•

•

FCA-Authorised EMI vs Bank UK: Key Differences for Business Accounts

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

An FCA-authorised EMI is a regulated non-bank that issues e-money and provides payment services. Unlike a UK bank, it does not take deposits. Customer funds are protected through safeguarding under the Electronic Money Regulations 2011, not through standard FSCS deposit cover on the EMI account balance. The protection model, lending permissions, and prudential rules are different — and those differences matter for businesses deciding how to hold and move money.

This guide explains the distinction in practical terms for finance teams, founders, and operations leads. It covers how safeguarding works, whether an EMI can hold GBP, EUR, and USD, and when to use an EMI alongside — or instead of — a traditional UK bank.

Key Takeaways

An FCA-authorised EMI is a regulated non-bank payment provider. It is not a PRA-authorised deposit taker.

EMI customer funds are protected through safeguarding under the Electronic Money Regulations 2011 — not through the FSCS deposit scheme that applies to eligible deposits at banks.

The FCA finalised a strengthened safeguarding regime in PS25/12, which takes effect on 7 May 2026.

Multi-currency capability (GBP, EUR, USD) is a product feature, not a function of bank status. Many FCA-authorised EMIs support it; many banks do not by default.

The right structure for most internationally active businesses is not "EMI or bank" but a considered combination — each used for what it does well.

EMI vs Bank UK: 7 Key Differences

The core difference is that a UK bank is a PRA-authorised deposit taker, while an FCA-authorised EMI is a regulated non-bank payment firm. The legal model, protection mechanism, and permitted activities are distinct.

FCA-Authorised EMI | PRA-Authorised UK Bank | |

|---|---|---|

Primary regulator | FCA | PRA and FCA |

Customer balance | E-money / payment account | Eligible deposit |

Money protection | Safeguarding under EMRs 2011 | FSCS up to £120,000 per eligible person per firm (from 1 Dec 2025) |

Takes deposits | No | Yes |

Can lend / overdraft | Limited — subject to FCA conditions; not from safeguarded funds | Yes |

Multi-currency balances | Provider-dependent | Provider-dependent |

Typical use case | Payments, collections, cross-border, FX | Operating account, lending, treasury, branch services |

Both institution types can look nearly identical in interface and daily use — same sort code format, same IBAN, same Faster Payments support. The difference sits in the regulatory structure underneath, not the app on the screen.

What Is an FCA-Authorised EMI in the UK?

An FCA-authorised EMI is a non-bank firm authorised by the Financial Conduct Authority to issue electronic money and provide payment services under the Electronic Money Regulations 2011.

"Electronic money" is digitally stored monetary value issued against the receipt of funds, usable for payment transactions. When a business funds an EMI account, the firm credits a payment account and holds the corresponding e-money value — it does not take that money as a bank deposit.

"FCA-authorised" means the firm is listed on the FCA Financial Services Register with permissions to issue e-money and provide payment services. Authorised EMIs hold initial capital of €350,000 and are subject to FCA oversight and safeguarding obligations. This is a meaningful regulatory threshold — not the same as being unregistered or lightly supervised.

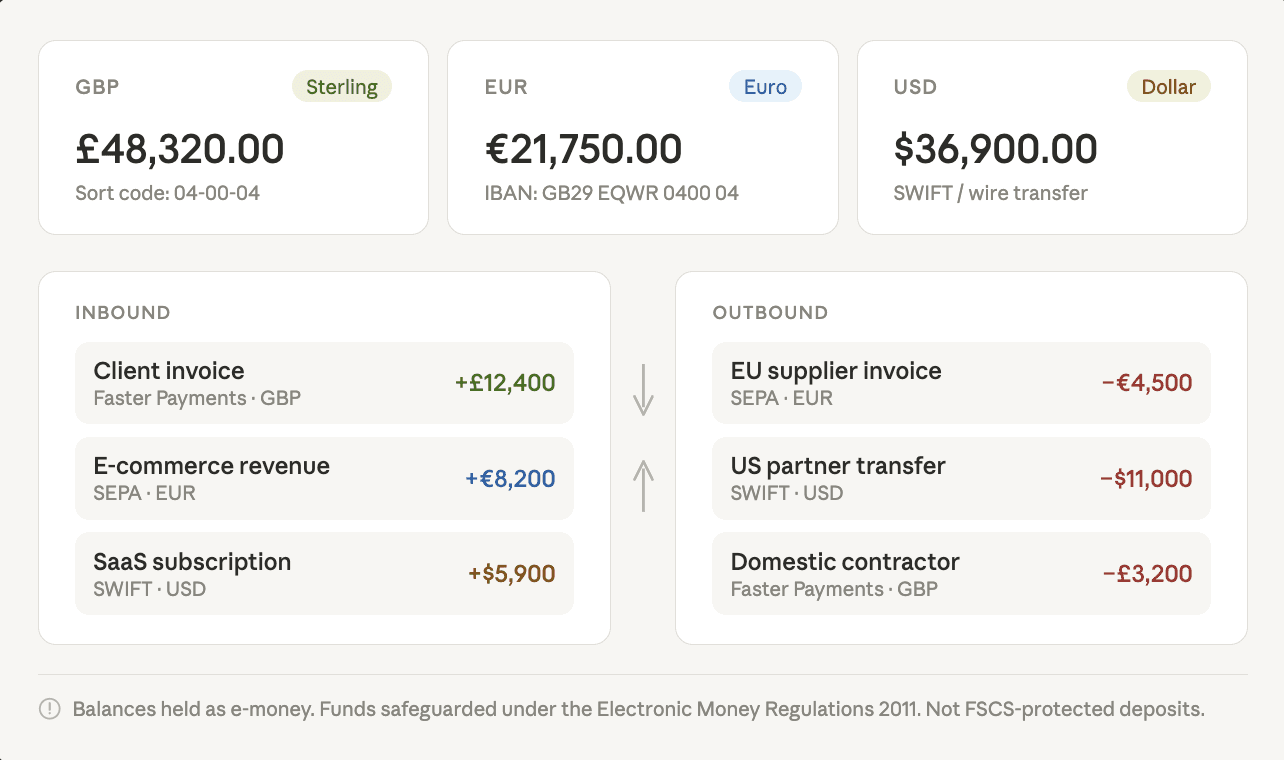

A practical example: a UK e-commerce business uses an EMI account to receive GBP customer payments, hold EUR for European supplier invoices, and send USD transfers to overseas partners — without needing a separate bank account in each currency.

How an EMI Account Works for Business Funds and Payments

An EMI account receives funds, credits e-money value, safeguards relevant customer funds, and enables payment activity in and out.

The operational flow in five steps:

Funds arrive — a client pays an invoice, or the business transfers working capital in.

The EMI credits the account — the amount is reflected as a payment-account balance.

Relevant funds are safeguarded — the EMI segregates customer money from its own and holds it at a credit institution or in qualifying assets, under FCA safeguarding requirements.

The business uses the account — sending payments, holding currency balances, converting between currencies, or receiving further inbound funds.

Funds can be redeemed or paid out — balances are available for withdrawal or onward transfer as needed.

The EMI is not lending your funds the way a bank uses retail deposits to fund loans. The model is built around payment operations. That distinction shapes both the account's capabilities and what happens to your money if something goes wrong.

Is Money in an EMI Account FSCS Protected?

EMI balances are not covered by the standard FSCS deposit scheme when an EMI itself fails. Relevant funds are instead protected through safeguarding — a separate regulatory framework with a different payout process.

This is the most important distinction for businesses holding operating funds in an EMI account.

Segregation: The EMI must hold relevant customer funds separately from its own money. Those funds sit at a credit institution or in qualifying liquid assets — ring-fenced from the firm's general balance sheet.

What happens if the EMI fails: Segregated funds should be identifiable and separable in insolvency. The FCA's position is that customers should receive most of their money back — but the process takes time, and insolvency costs such as administrator or liquidator fees may be deducted, meaning customers may not recover the full balance. This differs materially from an FSCS bank claim, which is typically processed within seven working days up to the £120,000 limit.

The FSCS and EMIs: Eligible deposits at PRA-authorised banks, building societies, and credit unions receive FSCS protection up to £120,000 per eligible person per authorised firm (since 1 December 2025). EMI balances held by the EMI itself are not eligible deposits under that scheme. A separate and distinct scenario: if the bank or credit institution holding the safeguarded funds were to fail, FSCS protection may become relevant to those funds — but that is not the same as saying the EMI account itself carries standard FSCS deposit protection.

The updated framework: The FCA finalised significant changes to the safeguarding regime in PS25/12, with new requirements taking effect on 7 May 2026. These changes introduce strengthened rules around how EMIs and payment institutions must hold, segregate, and report customer funds. Businesses should read current provider disclosures — not older fintech explainers — to understand how their money is actually held.

See how EQWIRE protects your money for a current, provider-specific description.

💡 Before choosing any payment provider, verify three things: FCA register status, safeguarding disclosure, and how the firm describes customer money protection. Read EQWIRE's regulatory disclosures and safeguarding explanation before comparing providers. Read our Important Information · How We Protect Your Money

Can an EMI Hold GBP, EUR and USD for a UK Business?

Yes — many FCA-authorised EMIs support GBP, EUR, and USD business balances, but that capability depends on the provider's product design and payment-rail setup, not on regulatory category.

Whether a specific provider supports GBP, EUR, and USD depends on its infrastructure, licences, and the corridors it has built — not on whether it is a bank or an EMI. Some banks offer only GBP for business by default. Some EMIs support a dozen currencies. The label does not determine the outcome.

For a UK SaaS company receiving USD subscription revenue, paying EUR contractors, and managing GBP operating costs, the relevant question is: does this provider support those three currencies with inbound and outbound payment capability? Providers like Wise and Airwallex have built multi-currency EMI-model infrastructure specifically for cross-border business payments. Traditional high-street banks have historically been slower to extend that to SMBs, though the gap has narrowed.

For e-commerce businesses, import/export companies, and SaaS platforms with recurring international revenue, an FCA-authorised EMI business account can cover GBP, EUR, and USD operations effectively. See EQWIRE's GBP/EUR/USD operating account guide for a concrete breakdown.

When Should a Business Use an EMI Instead of a Bank?

An EMI typically fits better when payment-flow efficiency, international reach, and multi-currency operations are the primary requirements — not lending, branch services, or FSCS-covered deposits.

Best for:

Receiving and sending cross-border payments with direct currency support and transparent fees

Holding GBP, EUR, and USD balances operationally without multiple bank relationships

Reconciling international trade payments or e-commerce revenue across currencies

Accessing UK local payment details for certain non-UK-incorporated entities — see EQWIRE's guide on GBP accounts for non-UK companies

Faster, more structured digital onboarding for international business models

Not ideal for:

Overdrafts, loans, or revolving credit — EMIs may grant limited credit under FCA conditions, but cannot fund it from safeguarded or payment transaction funds; full bank-style credit remains a bank function

Cash, cheque, or branch-dependent operations

Counterparties, auditors, or public-sector contracts that require a PRA-authorised bank account explicitly

Businesses whose treasury policy requires the FSCS deposit protection framework specifically

When to use both: Most internationally active SMBs, e-commerce businesses, and SaaS platforms find they need a bank for credit or domestic treasury — and an EMI for international payments and multi-currency operations. The two structures are complementary.

What an FCA Authorised EMI Business Account Can — and Cannot — Do

Capabilities vary significantly by provider. The list below reflects typical features, not universal guarantees.

Can usually include:

Inbound and outbound UK payments via Faster Payments, CHAPS, and Bacs — non-bank PSPs access these rails through direct or agency arrangements (Pay.UK)

International transfers via SWIFT or local payment rails

Local receiving details (sort code / account number for GBP; IBAN for EUR) — provider-dependent

Multi-currency balance holding (GBP, EUR, USD, and others — provider-dependent)

Currency conversion, often at or near mid-market rates

In some cases: payment cards, API access, batch payments, or accounting integrations

Typically cannot include:

Full bank-style lending or overdrafts funded from customer deposits

Standard FSCS deposit protection on the account balance itself

Every payment rail or currency — check current product specifications directly

Every feature implied by a bank-like interface

Common Misunderstandings: Myths vs Facts

Myth | Fact |

|---|---|

"If it has a sort code, it must be a bank." | Sort codes are issued to payment service providers, not only banks. An EMI can hold UK local payment details without being a PRA-authorised deposit taker. |

"EMI protection works exactly like FSCS bank protection." | EMI balances are protected through safeguarding, not FSCS directly. In an insolvency, customers should receive most of their money back — but the process takes longer than an FSCS claim and insolvency costs may reduce the amount recovered. |

"EMIs cannot lend at all." | FCA guidance confirms EMIs may grant credit under specific conditions — but not if funded from safeguarded or payment transaction funds. Full bank-style lending and overdrafts are not permitted. |

"A multi-currency account must be a bank product." | Multi-currency capability is a product feature. Banks and EMIs can both offer it; neither category guarantees it. |

"A business must choose: EMI or bank." | Most businesses with international payment flows use both — an EMI for cross-border operations and a bank for lending or domestic treasury. |

How to Check the FCA Register Before Choosing a Provider

The safest verification step is to search the FCA Financial Services Register directly and match the legal entity, firm type, and permissions to what the provider states on its website.

A short due-diligence checklist:

Search the register — find the firm at register.fca.org.uk by trading name or legal entity name

Confirm the firm type — is it listed as an EMI, a payment institution, or a PRA-authorised bank? These are different categories with different permissions

Match the legal entity — trading name and registered legal entity should align

Read the safeguarding disclosure — the provider should clearly state how customer funds are held and under what framework

Check product capabilities — currencies supported, payment rails, business type eligibility, and jurisdictional restrictions

EQWIRE's Important Information page sets out FCA authorisation status, regulatory disclosures, and the specific framing of EMI status and FSCS applicability.

What to Compare Before Choosing an EMI or a Bank

Use this checklist before committing to an account structure:

Money protection priority — does your business require FSCS-style deposit protection, or is regulated safeguarding an acceptable model for the funds you plan to hold?

Lending and credit access — do you need an overdraft or loan? If yes, you need a bank or separately authorised lender

Currencies and payment corridors — which currencies and payment rails does the provider actually support?

Local receiving details — does your model require a UK sort code/account number, a EUR IBAN, or both?

Onboarding requirements — what documentation and entity-structure requirements apply, especially for non-UK-incorporated businesses?

Payment rail access — Faster Payments, CHAPS, Bacs, SWIFT, SEPA — does the provider support your specific corridors?

Counterparty requirements — do key clients, auditors, or regulators require a PRA-authorised bank explicitly?

Balance exposure — for large operating balances, understand the safeguarding model and its insolvency implications under the new PS25/12 framework from 7 May 2026

💡 Comparing account structures for your international payment flows? Use EQWIRE's current disclosures, safeguarding explanation, and multi-currency capabilities as a benchmark for any provider comparison. Visit EQWIRE · Important Information · GBP/EUR/USD Operating Account

Conclusion

An FCA-authorised EMI is a regulated non-bank payment provider operating under FCA supervision and the Electronic Money Regulations 2011. It can issue e-money, hold payment account balances across multiple currencies, and facilitate domestic and international payment flows via Faster Payments, CHAPS, Bacs, and SWIFT — but it does not take deposits, does not carry standard FSCS deposit protection on the account balance, and cannot offer full bank-style lending from safeguarded funds.

That is not a quality gap — it is a structural difference that makes EMIs well-suited to payment-led business models and less suited to credit or counterparties requiring a PRA-authorised bank. Most businesses with international operations use both. The right starting point is to check the FCA register, read the provider's current safeguarding disclosures, and match capabilities to your actual operational requirements. With the FCA's updated regime under PS25/12 taking effect on 7 May 2026, current disclosures matter more than older fintech comparisons.

FAQ

What is an FCA authorised EMI account UK?

An FCA-authorised EMI account is a business payment account issued by an electronic money institution that holds FCA authorisation under the Electronic Money Regulations 2011. The balance represents e-money rather than an eligible bank deposit, and the firm is regulated as a payment service provider rather than a PRA-authorised deposit taker. These accounts are used for payments, collections, currency holding, and cross-border transactions — not for deposit-taking or bank-style lending.

What is an FCA authorised EMI and how does it work?

An FCA-authorised EMI is a non-bank firm authorised by the FCA to issue electronic money and provide payment services. When a business receives funds, the EMI credits the payment account and holds the corresponding e-money value. Relevant customer funds are safeguarded — segregated from the firm's own money and held at a credit institution or in qualifying assets. The business then uses the account to send, receive, hold, and convert funds via payment rails such as Faster Payments, CHAPS, SWIFT, and SEPA, depending on the provider.

What is the difference between an FCA EMI and a traditional UK bank account?

The core differences are legal model, money protection, and permitted activities. A UK bank is PRA-authorised to take deposits and extend credit; eligible deposits receive FSCS protection up to £120,000 per eligible person per firm (from 1 December 2025). An FCA-authorised EMI holds customer funds as e-money and protects them through safeguarding under the Electronic Money Regulations. EMIs may grant limited credit under specific FCA conditions but cannot fund lending from safeguarded funds. Both can support payment operations and multi-currency balances subject to provider setup — but the underlying legal and protection models are distinct.

Can an EMI hold GBP EUR USD like a bank UK?

Many FCA-authorised EMIs support GBP, EUR, and USD business balances, but this is a product feature rather than a consequence of regulatory category. Whether a specific provider offers all three currencies with inbound and outbound payment capability depends on its infrastructure and payment rail access. Businesses should verify the provider's current currency list and capabilities directly rather than assuming based on EMI or bank status alone.

Is my money safe in an FCA authorised EMI account UK?

Funds in an FCA-authorised EMI account are protected through safeguarding under the Electronic Money Regulations 2011 — not through the FSCS deposit scheme that applies to eligible deposits at PRA-authorised banks. Safeguarding means the EMI must hold relevant customer funds separately from its own money. If the EMI fails, those funds should be identifiable for return — but the process takes time, and insolvency costs may mean customers do not recover the full balance. The FCA's strengthened safeguarding framework under PS25/12 takes effect on 7 May 2026. Always read a provider's current safeguarding disclosure and verify its authorisation on the FCA Financial Services Register.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)