•

•

Personal GBP Account UK for Non-Residents: Sort Code and Account Number

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Most UK high-street banks require a residential UK address before issuing a personal GBP account. For non-residents — expats, remote workers, and foreign nationals receiving GBP payments from UK clients — that requirement results in an automatic rejection. No UK address, no sort code, no Faster Payments access.

The alternative is an FCA-authorised Electronic Money Institution (EMI). Non-residents can open a personal GBP account UK non-resident through an EMI entirely online, with a real UK sort code, account number, and IBAN issued upon approval. No branch visit required.

This guide explains what a personal GBP account with a UK sort code is, who qualifies, how to apply, and what the account enables once active.

[aa key-takeaways]

Key Takeaways

Non-residents — including expats and foreign nationals — can open a personal GBP account in the UK through an FCA-authorised EMI, without a UK address

Upon approval, the account holder receives a UK sort code, an 8-digit account number, and a GB IBAN

The sort code + account number combination enables Faster Payments and BACS receipts — the same rails as UK bank accounts

The entire application and KYC process is completed online; no branch visit is required

EQWIRE issues personal GBP accounts with UK sort codes under its FCA EMI authorisation

For cross-border use, the GB IBAN enables international transfers via SEPA and SWIFT

[aa btn]Open an Account[/aa]

[/aa]

What Is a Personal GBP Account with a UK Sort Code?

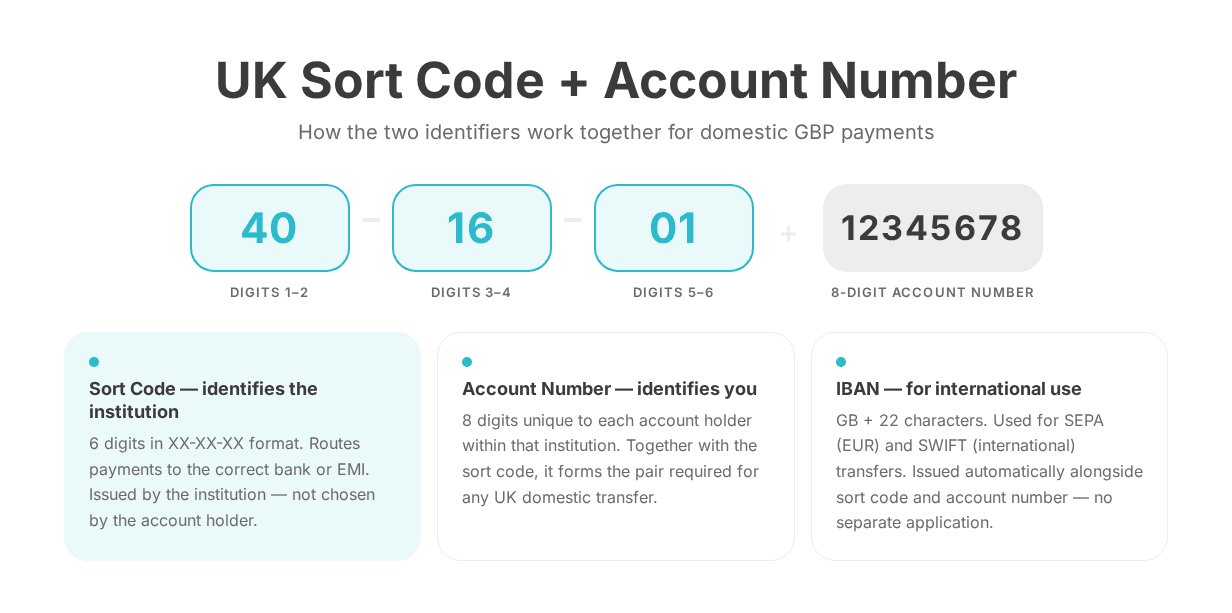

A personal GBP account in the UK has three identifiers: a sort code, an account number, and an IBAN. Each serves a distinct purpose, and the difference matters for non-residents receiving UK domestic payments.

The sort code is a 6-digit number in the format XX-XX-XX. It identifies the payment institution. The account number is an 8-digit reference identifying the individual account holder within that institution. Together, they form the pair required for UK domestic transfers.

The IBAN — formatted as GB followed by 22 characters — is used for international transfers: SEPA within Europe and SWIFT globally. For a UK client paying via Faster Payments, the sort code + account number is what is needed. The IBAN is relevant for cross-border GBP-to-EUR transfers from the same account.

[aa fast-fact]

Fast Fact: The Faster Payments Service (FPS) processes over 4 billion transactions per year in the UK, with near-instant settlement — typically within seconds, 24 hours a day.

[/aa]

Sort Code vs IBAN — What Each One Does

The sort code routes domestic UK payments: Faster Payments, BACS payroll, and CHAPS high-value transfers all use the sort code + account number pair. The IBAN is required for cross-border transfers.

Both identifiers are issued by FCA-authorised EMIs at account opening — there is no separate IBAN application. For a non-resident receiving UK client payments, the sort code functions identically to a bank-issued sort code from the sending party's perspective.

How Faster Payments Works with a UK Sort Code

The Faster Payments Service enables near-instant GBP transfers between accounts with valid sort codes — typically within seconds, 24/7. Payment limits vary by sending institution; most retail banks permit up to £1,000,000 per Faster Payment transaction.

BACS is a batch system used for payroll and direct debits, with a 3-business-day settlement cycle. For non-residents receiving regular GBP income from UK employers or contractors, a valid sort code and account number is all that is needed to be added to a payroll run.

Can a Non-Resident Open a Personal GBP Account in the UK?

Yes — but not through a traditional UK bank. High-street banks typically require a UK address, UK-issued proof of address, and in some cases a UK credit file. Non-residents rarely meet these criteria.

FCA-authorised EMIs operate under a different legal framework. The Electronic Money Regulations 2011 (SI 2011/99) and the Payment Services Regulations 2017 authorise EMIs to issue payment accounts — including personal accounts with UK sort codes — to customers regardless of residency, provided AML and KYC obligations are satisfied. A foreign residential address is acceptable.

[aa fast-fact]

Fast Fact: As of 2024, the FCA register lists over 200 authorised Electronic Money Institutions operating in the UK.

[/aa]

Legal Basis — FCA-Authorised EMIs vs Traditional Banks

The Electronic Money Regulations 2011 establish the regime under which EMIs are supervised by the FCA. Under this framework, an EMI may issue payment accounts — including personal accounts with a UK sort code — to any individual who satisfies its KYC and AML requirements. There is no statutory residency requirement.

Who Qualifies: Expats, Non-Residents, Remote Workers

Expats living outside the UK who receive GBP income from UK employers, pension providers, or clients

Freelancers and remote workers invoicing UK companies for services

Foreign nationals employed by UK entities who need a domestic GBP account for payroll

Individuals holding UK-sourced investments or rental income in GBP

[aa cta]

Open a Personal GBP Account with a UK Sort Code — No UK Address Required

EQWIRE issues personal GBP accounts to non-residents online, with a real sort code, account number, and IBAN under its FCA EMI authorisation.

[aa btn]Open an Account[/aa]

[/aa]

How to Open a Personal GBP Account Online Without a UK Address

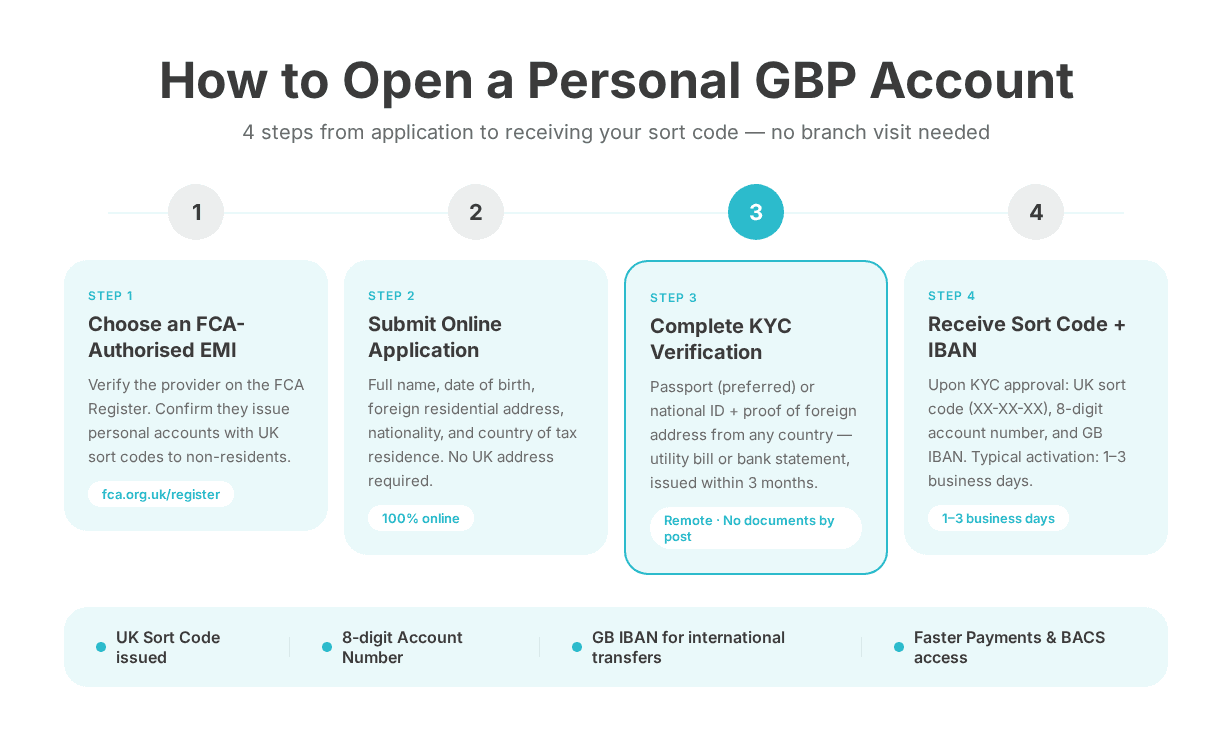

Opening a personal GBP account online UK no branch visit is a fully digital process through an FCA-authorised EMI. There is no requirement to post physical documents, visit a branch, or hold a UK address at any stage.

Step 1: Choose an FCA-Authorised EMI That Accepts Non-Residents

Confirm that the provider is listed on the FCA Register, offers personal GBP accounts with UK sort codes, and accepts applicants with foreign residential addresses.

Step 2: Submit the Application and Identity Documents Online

The application is completed on the provider's website. Standard information required: full name, date of birth, residential address (non-UK accepted), nationality, country of tax residence, and purpose of account.

Step 3: Complete KYC Verification

Government-issued photo ID: Passport preferred; national ID cards accepted from most jurisdictions

Proof of residential address: Utility bill, bank statement, or government document issued within 3 months — from any country

Source of funds / account purpose: A brief declaration

[aa fast-fact]

Fast Fact: JMLSG guidance — which FCA-regulated firms follow for AML compliance — does not require a UK address to verify customer identity. Foreign proof of address documents are fully accepted.

[/aa]

Step 4: Receive Sort Code, Account Number, and IBAN

Once KYC is approved, the account is activated. The holder receives a UK sort code (6 digits, XX-XX-XX format), an 8-digit account number, and a GB IBAN. Typical timeline: 1–3 business days from application to activation.

What You Can Do with a Personal GBP Account as a Non-Resident

A sort code + account number issued by an FCA EMI functions identically to a bank-issued account for UK domestic payment purposes.

Receiving Faster Payments and BACS

Faster Payments: near-instant, 24/7, typical limit up to £1,000,000 per transaction. BACS: 3-business-day settlement, used for recurring payroll and direct debits. CHAPS: same-day high-value transfers.

GBP to EUR Cross-Border Transfers

Once GBP is received, the account holder can hold GBP and EUR balances in the same account. For EU-based transfers, the GB IBAN routes via SEPA Credit Transfer (EUR) or SWIFT (GBP wire).

Conclusion

Non-residents can open a personal GBP account UK non-resident through an FCA-authorised EMI — legally, online, and without a UK address. The account provides a real UK sort code, account number, and GB IBAN.

FAQ

Can a non-resident open a personal GBP account in the UK with a sort code?

Yes. Non-residents can open a personal GBP account in the UK through an FCA-authorised EMI. Upon approval, the account holder receives a UK sort code, account number, and IBAN — no UK address required.

How do I get a UK sort code as a non-resident individual?

Apply online through an FCA-registered EMI, complete KYC using a passport and proof of foreign address, and the sort code is issued upon account activation.

Does a personal GBP account for expats include an IBAN?

Yes. FCA-authorised EMIs issue accounts with a GB IBAN alongside the sort code and account number.

Can I open a personal GBP account online in the UK without visiting a branch?

Yes. The entire application — including KYC verification and account activation — is completed remotely. No UK address or UK credit history is required.

What documents do I need to open a personal GBP account in the UK as a non-resident?

Government-issued photo ID (passport preferred), proof of residential address from any country (issued within 3 months), and information about the intended use of the account.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)