•

•

Faster Payments UK: How Businesses Can Access Same-Day GBP Transfers

A UK e-commerce business pays 40 domestic suppliers every Monday via Bacs. Three days later, two suppliers are chasing the finance team. One payment bounced on a sort code error; the other sat in a queue over a weekend fraud check. That three-day wait is entirely avoidable.

The Faster Payments System (FPS) settles GBP transfers between UK bank accounts in seconds — 24 hours a day, 365 days a year. No cut-off. No three-day cycle. No £25 CHAPS fee. Most UK businesses are already using it without realising it — every time a banking app shows an instant transfer, that's FPS.

This guide explains how FPS works, the three access routes for UK businesses (including FCA-authorised EMI accounts), how Direct Corporate Access enables batch same-day payments, and what Confirmation of Payee means for daily operations.

[aa key-takeaways]

Key Takeaways

Faster Payments (FPS) is the UK's real-time payment infrastructure, operated by Pay.UK, processing GBP transfers between UK bank accounts in seconds — 24/7/365, including weekends and bank holidays.

UK businesses access FPS via a traditional bank account, an indirect participant arrangement, or an FCA-authorised EMI — no traditional bank relationship required for the latter two.

The scheme supports transfers up to £1 million per transaction; individual provider limits may be lower.

Confirmation of Payee (CoP) checks the account holder name against the sort code and account number before each payment — a mandatory step since 2020 that prevents misdirected payments and APP fraud.

Direct Corporate Access (DCA) lets businesses submit bulk GBP payment files directly to FPS — same-day settlement speed, batch processing efficiency.

FCA-authorised EMIs access FPS via regulated banking partners, providing identical settlement speed to a traditional bank — typically with faster onboarding.

[aa btn]Open a GBP Business Account[/aa]

[/aa]

What Is the UK Faster Payments System and How Does It Work?

The Faster Payments System (FPS) is a UK real-time payment infrastructure, operated by Pay.UK, that processes GBP transfers between UK bank accounts in seconds — 24 hours a day, 365 days a year.

FPS launched in May 2008, replacing a system where bank-to-bank GBP transfers took up to three business days. Before that, paying a supplier on Friday meant hoping the funds arrived by Wednesday.

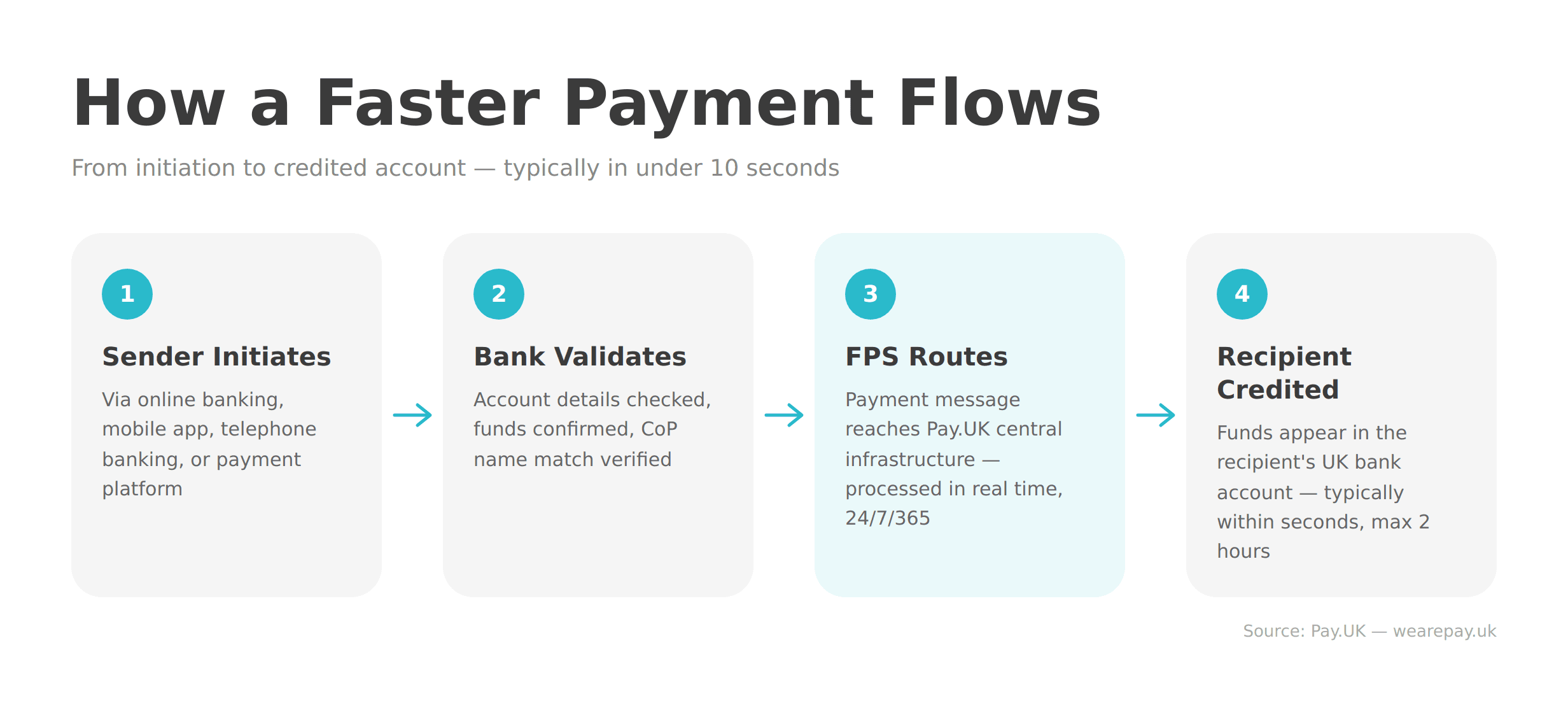

Here is how a standard Faster Payment flows:

The sender initiates a transfer via online banking, mobile app, telephone banking, or a payment platform.

The sender's bank validates the account details and checks available funds.

The payment message reaches the FPS central infrastructure, operated by Pay.UK.

The recipient's bank receives the message, performs its own checks, and credits the account — typically within seconds.

Most transfers complete in under 10 seconds. In rare cases — when either institution applies additional fraud or compliance checks — the process can take up to two hours. Pay.UK's rules guarantee funds arrive no later than the end of the following business day, but two-hour processing is the exception, not the norm.

As of May 2025, the scheme has 46 direct participants. In 2024, FPS processed 5.09 billion transactions worth £4.2 trillion — making it the backbone of UK domestic GBP payments.

[aa fast-fact]

Fast Fact: In 2024, the UK Faster Payments System processed £4.2 trillion across 5.09 billion transactions — operating 24 hours a day, every day of the year.

[/aa]

The Four Payment Types FPS Supports

FPS handles four distinct payment types. Single immediate payments — the most common — are one-off real-time transfers, available 24/7. Forward-dated payments are one-off transfers scheduled for a future date. Standing orders are fixed recurring payments, typically processed Monday to Friday. Direct Corporate Access (DCA) is a batch payment service for businesses submitting multiple payments simultaneously — same file format as Bacs, Faster Payments settlement speed. Not all providers offer DCA; confirm access before building batch workflows around it.

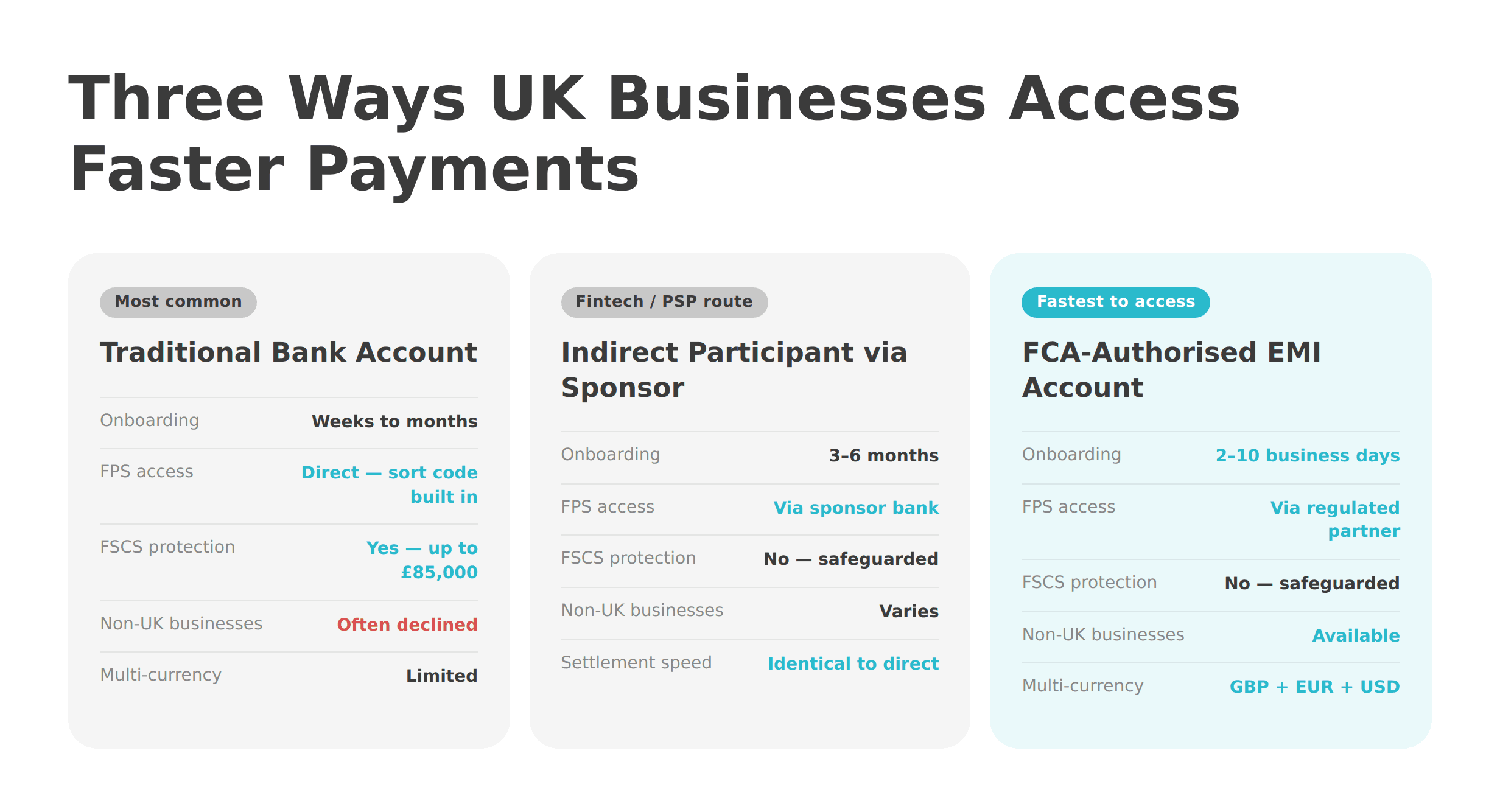

How Do UK Businesses Access the Faster Payments Network?

UK businesses access FPS in three ways: through a traditional bank account at a direct participant, through an indirect participant arrangement via a sponsoring institution, or through an FCA-authorised EMI with FPS connectivity.

The access route determines onboarding speed, operational flexibility, and whether multi-currency capability is available alongside GBP.

Route 1: Traditional Bank Account

The most common route. Open a GBP business account at a direct FPS participant — the bank provides a sort code and account number connected to the FPS network, and Faster Payments access is built in. Major UK banks (Barclays, HSBC, Lloyds, NatWest) and challenger banks (Starling, Monzo) are direct participants. The drawback: onboarding takes weeks or months, particularly for non-UK businesses or sectors banks consider higher risk.

Route 2: Indirect Participant via Sponsor Bank

Fintechs and payment service providers can access FPS as indirect participants, routing payments through a direct participant sponsor that handles clearing and settlement. This deploys in 3–6 months versus 12–18 months for direct membership, with no Bank of England settlement account required.

Route 3: FCA-Authorised EMI Account

FCA-authorised Electronic Money Institutions — regulated under the Electronic Money Regulations 2011 — can provide businesses with a named GBP account carrying a dedicated sort code and account number. These accounts connect to FPS via the EMI's regulated banking partner, delivering identical settlement speed to a traditional bank.

How do UK businesses access the Faster Payments network via this route? The process is simpler than most expect: submit KYB and AML documentation, pass the EMI's compliance review (typically 2–10 business days), and receive a named GBP account ready for Faster Payments. No branch visits. No lengthy credit assessment.

The key distinction between an FCA-authorised EMI and a traditional bank account lies in fund protection. EMI client funds are safeguarded in segregated accounts — protected, but not covered by the Financial Services Compensation Scheme (FSCS) as bank deposits are. For businesses prioritising speed of access, multi-currency capability, or non-UK registration, the EMI route is often the more practical path to FPS.

Same-Day GBP Transfers via Faster Payments: Settlement, Limits, and Cut-Off Times

Faster Payments delivers same-day — typically instant — GBP settlement, with no cut-off time for single immediate payments.

Same-day GBP transfer via Faster Payments for business works because the scheme runs continuously. A transfer at 11:58 p.m. on a Sunday processes identically to one at 9:00 a.m. on a Tuesday. No banking hours. No weekend penalties.

This is the core difference from CHAPS, which runs only Monday to Friday during business hours, costs £20–£35 per transaction, and stalls if the cut-off — typically 3:00–5:00 p.m. — is missed.

Transaction Limits

The FPS scheme maximum is £1 million per transaction — Pay.UK raised this limit from £250,000 in February 2022. Individual banks and EMIs may set lower limits. For the vast majority of UK business payments — supplier invoices, contractor fees, intra-company transfers — the ceiling is more than sufficient. Above £1 million, CHAPS is the appropriate route.

Step-by-step: same-day GBP T+0 settlement via a UK Faster Payments business account works as follows — the sender initiates the transfer, FPS central infrastructure processes the message, and the recipient's account is credited, typically within seconds.

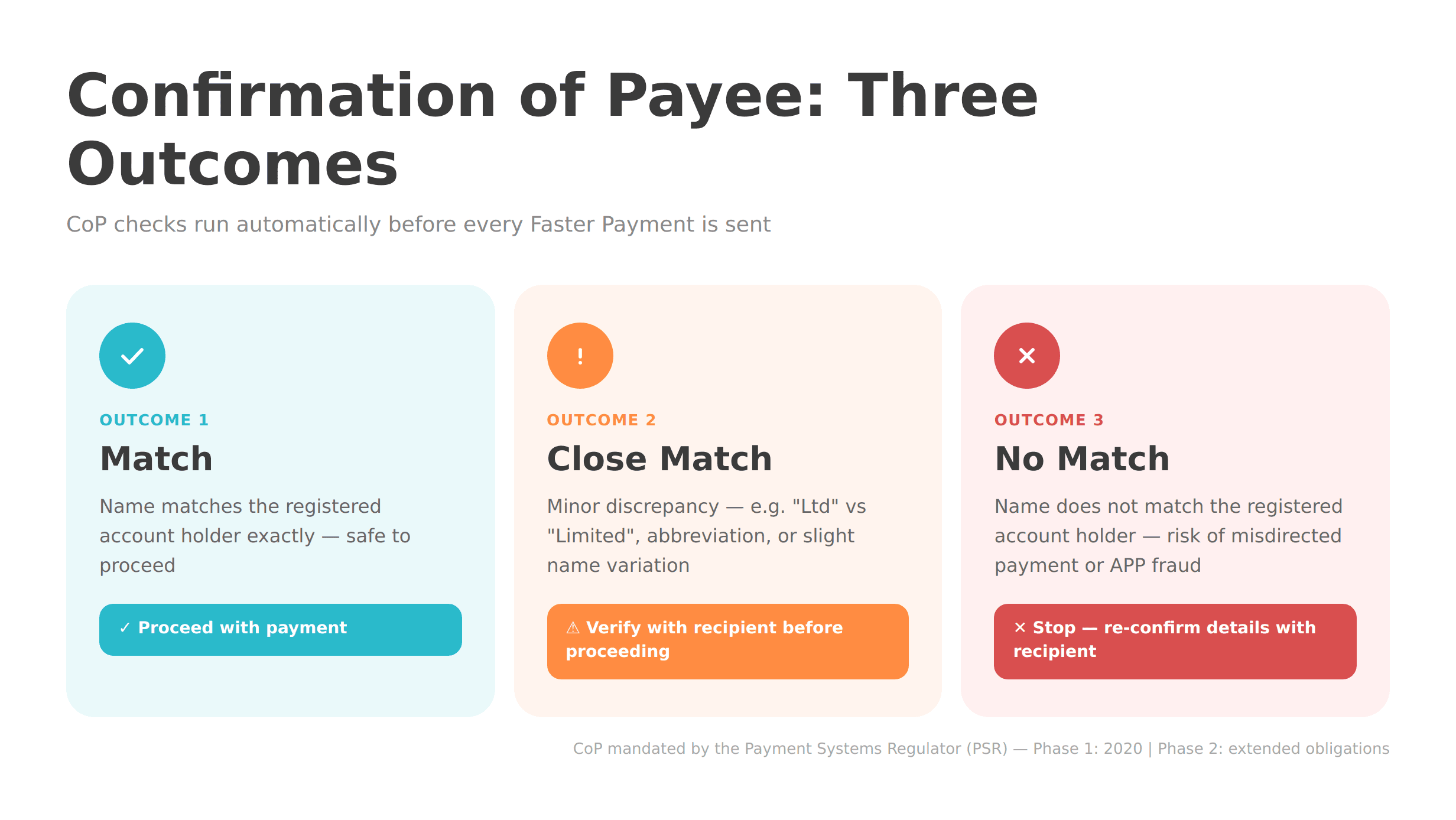

Confirmation of Payee: What It Is and Why It Matters

Confirmation of Payee (CoP) is a name-checking service, introduced in 2020, that verifies whether the account holder name matches the sort code and account number before a Faster Payment is sent.

CoP reduces two problems: payments misdirected by keying errors, and Authorised Push Payment (APP) fraud. The Payment Systems Regulator mandated CoP for the largest UK banks in 2020, with Phase 2 extending obligations further.

When a business initiates a Faster Payment, CoP runs automatically with three possible outcomes:

Outcome | Meaning | Action |

|---|---|---|

Match | Name matches registered account holder | Proceed |

Close Match | Minor discrepancy — e.g. "Ltd" vs "Limited" | Verify with recipient before proceeding |

No Match | Name does not match | Do not proceed; re-confirm details |

A No Match does not block the payment automatically — but treating it as a hard stop is sound practice for high-value transfers.

What CoP Means for Batch Payment Runs

Every entry in a DCA batch file is subject to CoP validation at the individual transaction level. A beneficiary stored as a trading name rather than their bank-registered legal name will generate a Close Match or No Match — flagging errors before the batch processes. The fix: maintain a verified beneficiary register with legal names only. "Acme Trading Ltd" and "Acme Ltd" are not the same to a CoP check.

Direct Corporate Access: Batch Faster Payments for Business

Direct Corporate Access (DCA) is an FPS payment type that allows businesses to submit bulk GBP payment files to the scheme — combining the settlement speed of Faster Payments with the operational efficiency of batch processing.

DCA is the relevant capability for payroll teams processing large numbers of payments, finance teams running weekly supplier payment cycles, and platforms disbursing mass payouts at scale. Batch payment files submitted via CSV follow the same structured format used for payroll uploads processed through Faster Payments — a familiar workflow for finance teams already using Bacs batch processing.

Key operational details for DCA:

Transaction limits: up to £1 million per individual payment in the batch (same as single FPS)

Settlement: near-instant once the batch processes — no three-day Bacs wait

Cut-off times: DCA batches may have provider-specific submission windows; a missed window queues the batch to the next business day. Confirm cut-off before scheduling runs.

Availability: not all providers offer DCA — confirm during account selection

The same infrastructure that powers instant GBP supplier payments also enables mass affiliate payout runs — a single DCA batch can disburse to hundreds of partners with near-instant settlement to each UK account.

[aa cta]

Run same-day GBP payment runs without CHAPS fees

A named UK GBP account with a dedicated sort code and Faster Payments access — no high street bank account required.

[aa btn]Open a GBP Business Account[/aa]

[/aa]

Faster Payments vs CHAPS vs Bacs: Choosing the Right Rail

For most business payments, the decision between the three UK GBP payment rails comes down to urgency, value, and volume.

Faster Payments (FPS) | CHAPS | Bacs | |

|---|---|---|---|

Speed | Seconds (max 2 hours) | Same day (business hours only) | 3 business days |

Availability | 24/7/365 | Monday–Friday, business hours | Monday–Friday |

Per-transaction limit | Up to £1 million | No upper limit | No standard limit |

Typical cost | Free or near-free | £20–£35 | Very low |

Best for | All same-day GBP under £1m | High-value transactions above £1m or where formal settlement confirmation is contractually required | Scheduled, recurring, high-volume payments |

Default to Faster Payments for any GBP payment under £1 million requiring same-day settlement. Use CHAPS only when the value exceeds £1 million or a contract requires a formal settlement confirmation — common in property and large corporate deals. Use Bacs for payroll and scheduled supplier payments where a three-day cycle is acceptable.

The cost difference is concrete: 100 CHAPS transfers at £25 each costs £2,500 a month. Faster Payments delivers the same same-day outcome for near-zero cost.

How to Access Faster Payments via an FCA EMI: Step by Step

For businesses that cannot open a traditional UK bank account — or those seeking faster onboarding and multi-currency capability — an FCA-authorised EMI provides identical FPS access with a simpler setup.

Here is how to access the UK Faster Payments network via an FCA EMI without opening a bank account:

Step 1 — Verify FCA authorisation. Search the FCA Financial Services Register and confirm the provider's status reads "Authorised Electronic Money Institution."

Step 2 — Submit KYB documentation. Standard requirements: Certificate of Incorporation, proof of registered address, director ID, UBO declaration, and intended payment volumes.

Step 3 — Complete AML/compliance review. Most FCA-authorised EMIs complete standard reviews in 2–10 business days.

Step 4 — Receive a named GBP account. The EMI issues a UK GBP account with a dedicated sort code and account number, connected to FPS via the EMI's regulated banking partner. From the recipient's perspective, the payment is identical to one sent from a traditional bank.

Step 5 — Initiate Faster Payments via the EMI's dashboard, API, or DCA batch upload.

Businesses holding GBP alongside EUR and USD in a single multi-currency UK account can route GBP via Faster Payments and EUR payments via SEPA from the same account — one onboarding, one account structure.

FAQ

How do UK businesses access the Faster Payments network?

UK businesses access FPS via a traditional bank account at a direct FPS participant, an indirect participant arrangement via a sponsoring institution, or through an FCA-authorised EMI. EMIs provide a named GBP account with a dedicated sort code and account number connected to FPS via a regulated banking partner — no bank licence required. Most EMI onboarding completes within 2–10 business days, significantly faster than traditional bank account opening for many business types.

What is the Faster Payments cut-off time for business transactions in the UK?

Single immediate Faster Payments have no cut-off — the scheme operates 24/7/365, including weekends and bank holidays. DCA batch submissions may have provider-specific processing windows; confirm the exact cut-off with your bank or EMI before scheduling payment runs. A batch submitted after the provider's DCA window will queue to the next business day.

How do I send a same-day GBP transfer via Faster Payments as a UK business?

Open a GBP business account with a bank or FCA-authorised EMI connected to the FPS network. Initiate a single immediate payment by entering the recipient's sort code, account number, and exact registered name. Confirmation of Payee validates the details automatically. On submission, the transfer is typically credited within seconds — guaranteed within 2 hours and by the end of the following business day at the latest.

How do I access the UK Faster Payments network via an FCA EMI without opening a bank account?

Apply for a business account with an FCA-authorised EMI — verify status on the FCA Financial Services Register. Submit KYB documentation, complete the AML review, and receive a named UK GBP account with a sort code linked to the FPS network. The EMI connects to Faster Payments via its regulated banking partner, providing the same network access and settlement speed as a traditional bank without requiring FSCS-covered deposits.

What is the difference between Faster Payments and CHAPS for business GBP transfers in the UK?

Faster Payments settles in seconds (maximum 2 hours), operates 24/7/365, and is free or near-free for transfers up to £1 million. CHAPS guarantees same-day settlement during business hours only — Monday to Friday — and costs £20–£35 per transaction. For most business payments under £1 million requiring same-day settlement, Faster Payments delivers equivalent speed at a fraction of the cost. CHAPS is appropriate only when the transfer value exceeds £1 million or a formal settlement confirmation is contractually required.

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)