•

•

Multi-Currency Account UK: Hold GBP, EUR and USD in One Place

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

Key Takeaways

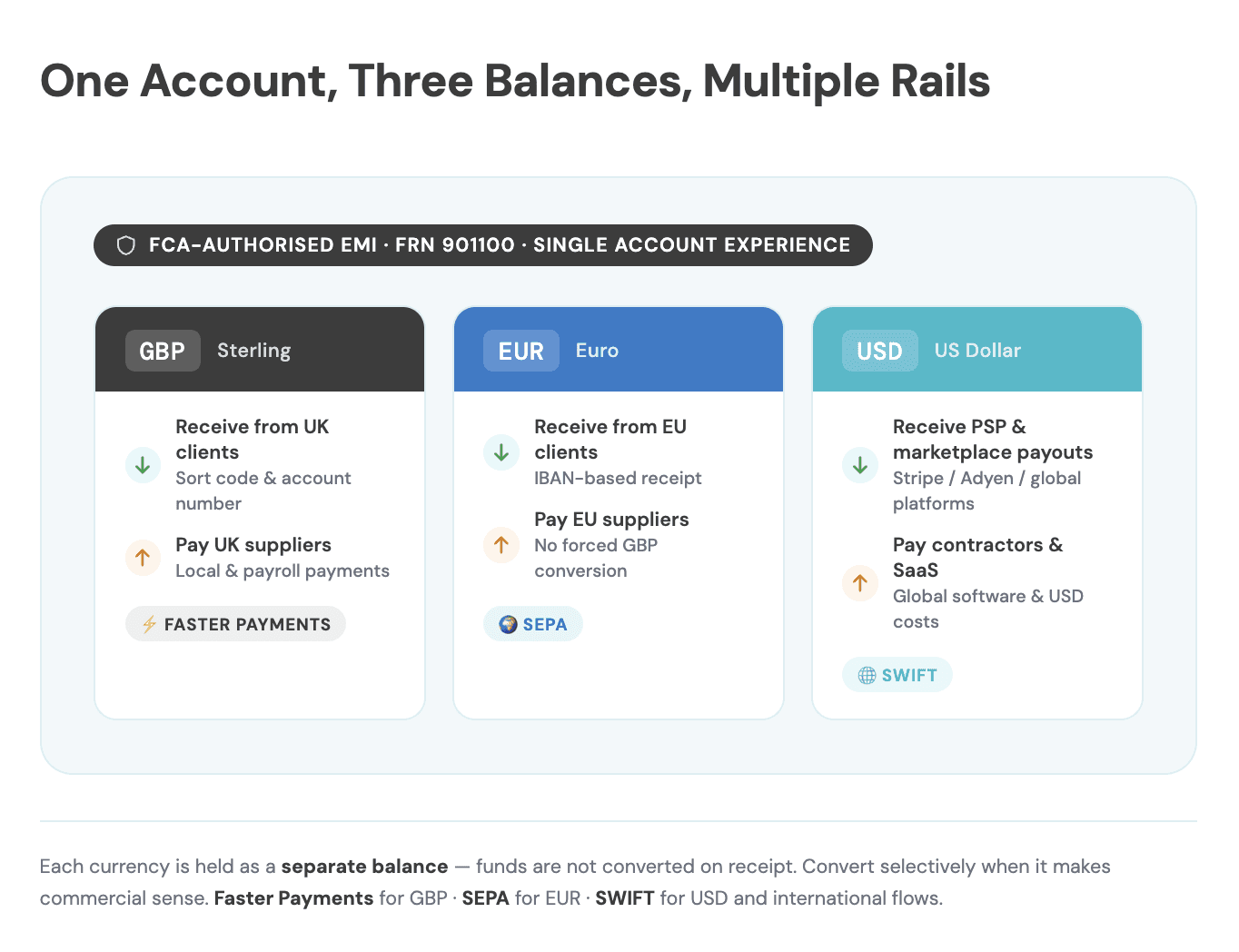

A multi-currency account holds GBP, EUR, and USD as separate balances — funds do not have to convert on receipt.

Faster Payments and SEPA solve different parts of the same workflow: one moves sterling in near-real time across UK accounts; the other moves euros across European banking infrastructure.

An FCA-authorised EMI is not a bank. Client money is protected through safeguarding arrangements — not the FSCS.

Separate currency balances give a business control over when to convert, not just how much it costs — a distinction that directly affects supplier payment timing and FX margin.

Choosing a provider on fees alone is the most common mistake in this category. Payment rail access, local receiving details, and onboarding fit matter more for operational performance.

Who This Guide Is For

Likely a good fit if you:

Run a UK-based SME, consultancy, e-commerce operation, or SaaS business that regularly sends or receives EUR and USD

Use Stripe, Adyen, or similar PSPs and want to hold settlement funds in their original currency

Pay EU or international suppliers and want to avoid converting GBP to EUR on every transaction

Invoice clients in multiple currencies and want control over when revenue gets exchanged

Less relevant if you:

Only operate in GBP with no regular EUR or USD flows

Need FSCS deposit protection on working capital balances

Are in a restricted industry or jurisdiction that falls outside standard EMI eligibility

What is a Multi-Currency Account?

A multi-currency account is an account structure that lets a business or professional hold, send, and receive more than one currency without automatically converting between them. The funds sit in separate currency balances — GBP stays GBP, EUR stays EUR — until the account holder decides to exchange.

Snippet definition: A UK multi-currency account lets a business hold GBP, EUR, and USD as separate balances under one account setup, so funds are not converted on receipt.

That distinction matters. Many businesses assume "multi-currency" simply means "a dashboard that shows multiple currencies." In practice, the difference between a genuine multi-currency account and a basic FX conversion facility lies in the holding model: does GBP received from a UK client remain in GBP until you choose otherwise, or is it converted automatically at the moment of receipt?

As EQWIRE's e-commerce account guide explains directly, the product is not the same as a high-street foreign currency account and not the same as a PayPal balance. That framing is useful regardless of which provider a business evaluates — the holding model is the starting point of any serious comparison.

A practical example: A UK consultancy invoices a Berlin firm in EUR and a New York agency in USD. Without a multi-currency account GBP EUR USD UK setup, both receipts convert to GBP on arrival. With separate balances, the business holds EUR to pay a European contractor the following month and holds USD to cover a recurring SaaS subscription — both without paying two unnecessary conversion spreads.

Why GBP, EUR and USD — Why These Three?

For many UK businesses trading domestically, across Europe, and with global software or marketplace providers, GBP, EUR, and USD are the three currencies that appear most often in day-to-day operations. That is a practical generalisation, not a universal rule — but it holds across most of the business types this account structure is built for.

GBP covers domestic UK operations: client invoices, local supplier payments, payroll, and tax obligations. A UK sort code and account number connected to Faster Payments is the operational baseline for any business with sterling flows.

EUR covers European trade. Import/export businesses paying German manufacturers, consultancies billing French clients, and e-commerce operations receiving payouts from EU marketplace buyers all encounter regular EUR obligations. Holding EUR from inbound receipts and paying out from that balance removes two conversion events per cycle.

USD covers the global layer. Cloud infrastructure (AWS, Google Cloud), SaaS platforms, US-based contractors, and international marketplaces predominantly operate in dollars. For a SaaS company paying monthly tool subscriptions or an e-commerce merchant receiving USD platform settlements, holding dollars directly avoids recurring FX friction on predictable costs.

The false assumption worth challenging: three currencies does not mean three providers or three onboarding processes. The right business multi-currency account UK online setup manages all three under one compliance relationship, one set of receiving details, and one account interface.

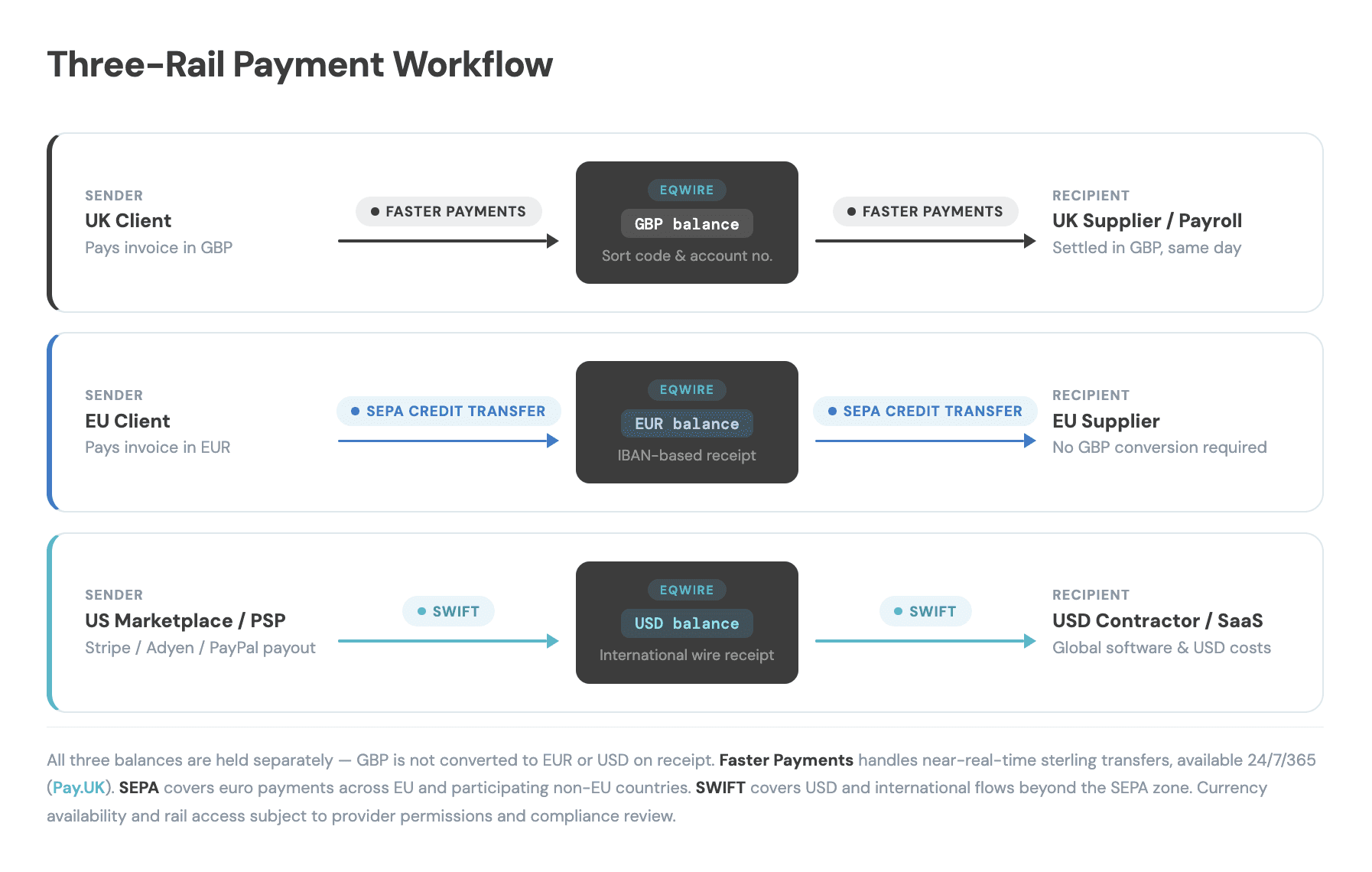

How the Payment Rails Work: Faster Payments, SEPA, and SWIFT

Understanding which rail moves which currency — and how — is one of the most practically important questions to ask before choosing a provider. Many accounts advertise multi-currency support without making the rail infrastructure transparent.

Faster Payments (GBP)

Faster Payments is the UK domestic infrastructure for near-real-time sterling transfers. Pay.UK states it operates around the clock, 365 days a year, and supports individual payments up to £1 million — though individual provider limits may apply. For a UK business, Faster Payments access means GBP received from clients arrives within seconds, and GBP sent to suppliers clears the same way. It requires a UK sort code and account number.

SEPA (EUR)

SEPA — the Single Euro Payments Area — is the standardised euro payment framework that connects banks and payment institutions across EU member states and a number of participating non-EU countries. The ECB describes SEPA as enabling fast, safe, and efficient euro payments across the participating region. SEPA Credit Transfer and SEPA Instant (where available) allow euro payments to route by IBAN without the cost and delay of international correspondent banking chains.

Important distinction: holding EUR in an account is not the same as having SEPA-connected sending and receiving capability. That depends on the provider's infrastructure and regulatory authorisations. Always confirm whether a provider supports both incoming and outgoing SEPA flows — not just balance holding.

SWIFT and international rails (USD and beyond)

SWIFT remains the standard for USD transactions, payments outside the SEPA zone, and larger international transfers. A multi-currency account that genuinely covers GBP, EUR, and USD needs direct or indirect access to all three rails — FPS for sterling, SEPA for euros, SWIFT or equivalent for dollars and international flows.

EQWIRE's account frames its offer around all three: FPS, SEPA, and SWIFT. Any business evaluating a UK multi-currency account with Faster Payments and SEPA access should verify this capability at provider level before applying.

💡 Rail access matters as much as currency support EQWIRE provides GBP, EUR, and USD accounts with Faster Payments, SEPA, and SWIFT access — structured for UK businesses that collect domestically, trade in Europe, and operate globally. Review the service overview and regulatory information at eqwire.com before deciding.

Multi-Currency Account vs Foreign Currency Account vs Traditional Business Bank Account

These three structures appear interchangeably in most comparison content. They are not equivalent.

Traditional business bank account | Foreign currency account (bank) | Multi-currency EMI account | |

|---|---|---|---|

Balance model | GBP base, conversion on receipt typical | GBP + additional currencies, varies by bank | Separate GBP, EUR, USD balances |

Local receiving details | UK sort code / account number | Often GBP-only; EUR IBAN may not be issued | GBP sort code, EUR IBAN, USD routing details |

Conversion timing | Often automatic | Provider-dependent | Account holder controls timing |

Payment rails | FPS, CHAPS | FPS + SWIFT (varies) | FPS, SEPA, SWIFT |

Client money protection | FSCS up to £85,000 per eligible depositor | FSCS (same bank) | EMI safeguarding — not FSCS |

Onboarding | Weeks to months, often branch-led | Similar to bank onboarding | Digital, KYB/KYC-led, typically faster |

Regulatory structure | Authorised bank | Authorised bank | FCA-authorised EMI |

A foreign currency account at a high-street bank may allow a business to hold one or two additional currencies alongside GBP. But onboarding tends to be slower, IBAN issuance for EUR is not guaranteed, and the conversion model may still convert receipts automatically unless configured otherwise.

A multi-currency EMI account is designed around digital onboarding, local receiving detail issuance, and connected payment rails. The trade-off is client money protection: funds are safeguarded, not deposit-protected. That distinction is covered directly in the next section.

FCA-Authorised EMI: What It Means and How Client Money is Protected

Is an EMI the same as a bank? No. An EMI issues electronic money and provides payment services. It is regulated by the FCA but does not hold a banking licence. The protection model for client money is different — and businesses should understand that before holding significant operational balances.

How safeguarding works: The FCA requires EMIs and authorised payment institutions to safeguard client funds — typically by placing them in a segregated account at a regulated bank, or by holding equivalent insurance or a comparable guarantee. The FCA states clearly that funds held by payment and e-money firms are not directly protected by the FSCS, and that while customers should generally receive most of their money back if a firm fails, the process may take time and the full amount may not be returned after costs are deducted.

What safeguarding is: A structural protection that keeps client money separate from the firm's own funds, reducing — but not eliminating — risk in a failure scenario.

What safeguarding is not: A guarantee equivalent to FSCS deposit protection. Businesses holding large operational balances in an EMI account should factor this into their treasury and risk policies.

Regulatory note:

EQWIRE is an FCA-authorised EMI, FRN 901100

Client funds are safeguarded, not FSCS-protected

EMI authorisation can be verified on the FCA register

Full regulatory disclosures: eqwire.com/important-information

Any business evaluating a best business multi-currency account UK EMI setup should read the provider's regulatory disclosure page — not just the product marketing — to understand precisely how funds are held and what recourse exists.

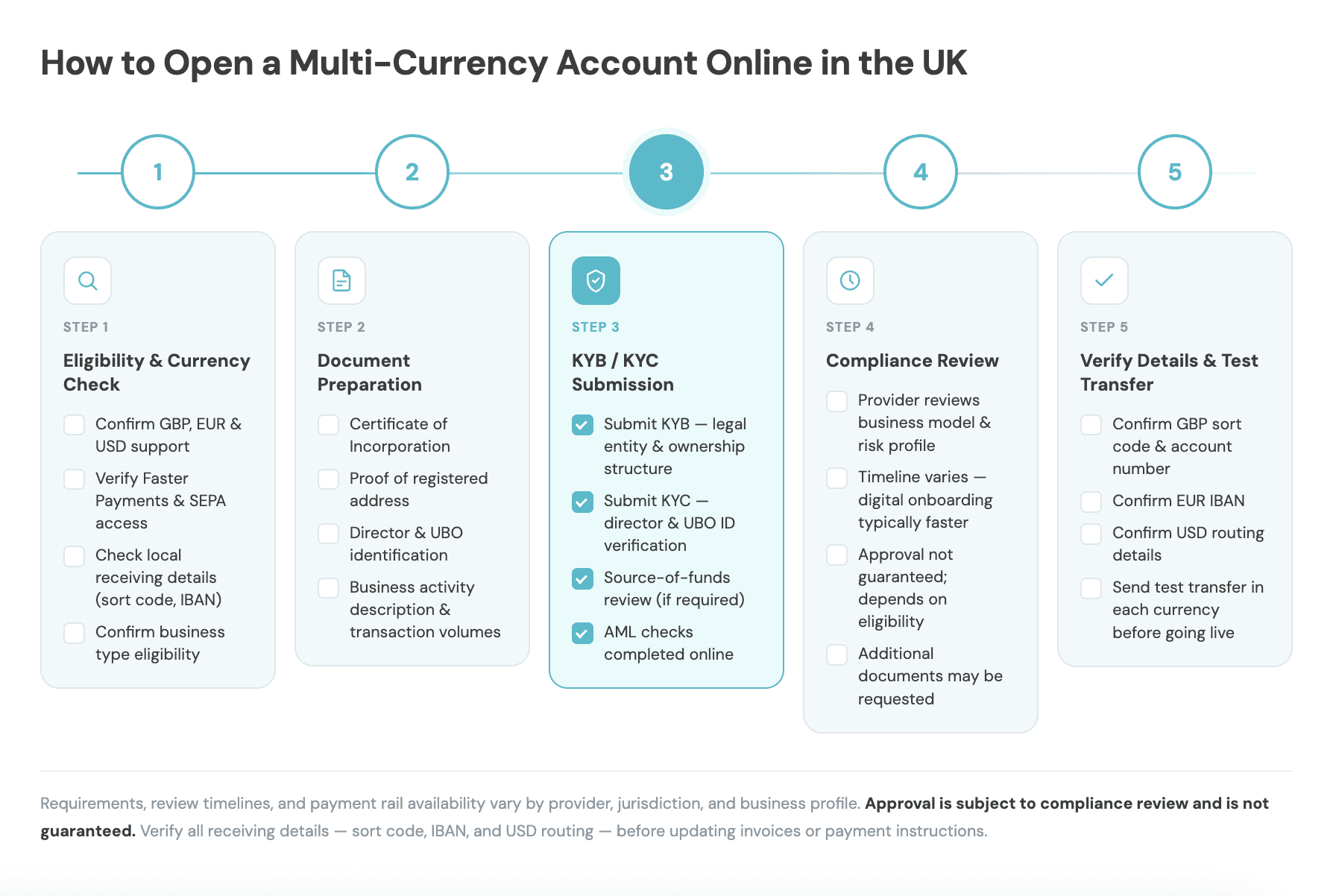

How to Open a Multi-Currency Account Online in the UK

Most FCA-authorised EMI providers offer fully digital onboarding — no branch visit required. The steps below reflect common practice, though specific requirements vary by provider, business type, and risk profile.

Step 1: Confirm the account actually fits your workflow Before starting: verify that the provider issues a UK sort code for GBP, an IBAN for EUR, and proper USD receiving details. Confirm Faster Payments and SEPA access for both incoming and outgoing flows. Check the EQWIRE currency list if broader currency coverage is relevant to your business.

Step 2: Prepare KYB and KYC documentation For a UK Ltd company, expect to provide: Certificate of Incorporation, registered address confirmation, details of directors and Ultimate Beneficial Owners (UBOs holding 25% or more), and a description of business activity and transaction volumes.

For an international company with UK payment flows, additional documentation is typically required depending on the provider's jurisdiction policies.

For a freelancer or self-employed professional, identification documents, proof of address, and evidence of professional activity are the standard baseline.

Step 3: Submit the application and complete compliance review KYB checks verify the legal entity and its ownership structure. KYC checks verify the identity of directors and UBOs via government-issued ID. Most digital providers run both online. Approval timelines vary materially by business type, risk profile, and application completeness — digital-first onboarding can be faster than branch-led banking, but timelines are not uniform and approval is not guaranteed.

Step 4: Verify receiving details before going live Once approved, confirm the exact sort code and account number for GBP, the IBAN for EUR, and USD routing details. Send a small test transfer in each currency before updating invoices or payment instructions.

What to Compare Before Choosing a UK Multi-Currency Account

A low-fee account is the wrong choice if it cannot issue the right receiving details, route euro payments over SEPA, or support your PSP payout flow. Build the comparison around operational fit, not headline pricing.

Holding model Does each currency sit in a genuinely separate balance, or does the account convert on receipt into a base currency? This single question determines whether the account solves the conversion-timing problem.

Local receiving details Does the provider issue a UK sort code and account number for GBP, a real IBAN for EUR, and USD routing details? Some providers hold currencies without issuing local-style receiving, which means counterparties cannot pay in via domestic rails.

Payment rail access — incoming and outgoing Confirm Faster Payments, SEPA, and SWIFT for both directions. Some providers support inbound only on certain rails. That limits utility for supplier payments or international disbursements.

FX costs and conversion control What is the FX spread? Is conversion triggered automatically or only on instruction? For an SME paying EUR suppliers from GBP revenue, spread costs on every receipt and every outgoing payment compound quickly across a year.

Onboarding fit Is the application process designed for your entity type — UK Ltd, international company, sole trader, or professional individual? Eligibility criteria and document requirements differ, and restricted industries may not qualify regardless of structure.

PSP settlement and supplier workflow compatibility For e-commerce businesses or digital platforms receiving payouts from Stripe, Adyen, or similar processors, verify that the provider's receiving details are compatible with the PSP payout configuration. EQWIRE's Stripe settlement account guide covers this workflow in detail.

Regulatory clarity Verify the provider's FCA registration, EMI authorisation status, and safeguarding disclosures independently via the FCA register before opening.

Which Businesses Benefit Most from This Structure?

SMBs with European trade exposure A UK importer buying from German or Italian suppliers faces a recurring EUR obligation each month. Holding EUR from sales receipts and paying suppliers directly from that balance removes two conversion events — the inbound receipt and the outgoing payment — each carrying a spread.

E-commerce businesses receiving PSP settlements Marketplace and payment processor payouts often arrive in the currency of sale: GBP from UK buyers, EUR from European customers, USD from US or global platforms. Holding each settlement in its original currency avoids forced conversion and allows funds to be deployed in the right currency when needed. For more on this workflow, see EQWIRE's e-commerce operating account guide.

SaaS and digital platforms Software businesses often collect revenue in GBP and EUR while paying for infrastructure, tools, and contractors in USD. Holding USD from US client payments or licensing income reduces the cost of recurring dollar-denominated expenses that recur every billing cycle.

Import/export and trade businesses Companies managing supplier payment schedules benefit from balance separation because they can time conversions around exchange rate conditions rather than converting on receipt under whatever rate is current at that moment.

Freelancers and global professionals A UK-based consultant invoicing a Frankfurt firm in EUR and a New York client in USD benefits from holding both currencies without converting to GBP immediately. EQWIRE explicitly addresses freelancers and professionally active individuals alongside SMEs and larger business types.

Operations and finance teams managing PSP or supplier flows Teams handling Stripe GBP settlements alongside 3PL supplier payments need a setup where receipt, holding, and disbursement happen in the right currency, without unnecessary conversion or reconciliation overhead.

Common Mistakes When Choosing a UK Multi-Currency Account

Choosing on fees alone. A zero-FX-fee account that converts on receipt, cannot issue a EUR IBAN, or is not compatible with your PSP payout setup costs more operationally than a provider with transparent fees and full rail access.

Confusing EMIs with banks. An EMI account is not a bank account. The protection model is different, the regulatory structure is different, and the operational constraints are different. Understanding this before opening — especially for businesses holding significant working capital — is not optional.

Ignoring rail direction. Faster Payments and SEPA may be available for outgoing payments but not for incoming receipts, or vice versa. Always confirm both directions before assuming a provider supports your full workflow.

Assuming all providers issue local receiving details. Some multi-currency accounts allow balance holding but only issue one set of receiving details — typically GBP. A EUR IBAN and USD routing details are not automatic; they depend on the provider's infrastructure and permissions.

Overlooking settlement workflow fit. A general-purpose account may not be configured for PSP settlement compatibility or structured to handle batched supplier payments across currencies efficiently.

Acting on unverified currency-count claims. Supported currency lists change. Always verify against the provider's live documentation — for EQWIRE, use the live currency list — before making operational decisions based on a specific number.

EQWIRE's Offering: What the Account Actually Provides

This is EQWIRE's guide, so it is worth being direct about what EQWIRE offers — and what to verify independently before applying.

EQWIRE is an FCA-authorised electronic money institution, FRN 901100. Its account provides a single setup for GBP, EUR, and USD, with access to Faster Payments, SEPA, and SWIFT. It is designed for SMEs, e-commerce companies, consultancies, import/export operations, SaaS and digital platforms, freelancers, and professionally active individuals.

What is confirmed on the live EQWIRE site:

GBP, EUR, and USD account experience with separate balance holding

FPS, SEPA, and SWIFT access

FCA-authorised EMI status, FRN 901100

Safeguarding of client funds (not FSCS-protected)

Digital onboarding, no branch visit required

What to verify directly before applying:

Full list of supported currencies: eqwire.com/currency-list

Regulatory and safeguarding disclosures: eqwire.com/important-information

Eligibility for your specific business type and jurisdiction

EQWIRE is one option in a broader market. The evaluation framework in this guide — holding model, rail access, local receiving details, FX costs, onboarding fit, and regulatory structure — applies equally to any provider being assessed.

Conclusion

The right UK multi-currency account is less about finding a single "best" product and more about matching a specific configuration to a specific operational reality. For businesses that collect GBP domestically, trade in EUR across Europe, and encounter USD through global platforms, software, or marketplaces, holding all three currencies separately — with Faster Payments, SEPA, and SWIFT access — removes a layer of conversion friction that compounds across every payment cycle.

The account structure, the holding model, the payment rails, and the client money framework all matter. An EMI account is not a bank account. Safeguarding is not FSCS protection. Faster Payments and SEPA solve different problems. Local receiving details are not a given.

For businesses evaluating a business multi-currency account UK online setup, the starting point is understanding what your payment flows actually require — then confirming, provider by provider, whether the infrastructure matches. EQWIRE's service overview and regulatory disclosures are available to review before applying.

Features, currency availability, rail access, and onboarding timelines vary by provider and customer profile. Approval is subject to compliance review and eligibility assessment. EQWIRE is an FCA-authorised EMI (FRN 901100); client funds are safeguarded, not FSCS-protected.

FAQ

How do I open a multi-currency account online in the UK?

The process typically involves confirming that the provider issues local receiving details for GBP, EUR, and USD, verifying Faster Payments and SEPA access for both incoming and outgoing flows, and preparing KYB/KYC documentation — company incorporation details, director and UBO identification, and evidence of business activity. Applications are submitted digitally, reviewed by the provider's compliance team, and approved subject to business type and risk profile. Approval timelines vary and are not guaranteed. Once approved, verify all receiving details and run a test transfer before updating invoices or payment instructions.

What is the best multi-currency business account UK for GBP EUR USD?

There is no universal answer. The right fit depends on whether the provider issues local receiving details for all three currencies, whether Faster Payments and SEPA are available for both incoming and outgoing flows, how the FX conversion model works, and whether the onboarding process matches your entity type. An SME paying European suppliers has different requirements from a SaaS platform managing PSP settlements. Evaluate providers against your specific payment workflow — not brand recognition or headline fees.

Can a UK multi-currency account include Faster Payments and SEPA access?

Some providers support both, but not all do so in the same way or for both directions. Pay.UK describes Faster Payments as operating around the clock, 365 days a year, for near-real-time sterling transfers up to £1 million (subject to individual provider limits). SEPA covers euro transfers across EU and participating non-EU countries. Confirm incoming and outgoing capability for each rail with the specific provider before opening.

Is a multi-currency account the same as a bank account?

No. A multi-currency account offered by an FCA-authorised EMI is not a bank account. Bank deposits held at UK-authorised banks are covered by the FSCS up to £85,000 per eligible depositor. EMI balances are safeguarded — held separately from the firm's own funds in a segregated account — but are not FSCS-protected. The FCA states that funds held by payment and e-money firms are not directly covered by the FSCS, and that recovery in a failure scenario may take time and may not represent the full balance after costs.

Can a business multi-currency account be used for supplier payments and PSP settlements?

Yes, and for many businesses this is the primary use case. Holding GBP, EUR, and USD in separate balances allows settlements from PSPs to remain in their original currency and supplier payments to go out in the correct currency — without converting twice. EQWIRE's 3PL supplier payment guide and Stripe settlement guide cover these workflows in more detail.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)