMIs, purpose-built for international onboarding, are increasingly the primary route through which non-UK businesses access UK payment infrastructure.

How Fintech Infrastructure Enables Faster Payments Access

An FCA-authorised EMI can:

Hold client funds in safeguarded accounts separate from its own capital

Issue local collection accounts — virtual GBP accounts with unique UK sort codes — enabling offshore entities to receive GBP as if they were domestic businesses

Access UK payment rails as an indirect participant via a sponsor bank fintech arrangement

Offer multi-currency account infrastructure alongside domestic GBP capability

UK payment rails are the domestic clearing networks — Faster Payments, CHAPS, and BACS — that move GBP between accounts without international correspondent routing. EMIs connect via a sponsor bank that holds direct scheme membership and processes payments on the EMI's behalf.

Platforms such as Airwallex and Revolut Business use this model to connect one account to GBP via Faster Payments, EUR via SEPA, and USD via ACH — with the sponsor bank arrangement transparent to the end user.

Receive GBP from UK Clients Without a UK Bank Account

EQWIRE provides offshore and international businesses with local GBP account details connected to UK Faster Payments, enabling same-day settlement without SWIFT delays.

Real Use Cases for Offshore Faster Payments Access

Import and Export Companies — A Cyprus-registered trading company shares a local sort code instead of asking clients to wire internationally, enabling same-day FX conversion and goods release.

SaaS and Digital Platforms — An Estonia-incorporated software business billing UK subscribers directs customers to a local sort code, reducing failed payments and keeping revenue within the billing cycle.

E-commerce Businesses — Offshore merchants receiving payouts from Amazon UK or eBay collect GBP on the platform's standard schedule without international wire delays.

Freelancers and Independent Contractors — A developer or designer outside the UK shares a UK sort code; clients pay as they would any local contractor, with funds arriving the same day.

Top Providers Offering GBP Local Accounts for Non-UK Companies

Provider | UK Sort Code | Faster Payments | Multi-Currency | Offshore Onboarding | Regulatory Status |

|---|---|---|---|---|---|

Wise Business | Yes | Yes | 50+ currencies | Most jurisdictions | FCA-authorised EMI |

Airwallex | Yes | Yes | 60+ currencies | Variable by jurisdiction | FCA-authorised EMI |

Revolut Business | Yes | Yes | 25+ currencies | Limited for higher-risk | FCA e-money institution |

Payoneer | Yes | Yes | Yes | Freelancers and marketplaces | FCA-registered |

Yes | Yes | Yes | Built for offshore businesses | FCA-authorised EMI (FRN 901100) |

For BVI, Cayman, or Seychelles structures, the critical factor is whether the provider's compliance team handles EDD for that jurisdiction. Confirm eligibility before applying.

Choosing Infrastructure for International GBP Payments

Regulatory standing — verifiable on the FCA Financial Services Register. EMI authorisation means client funds are safeguarded and formal recourse exists if issues arise.

Payment rail connectivity — a platform connecting to Faster Payments, SEPA, SWIFT, and local rails eliminates the need for separate banking relationships per currency.

Compliance infrastructure — platforms with built-in EDD processes for complex offshore structures onboard international clients faster than those designed primarily for domestic businesses.

Operational integrations — API access and webhook notifications reduce manual reconciliation; programmatic transaction data retrieval is a significant efficiency gain for higher-volume operations.

Conclusion

GBP Faster Payments gives offshore companies a practical path to same-day GBP settlement — without a UK-resident entity and without SWIFT delays. An offshore company receive GBP same day via FCA EMI Faster Payments UK network: the EMI issues a virtual GBP account with a local UK sort code, connects to the rail via a sponsor bank, and makes the receiving experience functionally identical to a domestic UK bank transfer.

For import/export companies, SaaS companies, e-commerce companies, and independent contractors billing UK clients, this eliminates a longstanding pain point in their operations, with their clients unaware of any change, and the offshore business able to control the timing and method of conversion or utilization of the received GBP funds.

The key choice is determining the necessary infrastructure, including its regulatory, rail, and compliance requirements.

FAQ

Can I receive GBP payments internationally without a UK company?

Yes. An FCA-regulated EMI issues UK local account details in the name of the foreign business. UK clients send a standard domestic transfer; the offshore company typically receives funds the same day without a UK legal entity or UK bank account for a non-resident company.

How to get same-day GBP settlement as an offshore company?

Open a multi-currency account with an FCA-regulated EMI that provides UK Faster Payments connectivity. The EMI issues a virtual GBP account with a UK sort code and account number. UK clients pay via standard domestic transfer; funds typically settle the same day through the Faster Payments rail, with no SWIFT routing required.

Can an offshore company use UK Faster Payments?

Not directly — but it can open a virtual GBP account with an FCA-regulated EMI that accesses UK payment rails via a sponsor bank, receiving a dedicated UK sort code and account number for same-day GBP receipt.

How does an offshore business get same-day GBP settlement from UK clients?

Open an account with an FCA-authorised EMI providing a UK sort code connected to Faster Payments. UK clients send standard domestic transfers; funds typically settle within seconds to minutes regardless of the company's country of registration, though processing times may vary depending on the sending institution.

Can a non-UK business receive GBP via Faster Payments without a UK bank account?

Yes. An EMI participating in the Faster Payments network provides UK account details and handles settlement on the offshore company's behalf — no direct UK banking relationship required.

What is the difference between SWIFT and UK Faster Payments?

SWIFT routes through correspondent banks, typically taking 1–3 business days with fees deducted at each hop. Faster Payments is a domestic UK rail that typically settles within seconds, 24/7, with minimal costs and no intermediary deductions.

What compliance documents does an offshore company need to open a GBP account via an EMI?

Typically: certified corporate registration documents, a beneficial ownership register, proof of source of funds, and ID for directors and significant shareholders. Processing times range from a few days to several weeks depending on the platform, jurisdiction, and ownership structure complexity.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)