•

•

Business Account for Andorra Company UK: GBP and EUR Options

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

Key Takeaways

An Andorra-registered company may be able to access UK payment infrastructure, but in practice the more workable route is often a regulated electronic money institution (EMI) rather than a traditional high-street bank. Approval is always provider-specific and subject to onboarding, KYC, KYB, and risk review.

GBP and EUR are separate operating needs: UK-local GBP collection runs through Faster Payments; euro-denominated transfers across Europe run through SEPA.

Andorra uses the euro and sits within the SEPA geographical scope, but UK domestic GBP flows require UK rails, not SEPA.

Document readiness and beneficial ownership transparency are the two factors that most often determine whether an application progresses or stalls.

No UK office can still be workable through the right regulated provider setup, but provider eligibility is case-specific and should always be checked before applying.

Introduction

An Andorra-registered company invoicing UK clients faces a practical gap. The GBP invoice goes out. The client pays in sterling. But without UK-local receiving details, that payment may arrive less cleanly, take longer than expected, or move through more expensive international routing than necessary. The same business may also be paying European suppliers in EUR — and needing that process to be efficient, not expensive.

The question most Andorra-based businesses ask is whether a UK business account is even accessible. The more useful question is which type of provider and which payment rails actually solve the operating problem.

This guide is for Andorra-based SMBs, import/export businesses, SaaS companies, IT consultancies, and e-commerce businesses managing both GBP and EUR payment flows. It explains how a business account for Andorra company UK infrastructure can work in practice — covering GBP collection, EUR operations, account types, document requirements, and common approval blockers.

Can an Andorra Company Open a UK Business Account?

Possibly — in principle. The realistic route depends on provider type, business profile, and ownership transparency.

An Andorra company is not automatically excluded from accessing UK payment infrastructure. However, two different categories of provider approach this very differently.

Traditional UK high-street banks have historically preferred companies with UK-resident directors, local economic substance, or established UK business ties. That does not mean an Andorra company cannot apply to one — it means the probability of approval through that route may be lower for entities with no UK footprint.

Electronic money institutions, regulated by the FCA under the Payment Services Regulations and Electronic Money Regulations, are often the more practical route for foreign-registered businesses needing cross-border operating accounts. These providers are built for remote onboarding, operate across multiple currencies and rails, and generally have a higher operational fit for non-UK entities than traditional banks.

The key distinction is that an EMI-issued account is not a bank account in the deposit-taking sense. It is a payment account held in electronic money. This does not make it less functional for day-to-day business use — but it does affect the regulatory protections that apply, and it is important to understand that distinction before selecting a provider. The FCA’s safeguarding framework for EMIs and payment institutions is different from bank deposit protection.

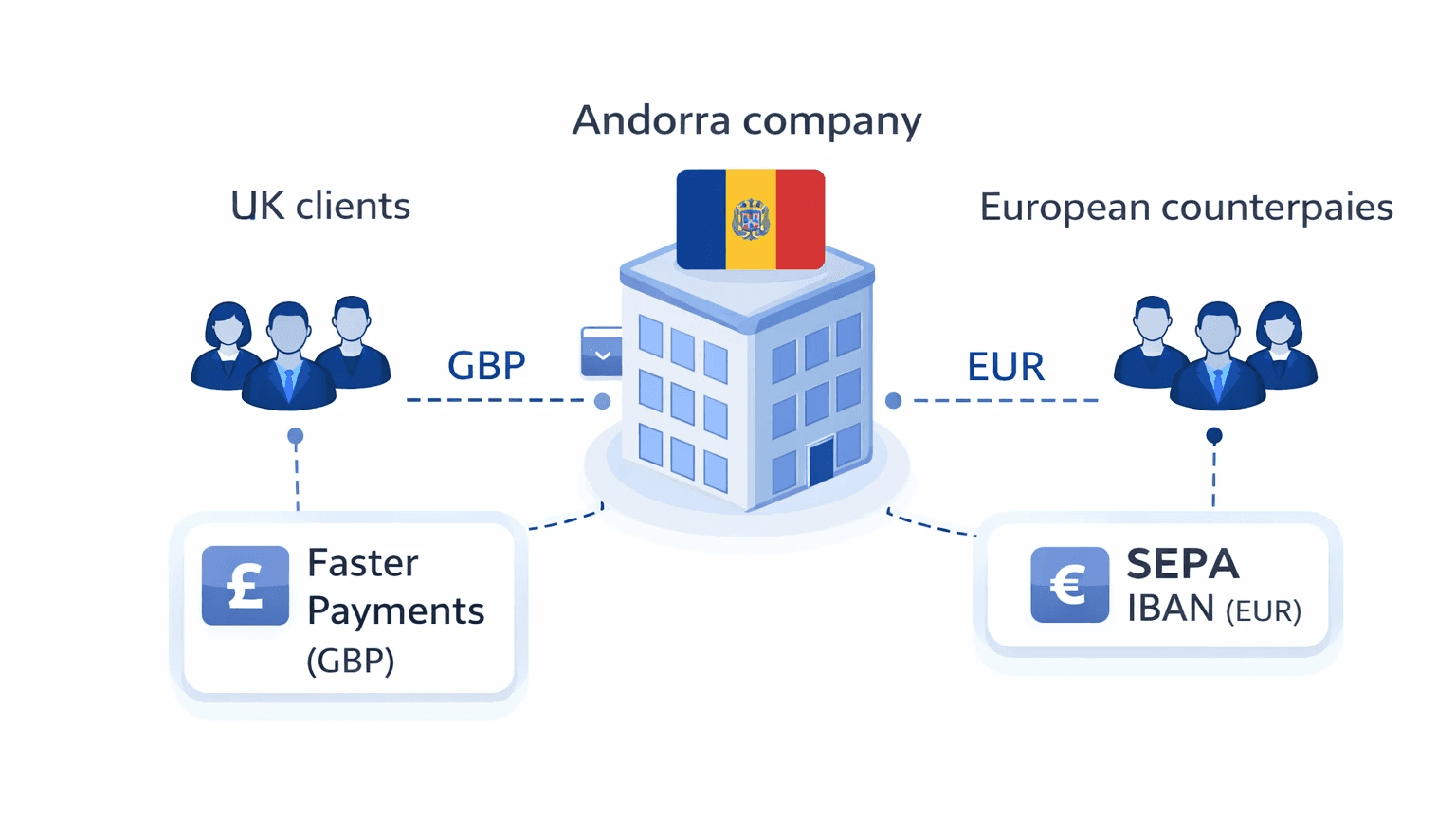

Consider two common examples. An Andorra-based consultancy invoicing UK clients in GBP needs UK-local receiving details so that clients can pay by domestic transfer rather than an international wire. An Andorra importer needs to receive GBP from UK buyers and then pay EUR to European suppliers. Both cases point to the same infrastructure need: a provider that can support GBP local details and EUR/SEPA capability together.

How a Business Account for Andorra Company UK Setup Works in Practice

A regulated provider onboards the Andorra entity, completes KYB and KYC, then issues account details for the supported currencies and rails.

The Andorra company does not join Faster Payments or SEPA directly. Access to those rails comes through the regulated institution’s own participation or scheme access model. The business receives account details that are usable within those networks — typically UK-local details for GBP and an IBAN for EUR — while the underlying scheme relationship sits with the provider. This is how many non-bank businesses access payment infrastructure in practice.

In practice, the setup looks like this:

GBP local details: a UK sort code and account number that allows sterling to be received via Faster Payments and, where supported, other UK payment methods. UK clients see local account details and pay in sterling through familiar domestic rails.

EUR account details: an IBAN that enables euro-denominated transfers to and from SEPA counterparties. EU suppliers, contractors, and platforms can be paid in EUR without relying on SWIFT for standard euro corridors.

Multi-currency operation: the business holds separate GBP and EUR balances and converts between them as needed, rather than converting every transaction on receipt.

The fact that the company has no UK office does not make this impossible. It makes provider selection more important. Not every EMI will onboard every entity type — but the right provider, with the right application, is where this kind of setup becomes workable.

What GBP and EUR Options Are Available for an Andorra-Registered Business?

The two core options are UK-local GBP receiving details and a SEPA-capable EUR IBAN — which can be held through one multi-currency setup or separately.

GBP: UK-Local Receiving Details

A UK sort code and account number allows an Andorra company to receive sterling from UK clients as a domestic-style payment. From the client’s perspective, they are paying local UK account details. There is no need to send a standard international wire for a routine GBP invoice, and the Andorra company receives GBP.

This is particularly valuable for businesses with recurring UK client relationships, marketplace settlements in sterling, or service invoices billed in GBP.

EUR: SEPA-Capable IBAN

A SEPA-capable IBAN allows an Andorra company to send and receive EUR across the SEPA area. Payments are standardised, typically lower-friction than SWIFT for euro corridors, and operationally better suited to routine EUR settlements. The ECB’s SEPA overview and the EPC’s SEPA geographical scope list are the clearest official references here.

Andorra participates in the SEPA geographical scope, which is why euro-denominated payment flows are a separate question from UK-local GBP collection. The two needs sit on different rails.

When a Multi-Currency Setup Makes Sense

Holding both GBP and EUR balances through one provider can reduce the friction of managing two separate institutions, two onboarding processes, and two compliance relationships. It also allows the business to decide when to convert — rather than being forced to convert on every transaction.

A UK customer pays a GBP invoice. The balance sits in GBP. An EU supplier invoice arrives in EUR. Rather than converting the GBP balance immediately at whatever rate is available, the business converts at a deliberate time, with full visibility of the amount and cost.

When SWIFT is still the right fallback: for payments to countries outside the SEPA area, or for currencies other than EUR and GBP, SWIFT remains the standard routing mechanism. A well-configured multi-currency account should support SWIFT outbound payments alongside Faster Payments and SEPA — not replace them entirely.

Payment rail | Best for | Currency | Typical speed | Main limitation |

|---|---|---|---|---|

Faster Payments | UK domestic business payments | GBP | Near real-time | UK domestic only |

SEPA | European euro transfers | EUR | Same day or next business day; instant where supported | EUR and SEPA geography only |

SWIFT | International and non-SEPA corridors | Multiple currencies | Variable | Higher cost and lower predictability |

Faster Payments vs SEPA: What Rail Does an Andorra Company Actually Need?

GBP domestic UK payments point to Faster Payments. EUR-denominated transfers across the SEPA area point to SEPA. These rails are complementary, not competing.

Faster Payments is the UK domestic sterling payment network. It processes transfers between UK accounts in near real time and operates day and night, 365 days a year. When a UK client transfers money to a sort code and account number, Faster Payments is often the rail doing the work.

SEPA covers euro-denominated transfers across the SEPA geographical scope. The ECB’s overview explains how SEPA standardises euro payments across participating countries and territories. Andorra is within that framework, but SEPA is not the same thing as UK domestic GBP infrastructure.

These two rails serve different currency and geographic contexts. A common misunderstanding is that SEPA handles GBP, or that Faster Payments solves EUR vendor payments. Neither is correct. Faster Payments is a sterling UK payment rail. SEPA is a euro payment framework.

For an Andorra company receiving from UK clients and paying European counterparties, both rails are typically needed. One handles the inbound sterling. The other handles outbound or inbound euros.

💡 Understanding both rails before choosing a provider saves significant friction later.

Businesses that need UK-local GBP collection and standardised EUR transfers often benefit from reviewing how each rail works before deciding whether a single multi-currency setup covers both needs.

→ GBP Faster Payments for Offshore Company: Same-Day Settlement Guide

UK Bank vs UK EMI: Which Route Is More Realistic for an Andorra Company?

For foreign-registered companies without UK presence, a regulated EMI is often the more realistic operational route.

The distinction matters both practically and legally.

A UK bank account is issued by a deposit-taking institution. A UK EMI account is issued by an electronic money institution regulated under the relevant UK payments and e-money framework. EMIs are not deposit-taking institutions — they hold client funds as e-money, which must be safeguarded in accordance with FCA requirements rather than protected in the same way as a standard bank deposit. That is an important regulatory distinction, but it does not make the account less functional for payments, collections, or FX operations.

Feature | Traditional UK Bank | UK FCA-Regulated EMI |

|---|---|---|

Regulatory framework | Deposit-taking institution | E-money / payment institution model |

UK presence often expected | Often, yes | Often not required |

Appetite for non-UK entities | Generally lower | Often higher, case by case |

GBP local receiving details | Yes, where approved | Yes, where supported |

EUR / SEPA capability | Varies | Common in multi-currency setups |

Remote onboarding | Less common | Common |

Onboarding complexity | High | Moderate to high |

The right choice depends on the business model, risk profile, and operating needs — not simply on which category sounds more familiar.

What Documents Does an Andorra Company Need to Open UK Account?

Exact requirements vary by provider, but the core file covers company formation, ownership structure, director and UBO identity, and a clear explanation of expected payment flows.

Document readiness is the most controllable factor in an onboarding outcome. Incomplete or inconsistent files are among the most common causes of application delays and rejections. The following checklist reflects what is typically required, not what any specific provider guarantees to accept:

Company documents:

Certificate of incorporation or equivalent registration evidence from Andorra

Articles of association or equivalent constitutional documents

Current register of directors and shareholders

Proof of registered address

Ownership and identity:

Full beneficial ownership (UBO) structure, documented clearly

Passport or national ID for each director and UBO

Proof of residential address for each director and UBO (utility bill, bank statement, or equivalent dated within 3 months)

Business activity and payment flows:

Website URL and description of business activity

Sample contracts, invoices, or commercial agreements

Explanation of expected transaction flows: which countries, which currencies, which counterparties, and approximate volumes

Source of funds or source of wealth documentation, where requested

Translated or certified copies may be required for Andorran-issued documents, depending on the provider. This should not be assumed as universal, but businesses should be prepared to provide certified translations if asked.

The business narrative — the explanation of what the company does, who it pays and receives from, and why it needs UK and EUR capability — is as important as the formal documentation. Providers assess both the documents and the coherence of the business model presented.

Step-by-Step: How to Open GBP and EUR Account for Andorra Registered Business

The process runs from defining the operating need through to testing the first live payment — and each step has a specific purpose.

Businesses that approach the process sequentially are usually better positioned than those who apply to multiple providers simultaneously without preparation.

Step 1 — Define the real use case

Establish whether the business needs UK GBP collection, EUR SEPA payouts, or both. This determines which providers are relevant and what account structure to request. A business that only needs EUR has different requirements from one managing dual-currency flows.

Step 2 — Choose provider type based on entity and risk profile

Assess whether a traditional bank or a regulated EMI is the more realistic route given the company’s ownership structure, industry, and operating geography. For many foreign-registered entities without UK presence, an FCA-regulated EMI is the more workable starting point.

Step 3 — Prepare the KYB/KYC file

Compile all documents listed in the previous section before beginning any application. Incomplete applications are a common and avoidable source of delay.

Step 4 — Explain ownership, activity, and expected flows clearly

Write a clear, consistent narrative covering what the business does, who the counterparties are, and why the account is needed. Providers conduct compliance reviews — a well-prepared narrative can accelerate that review.

Step 5 — Complete onboarding and compliance review

Submit documents and respond promptly to any additional information requests. Compliance review timelines vary by provider and application complexity.

Step 6 — Receive and verify account details

Once approved, verify that the issued details match what was requested — sort code and account number for GBP, and an IBAN for EUR, where supported.

Step 7 — Test before relying on the setup operationally

Send one small inbound GBP payment and one small inbound EUR transfer before routing real business volume through the account. This confirms the setup is functioning as expected before it matters.

Common Approval Blockers and Compliance Questions for Andorra Companies

The most common reasons applications stall are ownership opacity, flow inconsistency, and insufficient business substance signals.

Understanding these blockers in advance lets businesses address them before submission rather than after rejection.

Unclear beneficial ownership is one of the leading causes of delays. If the UBO structure involves multiple layers — holding companies, nominee arrangements, or indirect shareholders — the provider needs to understand the full chain of ownership. Documenting this clearly and proactively removes a major source of compliance friction.

Mismatch between described activity and expected flows is another common blocker. A company that describes itself as a consultancy but expects high-volume marketplace-style collections creates an inconsistency that compliance teams will flag. The business description and the expected transaction profile need to align.

Poor or absent business substance signals affect applications where the website is sparse, there are no visible contracts or commercial relationships, and the business model is difficult to verify independently. A functional website, sample commercial documents, and a coherent explanation of counterparties materially improve the quality of the application.

Incomplete or mistranslated documentation delays review, even when the underlying business is straightforward. Andorran company documents issued in Catalan may require certified translation depending on the provider.

Unclear source of funds is relevant where the business is new, where initial capitalisation is significant, or where the provider’s risk team requests additional information. Being prepared to explain the commercial origin of operating funds — client revenues, founder investment, or prior trading history — prevents this from becoming a blocker.

Who Benefits Most from This Setup?

The dual-currency, dual-rail setup is most useful for businesses that regularly move value between the UK and mainland Europe.

Import/Export Companies with UK buyers and European suppliers have the clearest use case. GBP comes in from the UK side via Faster Payments. EUR goes out to European counterparties via SEPA. Holding both balances can reduce unnecessary conversion and give the business control over FX timing.

SaaS and Digital Platforms billing UK customers in GBP but holding treasury reserves in EUR benefit from local collection without forced conversion. Subscription revenues arrive in sterling, and the business converts on its own schedule.

IT Service Providers and Consultancies issuing GBP invoices to UK clients while paying EU-based contractors or subcontractors in EUR may find that a single multi-currency setup replaces a fragmented arrangement of separate accounts and wire transfers.

E-commerce Businesses with UK marketplace settlements or UK customer bases and EUR operating costs — warehousing, logistics, software platforms — benefit from the same dual-rail model.

In each case, the value is not simply in having an account. It is in having the right rails available so that payments can move more like domestic transactions rather than through a slower, more expensive correspondent chain.

💡 Before applying, check provider fit, supported entity types, and document readiness.

For a comparable example of how provider eligibility and UK-local payment details are assessed for another offshore structure, see:

→ How a BVI Company Can Get UK Bank Details Without UK Presence

What Should an Andorra Company Check Before Choosing a Provider?

The right provider is the one whose supported entity types, rails, safeguarding model, and onboarding appetite match the actual business — not simply the one with the lowest fee.

Before selecting a provider, Andorra-registered businesses should review the following:

Supported entity type: not every EMI or payment provider accepts non-UK registered companies from all jurisdictions. Confirming that Andorra-incorporated entities are within scope saves time before beginning a formal application.

GBP local details: confirm that the provider issues genuine UK-local receiving details suitable for sterling collection. Actual UK-local payment details are what enable domestic Faster Payments settlement.

EUR account structure: confirm that the EUR account supports outbound SEPA Credit Transfers as well as inbound EUR receipts. Some providers support EUR receipt but have limited outbound SEPA functionality.

Safeguarding model: understand how client funds are held. FCA-regulated EMIs are required to safeguard relevant funds. The specific model differs from traditional bank deposit protection and should be reviewed before committing to a provider.

Onboarding appetite: some providers publish their accepted jurisdictions and entity types. Others assess on a case-by-case basis. Checking this before submitting a full application is a sensible step.

FX handling and fees: understand whether FX conversion is priced with a visible fee, a spread embedded in the rate, or both. For businesses converting regularly between GBP and EUR, this compounds over time.

The right setup is not the cheapest one or the most feature-rich one. It is the one that matches the business’s actual payment flows, entity structure, and compliance profile. An Andorra company with straightforward UK billing and EU supplier payments needs a provider that supports both rails reliably — and is prepared to review the entity on its own merits.

Conclusion

A business account for Andorra company UK use cases is not a purely theoretical question — it is a practical operating issue for Andorra-based businesses that invoice in GBP, pay in EUR, or manage both. The workable route for many of those businesses is not necessarily a traditional high-street bank, but a regulated provider that can support UK-local GBP receiving details and a SEPA-capable EUR setup within one multi-currency structure.

The key is to approach the process correctly: understand which rails are needed and why, prepare documentation that covers both company structure and payment flow context, and choose a provider whose onboarding appetite and account infrastructure match the business model. No UK physical presence is not always a barrier — but provider eligibility is always case-specific.

For Andorra companies managing UK client revenue and European operating costs, the dual-rail model — Faster Payments for GBP, SEPA for EUR — is often the most efficient structure to evaluate before falling back on SWIFT-only routing.

FAQ

Can an Andorra company open a UK business account?

Possibly, yes. The more realistic route for many Andorra-registered businesses is a regulated UK electronic money institution (EMI) rather than a traditional high-street bank. Approval depends on provider type, business profile, ownership transparency, and the outcome of the provider’s compliance review. No approval or eligibility can be guaranteed in advance.

How to open GBP and EUR account for Andorra registered business?

The process involves defining the operating need, selecting a provider with appetite for the entity type, preparing KYB and KYC documentation, submitting the application with a clear explanation of business activity and expected payment flows, completing the compliance review, and verifying the issued account details. Testing with a small payment before relying on the setup operationally is advisable.

Can an Andorra company access Faster Payments and SEPA from a UK EMI?

It may be able to, through the provider’s own payment infrastructure rather than through direct company membership in the schemes. The Andorra company receives account details that are usable within those networks, subject to what the provider supports.

What documents does an Andorra company need to open a UK account?

Typically: certificate of incorporation and constitutional documents, full beneficial ownership structure, passports and proof of residential address for all directors and UBOs, evidence of business activity, and an explanation of expected transaction flows including countries, currencies, counterparties, and volumes. Source-of-funds documentation may also be requested. Requirements vary by provider and risk profile.

Can an Andorra company receive GBP and EUR without UK physical presence?

No UK office can still be workable through the right EMI or payment account setup. Physical presence in the UK is not always required for accessing UK payment functionality through a licensed provider. However, eligibility is assessed case by case, and not every provider will onboard every entity type or jurisdiction.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)