•

•

EUR IBAN for Seychelles Company: How to Receive SEPA Payments Offshore

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

Introduction

For founders running a Seychelles company, one operational friction point tends to appear early: EU clients want to pay in EUR using a standard bank transfer — not a SWIFT wire. From the payer's side, initiating an international wire to a non-EU account involves extra steps, higher bank fees, and unfamiliar payment instructions. For a German or Dutch accounts-payable team accustomed to SEPA credit transfers, it can be enough to delay payment or prompt a request to invoice differently.

The question is whether a Seychelles International Business Company can hold a EUR IBAN and receive SEPA payments without relocating, reincorporating, or establishing a presence inside the EU. The short answer is that this setup is possible — but it depends almost entirely on which provider agrees to onboard the entity and under what compliance conditions.

This article explains how SEPA access works for offshore structures, what a EUR IBAN from a UK EMI involves, why Seychelles entities face higher-friction onboarding, and how to prepare a credible application. The goal is to help founders and finance operators make an informed decision before approaching any provider.

Key Takeaways

A Seychelles company can receive EUR via SEPA, but eligibility depends on the payment provider's onboarding criteria — not on incorporation jurisdiction alone.

UK FCA-authorised Electronic Money Institutions (EMIs) are the most commonly used regulated route for offshore entities seeking a EUR IBAN with SEPA access.

EMI accounts differ meaningfully from bank accounts: client funds are safeguarded in segregated accounts, not covered by FSCS deposit insurance.

Seychelles IBCs typically trigger enhanced due diligence (EDD) — not automatic rejection — and the quality of business substance documentation is the primary factor in approval outcomes.

GB-prefix IBANs issued by UK EMIs may encounter IBAN discrimination from some EU payers; this should be confirmed with any prospective provider before applying.

Choosing a regulated provider requires evaluating regulatory authorisation, SEPA scheme participation, safeguarding model, and stated eligibility criteria for offshore structures.

What Is a EUR IBAN — and Can a Seychelles Company Get One?

A EUR IBAN is a standardised account number denominated in euros, used to send and receive payments across the SEPA zone. SEPA — the Single Euro Payments Area — covers 36 countries, including all EU member states, the UK, Switzerland, and several others. SEPA credit transfers allow businesses and individuals to move EUR between accounts within this zone, with standardised settlement and lower transaction costs than international wires.

A Seychelles company can, in principle, hold a EUR IBAN — but the company's incorporation jurisdiction is not what determines eligibility. What matters is whether the payment institution providing the account is an authorised SEPA participant, and whether it will onboard a Seychelles entity under its compliance framework — the same principle that applies when opening a SEPA business account for a Caribbean company.

How SEPA Access Works — and Why Jurisdiction Is Not the Deciding Factor

SEPA access flows from the provider, not the client. If a regulated EMI is an authorised SEPA scheme participant, it can issue IBAN-formatted account details to eligible business clients — including offshore entities — and route incoming EUR payments through the SEPA rails.

This means a Seychelles IBC does not need an EU subsidiary, a European address, or a domestic EU bank account to receive SEPA payments. It needs to be onboarded by a regulated provider that is willing to accept it, has conducted the appropriate compliance review, and can issue a SEPA-reachable IBAN.

Bank Account or EMI Account: What Offshore Companies Actually Receive

Offshore business owners frequently conflate bank accounts with EMI accounts — these are structurally different products with different regulatory frameworks and client fund protections.

A traditional bank account is a deposit account. Banks are licensed to take deposits and lend, and in many jurisdictions, deposits up to a specified limit are covered by a national guarantee scheme — such as FSCS protection up to £85,000 in the UK.

An EMI account is an e-money account. The EMI does not lend client funds. Instead, it is legally required to safeguard those funds — holding them in a segregated account at a credit institution or in eligible liquid assets, separate from the EMI's own operational funds. This protects client balances in the event of the EMI's insolvency, but it is not deposit insurance and is not covered by FSCS.

Feature | Bank Account | EMI Account |

|---|---|---|

Account type | Deposit account | E-money account |

Funds lent by provider? | Yes (fractional reserve) | No |

Client fund protection | FSCS (up to £85,000 in UK) | Safeguarding (segregated funds) |

SEPA access | Where offered | Where offered |

Offshore entity eligibility | Generally lower | Varies by provider |

For a Seychelles IBC seeking to receive EUR from EU clients, EMI onboarding through a UK-regulated provider is generally the more accessible route. Traditional banks — particularly in the EU — have significantly narrowed offshore entity access in recent years due to AML regulatory pressure and correspondent banking de-risking.

Understanding this distinction matters when evaluating providers and when explaining the account structure to EU clients, auditors, or banking partners.

Why UK EMIs Are the Most Common Route for Offshore EUR Accounts

The UK is within the SEPA geographical area, and UK-regulated payment institutions can participate in SEPA credit transfer schemes. FCA-authorised EMIs continue to offer SEPA-connected infrastructure to business clients, including entities incorporated outside the UK and EU.

Some FCA-authorised payment institutions accept applications from offshore entities, subject to their own eligibility criteria and compliance screening. Authorisation status can be verified directly on the FCA's public register at fca.org.uk/register before engaging any provider.

IBAN Format and IBAN Discrimination — What to Confirm Before Applying

IBANs issued by UK EMIs typically carry a GB prefix. While these IBANs are technically SEPA-reachable, GB-prefix IBANs have in some cases encountered IBAN discrimination — where EU banks or corporate payment systems reject non-EU IBAN formats, contrary to EU SEPA regulations that prohibit such discrimination among SEPA participants.

This is a documented and practical issue, not a theoretical one. Before applying to any provider, Seychelles companies should ask specifically:

What IBAN format will be issued — and is it a GB-prefix or EU-prefix IBAN?

Has the provider identified any EU banking partners that have raised issues with their IBAN format?

Is there a fallback route if a specific EU payer cannot process the issued IBAN?

Some UK EMIs issue IBANs through correspondent arrangements with EU institutions, which may carry a non-GB prefix. Confirming this upfront avoids operational friction after the account is open.

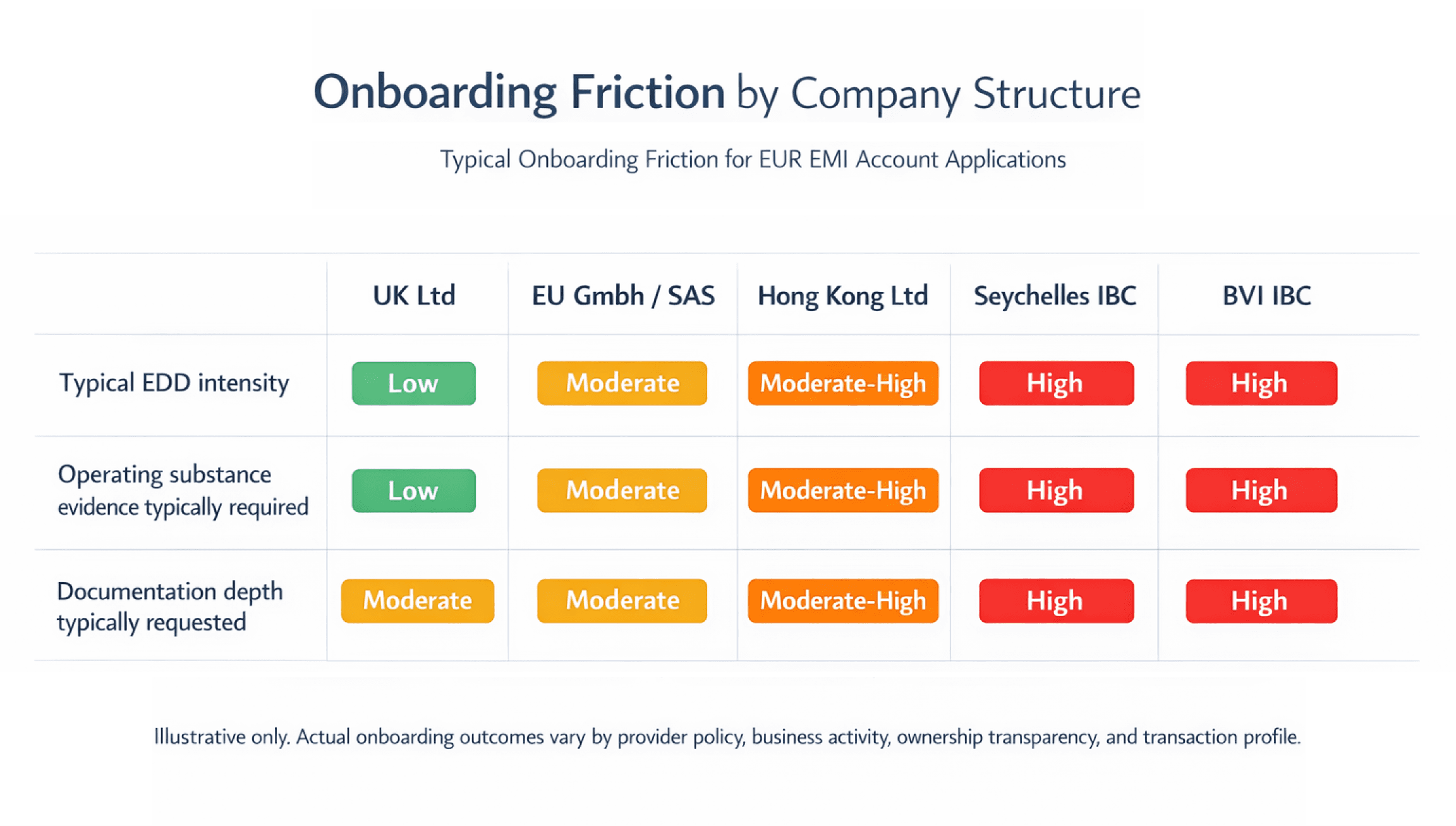

Why Seychelles Companies Face Enhanced Due Diligence — and How to Prepare

A Seychelles IBC is not automatically disqualified from opening a EUR account, but it will almost always trigger enhanced due diligence (EDD) at any regulated institution.

Several structural features of Seychelles IBCs drive this outcome:

Jurisdiction classification. The Seychelles appears on various international AML and tax transparency lists, which requires regulated providers to apply heightened scrutiny when onboarding entities from that jurisdiction.

Nominee structures. Many Seychelles IBCs use nominee directors or shareholders. This can obscure the beneficial ownership chain — a central concern for AML compliance teams.

Low domestic substance. Seychelles IBCs typically lack local staff, offices, or banking relationships, making it harder for providers to verify economic substance and operating purpose.

Limited verification channels. Providers cannot easily cross-reference Seychelles entities through accessible public registries or regulatory channels in the same way they can for UK or EU companies.

None of these factors are grounds for automatic rejection. They do mean, however, that the compliance review will go further than it would for a UK Ltd or a German GmbH — and that document preparation needs to match that standard.

Not sure whether an EMI account is the right route for your structure?

Understanding what a regulated EUR account involves — and what providers typically require — is a useful step before submitting any application. EQWIRE offers EUR SEPA accounts for international businesses, subject to compliance review.

What Documents a Seychelles Company Needs to Open a EUR IBAN

The documents required go well beyond standard formation papers. Providers need to understand not just that the company exists, but that it is an operational business with real clients, real transactions, and a legitimate reason to receive EUR via SEPA.

Corporate Structure Documents

Certificate of Incorporation

Memorandum and Articles of Association

Register of Directors and Register of Shareholders (certified copies)

Certificate of Good Standing (typically required within the last 3–6 months)

If nominee directors or shareholders are used: the Nominee Agreement and Declaration of Trust

Beneficial Ownership Documentation

Government-issued photo ID and proof of residential address for all Ultimate Beneficial Owners (UBOs)

Full corporate structure diagram showing the ownership chain down to natural persons

If UBO ownership runs through additional offshore entities: documentation for each intermediate layer

Business Substance Evidence

This is where many Seychelles IBC applications fall short. Compliance reviewers need to build a picture of the business: who owns it, who it serves, what it invoices, and why those funds flow in EUR. The more clearly that picture can be drawn from submitted documents, the more straightforward the review process becomes.

Clear written description of the company's services, client geography, and revenue model

Client contracts or service agreements, particularly with EU counterparties

EUR-denominated invoices

Bank statements from an existing account showing transaction history (where available)

Company website or verifiable online presence

For IT, SaaS, or consulting businesses: representative examples of deliverables or client correspondence (where available and appropriate)

Signatory and Operational Documentation

Authorised signatory documentation (if the account operator is not the UBO)

Power of Attorney (where applicable)

Source of funds declaration

What to Expect During the Compliance Review

Compliance reviews for offshore structures are typically more involved than for UK or EU-incorporated entities. Expect the possibility of additional document requests, extended review timelines, and questions about transaction volumes and counterparties. Providers may also conduct periodic document refreshes and ongoing transaction monitoring after account opening. Thorough document preparation upfront reduces the likelihood of delays during the initial review.

Common Reasons Applications Are Delayed or Declined

Most Seychelles IBC applications that fail do so because of insufficient business substance documentation — not solely because of the incorporation jurisdiction.

The most frequent blockers include:

Undisclosed or unclear nominee structures. If the compliance team cannot identify the natural person in ultimate control, the application will stall or be declined.

No existing transaction history. A newly incorporated company with no banking history and no contracts is difficult for a provider's risk team to assess. Even limited documentation of prior activity helps.

Vague business descriptions. "International consulting" without further detail is a common red flag. Providers want to understand the specific service, the client profile, and the expected payment volumes.

Mismatch between stated activity and evidence. A Seychelles company claiming to serve EU clients but unable to provide any contracts, invoices, or client references to support that claim creates a credibility gap.

PEP status or adverse media. If the UBO is a politically exposed person or has documented adverse media associations, EDD will extend significantly and may result in decline at some providers.

Addressing these issues before submitting an application materially reduces the likelihood of delays or additional information requests during compliance review.

How to Evaluate a Provider Before Applying

Not every payment institution accepts offshore company applications, and stated eligibility criteria vary significantly between providers. Before beginning any application, evaluate prospective providers against the following:

1. Regulatory authorisation (non-negotiable). The provider must be authorised by a credible financial regulator. In the UK, this means FCA authorisation as an Authorised Payment Institution (API) or Electronic Money Institution (EMI). Verify directly on the FCA register. In the EU, check the relevant national competent authority.

2. SEPA reachability (operational requirement). Confirm that the provider is a direct or indirect SEPA Credit Transfer scheme participant. Ask what IBAN format will be issued and whether EU corporate payers have encountered any routing issues with that format.

3. Safeguarding model (client fund security). Confirm how client funds are held. Regulated EMIs are required to safeguard funds separately from their own operational accounts. Ask which institution holds the safeguarded funds.

4. Offshore entity eligibility (provider-specific). Ask directly whether the provider accepts Seychelles IBC applications, what the typical document requirements are, and what the expected review timeline looks like. Providers with established compliance frameworks for offshore structures will be able to answer these questions clearly.

5. Multi-currency capabilities (where relevant). If the business also invoices in USD, GBP, or other currencies, evaluate whether the provider can support those payment rails alongside EUR SEPA. For UK-facing flows, access to GBP Faster Payments for offshore companies may be just as important as SEPA reachability. Confirm fee structures for both incoming and outgoing multi-currency transactions.

SEPA vs. SWIFT for EUR Collections: What Changes With a EUR IBAN

One of the core operational reasons Seychelles companies pursue a EUR IBAN is to replace SWIFT-based EUR collections with SEPA-compatible payment instructions.

A SWIFT wire to a non-EU account requires EU clients to initiate an international transfer — typically involving more steps, higher sender fees, and longer settlement times than a domestic payment. For a European SMB paying a regular service invoice, this adds friction that a SEPA transfer does not.

A EUR IBAN with SEPA access means the EU client can initiate the payment as a standard credit transfer. SEPA Credit Transfers typically settle within one business day under standard processing. From the payer's perspective, it functions like a domestic payment.

Whether this is worth pursuing depends on EUR invoice frequency and volume. For businesses with regular EUR billing cycles, SEPA access tends to reduce payment friction meaningfully. For occasional EUR receipts, a SWIFT-only setup may be adequate.

One point to confirm in advance: some EMIs charge fees for receiving SEPA transfers, while others do not. Fee structures differ by provider and should be reviewed before account opening.

Conclusion

A EUR IBAN for a Seychelles company is achievable through the right regulated provider — but it is not a commodity product available to any offshore structure without scrutiny. The determining factors are provider eligibility, compliance readiness, and the quality of business substance documentation.

Seychelles IBCs will face enhanced due diligence as a baseline. That is not a reason to avoid pursuing a EUR SEPA account — it is a reason to prepare thoroughly. Companies with clear beneficial ownership structures, demonstrable client relationships, and a coherent transaction narrative are in a stronger position to complete onboarding with an FCA-authorised EMI.

The practical route most accessible to offshore structures seeking a EUR IBAN with SEPA access runs through UK or EU-regulated payment institutions, not traditional banks. Understanding the difference between an EMI account and a bank account — and what safeguarding means in practice — helps set accurate expectations before any application begins.

Exploring a EUR IBAN for your Seychelles company?

EQWIRE is an FCA-authorised Electronic Money Institution offering EUR SEPA accounts, multi-currency infrastructure, and SWIFT access for international businesses, including offshore structures. Eligibility is subject to compliance review.

FAQ

Can a Seychelles IBC get a EUR IBAN with SEPA access?

Yes, in principle. A Seychelles IBC can obtain a EUR IBAN and receive SEPA payments if it is onboarded by a regulated payment institution — such as a UK FCA-authorised EMI — that accepts offshore entities and is an authorised SEPA scheme participant. Eligibility is determined by the provider's compliance criteria, not by the company's incorporation jurisdiction. Enhanced due diligence is standard for Seychelles structures and should be anticipated.

How do I open a EUR account for a Seychelles offshore company with a UK EMI?

The process typically involves submitting corporate formation documents, full beneficial ownership information, proof of identity for all UBOs, and evidence of real business activity — including contracts, invoices, and bank statements where available. The application then goes through a compliance review, which may include additional document requests. Timelines vary significantly depending on the provider and the complexity of the compliance review; offshore structures generally require a more thorough process than UK or EU-incorporated entities.

What documents does a Seychelles company need to open a EUR IBAN?

Core requirements include a Certificate of Incorporation, Memorandum and Articles of Association, a recent Certificate of Good Standing, full UBO identification documents, and a clear description of the business and its revenue model. Providers will also typically require evidence of existing business activity — such as client contracts, invoices, or bank statements — to assess business substance. Nominee arrangements must be fully disclosed, including the underlying Declaration of Trust.

Can a Seychelles company receive EUR payments via SEPA through a UK EMI?

Yes. UK EMIs that are authorised SEPA scheme participants can issue EUR IBANs to eligible business clients, including Seychelles IBCs, and route incoming EUR payments through the SEPA Credit Transfer scheme. Applicants should confirm with their provider that the issued IBAN is consistently accepted by EU corporate payers, particularly where a GB-prefix IBAN is involved.

What is the difference between a bank account and an EMI account for an offshore company?

A bank account is a deposit account; some bank deposits are covered by national guarantee schemes such as FSCS in the UK. An EMI account is an e-money account. The EMI does not lend client funds — instead, it is legally required to safeguard them in a segregated account separate from the EMI's own funds. This protects client balances in the event of EMI insolvency, though it is not the same as deposit insurance. For offshore entities, EMI onboarding is generally more accessible than traditional bank onboarding.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)