•

•

PSP Settlement into a Multi-Currency EMI Account: How It Works

Many businesses using Stripe, Adyen, or PayPal end up with settlement balances accumulating across multiple dashboards, paying out in different currencies to different accounts. The result is fragmented cash visibility, unnecessary FX conversion, and a reconciliation process that closes too slowly.

Routing PSP settlement into a multi-currency EMI account is one approach to consolidate that flow — but it works only when specific conditions align across payout-account validation, settlement currency support, legal-entity matching, and receiving-account format. This article explains the routing logic, where FX still occurs, and how finance teams should approach reconciliation once payouts are centralised.

Can this model work for your business?

If most of the following are true, this setup is likely worth evaluating:

You use two or more PSPs (e.g. Stripe and Adyen)

You collect revenue in GBP, EUR, and/or USD

You want to hold currencies before converting, rather than convert at payout

Your legal entity matches your intended payout destination details

Your PSPs support same-currency payout to your account format

Key Takeaways

A multi-currency EMI account can centralise PSP payouts where provider rules, legal-entity matching, payout currency support, and receiving-account format requirements are all correctly aligned.

Same-currency settlement — matching PSP payout currency to receiving-account currency — matters more than simply "one account."

Stripe, Adyen, and PayPal each handle balances, payout configuration, and reporting differently. There is no single universal setup that works for all three out of the box.

Consolidating payouts reduces fragmentation but does not eliminate the need for PSP-level reconciliation reports.

An EMI account is not the same as a bank account: client funds are safeguarded under the applicable e-money and payments regime, not covered by FSCS deposit insurance.

This article is designed to help finance and operations teams evaluate whether this model fits their setup before making changes to live payout instructions.

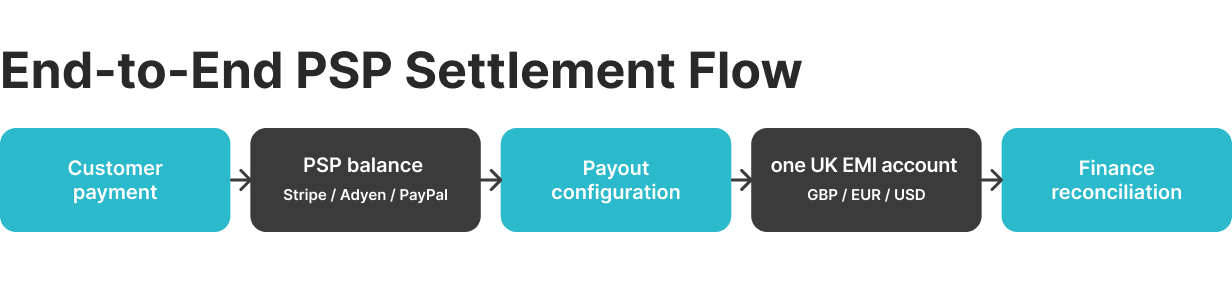

What Does PSP Settlement into a Multi-Currency EMI Account Mean?

PSP settlement into a multi-currency EMI account means routing merchant payouts from payment service providers into a single regulated account that can hold and transact in more than one currency — typically GBP, EUR, and USD for UK-based operations.

Four terms are worth distinguishing clearly:

Presentment currency — the currency a customer sees and pays in at checkout.

Settlement currency — the currency in which the PSP accumulates the merchant's balance, after any conversion the provider applies.

Payout currency — the currency in which the PSP transfers funds to the merchant's receiving account.

Receiving-account currency — the denomination of the account the merchant has registered as the payout destination.

When these four are misaligned, forced FX usually occurs somewhere in the chain. The goal of a multi-currency setup is to keep GBP, EUR, and USD separate — reducing unnecessary conversion and giving treasury a cleaner view of what the business holds per currency.

On the regulatory side: EQWIRE operates as an FCA-authorised electronic money institution. According to the FCA Register, authorised EMIs are required to safeguard relevant funds under UK rules — meaning client money is held separately from the institution's own operational funds. This is different from the deposit protection a bank provides. See How We Protect Your Money and the FCA's safeguarding requirements for full detail.

Provider Comparison: Stripe, Adyen, and PayPal at a Glance

Before going further, here is a summary of how each provider handles multi-currency payout. This table covers general behaviour; confirm the current state against provider documentation before changing any live settings.

Provider | Multi-currency balance support | Separate payout details required per currency? | Same-currency payout possible? | Primary reconciliation file |

|---|---|---|---|---|

Stripe | Yes | Yes — one verified account per settlement currency | Yes, where configured | Payout reconciliation report |

Adyen | Yes / depends on acquiring setup | Yes | Yes, where supported for currency/country pair | Settlement details report |

PayPal | Per-currency balance reporting | Varies by setup | More limited — evaluate separately | Settlement report (SFTP) |

Sources: Stripe multi-currency settlement, Adyen getting paid, PayPal settlement report.

Why Do Businesses Route PSP Settlements into One Multi-Currency Account?

The operational problem is straightforward. A business running Stripe for card payments, Adyen for platform flows, and PayPal as an alternative checkout option ends up with three dashboards, three payout schedules, and three reporting formats. If each PSP pays out to a different account in a different currency, finance teams are reconciling against three separate statements every month.

Common pain points:

GBP and EUR balances split across PSP dashboards with no unified treasury view

Forced FX when PSP payout currencies do not match receiving-account currencies

Slower month-end close when PSP reports must be mapped to multiple bank or EMI statements

Overdependence on a high-street bank that was not designed for multi-currency digital operations

Unclear net payout figures after PSP fees, refunds, and reserve deductions

Two illustrative scenarios:

An e-commerce brand selling across a UK and a European storefront collects GBP and EUR daily, but if both currencies route to a single GBP account, conversion happens at the PSP's rate before the money arrives. A SaaS platform billing globally in USD and EUR, managed from one UK entity, faces the same problem: USD revenue converted at payout rather than held and managed at the treasury level.

A correctly configured multi-currency EMI account with matched receiving-account details per currency can resolve both scenarios — subject to provider rules and account eligibility.

💡 Is your current payout setup working against you? If your Stripe, Adyen, or PayPal payout currencies do not match your receiving-account currencies, you may be paying for FX you could avoid. Check whether your account structure is aligned to the currencies your business actually needs to hold. Review your setup at EQWIRE →

How to Route Stripe, Adyen, and PayPal Payouts into a Multi-Currency EMI Account

PSPs process customer transactions, accumulate merchant balances under their own rules, and transfer funds based on configured payout accounts, supported currencies, payout schedules, and compliance requirements. How each provider handles this differs in ways that matter operationally.

Can Stripe Pay EUR into a EUR EMI Account?

Yes, where multi-currency settlement is configured and the receiving account passes Stripe's validation. Stripe's multi-currency settlement allows accounts to accumulate balances and receive payouts in additional currencies beyond the default. For each configured settlement currency, Stripe requires a separate supported bank account denominated in that currency — a SEPA-reachable EUR account for EUR payouts, a UK account with local sort code and account number for GBP payouts.

If a merchant processes PayPal payments through Stripe, there is a separate configuration choice: PayPal funds can settle on Stripe (as a Stripe balance) or settle directly to PayPal. Each option changes the money flow and the reconciliation logic, so this choice should be made deliberately and documented before going live.

When Adyen Like-for-Like Settlement Actually Works

Adyen operates at merchant-account level and pays out in batches. Merchants can link multiple bank accounts to one merchant account when accepting multiple currencies, and approved payout details can be copied across merchant accounts under the same legal entity.

Like-for-like settlement means EUR collected from European card transactions can settle and pay out as EUR — avoiding in-chain conversion. But this depends on the acquiring country and currency combination. Not all pairs support local payout, and cross-border payout behaviour varies. Checking Adyen's supported payout currencies before configuring a new payout destination is a required step, not an optional one.

Why PayPal Is the Exception in a Consolidated Payout Model

PayPal's settlement model is less directly configurable for "one EMI account" routing than Stripe or Adyen. PayPal's settlement report organises debits, credits, and opening/closing balances per currency — which is useful for consolidated reconciliation visibility, but it means PayPal reporting needs to be handled on its own terms rather than assumed to behave identically to the other two providers.

Treat PayPal's contribution to a centralised setup as currency-level reporting that feeds your consolidated reconciliation model, rather than a direct payout-routing parallel to Stripe or Adyen.

What Conditions Must Be in Place Before Routing Payouts to a UK EMI Account?

"One EMI account" works operationally only when several conditions are correctly met. These are the ones that most commonly cause problems.

Legal Entity and Account-Name Alignment

PSP payout accounts must match the verified legal entity registered with the provider. The account name, company registration details, and ownership structure must be consistent across your PSP setup and your EMI account. Attempting to route payouts across unrelated legal entities will typically fail verification.

If your business has multiple entities operating different storefronts or geographies, map this carefully before making any changes.

Supported Payout Currency and Local Account-Detail Format

GBP payouts from UK PSP flows generally require UK sort code and account number details in the Faster Payments format. EUR payouts require an IBAN in SEPA-reachable format. USD payouts require US routing details or SWIFT-based instructions depending on the provider.

Stripe requires a bank account matching each configured settlement currency. Adyen differentiates between local and cross-border payout depending on the currency and acquiring region. Providing the wrong account format for a given currency typically results in rejected payouts.

Compliance, Safeguarding, and Account Review

A regulated EMI account operates within a safeguarding framework defined by the FCA's requirements for payment institutions and EMIs. Client funds must be held in segregated accounts, separate from the EMI's own operational money. That is intended to improve protection and the return of funds if a firm fails — but it is not the same mechanism as deposit insurance, and outcomes depend on the firm's compliance and the specific insolvency process.

For UK payment-system access, non-bank payment service providers can participate directly or indirectly in systems including Faster Payments, Bacs, and the Image Clearing System, as documented by the Bank of England. EQWIRE's Important Information page covers how this applies to its own setup.

How to Avoid Forced FX Across GBP, EUR, and USD

Forced FX typically enters the picture in one of two places: inside the PSP before payout, when the settlement currency and payout currency do not match, or at payout when the destination account is denominated in a different currency. A multi-currency EMI account addresses the second problem. It cannot override PSP-level settlement rules that cause conversion before payout.

Stripe example: A UK merchant collects EUR from European customers. If their Stripe account has only a GBP payout destination, Stripe converts EUR balances to GBP before payout. Configuring a SEPA-reachable EUR receiving account and enabling EUR as a settlement currency allows Stripe to pay out EUR directly — preserving the currency through to the EMI account.

Adyen example: Adyen's like-for-like settlement means EUR collected from European card transactions can settle and pay out in EUR where the acquiring setup supports it. If the linked payout account is GBP-denominated, that like-for-like benefit is lost at the final step, even though Adyen processed the transaction in EUR throughout.

A practical example with numbers: A business receives €120,000 in Stripe settlements. After €3,200 in processing fees, €1,100 in refunds, and a €500 reserve deduction, the net payout to the EUR EMI account is €115,200. If that account is GBP-denominated instead, that €115,200 is converted at Stripe's rate before arrival — typically at a spread above mid-market. Holding EUR requires only a correctly configured EUR receiving account registered with Stripe.

The rule: for each currency you want to hold without conversion, register a correctly formatted receiving account for that currency with each relevant PSP. A multi-currency EMI account is only effective when each PSP has been configured to pay those currencies to matching account details.

For EQWIRE's supported currencies and settlement timing, see the currency list page.

How PSP Settlement Routing Works with a UK EMI Account in Finance Operations

Centralising payouts into one EMI account simplifies cash visibility. It does not simplify reconciliation on its own — and teams that assume "one account" means "one report" typically find that month-end becomes harder until the right reconciliation logic is built.

What needs to be tracked:

Gross sales vs net payout: PSPs pay out net of fees. Adyen's settlement details report separates gross transaction value, interchange, scheme fees, processing fees, and net payout. Stripe's payout reconciliation report provides equivalent detail. Each PSP line must map to its corresponding EMI account credit.

Refunds, chargebacks, and reserves: These deduct from settlement and are not always batched in the same payout cycle as the original transaction. A chargeback on a Stripe payment from three weeks ago may reduce this week's payout amount.

Payout batches and timing: Adyen pays in batches on a schedule and notes that payout funds can take up to two business days depending on the currency and receiving bank. Stripe payout timing varies by account settings, country, and whether next-day or standard payout is configured. PayPal operates on its own release schedule. When all three land in one EMI account, multiple credits with different references will appear on overlapping days.

Statement narration and references: PSP payouts arrive with provider-specific reference strings. Mapping those references in your accounting system before going live saves significant time during reconciliation.

Consolidation into one EMI account gives treasury a currency-level view of balances — but each balance still needs to be reconciled against the originating PSP report.

💡 Is reconciliation taking longer than it should? If GBP, EUR, and USD settlements arrive in separate accounts across multiple providers, building a consolidated view costs time every month. Compare your current setup against a structure where all three currencies are held in one EMI environment with matched payout routing from each PSP.

EMI Account vs Bank Account for PSP Settlement: What Is the Difference?

For PSP payout routing purposes, an EMI account can often be used as the receiving destination — but only where the PSP supports the currency, account format, and legal-entity match required for that payout flow. In practice, that means the account may function like a bank account for some payout routes, but it is not a universal substitute across every provider-country-currency combination.

The more important distinction is protection. Eligible deposits at UK-authorised banks, building societies, and credit unions are covered by the FSCS up to £120,000 per eligible depositor since 1 December 2025. EMI accounts are not covered in the same way. Instead, EMIs are required to safeguard relevant client funds separately from their own money. That is intended to improve protection and the return of funds if a firm fails, but it is not the same mechanism as deposit insurance.

When Is a Multi-Currency EMI Account the Right Fit?

Most likely to be a good fit:

E-commerce businesses operating across UK and European markets, collecting GBP and EUR, that want to avoid conversion before funds are operationally needed in a specific currency.

SaaS and digital platforms with recurring revenue in multiple currencies that need clean treasury visibility and predictable FX management.

SMBs using two or more PSPs that are struggling to reconcile fragmented settlement across multiple receiving accounts.

Global operators and non-UK businesses that need a UK-based infrastructure point for GBP receipts and Faster Payments capability without a UK high-street banking relationship.

See also: GBP Faster Payments for Offshore Company: Settlement Guide for a related look at how non-UK entities can access UK payment rails through an EMI structure.

Common Mistakes When Consolidating PSP Settlements

Assuming every PSP accepts the same payout-account structure. Stripe, Adyen, and PayPal each have different validation requirements, supported currency lists, and account-linking rules.

Confusing presentment currency with settlement currency. A customer paying in EUR does not automatically mean the PSP settles in EUR — it depends on how the merchant account is configured.

Ignoring legal-entity matching. PSP payout destinations must match the verified business entity. Mismatches cause rejected payouts.

Overlooking minimum payout thresholds. Stripe documents minimum payout amounts per currency for additional settlement currencies. Balances below the threshold are not paid out until the threshold is met.

Treating safeguarding like deposit insurance. They are different mechanisms with different implications in a firm failure scenario.

Removing legacy payout accounts before reconciliation is stable. Switching live payout settings before reconciliation mapping is validated creates gaps in the audit trail.

Assuming "one account" means "one report." PSP-level reporting is still required. The EMI statement records what arrived; PSP reports explain why.

Final Checklist Before Updating Payout Settings

Confirm the legal entity that owns each PSP account and matches the EMI account holder name.

Map customer presentment currencies against settlement currencies currently configured per PSP.

Identify the receiving-account details required per currency — UK sort code/account number for GBP, IBAN for EUR, routing details for USD.

Confirm whether same-currency or like-for-like settlement is available for each PSP/currency combination.

Review fees, minimum payout thresholds, and payout timing schedules per provider.

Build and test reconciliation rules before switching any live payout destination.

Prepare fallback instructions for failed, delayed, or rejected payouts.

Confirm internal understanding of EMI safeguarding and how it differs from bank deposit protection.

Next Step: Evaluate Whether One EMI Setup Can Replace Fragmented Payout Accounts

Before changing live payout settings across Stripe, Adyen, or PayPal, map current payout currencies and receiving-account configurations against the structure you want to move to.

EQWIRE's multi-currency account may support GBP, EUR, and USD with access to Faster Payments, SEPA, and international payment rails, subject to onboarding and eligibility. Funds are held under FCA safeguarding requirements. The currency list page covers settlement timing and supported currencies in detail.

Compare your current PSP payout settings against EQWIRE's account capabilities and safeguarding model before making any changes to live settlement instructions.

FAQ

Can I receive Stripe, Adyen, and PayPal payouts into one UK EMI account?

In many setups, yes — but only where PSP validation rules, legal-entity matching, supported payout currencies, and receiving-account format requirements all align. Stripe requires a separately registered and verified account per settlement currency. Adyen requires verified payout details consistent with the legal entity. PayPal's payout routing behaviour differs from the other two and should be evaluated separately. There is no universal guarantee that all three will work identically to a single EMI account out of the box.

Does a multi-currency EMI account prevent forced FX?

It can reduce or eliminate forced FX at the receiving-account stage when same-currency settlement is configured and correctly formatted receiving-account details are registered with each PSP. It does not remove FX where the PSP's own rules require conversion before payout — for example, where a specific currency is not supported for local payout in a given market.

What is the difference between settlement currency and payout currency?

Settlement currency is the currency in which the PSP accumulates your merchant balance after processing customer transactions. Payout currency is the currency in which the PSP transfers funds to your receiving account. These can differ if multi-currency settlement is not configured. For example, a UK merchant collecting EUR from European customers may have GBP as the default settlement currency, meaning EUR transactions are converted to GBP before the balance is formed — and paid out in GBP. Configuring EUR as an additional settlement currency with a matching EUR receiving account keeps the EUR balance intact through to payout. Stripe's currency documentation covers this in detail.

Is an EMI account protected like a bank account?

No. EMI accounts are not covered by the FSCS. Eligible deposits at UK-authorised banks, building societies, and credit unions are protected up to £120,000 per eligible depositor since 1 December 2025. EMIs must instead safeguard client funds by holding them in segregated accounts at a regulated credit institution, separate from the EMI's own money. This is intended to protect clients if the EMI fails, but the mechanism is different from FSCS deposit insurance. See How We Protect Your Money and the FCA's safeguarding requirements for full detail.

How long does PSP settlement usually take?

Settlement timing varies by provider, currency, payout destination, and account configuration. Adyen notes that payout funds can take up to two business days depending on the currency and receiving bank. Stripe's payout timing depends on account settings, country, and whether standard or next-day settlement is configured — it is not a fixed rule. EQWIRE's currency list page sets out settlement timing for GBP, EUR, and USD based on destination currency, local banking system, and applicable cut-off times.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)