•

•

Multi-Currency Account for Law Firms: Segregated Client Funds UK

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

UK law firms handling cross-border clients have long faced a structural problem: SRA Accounts Rules require strict segregation of client money, but most high-street banks only offer GBP client accounts. A law firm receiving a €250,000 retainer in euros must either convert it immediately — losing 1.5–3% on the FX spread — or open a second account at a different institution and manage reconciliation across two systems.

A law firm multi-currency account solves this directly: it holds GBP, EUR, and USD in technically separate sub-accounts under a single master account, eliminating forced conversion and keeping audit trails consolidated in one place.

This article compares the three main provider types — high-street banks, FCA-authorised electronic money institutions (EMIs), and specialist fintech accounts — across the criteria that matter most to UK law firms: SRA compliance, audit-ready reporting, currency flexibility, and onboarding speed.

[aa key-takeaways]

Key Takeaways

Traditional banks, EMIs, and specialist fintechs offer fundamentally different multi-currency structures for UK law firm client money

SRA compliance depends on legal structure and technical setup — not just the provider's name or regulatory status

EMI accounts can legally hold segregated client funds when the provider is FCA-authorised and meets CASS safeguarding conditions

Audit-ready banking means per-transaction export with date stamps and currency separation — monthly PDFs do not satisfy SRA requirements in most scenarios

The right account depends on transaction volume, currencies needed, and SRA audit exposure

A trust accounting multi-currency account for law firm UK with client fund segregation requires sub-account-level technical architecture — not just a multi-currency wallet

[aa btn]Open a Law Firm Account[/aa]

[/aa]

What UK Law Firms Actually Need From a Multi-Currency Account

Not every account labelled "multi-currency" meets the legal standard for holding client funds. Understanding what the SRA actually mandates — and what "audit-ready" means in practice — is the prerequisite to evaluating any provider.

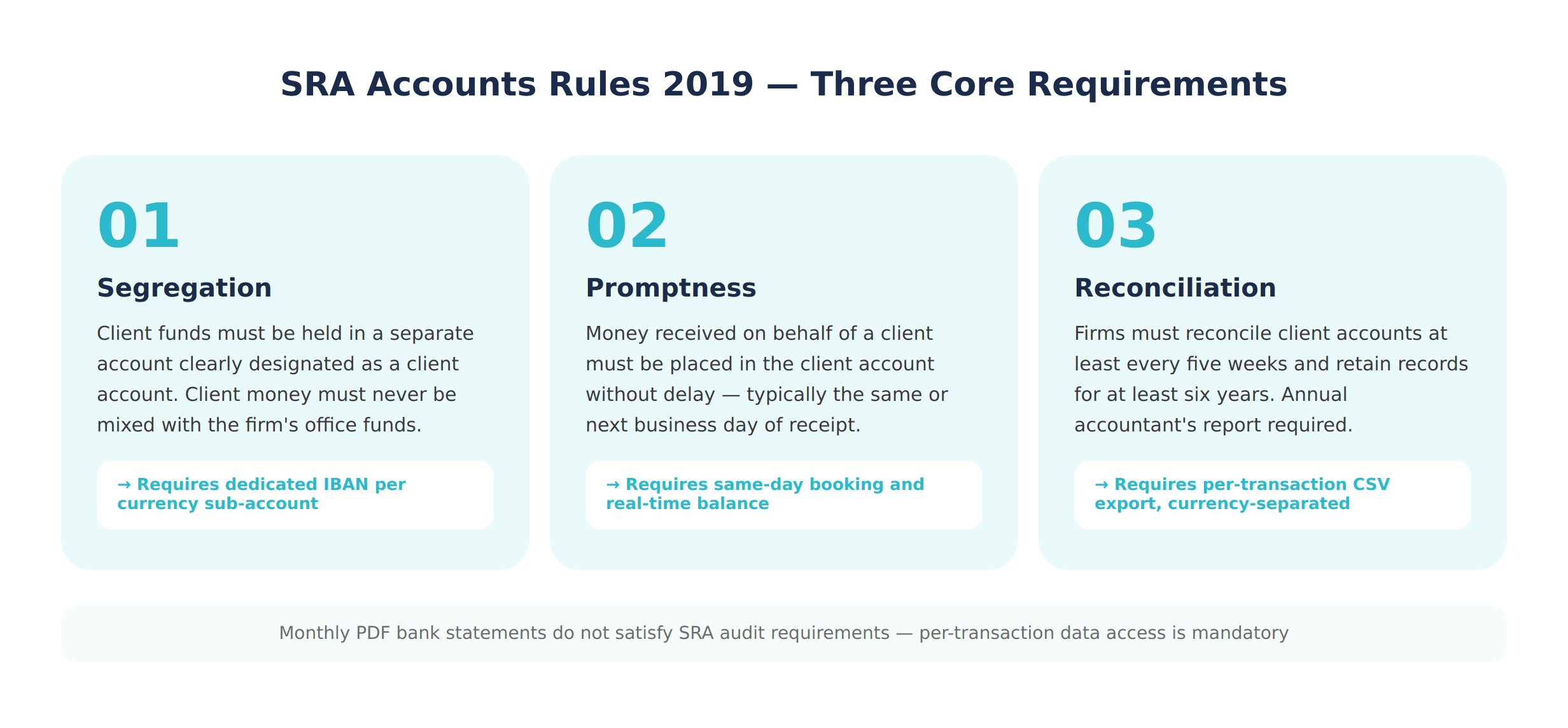

SRA Accounts Rules 2019 — The Non-Negotiables

The SRA Accounts Rules 2019 impose three core requirements on client money:

Segregation: Client funds must be held in a separate bank account, clearly designated as a client account. Client money must never be mixed with the firm's own office funds.

Promptness: Money received or paid on behalf of a client must be placed in a client account without delay — typically the same or next business day.

Reconciliation: Firms must carry out a client account reconciliation at least every five weeks and retain records for at least six years.

A client funds account UK segregated GBP EUR must satisfy all three — which means the account architecture itself must make commingling technically impossible, not merely impractical.

What "Audit-Ready" Actually Means

The term "audit-ready banking UK law firm" is used loosely by many providers. In practice, meeting SRA audit requirements means the account can produce:

Per-transaction records (not just end-of-day balances)

Date and time stamps for every credit and debit

Currency-separated statements — GBP transactions reported separately from EUR and USD

Exportable formats compatible with the annual accountant's report

Monthly PDF bank statements rarely satisfy these requirements. The SRA's annual accountant's report process requires the reporting accountant to test individual transactions — which means CSV or API-level data access, not a 12-page PDF summary.

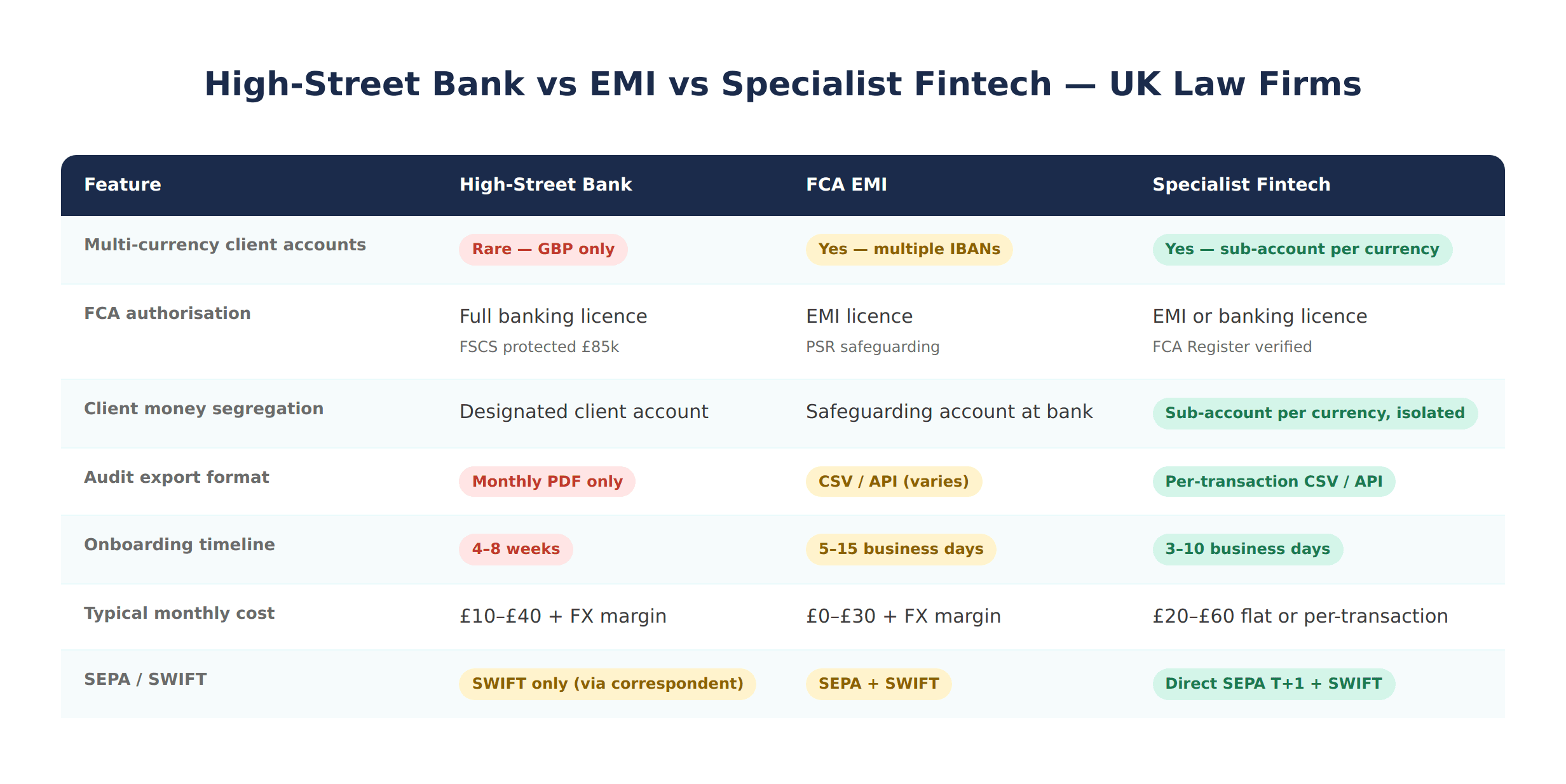

High-Street Bank vs. EMI vs. Specialist Fintech — Comparison for UK Law Firms

Here's where most firms make the wrong decision — choosing a provider based on brand familiarity rather than technical capability.

Feature | High-Street Bank | FCA EMI | Specialist Fintech |

|---|---|---|---|

Multi-currency client accounts | Rare — usually GBP only | Yes — multiple IBANs | Yes — sub-accounts per currency |

FCA authorisation type | Full banking licence (FSCS protected) | EMI licence (PSR safeguarding) | EMI or banking licence |

Client money segregation model | Designated client account | Safeguarding account at credit institution | Sub-account per currency, isolated |

Audit export format | Monthly PDF statements | CSV / API (varies by provider) | Per-transaction CSV / API |

Onboarding timeline | 4–8 weeks for law firms | 5–15 business days | 3–10 business days |

Typical monthly cost | £10–£40 + FX margin | £0–£30 + FX margin | £20–£60 flat or per-transaction |

SEPA / SWIFT | SWIFT only (via correspondent) | SEPA + SWIFT | Direct SEPA T+1 + SWIFT |

High-Street Banks — What They Offer and Where They Fall Short

Traditional banks carry real advantages for law firms: FSCS deposit protection up to £85,000 per institution, established relationship banking, and recognition by the SRA as approved client account holders.

The limitations are structural. Most UK high-street banks do not offer multi-currency client accounts as a standard product. A firm wanting to hold EUR client funds at a major UK bank will typically be told to open a separate account — which creates a reconciliation problem, not a solution. Onboarding is slow: law firms regularly report 6–8 week timelines due to enhanced due diligence requirements.

For firms with occasional foreign currency receipts and low transaction volumes, a high-street bank remains a defensible choice. For firms with regular EUR or USD client inflows, it is operationally inadequate.

EMI Accounts — When They Qualify for Client Money

The question "can a law firm use an EMI account for segregated client money UK?" has a nuanced answer: yes, under specific conditions.

Under the Payment Services Regulations 2017, an FCA-authorised EMI must safeguard customer funds in a designated safeguarding account held at a credit institution (a bank). This means the EMI holds client money in a ring-fenced account at a regulated bank — structurally similar to the segregation model required under SRA Accounts Rules 2019.

The key test is whether the account is clearly designated as a client account and whether the safeguarding arrangements satisfy the SRA's definition of an approved bank. Law firms should verify the provider's entry on the FCA Register and obtain written confirmation of its safeguarding model before using an EMI account for client money.

What this means in practice: an EMI that uses a Tier 1 bank as its safeguarding institution can provide a structurally compliant client account — with faster onboarding and better multi-currency architecture than most traditional banks.

Specialist Fintech Accounts — The Emerging Option

Purpose-built multi-currency accounts from FCA-regulated fintechs represent the most practical solution for law firms with regular cross-border client activity. The architecture is designed for exactly the use case SRA compliance demands: each currency (GBP, EUR, USD) is assigned a distinct IBAN within a single master account.

This sub-account model makes segregation technically enforced rather than procedurally dependent. Per-transaction exports are standard. SEPA and SWIFT transfers are supported natively, with settlement times of T+1 for SEPA and T+1–2 for SWIFT in most cases.

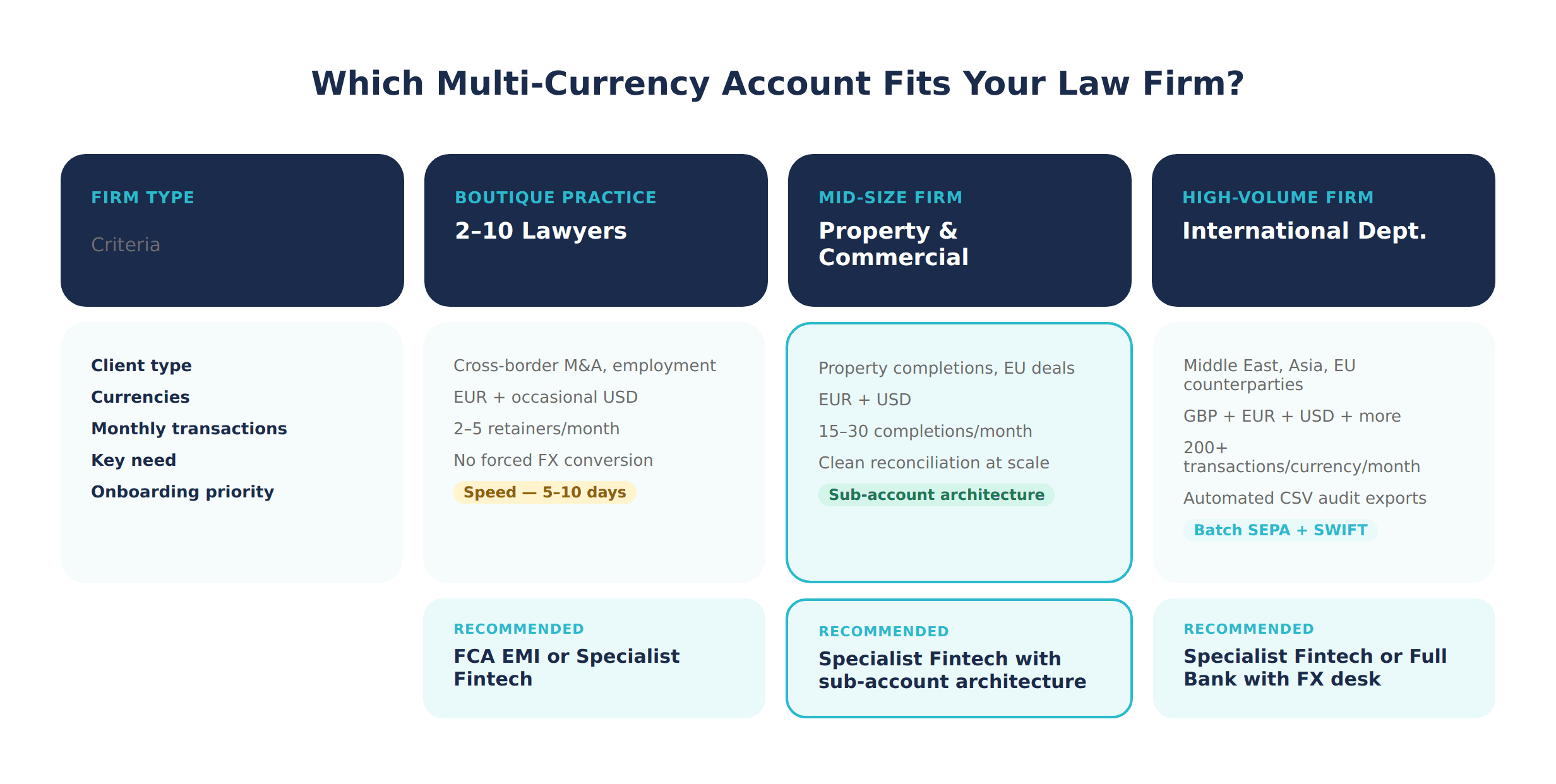

Use Cases — Which Account Fits Which Law Firm Type

Boutique International Practice (2–10 Lawyers)

Profile: A 6-partner firm specialising in cross-border M&A and employment law. Two or three international client retainers per month in EUR; occasional USD receipts from US-based clients.

Key needs: Fast onboarding, no forced FX conversion, simple reconciliation. The firm cannot afford a 6-week bank delay when a client engagement starts immediately.

Recommendation: An FCA-authorised EMI or specialist fintech. Onboarding in 5–10 business days. EUR client funds held in a dedicated EUR sub-account. Per-transaction exports satisfy the annual accountant's report without additional processing. Understanding how law firms open multi-currency accounts for segregated client funds UK is straightforward at this scale — documentation required includes SRA registration number, AML policy, and partner ID verification.

Mid-Size Firm With Property and Commercial Clients in EUR/USD

Profile: A 25-lawyer firm handling residential conveyancing for international buyers and commercial real estate transactions with European counterparties. Completion funds arrive in EUR; some sellers receive USD.

Key needs: Trust accounting UK multi-currency account with reliable reconciliation. Completion funds are time-sensitive — a delay at property completion is a serious client service failure. Reconciliation must be clean and auditable across 15–30 completions per month.

Recommendation: Specialist fintech with sub-account architecture. Receiving EUR directly into a designated EUR client sub-account — without conversion at point of receipt — eliminates FX risk and simplifies the per-transaction audit trail. Automated CSV exports are essential at this transaction volume.

High-Volume Firm With Regular SWIFT and SEPA Transactions

Profile: A 50-lawyer firm with a dedicated international department. Regular SWIFT receipts from clients in the Middle East and Asia, SEPA transfers to and from EU counterparties, monthly accountant's report covering 200+ client transactions per currency.

Key needs: Batch SEPA capability, SWIFT routing with competitive fees, transaction-level audit exports formatted for direct import into the firm's case management system. Audit-ready banking UK law firm at this scale means automated export, not manual data requests to the bank.

Recommendation: Specialist fintech or a full banking licence provider with FX desk support. SEPA costs typically run £0.20–£2.00 per transaction vs. £10–£30 for SWIFT, making direct SEPA access a meaningful cost difference at high volume.

[aa cta]

Find the Right Multi-Currency Account for Your Law Firm

FCA-regulated, GBP EUR USD sub-accounts, per-transaction audit exports — built for UK law firm client fund compliance.

[aa btn]Open a Law Firm Account[/aa]

[/aa]

How UK Law Firms Hold Client Money in GBP EUR USD With Audit-Ready Transaction Records

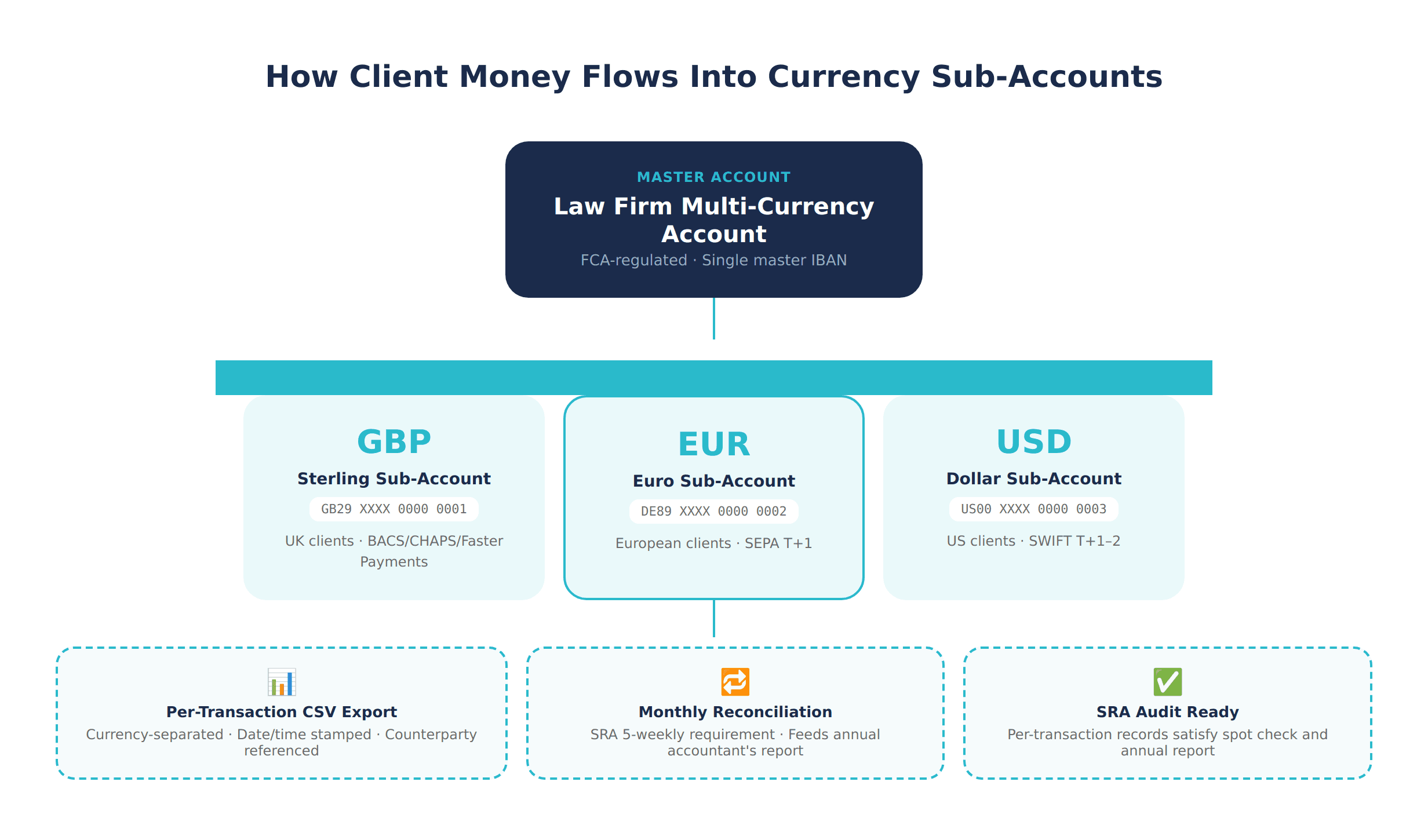

How UK law firms hold client money in GBP EUR USD with audit-ready transaction records comes down to account architecture. The sub-account model — one dedicated IBAN per currency under a single master account — is the technical foundation. Here is how it works operationally:

The law firm opens a multi-currency account with an FCA-regulated provider and configures sub-accounts: GBP, EUR, USD.

Each sub-account receives its own IBAN. The GBP IBAN is provided to UK clients; the EUR IBAN to European clients; the USD IBAN to US clients.

Incoming payments route directly to the correct sub-account. No conversion occurs at point of receipt.

The firm's case management system references the relevant sub-account IBAN for each client matter.

At month-end, the provider exports per-transaction CSV reports — one per currency — feeding directly into the five-weekly reconciliation and annual accountant's report.

The sub-account structure also makes it straightforward to demonstrate segregation during an SRA spot check: each currency sub-account is a distinct ledger, clearly labelled and independently reconcilable.

For the step-by-step: law firm multi-currency account for segregated client funds UK FCA EMI setup involves KYB documentation (SRA registration number, AML policy, director ID), account configuration, and safeguarding confirmation — typically completed in 3–10 business days with a specialist provider.

Trust Accounting Multi-Currency Account for Law Firm UK — Decision Checklist

A trust accounting multi-currency account for law firm UK with client fund segregation must satisfy regulatory requirements, operational needs, and audit standards simultaneously. Use this checklist when evaluating any provider.

# | Criterion | What to check |

|---|---|---|

1 | FCA authorisation | Verify on the FCA Register. Banking licence or EMI authorisation — confirm which. |

2 | Segregation model | Sub-accounts with individual IBANs per currency, not a shared pool with internal allocation |

3 | SRA designation | Can the account be formally designated as a client account under SRA Accounts Rules 2019? |

4 | Audit export format | Per-transaction CSV, currency-separated, with date/time stamp and counterparty reference |

5 | Reconciliation support | Export frequency (daily / on-demand), compatibility with your case management system |

6 | SEPA access | Direct SEPA participation or via correspondent bank? Direct is faster (T+1) and cheaper. |

7 | SWIFT capability | Supported currencies and corridors; typical settlement time; per-transaction fee |

8 | FX conversion control | Can the firm choose when to convert? What is the FX margin? |

9 | Onboarding timeline | Typical KYB completion time for law firms; legal sector onboarding track? |

10 | Safeguarding confirmation | For EMI providers: written confirmation of safeguarding bank and structure, for SRA records |

The checklist maps directly to the evaluation process for any multi-currency account for law firm UK GBP EUR USD audit-ready requirement. Items 1–4 are non-negotiable for SRA compliance. Items 5–10 determine operational fit and total cost.

[aa cta]

Open a Compliant Law Firm Multi-Currency Account

EQWIRE offers FCA-regulated multi-currency accounts with GBP, EUR, and USD sub-accounts and per-transaction audit exports — designed for UK professional services firms.

[aa btn]Get Started[/aa]

[/aa]

FAQ

Can a law firm use an EMI account for segregated client money UK?

Yes — but only under specific conditions. An FCA-authorised EMI can hold client funds if it operates a designated safeguarding account at a credit institution, as required under the Payment Services Regulations 2017. The key test under SRA Accounts Rules 2019 is whether funds are held in a separate account clearly designated as a client account. Law firms should verify the provider's FCA register entry and request written confirmation of its safeguarding model before using an EMI account for client money.

What is the difference between a client funds account UK and an office account?

A client funds account holds money belonging to clients — not the firm. Under SRA Accounts Rules 2019, these funds must never be mixed with office money (the firm's own funds). A client account must be held at an authorised bank or building society and clearly labelled as such. A multi-currency client funds account extends this model across currencies, holding GBP, EUR, and USD funds in separate sub-accounts to prevent commingling.

Multi-currency account for law firm UK GBP EUR USD audit-ready — what features are mandatory?

An audit-ready multi-currency account for a UK law firm must provide: (1) currency-separated sub-accounts with individual IBANs, (2) per-transaction exportable records — not monthly PDFs, (3) date and time stamps per transaction, (4) clear labelling of inflows and outflows by counterparty reference, and (5) export formats compatible with the annual accountant's report process. Monthly bank statements do not satisfy these requirements in most SRA audit scenarios.

How do law firms open multi-currency accounts for segregated client funds UK?

The process involves selecting an FCA-authorised provider, completing KYB onboarding with AML policy documentation, SRA registration number, and partner ID verification, then configuring separate sub-accounts per currency. How law firms open multi-currency accounts for segregated client funds UK typically takes 3–10 business days with a specialist fintech and 4–8 weeks with a traditional bank. Some providers offer dedicated legal sector onboarding with pre-configured client account structures.

Trust accounting multi-currency account for law firm UK with client fund segregation — how does it work technically?

A trust accounting multi-currency account for law firm UK with client fund segregation uses a sub-account architecture where each currency (GBP, EUR, USD) is assigned a distinct IBAN under a single master account. Incoming client funds route to the appropriate currency sub-account — they never pass through an office account. Reconciliation is performed against each sub-account separately, and the provider exports transaction records by currency for the firm's monthly SRA reconciliation and annual accountant's report.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)