•

•

How to Pay UK Suppliers from a UAE Business Account

For UAE companies working with UK suppliers, international payments often become an unexpected operational cost centre.

A £10,000 supplier invoice sent through a traditional bank wire may arrive days later — and hundreds of pounds short — after FX spreads and intermediary deductions have taken their share. The supplier chases the shortfall. Your finance team reconciles the difference. The cycle repeats.

The good news: UAE businesses no longer need a UK bank account to send local GBP payments inside the UK. This guide explains exactly how to pay UK suppliers from a UAE business efficiently, what each method costs, and how modern payment infrastructure removes the friction from this corridor.

Key Takeaways

Traditional SWIFT transfers between UAE and UK accounts are slow, costly, and involve multiple intermediary fees

UAE businesses can send GBP locally inside the UK using Faster Payments rails — without needing a UK bank account or UK entity

For businesses holding GBP balances in advance, repeated FX conversions on each payment run are eliminated

Modern fintech rails offer same-day GBP settlement at a fraction of SWIFT's operational cost

Compliance documentation — invoices, AML checks, FCA-regulated safeguarding — is required regardless of payment method

What Is the Best Way to Pay UK Suppliers from a UAE Business?

The most efficient method is a multi-currency business account with a GBP balance and UK Faster Payments access. This allows UAE companies to send local GBP transfers inside the UK — bypassing SWIFT correspondent banking, eliminating intermediary fees, and enabling same-day settlement. No UK legal entity is required. The account is held with an FCA-authorised Electronic Money Institution (EMI), which issues a real UK sort code and account number. UAE businesses use these details to pay suppliers directly on domestic cross-border payment rails, just as a UK-registered company would.

Why UAE Businesses Need Efficient International Supplier Payments

The UAE is a major global import hub. Businesses regularly source goods, technology, and logistics from the UK — and payment friction hits margins directly.

Common scenarios where UAE companies need to pay UK suppliers from an overseas company structure include:

Import businesses purchasing from UK manufacturers or wholesalers

E-commerce companies paying UK 3PL providers for warehousing and fulfilment

Technology firms hiring UK developers, agencies, or SaaS vendors

Logistics operators settling freight and carrier invoices with UK counterparties

The real cost of a UAE to UK bank transfer via traditional banking includes more than the headline wire fee. According to the FSB's Annual Progress Report on Cross-Border Payments, approximately 25% of global payment corridors still exceed the G20's 3% total cost target.

For UAE businesses paying UK vendors, that cost typically breaks down as:

FX spreads of 1.5–4% above mid-market at traditional banks

SWIFT intermediary deductions of $25–$50 per transaction

Settlement delays of 2–5 business days

Limited or no real-time payment tracking

These aren't one-off issues. They compound across every payment run.

Three Ways to Send International Supplier Payments from UAE to UK

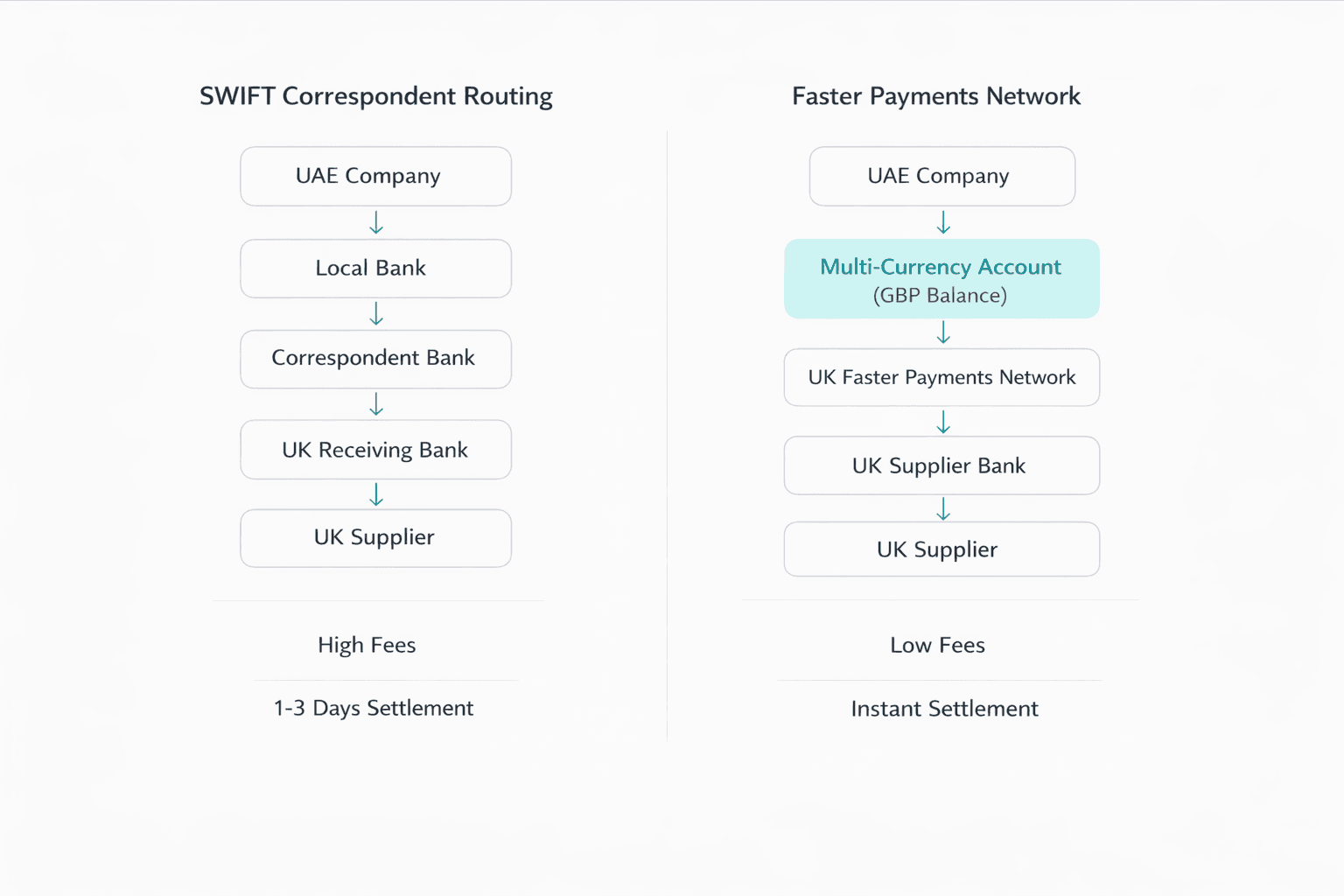

SWIFT and Correspondent Banking: How It Works and What It Costs

Most UAE businesses start here. Most eventually look for something better.

SWIFT is the messaging network most international banks use to coordinate cross-border payment rails for international wires. When a UAE business initiates a UAE to UK bank transfer, funds typically pass through one or more correspondent banks before reaching the recipient — each deducting its own processing fee without advance notice to either party.

Here's what makes correspondent banking expensive by design: there is no direct relationship between the UAE sending bank and the UK receiving bank. Intermediaries fill that gap — and charge for it:

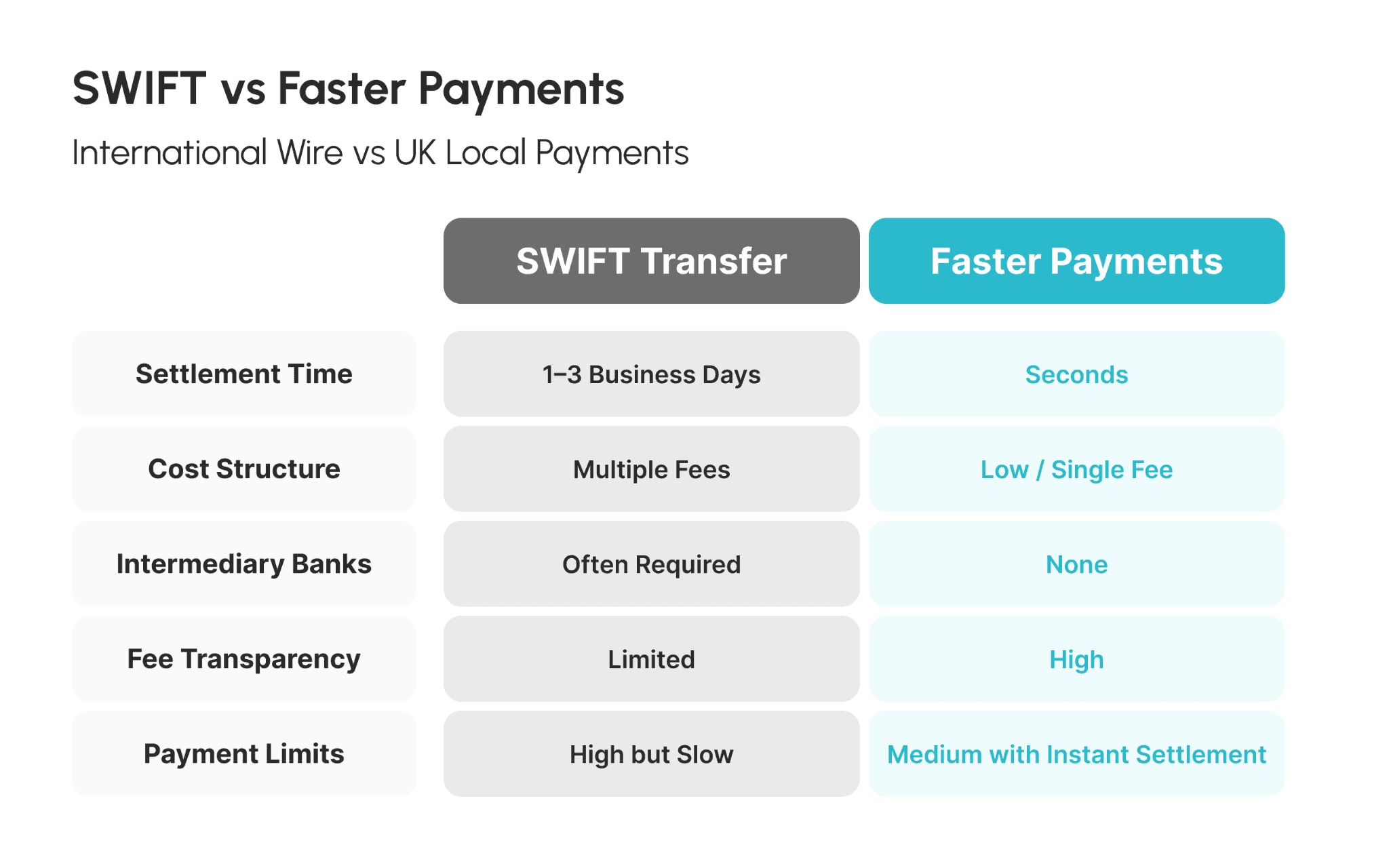

Total transfer cost of 2–5% of payment value

Settlement in 2–5 business days, longer if compliance checks trigger

Unpredictable deductions with no advance warning to either party

SWIFT still serves a purpose for large one-off transactions. For routine international supplier payments, it is the most expensive option available.

International Payment Platforms: Better Rates, Still Per-Transfer

A meaningful step up from bank wires — but not the full solution for high-volume businesses.

Fintech providers like Wise Business and Airwallex reduce costs by collecting funds locally and paying out from their own balance in the destination country — bypassing correspondent bank chains. FX rates sit closer to mid-market, fees are disclosed upfront, and settlement typically takes one to two business days.

The limitations become visible at scale:

Per-transaction fees that accumulate on high payment volumes

Transfer limits that restrict larger supplier invoices

Limited ERP and accounting system integration for finance teams managing multiple suppliers

GBP Accounts for Non-UK Companies: The Infrastructure Layer

This is where the operational equation changes fundamentally.

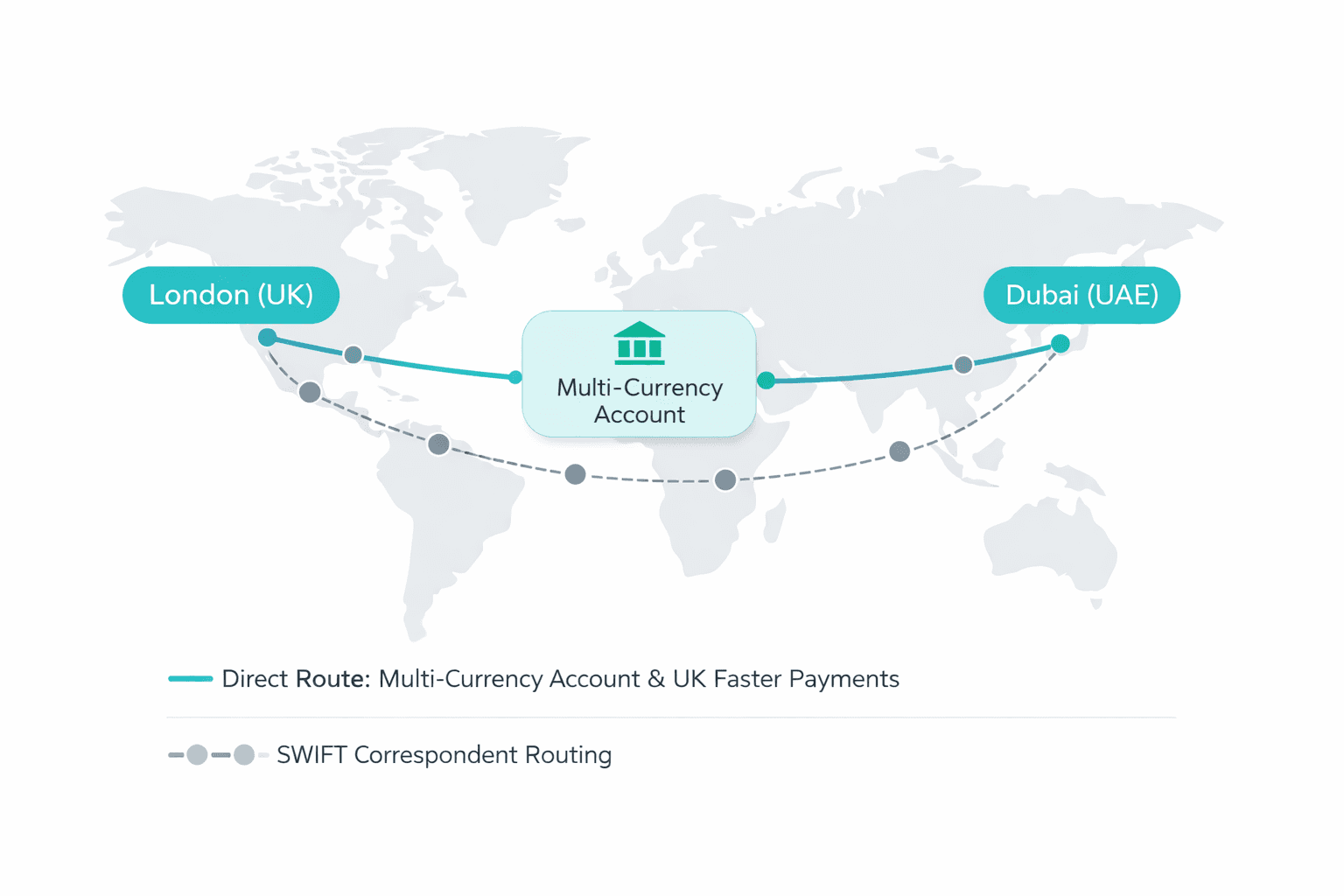

Multi-currency business accounts are the most operationally efficient infrastructure for UAE companies making regular GBP payments. They allow a business to hold AED, USD, GBP, and EUR within a single platform and instruct payments via local rails in each currency's home market. Crucially, a GBP account for non-UK companies — issued by an FCA-authorised EMI — provides a real UK sort code and account number, so suppliers receive funds as standard domestic transfers. Learn how to open a GBP account with a UK sort code as a non-UK company in our complete guide.

For UK international business payments from UAE, this means instructing transfers via UK Faster Payments or BACS — exactly as a UK-registered business would. The supplier receives a domestic transfer with no SWIFT involvement and no intermediary deductions. For businesses holding GBP balances in advance, this eliminates repeated FX conversions on each payment run, making it the most cost-efficient solution for sending GBP to UK suppliers from a UAE account on a recurring basis.

Step-by-Step: How to Send GBP to UK Suppliers from a UAE Business Account

Step 1: Hold Funds in Multiple Currencies

Before you can pay suppliers efficiently, you need the right account structure.

The foundation is a multi-currency account supporting at least AED, USD, and GBP balances. Opening a GBP account with a UK sort code as a UAE company is now possible through regulated EMI providers — no UK entity required.

Holding GBP in advance means converting at a time you choose rather than at the moment each invoice arrives — reducing total annual FX cost materially for businesses with predictable UK payment volumes.

Step 2: Convert Currency Transparently

Not all FX rates are equal. The number to watch is the FX spread: the gap between the mid-market rate and what your provider actually applies.

Traditional bank FX desks: 1.5–3.5% above mid-market

Fintech platforms: typically 0.3–1%, often with a disclosed flat fee

Always confirm the exact rate and total cost before confirming a conversion.

Step 3: Send Local GBP Payments Inside the UK

This is the step that eliminates SWIFT entirely.

Once funds sit in a GBP balance, the business instructs transfers via domestic UK payment rails:

Faster Payments: Settle within seconds, available 24/7. Individual banks set their own transaction limits, which typically range from £250,000 to £1,000,000 per payment. According to Pay.UK, the network processed 5.09 billion transactions worth £4.2 trillion in 2024, making it the UK's primary real-time domestic payment rail.

BACS: Three-day batch processing for regular supplier settlements and payroll

CHAPS: Same-day settlement for high-value transactions, with a per-transaction fee

The ability to replace SWIFT with Faster Payments for UAE to UK supplier payments is the most significant operational upgrade available to import and e-commerce businesses. A UAE company instructing a Faster Payments transfer via a GBP account reaches the UK supplier's account within seconds — with no intermediary deductions and the full payment amount received.

Step 4: Track, Reconcile, and Build International Treasury Infrastructure

Modern multi-currency platforms provide payment confirmations, reference numbers, and real-time status for every transfer — downloadable receipts, API integration with Xero or QuickBooks, and automated invoice matching.

As supplier networks expand beyond the UK, this same infrastructure supports broader international treasury operations across regions and currencies.

How Much Does It Cost to Pay UK Suppliers from UAE?

Cost queries are often what bring businesses to this topic. Here is what a UAE to UK bank transfer actually costs across each method — using a £10,000 payment as a reference point.

Transfer Type | Estimated Cost on £10,000 | Settlement Time |

|---|---|---|

Bank SWIFT wire | £200–£500 (fees + FX spread) | 2–5 business days |

Fintech transfer (Wise, Airwallex) | £50–£120 (flat fee + reduced spread) | 1–2 business days |

Local GBP via Faster Payments | £0–£20 (account fee only) | Same day, often seconds |

These figures reflect typical ranges — actual UAE to UK bank transfer fees vary by provider, account type, and transaction size.

The highest hidden cost in SWIFT transfers is the correspondent bank deduction — a direct consequence of how correspondent banking costs work. Here is what that looks like in practice:

A UAE business sends £5,000 to a UK supplier. The supplier receives £4,850. Three intermediary banks deducted their fees along the route — and neither party was told in advance.

SWIFT vs Faster Payments is not just a speed comparison — it is a structural cost difference. SWIFT routes payments through a chain of intermediary banks, each adding latency and fees. UK Faster Payments uses direct settlement across cross-border payment rails that connect the GBP account to the UK banking system, with no intermediaries between sender and recipient.

For businesses evaluating the cheapest way to send GBP to UK suppliers, the decision comes down to frequency:

Occasional transfers: fintech platforms offer a good cost-convenience balance

High-frequency payments (weekly orders, recurring invoices, contractor retainers): local GBP rails are the only operationally viable option

How Multi-Currency Accounts Replace SWIFT for Recurring UK Supplier Payments

Multi-currency accounts address the full operational stack, not just the transfer mechanism. For a UAE company paying UK contractors from an offshore business structure, the benefits extend beyond per-transfer cost.

Local payment rails mean suppliers receive domestic transfers — no deductions, no processing delays. Automated reconciliation matches outbound payments to invoices automatically, reducing manual accounts payable work for high-volume operations.

Reduce UK Supplier Payment Costs by up to 80%

Open an EQWIRE multi-currency account to hold GBP balances, send UK payments in seconds, and eliminate intermediary bank deductions.

Compliance Considerations for Cross-Border Business Payments from UAE

The payment method changes. The compliance obligations don't.

AML verification is mandatory for platforms facilitating international transfers — required under both UAE Central Bank regulations and the UK's FCA framework. Before the first transfer to a new supplier, verify their registered company name, UK sort code and account number, and request a copy of their company registration or a recent invoice with banking details.

Retain the purchase order, supplier invoice, payment confirmation, and bank statement for tax and audit purposes. Payment providers operating in the UK must comply with FCA safeguarding rules for Electronic Money Institutions — client funds are held in segregated accounts at authorised credit institutions, ring-fenced from the provider's own capital. Confirm your provider's safeguarding arrangements before transferring operational funds.

Choosing the Right Payment Infrastructure for Global Businesses

Not all multi-currency accounts are equal. Here's what separates providers for UAE to UK supplier payment operations:

GBP access via UK rails: The provider should hold its own FCA-licensed GBP account — not route through a correspondent arrangement

Payment speed: Same-day Faster Payments capability is essential for time-sensitive supplier invoices

FX transparency: Mid-market rates with a disclosed spread, not opaque "transfer rates" with embedded margin

Integration: API connectivity and accounting software sync eliminate manual reconciliation at scale

Currency coverage: Infrastructure supporting EUR (SEPA) and USD (ACH) scales as supplier networks expand

Manage UAE to UK Supplier Payments from One Platform

Access GBP Faster Payments, transparent FX rates, and multi-currency account infrastructure — purpose-built for internationally operating businesses.

Conclusion

The question of how to pay UK suppliers from a UAE business account has a clear operational answer in 2026: multi-currency infrastructure with local GBP rail access.

SWIFT is not broken — it is simply designed for a different era, and a different transaction frequency. For UAE businesses making recurring payments to UK vendors, the cost, speed, and transparency gap between traditional bank wires and modern payment rails is too large to ignore.

The businesses that move first — establishing GBP account infrastructure, eliminating SWIFT intermediaries, and automating reconciliation — absorb less cost, pay suppliers faster, and build the financial foundation to scale their supplier network without rebuilding their payment stack at every step.

FAQ

What is the best way to pay UK vendors from a UAE business bank account?

The most cost-effective approach is a multi-currency account that holds GBP and accesses UK Faster Payments directly. This eliminates SWIFT intermediary fees and repeated FX conversion costs. For occasional transfers, regulated fintech platforms like Wise Business or Airwallex offer better rates than traditional bank wires.

Can a UAE company open a GBP account without a UK entity?

Yes. FCA-authorised Electronic Money Institutions issue GBP accounts — including a real UK sort code and account number — to non-UK registered companies. UAE businesses can send and receive GBP via Faster Payments, BACS, and CHAPS without a UK office or UK-resident director. See our full guide on GBP accounts for non-UK companies for the complete onboarding process.

How long do payments from UAE to UK typically take?

SWIFT transfers take two to five business days, often longer when compliance checks are triggered. Fintech platforms settle in one to two days. Payments via UK Faster Payments — instructed through a multi-currency GBP account — arrive the same day, often within seconds during UK banking hours.

What is the UK Faster Payments limit for business transfers?

Individual banks and EMI providers set their own limits, which typically range from £250,000 to £1,000,000 per payment. CHAPS is the appropriate rail for transfers that exceed these thresholds, offering same-day settlement with no upper value limit.

How can businesses send GBP to UK suppliers without SWIFT fees?

Hold GBP in a multi-currency account and instruct UK Faster Payments transfers directly to the supplier's bank account. This removes all correspondent bank intermediaries. For businesses making frequent UK supplier payments, a dedicated GBP account with Faster Payments access delivers the greatest long-term cost reduction.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)