•

•

AED Business Account for UAE Company: Hold Dirhams and GBP in One Place

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Opening a UAE bank account for a company without local residency typically requires branch visits, a minimum 6–12 week review, and proof of physical presence in the emirate. For UAE Free Zone companies, offshore holding structures, and BVI-registered entities operating across UAE and UK markets, this creates a practical bottleneck: two currencies, two banking relationships, and compounding operational overhead.

An AED business account UK EMI offers a different path. A UK Electronic Money Institution (EMI) authorised by the Financial Conduct Authority (FCA) can provide UAE-registered and offshore companies with a multi-currency account that holds AED and GBP under a single IBAN — no UAE banking relationship required. This article compares both approaches, identifies which company types qualify, and outlines the scenarios where a UK EMI is the more practical choice.

[aa key-takeaways]

Key Takeaways

A UK EMI with FCA authorisation can open an AED business account for UAE company structures — including Free Zone, mainland, BVI, Cayman, and Bermuda-registered entities.

AED and GBP can be held simultaneously in one multi-currency account, with AED received via SWIFT MT103 and GBP via Faster Payments or CHAPS.

UK EMI onboarding typically takes 5–14 business days for offshore companies with a complete KYC package — compared to 6–12 weeks at UAE banks.

AED balances at a UK EMI are electronic money safeguarded under the Electronic Money Regulations 2011, not bank deposits under UAE law.

FX conversion between AED and GBP at a UK EMI typically costs 0.3–1.5% — compared to 2–3% at traditional banks.

[aa btn]Book a Call[/aa]

[/aa]

UAE Bank vs UK EMI — Core Differences for AED Business Accounts

The core difference between a UAE bank and a UK EMI for AED accounts lies in the entity types accepted, the onboarding timeline, and the regulatory framework that protects deposited funds.

A dirham business account at a UAE bank is a local bank deposit held under UAE Central Bank (CBUAE) supervision. An AED balance at a UK EMI is electronic money held in a safeguarded account under FCA oversight — accessed via SWIFT. UAE banks require physical presence in the emirate, proof of a UAE trade licence, and branch-level KYC. UK EMIs complete the entire process remotely, accepting a wider range of company types under the Electronic Money Regulations 2011.

Comparison: UAE Bank vs UK EMI for AED

Criteria | UAE Bank | UK EMI |

|---|---|---|

Opening timeline | 6–12 weeks | 5–14 business days |

KYC process | Branch visit required | Fully remote, digital |

UAE residency required | Yes (typically) | No |

AED access | Direct local deposit | SWIFT MT103 routing |

GBP on same account | Separate account needed | Yes — multi-currency |

Offshore entities (BVI, Cayman) | Rarely accepted | Accepted by select providers |

Regulatory framework | CBUAE | FCA (UK EMR 2011) |

Safeguarding | Central bank deposit rules | Segregated client funds |

When a UAE Bank Is Still the Right Choice

A UAE bank remains the better option for companies that process high volumes of local AED cash transactions, require letter of credit (L/C) facilities, need to issue physical cheques to UAE counterparties, or hold a UAE mainland trade licence with substantial local operations. For those structures, CBUAE-regulated bank infrastructure provides services that UK EMIs do not.

[aa fast-fact]

Fast Fact: According to the BIS 2024 Cross-Border Payments Monitoring Survey, 90.4% of wholesale SWIFT payments completed within one hour in 2024 — up 0.9 percentage points year-on-year, reflecting improvements across the Middle East and Africa corridor.

[/aa]

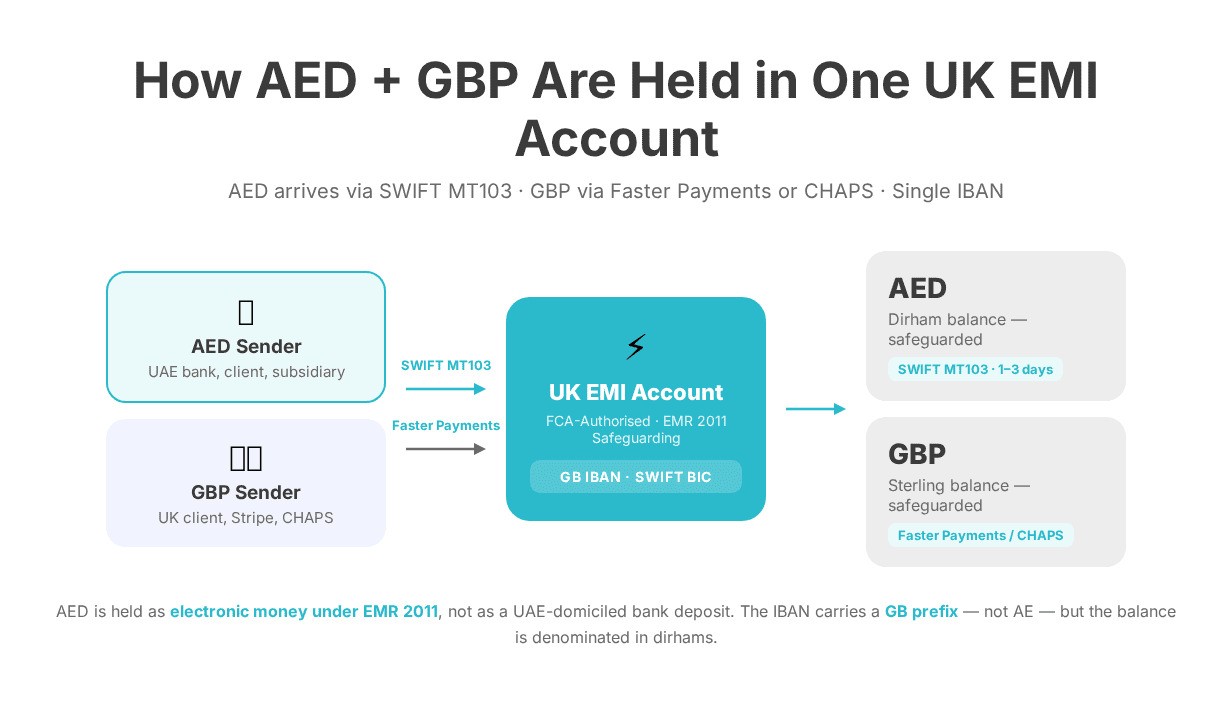

How a UK EMI Enables AED and GBP on One Account

An AED business account through a UK EMI works differently from a UAE bank account: the EMI holds AED as electronic money in a multi-currency balance, accessible through a single IBAN issued under the UK payments framework. Under the FCA's Electronic Money and Payment Institutions framework, FCA-authorised EMIs are permitted to issue e-money and provide payment services — including multi-currency accounts — to business clients, covering offshore-registered entities.

This model allows a UAE Free Zone company or a BVI holding structure to hold AED and GBP in one account without maintaining two separate banking relationships across two jurisdictions.

Multi-Currency Balance Structure

Holding AED and GBP in one account at a UK EMI means maintaining separate currency pots under a single account identifier — typically a GB IBAN. Each currency pot receives and sends payments independently. GBP transactions route via Faster Payments or CHAPS for domestic UK transfers. AED inflows arrive via SWIFT.

The GB IBAN vs AE IBAN distinction matters here. UK EMIs issue IBANs with a GB prefix — not an AE prefix. AED is held as a currency balance denominated in dirhams, not as a UAE-domiciled account. Counterparties sending AED payments use the EMI's SWIFT BIC to route funds through the correspondent banking network.

Under the EMR 2011 safeguarding requirements, UK EMIs are legally required to segregate client funds — including AED balances — from their own assets. This obligation applies regardless of the account holder's jurisdiction of incorporation.

SWIFT vs Local AED Payment Rails

AED payments to a UK EMI account route via SWIFT MT103, using the EMI's correspondent banking relationships to settle funds without requiring a UAE-domiciled bank account. Inbound AED SWIFT payments typically settle within 1–3 business days, depending on the sending bank's correspondent chain.

Offshore companies can receive AED through a UK EMI by providing counterparties with the EMI's SWIFT BIC and account IBAN. The payment routes through the correspondent network and is credited to the AED currency balance. According to BIS correspondent banking data, active correspondent banking relationships — though declining globally in number — remain the primary infrastructure for cross-border AED flows outside the UAE domestic network.

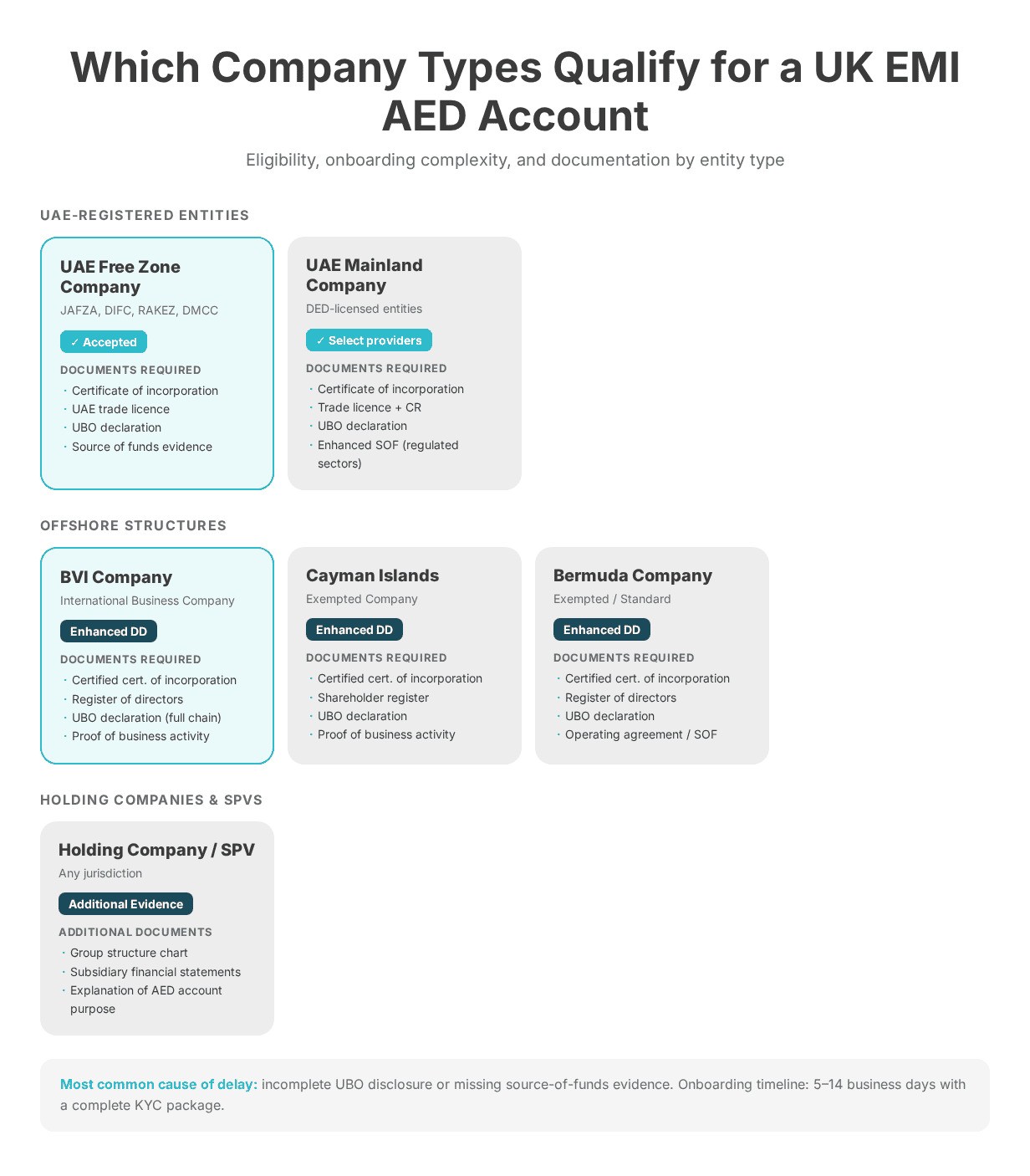

Which Company Types Qualify for an AED Account at a UK EMI

Not all UK EMIs accept offshore-registered entities, and the acceptance criteria vary by jurisdiction and the EMI's own risk appetite under FCA AML obligations. Company type is the primary filter — and it determines both onboarding complexity and the document set required.

Opening an AED account as an offshore company through a UK provider requires matching the EMI's accepted jurisdictions list and submitting a complete KYC package upfront.

UAE Free Zone and Mainland Companies

UAE Free Zone companies — registered in jurisdictions such as JAFZA, DIFC, RAKEZ, or DMCC — are generally treated as lower-risk entities by UK EMIs. They hold a recognised UAE trade licence and typically have straightforward UBO structures. Required documents usually include the certificate of incorporation, trade licence, UBO declaration, and source-of-funds evidence.

Mainland UAE companies are accepted by select UK EMIs, though they may require additional source-of-funds documentation, particularly where the company operates in regulated sectors. An FCA-authorised payment account for UAE company structures in both categories is available from providers with broad jurisdictional acceptance policies.

Offshore Structures: BVI, Cayman, Bermuda

BVI, Cayman Islands, and Bermuda-registered companies are accepted by a number of UK EMIs, subject to enhanced due diligence under KYC/AML frameworks. Offshore entities require a certified certificate of incorporation, register of directors, UBO declaration, proof of business activity, and — where applicable — a shareholder register or operating agreement.

EQWIRE accepts BVI, Cayman, and Bermuda-registered entities through a fully remote onboarding process. Incomplete UBO disclosure is the most common cause of application delays or rejection. For BVI-registered companies already operating with UK banking infrastructure, the process mirrors how BVI-registered companies obtain UK bank details through an FCA-authorised EMI. Similarly, Bermuda-registered entities access GBP sort codes and UK payment accounts through the same remote onboarding model.

Holding Companies and SPVs

Holding companies and special purpose vehicles (SPVs) require additional evidence of operating subsidiaries or underlying commercial activity. A UK EMI will typically request group structure charts, subsidiary financial statements, and a clear explanation of the AED account's purpose — particularly for entities receiving royalties, dividend distributions, or inter-company AED transfers.

[aa cta]

Open an AED + GBP Account Without a UAE Bank

EQWIRE is FCA-authorised and accepts UAE Free Zone, mainland, and offshore-registered companies — fully remote onboarding, no branch visits required.

[aa btn]Create Account[/aa]

[/aa]

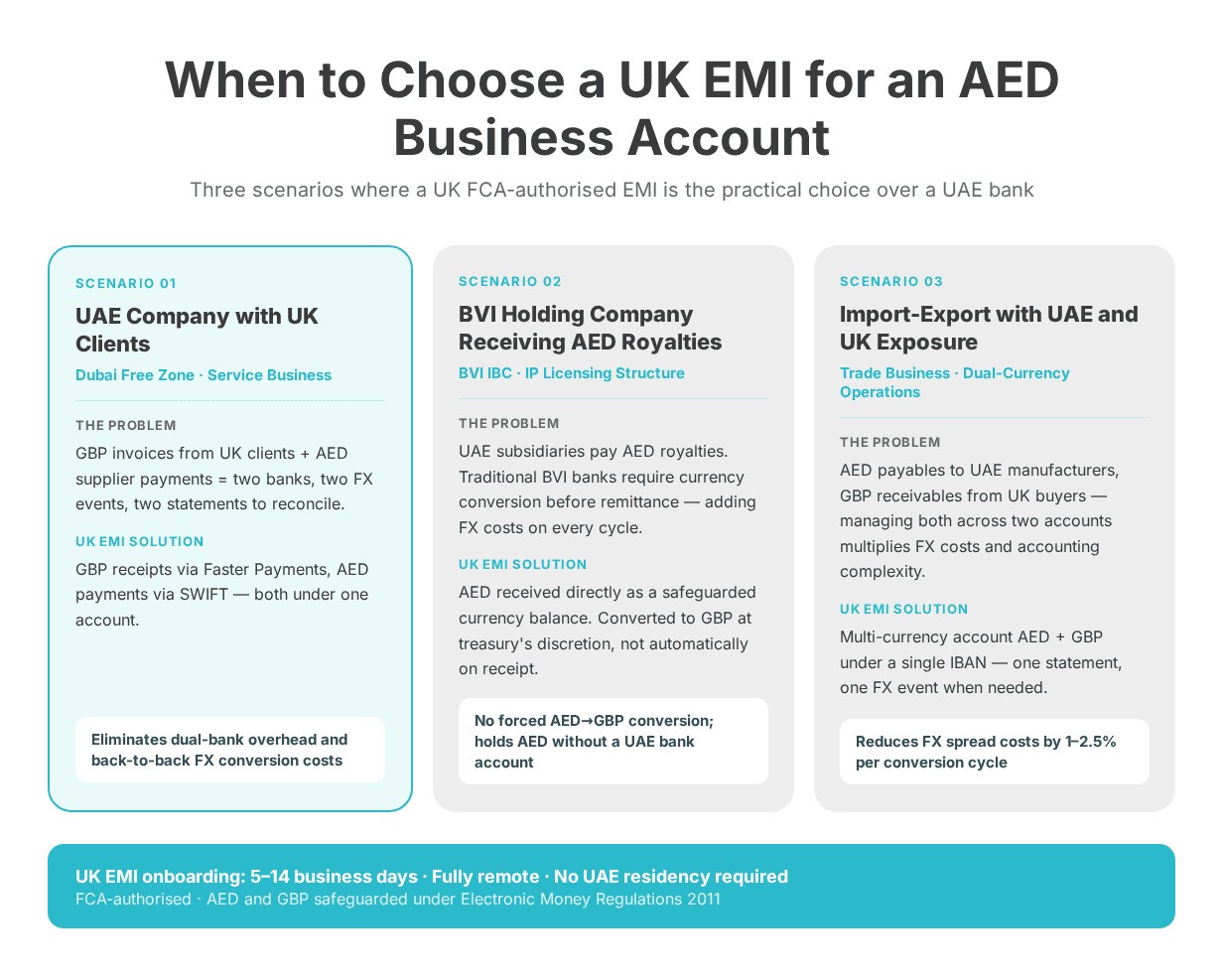

When to Choose a UK EMI for an AED Business Account

A UK EMI is the practical choice for UAE-registered and offshore companies that need to send or receive AED without maintaining a UAE bank relationship. Three business scenarios illustrate where the model creates measurable operational and cost advantages.

UAE Company with UK Clients

A Dubai Free Zone company supplying services to UK-based clients faces a recurring cash flow challenge: invoices settle in GBP, but supplier payments and local overhead in the UAE are denominated in AED. Managing this across two separate banks — one UAE, one UK — means two fee structures, two FX conversion events, and reconciliation across two statements.

A UAE company UK payment account at a UK EMI consolidates both currencies under one account. GBP receipts from UK clients arrive via Faster Payments. AED supplier payments go out via SWIFT. For companies collecting GBP through platforms like Stripe, having a UK settlement account for international businesses that also holds AED removes one more layer of operational friction.

BVI Holding Company Receiving AED Royalties

A BVI holding company licensing intellectual property to UAE-based subsidiaries typically receives royalty payments denominated in AED. Traditional offshore banks in BVI or Caribbean jurisdictions often require currency conversion before remittance — adding FX costs and settlement delays on every payment cycle.

Through a UK EMI, the BVI holding company can receive AED directly as a currency balance, without conversion on receipt. This resolves a common treasury problem for offshore structures: how to receive AED payments without a UAE bank account. The AED balance can be held, converted to GBP at the treasury's discretion, or used directly for SWIFT payments to other counterparties.

Import-Export Businesses with UAE and UK Exposure

An import-export business purchasing goods from UAE manufacturers and selling into the UK market needs to manage AED payables and GBP receivables simultaneously. A multi-currency account AED GBP setup at a UK EMI eliminates back-to-back FX conversions on every trade cycle and provides a single statement for reconciliation — reducing the accounting overhead that dual-bank setups create.

Cost and FX Comparison — AED/GBP at a UK EMI vs Traditional Bank

FX conversion between AED and GBP is where the cost difference between a UK EMI and a traditional bank becomes most visible. Holding AED and GBP in one account at a UK EMI avoids the automatic conversion that many traditional banks apply when receiving a foreign currency payment — a default that erodes value on every inbound AED transfer.

The market range for AED/GBP FX at UK EMIs is typically 0.3–1.5% spread, depending on the provider and account tier. Traditional banks — including UAE banks processing cross-border AED/GBP transactions — typically apply a 2–3% FX markup, plus separate transaction fees ranging from £15 to £45 per outbound SWIFT payment.

What that means in practice: for a company converting AED 200,000 to GBP monthly at current rates, the difference between a 1% EMI spread and a 2.5% bank spread represents approximately £1,400–£1,600 in monthly savings, depending on the AED/GBP rate at time of conversion.

[aa fast-fact]

Fast Fact: The global average cost of sending a $200 cross-border payment stood at 6.5% in Q1 2025, according to the BIS cross-border payments report — illustrating the cost premium embedded in traditional correspondent banking chains.

[/aa]

Transfer fees at UK EMIs are typically flat — ranging from £5–£25 per outbound SWIFT payment, with no incoming transfer fees in most cases. Monthly account maintenance fees vary by provider and tier. A dirham business account through a UK EMI often carries no minimum balance requirement, unlike UAE bank accounts, which may require minimum deposits of AED 10,000–50,000.

One limitation to note: UK EMIs do not provide CBUAE-regulated bank accounts. AED held at a UK EMI is electronic money under UK law — not a UAE bank deposit. Finance teams should factor this regulatory distinction into treasury policy, particularly for companies operating under UAE Central Bank regulatory oversight.

FAQ

Can a BVI company hold AED balance in a UK EMI account?

Yes. A BVI-registered company can hold an AED balance at a UK EMI, subject to the EMI's KYC/AML policy and jurisdiction acceptance criteria. Select FCA-authorised UK EMIs accept BVI International Business Companies through a remote onboarding process. Required documentation typically includes a certified certificate of incorporation, register of directors, UBO declaration, and proof of business activity. The AED balance is held as electronic money under the Electronic Money Regulations 2011 and is safeguarded separately from the EMI's own assets. Onboarding for BVI structures with a complete document package typically takes 7–14 business days.

How do offshore companies receive AED without a UAE bank?

Offshore companies can receive AED through a UK EMI by using SWIFT MT103 transfers routed via the EMI's correspondent banking network. The AED is credited to the company's multi-currency balance and held as safeguarded electronic money — no UAE bank account required. The process requires the offshore company to provide counterparties with the UK EMI's SWIFT BIC and account IBAN. Inbound AED SWIFT payments typically settle within 1–3 business days. This mechanism allows BVI, Cayman, Bermuda, and other offshore structures to receive AED royalties, service fees, or inter-company payments without a UAE banking relationship.

What is the difference between an AED account at a UK EMI and a UAE bank account?

The primary difference is the regulatory framework and account structure. A UAE bank AED account is a bank deposit held under UAE Central Bank supervision, with direct access to the local AED payment infrastructure. A UK EMI AED account is electronic money held in a safeguarded account under FCA authorisation and the Electronic Money Regulations 2011. It receives AED via SWIFT — not via local UAE payment rails — and does not constitute a UAE-domiciled bank account. UK EMIs accept a wider range of company types, including offshore structures, and offer faster remote onboarding. UAE banks provide services that UK EMIs do not, including letter of credit issuance and physical cheque handling.

How long does it take to open an AED business account for a UAE company at a UK EMI?

The onboarding timeline at a UK EMI for a UAE-registered company is typically 5–14 business days, provided the KYC package is complete on first submission. UAE Free Zone companies with straightforward UBO structures generally complete onboarding at the faster end of that range. Offshore structures — including BVI, Cayman, and Bermuda entities — may require 10–14 business days due to enhanced due diligence. By comparison, opening a UAE bank account typically takes 6–12 weeks and requires branch visits. Incomplete UBO disclosure or missing source-of-funds evidence are the most common causes of delay at any UK EMI.

Can GBP and AED be held in the same UK EMI account?

Yes. Select UK EMIs offer multi-currency accounts that hold both GBP and AED under a single IBAN. GBP is accessed via Faster Payments and CHAPS for UK domestic transfers. AED is received and sent via SWIFT MT103. Both currencies are managed through a single account interface with separate currency balances. Conversion between AED and GBP is executed at the EMI's prevailing FX rate — typically within a 0.3–1.5% spread — and can be initiated on demand rather than applied automatically on receipt.

For UAE-registered and offshore companies operating across UAE and UK markets, maintaining separate banking relationships for AED and GBP introduces unnecessary complexity. An AED business account UK EMI consolidates both currencies, eliminates residency requirements, and processes inbound AED via SWIFT — without the 6–12 week onboarding timeline that UAE banks typically require. EQWIRE is FCA-authorised and accepts UAE Free Zone, mainland, BVI, Cayman, and Bermuda-registered entities through a fully remote process. Companies ready to consolidate AED and GBP under one account can open an EQWIRE account to get started.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)