•

•

UK Payment Account for Bermuda Company: GBP Without a UK Office

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Bermuda-registered companies that invoice UK clients regularly face the same friction: UK Faster Payments require a UK sort code, and UK sort codes require a UK bank account. Most UK banks will not open accounts for offshore-registered entities without physical UK presence. The result is that GBP receipts arrive via SWIFT — slower, more expensive, and without the real-time settlement UK clients expect.

A Bermuda company UK payment account is accessible through an FCA-authorised Electronic Money Institution (EMI). EMIs are licensed under UK financial regulation to issue named UK sort codes and account numbers to non-resident entities, including Bermuda-incorporated businesses. No UK office, UK director, or UK shareholder is required.

This article explains how the regulatory framework enables this, what the account structure looks like, what documentation a Bermuda company needs to apply, and what payment capabilities become available once the account is live.

[aa key-takeaways]

Key Takeaways

Bermuda-registered companies can obtain a named UK sort code and account number through an FCA-authorised EMI — no UK physical presence required

FCA Electronic Money Institutions operate under the Electronic Money Regulations 2011 and are legally authorised to provide UK payment accounts to non-resident entities

GBP Faster Payments (real-time), CHAPS (same-day high-value), and SWIFT inbound are all available on an EMI-issued UK account

UK high-street banks reject Bermuda entities for structural reasons — physical presence requirements and correspondent banking risk policy — not because of Bermuda’s regulatory standing

Document preparation, especially for complex beneficial ownership structures, is the primary variable in the application timeline

[aa btn]Open an Account[/aa]

[/aa]

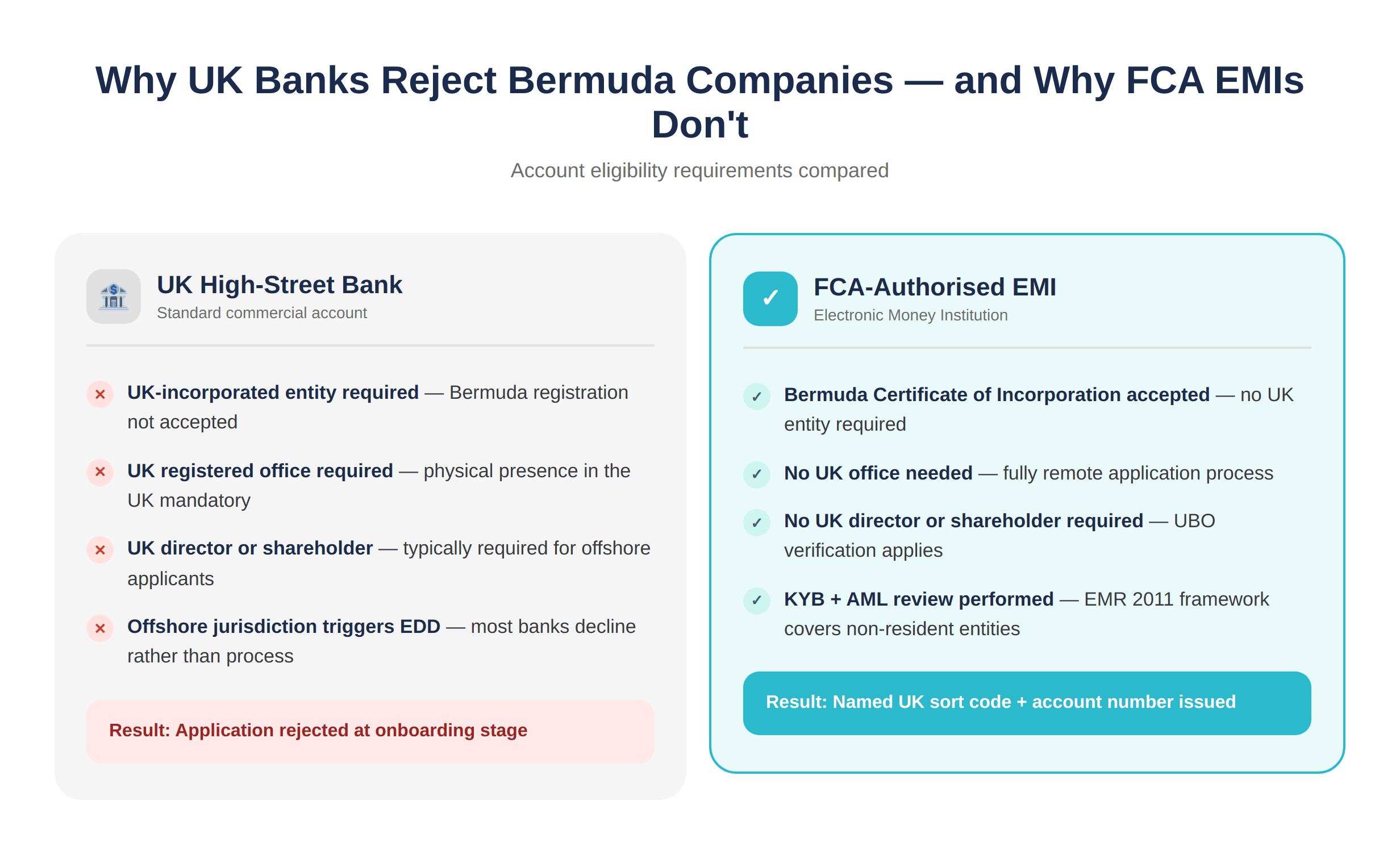

Why UK Banks Turn Down Bermuda Companies

Bermuda is a British Overseas Territory with an established financial regulatory framework overseen by the Bermuda Monetary Authority. It is not on any international sanctions list. Despite this, the majority of UK retail and commercial banks routinely decline applications from Bermuda-registered entities. The reasons are structural, not reputational.

The Physical Presence Requirement

Most UK banks require one of three things to open a business account: a UK-registered legal entity, a UK-based director, or a physical UK office address. A Bermuda Certificate of Incorporation satisfies none of these.

This requirement exists because UK banks built their onboarding frameworks around domestic corporate clients. Offshore-incorporated entities fall outside those frameworks by design — the banks’ systems cannot easily process them, and their compliance teams are not resourced to handle the enhanced due diligence that offshore structures require.

Having UK clients, a UK SWIFT correspondent, or even a UK subsidiary does not substitute for a UK-incorporated entity in a bank’s account opening process.

Correspondent Banking Risk Appetite and Offshore Jurisdictions

The second structural barrier is risk appetite. UK banks assess each client against their own correspondent banking risk policy. Offshore jurisdictions — even compliant ones like Bermuda — often trigger mandatory enhanced due diligence that many banks choose not to perform.

The FCA has published guidance on correspondent banking de-risking, acknowledging that financial institutions increasingly exit relationships with offshore clients rather than invest in the compliance infrastructure to manage them.

What this means in practice: a Bermuda holding company applying to a major UK bank faces near-100% rejection rates — not because it is high-risk, but because it does not fit the bank’s onboarding model.

What Is an FCA-Authorised EMI — and How Does It Differ from a UK Bank

An FCA-authorised EMI operates under a different regulatory model from a bank. EMIs are licensed to issue electronic money and provide payment services — but they are not deposit-taking institutions and do not offer credit facilities, overdrafts, or FSCS deposit protection.

What they can do is provide fully functional UK payment accounts — including named sort codes and account numbers — to entities that banks will not serve.

Regulatory Basis: The Electronic Money Regulations 2011

FCA authorisation for EMIs is granted under the Electronic Money Regulations 2011 (SI 2011/99). Under this framework, an EMI may provide payment account services to any eligible business client — including businesses incorporated outside the UK — provided standard KYB and AML requirements are met.

There is no requirement in the EMR 2011 for the account holder to be a UK-incorporated entity or to maintain any physical UK presence. This is the regulatory basis on which a Bermuda company can hold a UK sort code and account number. It is not a workaround — it is a separate and fully legitimate class of payment service provider.

What Payment Services an EMI Can Provide to a Bermuda Entity

An FCA-authorised EMI can provide the following to a Bermuda-registered business:

Named UK sort code and account number — issued directly in the company’s legal name

GBP Faster Payments — inbound and outbound, real-time, 24/7

CHAPS — same-day high-value domestic GBP transfers

SWIFT BIC — for receiving international wire transfers in GBP from overseas counterparties

[aa fast-fact]

Fast Fact: EMI clients’ funds are protected through safeguarding requirements under the EMR 2011. EMIs must hold client funds in segregated accounts at a credit institution — a different form of protection from FSCS, but a meaningful one.

[/aa]

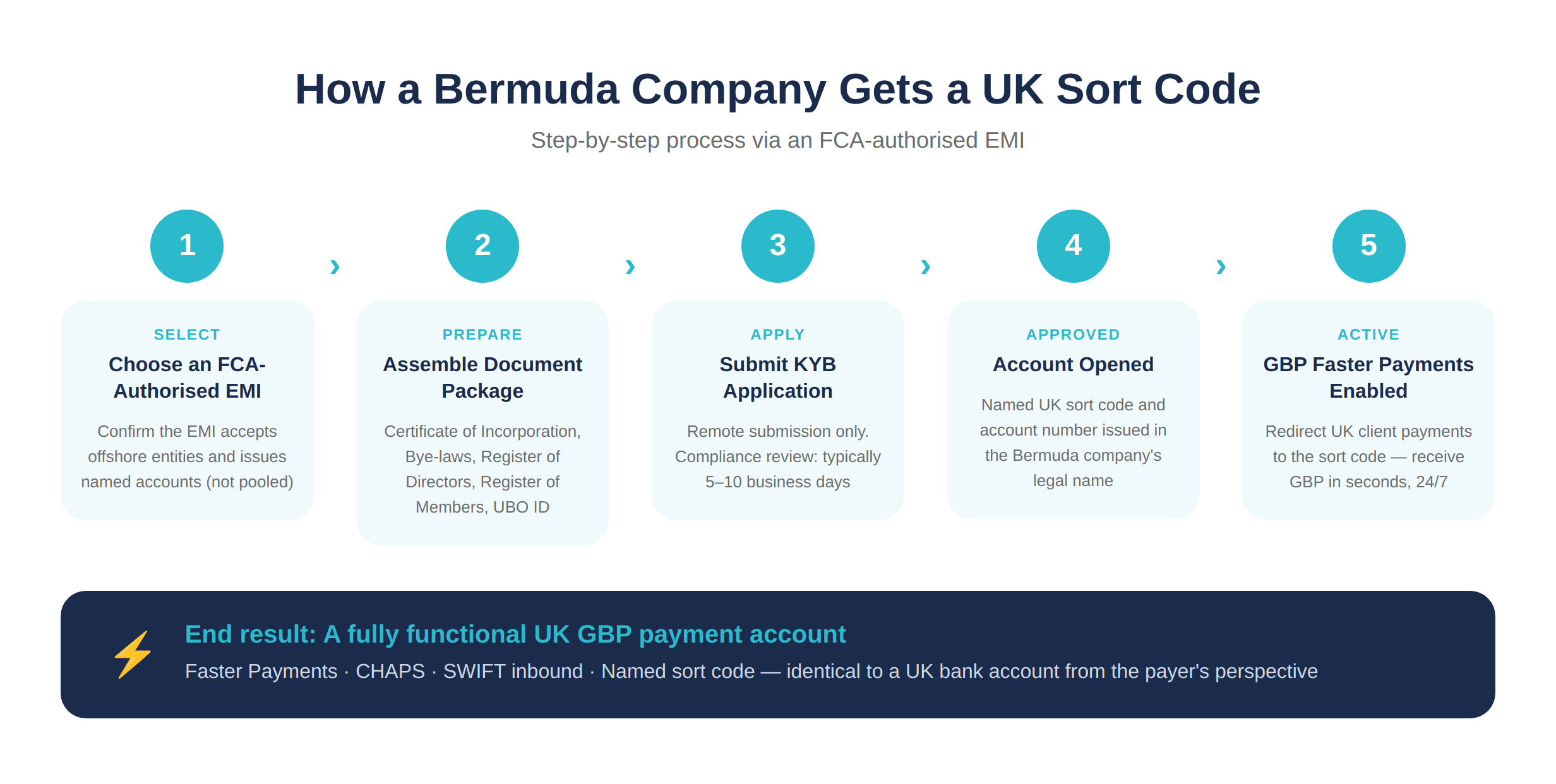

Bermuda Company UK Payment Account — How to Get a UK Sort Code

The account structure offered by FCA-authorised EMIs is functionally equivalent to a standard UK business bank account from a payer’s perspective.

Named UK Sort Code and Account Number Explained

A named account means a unique UK sort code and account number is issued directly in the Bermuda company’s legal name. When a UK client makes a Faster Payment, the Bermuda company’s name appears on the client’s bank statement as the payee. No reference number is required.

A Bermuda holding company seeking UK sort code and account number access via EMI should confirm during the application process that the account will be issued in the company’s own name with a dedicated sort code — not a shared pooled account identified by reference.

GBP Faster Payments Access for Non-UK Entities

Faster Payments is the UK’s real-time payment infrastructure. Payments arrive within seconds, 24 hours a day. For a Bermuda company receiving GBP from UK clients, this eliminates the 2–5 business day delays and £15–£30 correspondent fees associated with SWIFT receipts.

A Bermuda company receiving 20 GBP payments per month from UK clients can eliminate up to £600/month in correspondent fees by redirecting payments to the EMI account’s UK sort code.

CHAPS and International SWIFT Inbound

Alongside Faster Payments: CHAPS covers same-day high-value domestic GBP transfers; a SWIFT BIC enables GBP wire receipts from overseas counterparties whose banks do not support Faster Payments.

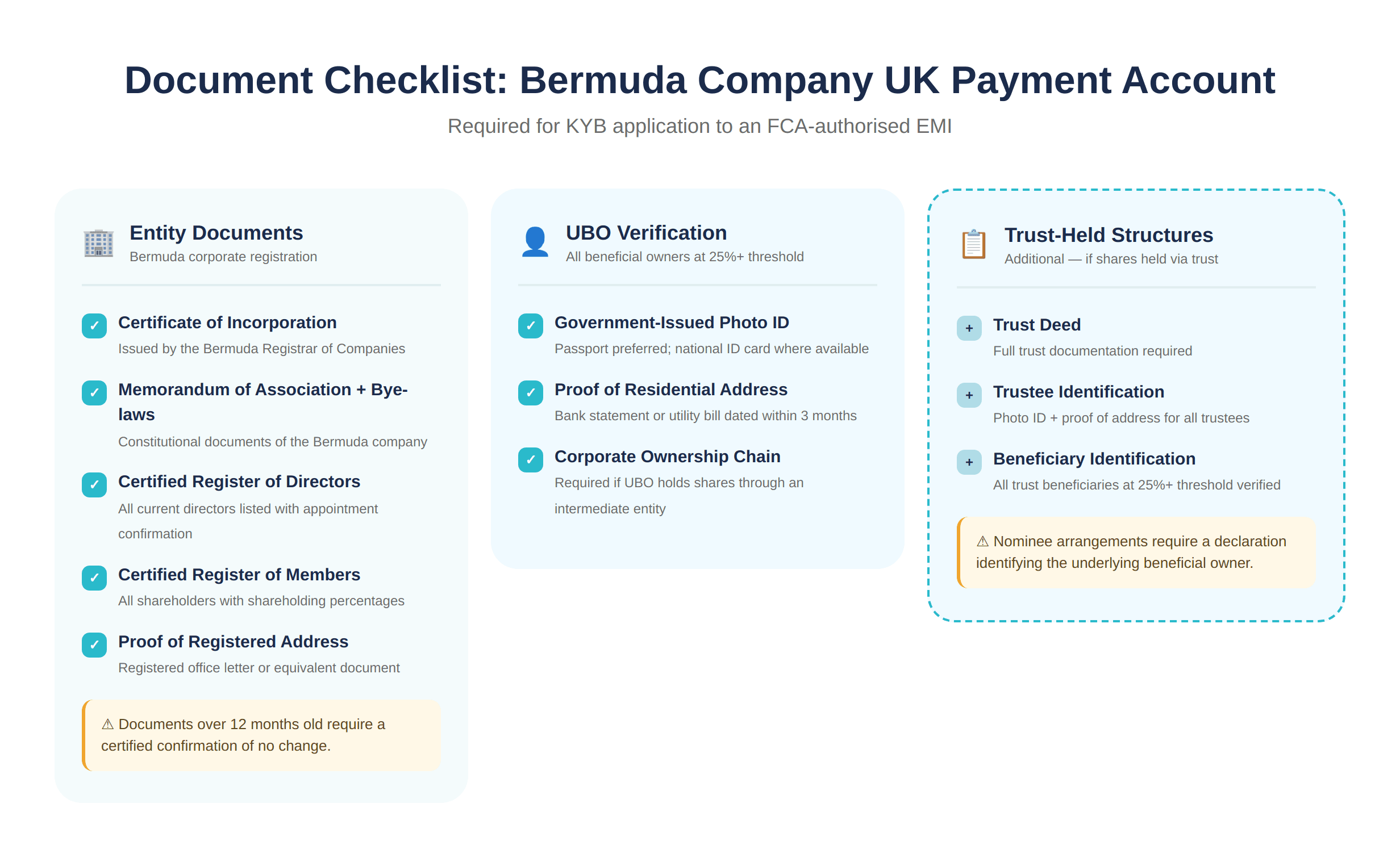

What Documents Does a Bermuda Company Need to Open a UK Payment Account

Document preparation is where most applications stall. Bermuda corporate structures can involve holding companies, nominee arrangements, and multi-layer ownership chains — all of which require full beneficial ownership tracing before an EMI can open the account.

Corporate Structure Documents for Bermuda Entities

At entity level, the following are typically required:

Certificate of Incorporation — issued by the Bermuda Registrar of Companies

Memorandum of Association and Bye-laws — the constitutional documents

Certified Register of Directors and Officers — listing all current directors

Certified Register of Members (Shareholders) — with shareholding percentages

Proof of registered address in Bermuda — registered office letter or equivalent

All documents must be current. Documents over 12 months old typically require a certified confirmation of no change.

UBO Identification and Enhanced Due Diligence

Every natural person who ultimately owns or controls 25% or more of the Bermuda company must be individually verified — regardless of how many corporate layers exist between the UBO and the entity.

Each UBO must provide: government-issued photo ID (passport preferred) and proof of residential address dated within 3 months.

Document | Standard Company | Trust-Held Structure |

|---|---|---|

Certificate of Incorporation | ✓ Required | ✓ Required |

Memorandum + Bye-laws | ✓ Required | ✓ Required |

Register of Directors | ✓ Required | ✓ Required |

Register of Members | ✓ Required | ✓ Required |

Trust deed | ✗ Not required | ✓ Required |

Trustee ID + address | ✗ Not required | ✓ Required |

UBO photo ID | ✓ Required | ✓ Required |

UBO proof of address | ✓ Required | ✓ Required |

Incomplete UBO documentation is the most common reason for application delays. Preparing the full document package before submitting — including certified translations if documents are not in English — significantly reduces review time.

[aa cta]

Get a UK Sort Code for Your Bermuda Company — Without a UK Office

EQWIRE is FCA-authorised and accepts Bermuda-registered entities for fully remote account opening.

[aa btn]Apply for a UK Payment Account[/aa]

[/aa]

What a UK Payment Account Enables for a Bermuda Business

Inbound GBP from UK clients arrives via Faster Payments in seconds — replacing SWIFT delays of 2–5 days and per-transaction fees of £15–£30. A Bermuda company can also receive GBP via Faster Payments from UK payers without requiring them to initiate a SWIFT wire — removing a friction point that UK clients often encounter with international suppliers.

Outbound GBP to UK suppliers and contractors is sent by Faster Payments as well. This covers payroll, contractor invoices, and supplier settlements without international wire processing times.

GBP balance retention allows the company to hold GBP in the account without forced conversion to a base currency. For businesses with both GBP income and GBP expenditure, this eliminates two FX conversion events per transaction cycle. Companies needing to hold EUR or USD alongside GBP can pair this with a multi-currency account to manage balances across currencies without conversion friction.

Conclusion

The barrier preventing Bermuda companies from accessing the UK payment system is structural, not regulatory. UK banks restrict access based on physical presence requirements that offshore-incorporated entities cannot satisfy by definition. FCA-authorised EMIs operate under a different framework that removes this restriction.

A Bermuda company UK payment account issued by an FCA-authorised EMI provides a named UK sort code and account number, access to GBP Faster Payments and CHAPS, and a SWIFT BIC for international inbound transfers — all without a UK office or UK-incorporated entity. The process is fully remote. Document preparation for the corporate structure and UBO verification is the primary variable in the application timeline, particularly for trust-held or multi-layer Bermuda structures.

For Bermuda-registered businesses that invoice UK clients, pay UK suppliers, or need to hold GBP balances, an EMI-issued UK payment account is the most direct and cost-effective solution available.

[aa cta]

Open a UK Payment Account as a Bermuda Company

Start the application online — no UK office, no in-person visit required.

[aa btn]Open an Account[/aa]

[/aa]

FAQ

How can a Bermuda company open a GBP account in the UK?

A Bermuda-registered company can open a GBP account in the UK through an FCA-authorised Electronic Money Institution. Under the Electronic Money Regulations 2011, EMIs are licensed to provide UK payment accounts — including named sort codes and account numbers — to non-UK-resident entities. The application is completed remotely and requires corporate registration documents and UBO identity verification.

Can a Bermuda registered business get UK bank details?

Yes. While traditional UK banks typically require a UK office or UK-incorporated entity, FCA-authorised EMIs can issue a named UK sort code and account number to a Bermuda-registered business. The account functions identically to a standard UK bank account from a payer’s perspective — the company’s legal name appears on the payee field of any Faster Payment received.

What documents does a Bermuda company need to open a UK payment account?

At minimum: Certificate of Incorporation from the Bermuda Registrar, Memorandum of Association and Bye-laws, certified Register of Directors, certified Register of Members (shareholders), proof of registered address in Bermuda, and government-issued photo ID plus proof of residential address for all UBOs holding 25% or more. Trust-held structures require additional documentation including the trust deed and trustee identification.

Can a Bermuda company receive GBP Faster Payments without UK presence?

Yes. An FCA-authorised EMI provides a UK payment account with access to the Faster Payments Scheme — meaning a Bermuda company can receive GBP in real time from UK bank accounts without a UK office, UK director, or any UK physical presence. Payments arrive within seconds, 24 hours a day.

How to receive GBP as a Bermuda company without a UK bank account?

The most direct route is opening a UK payment account via an FCA-authorised EMI. This provides a named UK sort code and account number that accepts GBP Faster Payments, CHAPS, and SWIFT inbound. Alternative approaches — offshore GBP accounts or SWIFT-only receipt arrangements — are slower and carry correspondent banking fees of £15–£30 per incoming transaction.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)