•

•

UK Bank Details for BVI Company: How to Get GBP Sort Code Without UK Office

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

A BVI company incorporated in the British Virgin Islands — governed by the BVI Business Companies Act 2004 — faces a predictable problem when billing UK clients: how do you receive GBP locally, at speed, without paying avoidable FX conversion fees on every invoice?

Most traditional UK banks require a physical office, a UK-resident director, or both. For offshore companies operating internationally, that requirement closes off the obvious route — slower payments, higher costs, and confusion for UK-based clients expecting a familiar sort code and account number.

UK bank details for BVI company without UK presence are now accessible through regulated fintech infrastructure. This article explains exactly how that works, what documents you need, and how to get set up.

Key Takeaways

A BVI-registered company can have UK bank details, including sort code and account number, without the need for a UK office or resident director.

UK Electronic Money Institutions (EMIs) regulated by the Financial Conduct Authority (FCA) provide this infrastructure to offshore companies.

GBP sort codes route payments through the UK Faster Payments network, enabling near-instant domestic transfers.

Onboarding requires company incorporation documents, UBO verification, and business activity evidence — enhanced compliance checks apply.

BVI companies can also receive EUR via SEPA through European EMI partners, depending on the provider.

This infrastructure serves SaaS platforms, e-commerce sellers, consultancies, and import/export businesses billing UK clients.

Can a BVI Company Open a UK Bank Account?

A BVI company can acquire fully functional UK banking details, including a GBP account number, a UK sort code, and access to the Faster Payments network, without needing a UK address, resident director, or incorporation in the UK. This is done by passing through a regulated Electronic Money Institution (EMI) that is authorised by the FCA. These providers issue GBP sort codes and account numbers that connect to UK payment rails, enabling the company to receive GBP payments from UK clients just like any local business account.

EMIs vs Traditional Banks

The distinction matters. Traditional banks like Barclays or HSBC operate under full banking licences and typically require a UK business address, local directors, or demonstrable trading activity in the UK. EMIs operate under a different regulatory framework but provide genuine payment functionality:

Traditional Bank | UK EMI | |

|---|---|---|

UK physical presence required | Usually yes | No |

FCA regulated | Yes | Yes |

GBP sort code issued | Yes | Yes |

Faster Payments access | Yes | Yes |

Offshore company eligibility | Restricted | Typically supported |

Account opening timeline | Weeks to months | Days to weeks |

FSCS deposit protection | Yes (up to £85,000) | No (safeguarding applies instead) |

Electronic Money Institutions (EMIs) authorised by the UK Financial Conduct Authority are permitted to issue payment accounts and electronic money under the Electronic Money Regulations 2011, including UK sort codes and account numbers, to eligible business clients — including offshore entities such as BVI International Business Companies (IBCs).

How UK EMIs Provide GBP Sort Codes to Offshore Companies

An offshore company cannot join the UK Faster Payments Scheme directly — that requires a full UK banking licence. By holding an account with an FCA-regulated EMI that is a scheme participant, the company gains effective access to the same infrastructure. EMIs access Faster Payments, BACS, and CHAPS through direct membership or agency relationships with sponsor banks, then pass that access to their account holders under the Electronic Money Regulations 2011.

Under Regulation 21 of the EMR 2011 and FCA safeguarding requirements, client funds must be held in segregated accounts at authorised credit institutions. Platforms providing global payment infrastructure for offshore companies — including EQWIRE — operate within this model, offering multi-currency accounts with local payment details across multiple jurisdictions.

Regulatory note: EMI accounts are not bank accounts and are not covered by the Financial Services Compensation Scheme (FSCS). Client funds are protected through FCA-mandated safeguarding instead — meaningful protection, but different from the FSCS deposit guarantee up to £85,000.

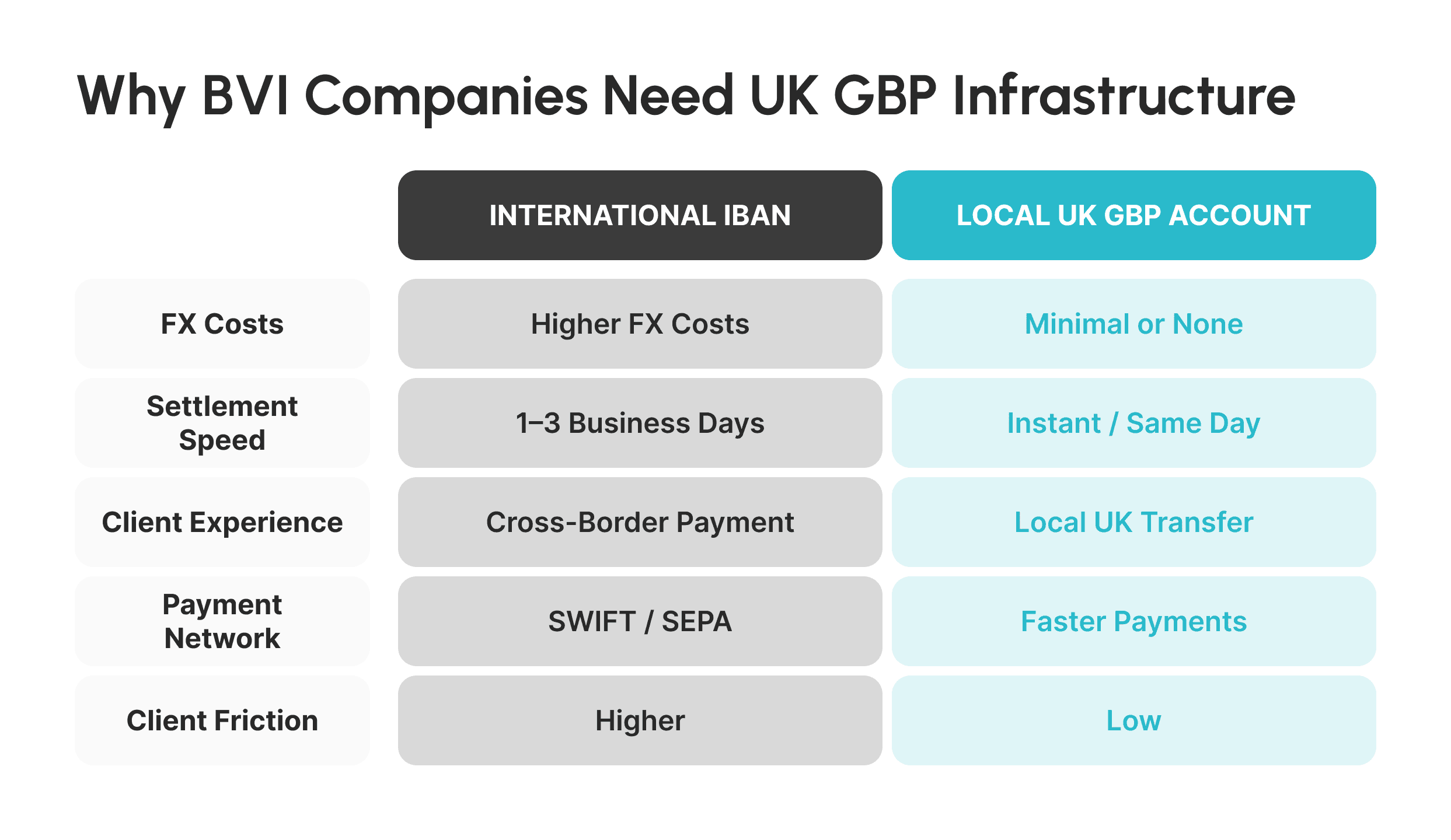

Why BVI Companies Need Local GBP Payment Infrastructure

For any UK business bank account for offshore company use case, the absence of local GBP infrastructure creates measurable costs. Every payment received in a foreign currency involves an FX margin — traditional bank FX markups commonly range from 1–3% above the mid-market rate, according to Wise's published cost analysis. For a company billing £50,000 monthly to UK clients, that adds up quickly.

Beyond cost, there are credibility and operational reasons:

UK clients prefer paying to a UK account. International IBANs or third-party payment processors can trigger hesitation or additional bank-side scrutiny. A UK sort code removes that friction entirely.

Settlement is faster. Faster Payments transactions typically complete within seconds, available 24/7 including weekends. Cross-border wires can take 1–3 business days.

Invoicing is cleaner. A sort code and account number on an invoice signals operational maturity to UK businesses and removes questions about where the money is going.

Common use cases for a GBP account for BVI company with no UK office:

SaaS companies billing UK clients on monthly or annual subscriptions

E-commerce sellers receiving GBP from UK marketplaces or direct customers

Consulting agencies invoicing UK businesses for project work

Import/export companies settling with UK-based suppliers or buyers

[Visual: Why BVI Companies Need UK GBP Infrastructure — Comparison chart showing FX cost, settlement speed, and client friction for international IBAN vs local GBP account] Alt text: Comparison table showing cost and speed differences between receiving GBP via an international IBAN and a local UK sort code account

What UK Bank Details Include (Sort Code Explained)

When asked to provide "bank details" from a UK business, they require an account number (eight digits), sort code (six digits that identify the financial institution and routing center, e.g., "04-00-75"), institution name, and confirmation of Faster Payments service eligibility.

The sort code determines how a payment routes through the UK interbank system, as defined by UK Finance. For a BVI company receiving GBP through a UK EMI, the flow is:

UK client's bank → Faster Payments Scheme → EMI's sort code → Your GBP account

Faster Payments settles the vast majority of transactions within seconds, around the clock including weekends — unlike BACS transfers, which run on a three-day cycle.

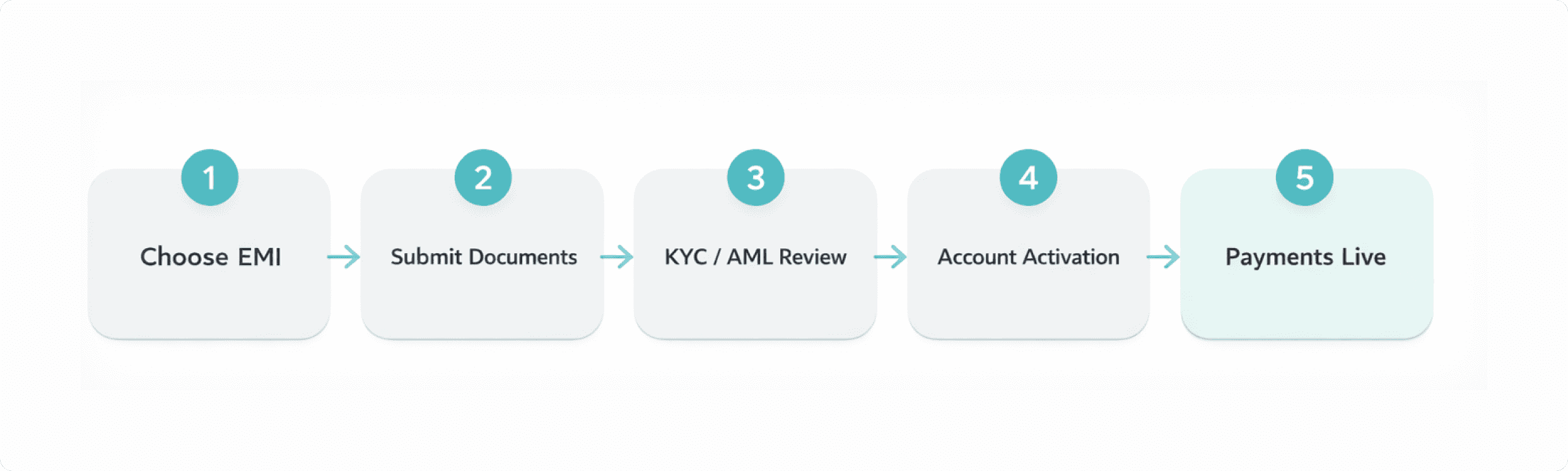

Step-by-Step: Opening a UK Payment Account for a BVI Company

The process is a structured compliance workflow. Regulated EMIs complete the onboarding process in five to fifteen business days, depending on the completeness of the documents and the complexity of the case.

Step 1 — Choose a Regulated EMI

Select a provider holding an FCA e-money institution licence or payment institution licence. This confirms the provider is authorised to issue payment accounts and access UK payment rails. For example, EQWIRE's infrastructure provides multi-currency accounts designed specifically for international and offshore businesses.

Step 2 — Submit Company Verification

You will be required to provide documentation that proves the existence of the company and the ownership structure:

Certificate of Incorporation (issued by the BVI Registry of Corporate Affairs)

Memorandum and Articles of Association

Register of Directors

Ultimate Beneficial Owner (UBO) Declaration – this is required if the individual owns 25% or more of the company and is in line with UK Money Laundering Regulations 2017

Step 3 — Compliance Review

EMIs have to comply with the Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017 and perform KYC checks on the entity and its beneficial owners. For offshore companies, there is an additional level of due diligence under Regulation 33. This is a routine requirement and not an indication that the offshore company is suspect. The source of funds, business type, geographic location, and volume are assessed.

Step 4 — Account Activation

Once the provider approves your application, you receive:

A GBP account number

A UK sort code

Access to a payment dashboard for managing transfers, statements, and currency balances

Step 5 — Payment Capabilities Go Live

From activation, the account typically supports:

Receiving GBP via Faster Payments from UK clients

Sending GBP domestically or internationally

International wire transfers via SWIFT

Multi-currency balance management

Documents Required for Offshore Company Onboarding

Offshore companies undergo enhanced due diligence as standard — more extensive than for UK-registered entities. Have the following ready before applying:

Company documents: Certificate of Incorporation · Articles of Association · Certificate of Good Standing (within 12 months)

Ownership documents: Shareholder register · UBO verification for each beneficial owner above 25% · Corporate structure chart (if layered ownership applies)

Identity documents: Valid passport · Proof of address (utility bill or bank statement, within three months)

Business activity documents: Active company website · Sample invoices or contracts · Description of services · Expected monthly GBP volume

The BVI Financial Services Commission does not restrict companies from opening payment accounts abroad, but individual EMIs apply their own policies. Confirm eligibility before starting your application.

How Faster Payments Works for International Businesses

Faster Payments for international businesses is one of the most practical advantages of a UK EMI account. The scheme operates instantly, 24 hours a day, 365 days a year, including bank holidays. The Faster Payments Scheme processed over 4 billion transactions in 2023, making it one of the world’s highest volume infrastructures for instant payments.

For BVI companies, this means UK client invoices settle within seconds regardless of when they are paid — no correspondent bank delays, no cut-off times. Most EMI accounts also support SWIFT wires for international transfers, giving a single account both domestic GBP speed and global reach.

Ready to Accept GBP Payments?

EQWIRE provides multi-currency accounts with local GBP sort codes, Faster Payments access, and SWIFT wire capability — built for international businesses operating without a UK presence.

Best Providers Offering UK Bank Details for Offshore Companies

Several regulated EMIs support UK bank account without UK address requirements for BVI and other offshore structures. Each provider differs on fees, onboarding speed, multi-currency capability, and compliance appetite for offshore entities.

Provider | FCA Regulated | GBP Sort Code | Offshore Company Support | Best For |

|---|---|---|---|---|

Wise Business | Yes | Yes | Limited / case-by-case | SMBs, freelancers, low fees |

Airwallex | Yes | Yes | Yes | SaaS, e-commerce, API-first |

Revolut Business | Yes | Yes | Limited / often declined | Startups, fast onboarding |

FCA-regulated infrastructure | Yes | Yes — built for offshore | International businesses, cross-border infrastructure, SMBs, freelancers, low fees, Fast Onboarding |

Key things to consider:

Compliance appetite — Not all EMIs support BVI companies. It is important to check if you're eligible before making an application.

Fee structure — Monthly account fees, FX conversion margins, and wire costs vary significantly across providers. Always compare total costs against your expected monthly transaction volume before applying..

Multi-currency and API — If you're looking to create EUR IBANs or need to automate payments, ensure that the provider supports local IBANs and has an API.

Note: This comparison reflects general product capabilities as of early 2026. Always verify current terms directly with each provider. Provider capabilities and onboarding policies vary depending on jurisdiction, ownership structure, and risk assessment. Always confirm eligibility directly with the provider before applying.

Can BVI Companies receive EUR via SEPA?

Yes — depending on the payment provider and their European licensing arrangements.

SEPA (Single Euro Payments Area) covers 36 countries and enables EUR transfers via IBAN within a shared clearing framework. To receive EUR via SEPA, a company needs an IBAN issued by a SEPA-member institution.

Some UK-based EMIs are FCA-authorised and have both FCA and EU e-money licences (or have an EU-licensed subsidiary), allowing GBP and EUR IBANs from the same account.

Some EU-based EMIs require that the company has a ‘nexus’ into the European market – i.e., a client base, contracts, or director based in Europe.

Post-Brexit, UK IBANs are not automatically SEPA-compliant. A separate EUR IBAN from an EU-licensed institution is typically required.

Providers like Airwallex and Wise Business issue EUR IBANs through their EU entities (Lithuania or Belgium) alongside UK GBP accounts.

Build Reliable Global Payment Infrastructure for Your Offshore Business

EQWIRE supports multi-currency accounts, local GBP and EUR payment details, and international wire transfers — designed for companies operating across borders without a local office.

Conclusion

A BVI company can obtain UK bank details — including a GBP sort code and Faster Payments access — without a UK office, resident director, or domestic incorporation. The route runs through FCA-regulated Electronic Money Institutions, which provide genuine UK bank account for non-resident company access under the Electronic Money Regulations 2011.

The process requires structured documentation and enhanced compliance review as standard. Once approved, the account enables faster GBP settlement, eliminates unnecessary FX conversion, and removes friction for UK clients.

For any BVI company seeking UK bank details for BVI company without UK presence, the infrastructure now exists across multiple regulated providers. The practical question is choosing one with the right geographic coverage, compliance track record, and payment rail access for your specific business model.

FAQ

Can a BVI company get UK bank details without UK presence?

Yes. A BVI-registered company can obtain UK bank details — including a sort code and GBP account number — through a UK Electronic Money Institution (EMI) regulated by the FCA. Traditional banks typically require a UK address or resident director, but EMIs can provide the same payment functionality to offshore entities following successful compliance review.

How do I open a UK payment account for a BVI registered company?

The process involves selecting an FCA-regulated EMI, submitting company and UBO documentation, passing an AML/KYC compliance review, and receiving your account details upon approval. Most providers complete onboarding within five to fifteen business days. Required documents include a Certificate of Incorporation, Articles of Association, Certificate of Good Standing, director and UBO identity verification, and evidence of business activity.

Can a BVI IBC receive GBP via Faster Payments?

Yes, provided the EMI holding your account is a member or sponsored participant in the UK Faster Payments Scheme. When the EMI has this access, GBP transfers from UK clients route through Faster Payments and typically settle within seconds, regardless of time of day or day of week.

What documents does a BVI company need to open a UK account?

Standard requirements include: Certificate of Incorporation, Articles of Association, Certificate of Good Standing, shareholder register, UBO passports and proof of address, and business activity documentation such as invoices, contracts, or a company website. Offshore companies typically undergo enhanced due diligence, so document quality and completeness directly affect processing speed.

Can a BVI company receive EUR via SEPA without EU incorporation?

In many cases, yes. Some EMIs hold EU e-money licences or partner with EU-licensed institutions, allowing them to issue EUR IBANs to offshore companies including BVI entities. However, certain EU providers require a demonstrated connection to the European market. The most practical solution for companies needing both GBP and EUR is a multi-currency account that consolidates both currencies under one provider.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)