•

•

Can a Cayman Company Receive GBP via Faster Payments?

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

Key Takeaways

Cayman exempted companies can receive GBP via Faster Payments, but only through a UK-local account held at a bank or FCA-authorised EMI or payment provider connected to the scheme.

UK payers need a UK sort code and account number to trigger the Faster Payments rail — an IBAN alone is not sufficient.

FCA-authorised EMIs and payment institutions can issue UK-local GBP details to non-UK entities without requiring UK incorporation, subject to provider eligibility policy and compliance review.

EMI accounts use safeguarding, not FSCS deposit protection — the mechanisms differ in how funds are protected and how quickly they are returned in the event of firm failure.

Provider eligibility policy and documentation quality are typically the real gatekeepers, not the payment rail or the Cayman jurisdiction itself.

Confirmation of Payee (CoP) is now a hygiene factor for UK domestic payments — the account name registered with the provider must match what UK payers enter, or the first transfer may stall.

Same-day GBP receipt is typical once the account is live, but is not guaranteed for every transaction.

What You Need — and What You Do Not

Before reading further, here is the practical summary.

You need:

A provider that explicitly accepts Cayman exempted companies

A genuine UK sort code and account number issued to the entity

Incoming Faster Payments enabled on that account

Completed KYB/KYC including UBO disclosure and source-of-funds review

A registered account name that matches what UK payers will enter (CoP-critical)

You do not necessarily need:

UK incorporation

A UK registered office

A UK-resident director (though some banks require this — EMI/PSP models often do not)

A local Cayman bank account to receive GBP

What usually blocks approval:

Layered or nominee ownership structures without clear UBO documentation

No evidence of commercial activity or business substance

Unclear explanation of why UK-local GBP collection is needed

Account name/trading name mismatch that causes CoP failures with UK payers

Can a Cayman Company Receive GBP via Faster Payments?

Yes — with the right provider setup and account infrastructure.

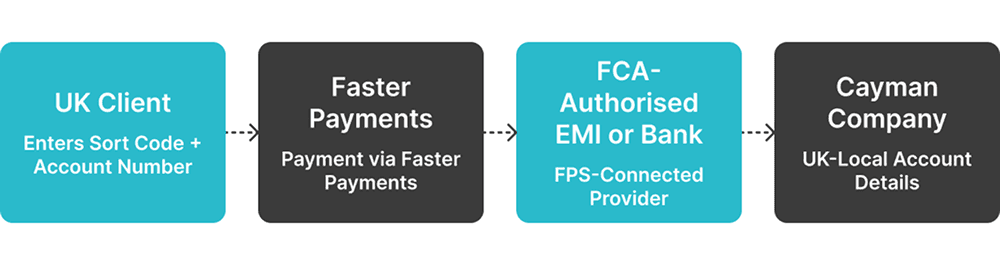

Faster Payments is a UK domestic rail operated by Pay.UK. It moves GBP between accounts using sort codes and account numbers, processes in real time, runs 24 hours a day, 365 days per year, and supports individual transfers up to £1 million. It does not screen for company jurisdiction. What it requires is that the receiving account is held at a provider connected to the scheme — either directly, indirectly, or through a sponsoring participant.

For a Cayman exempted company, the question is therefore about account infrastructure: does the company hold UK-local GBP receiving details through a provider that participates in FPS and is willing to onboard the entity? If yes, inbound GBP from UK payers will typically flow through Faster Payments in the same way it would for any account held at an FPS-connected provider — regardless of where the account holder is incorporated.

The assumption that "offshore company equals SWIFT only" is operationally wrong. The payment rail routes based on sort code and account number, not on company domicile. Provider eligibility policy and compliance review are the practical gatekeepers.

Why UK Faster Payments Rather Than SWIFT for a Cayman Islands Business?

UK-local GBP details remove payer friction, accelerate collection, and avoid the cost and complexity of correspondent banking for routine GBP receipts.

When a UK client pays an invoice, the default path is a domestic transfer: open the banking app, enter a sort code and account number, and the credit arrives within seconds. If the Cayman entity only holds SWIFT details — a BIC and IBAN — the payer must initiate an international wire. That means higher fees, a multi-day clearing window, and avoidable reconciliation gaps where SWIFT credits arrive net of correspondent bank charges with truncated remittance data.

Common operational use cases for Cayman entities wanting UK Faster Payments access include:

SaaS businesses billing UK corporate clients on monthly subscription invoices

IT consultancies and professional services firms collecting GBP retainers from UK counterparties

Holding companies receiving GBP from UK operating subsidiaries or group entities

E-commerce or platform businesses collecting sterling from UK merchants or marketplaces

In each case, forcing UK payers through a SWIFT workflow creates friction that UK-local collection eliminates entirely.

What Does a Cayman Exempted Company Actually Need?

The building blocks are about account infrastructure and provider onboarding — not Cayman law.

1. A provider that accepts Cayman entities. Not every bank, EMI, or fintech onboards Cayman exempted companies. Provider policy differs significantly. Some include Cayman in their eligible jurisdiction list; others apply enhanced scrutiny; some exclude it. This is the first filter — confirm eligibility before preparing any documentation.

2. A genuine UK sort code and account number. A UK sort code is what routes a domestic GBP credit through Faster Payments. Pay.UK notes that a sort code embedded in an IBAN does not necessarily mean the provider participates in UK payment systems. The account must include a dedicated UK sort code and account number, not only an IBAN.

3. Incoming Faster Payments enabled. The provider must support FPS for inbound GBP on the specific account type being issued. Confirm this explicitly — some international business accounts support SWIFT inbound only.

4. Completed KYB/KYC and UBO review. Cayman exempted companies require full corporate documentation and beneficial ownership disclosure. Enhanced due diligence is standard for offshore-incorporated entities.

5. A Confirmation of Payee-registered account name. Pay.UK's Confirmation of Payee (CoP) is an account name-checking service now covering most Faster Payments and CHAPS traffic. When a UK payer sets up the Cayman entity as a new payee, CoP checks whether the name they enter matches the name registered on the account. A mismatch generates a warning at the UK payer's end and may prevent the first transfer from completing. The name registered with the provider — company registered name or trading name — must match what UK clients will enter. Confirm this with the provider before going live.

Can a Cayman Exempted Company Get UK Bank Details Without a UK Registered Office?

Often yes — but this is a provider policy question, not a scheme technology question.

Faster Payments does not require the receiving entity to have a UK registered office, a UK-resident director, or UK incorporation. The payment rail routes based on sort code, not on company domicile. The relevant question is whether the provider's onboarding policy permits non-UK entities to hold UK-local accounts.

Traditional UK high-street banks are typically the most restrictive. Most require UK incorporation, a meaningful UK trading presence, or a UK-resident director for a GBP current account with sort code. For a Cayman entity with no UK footprint, this route is difficult in practice.

FCA-authorised EMIs and payment institutions operate differently. Many have built onboarding infrastructure specifically for international businesses — including offshore-incorporated entities — and issue UK-local GBP details to eligible non-UK companies after completing compliance review. Provider policy still varies, and there is no universal Cayman acceptance.

A practical illustration: a Cayman holding company that bills UK software clients, can demonstrate active invoicing, holds transparent ownership, and provides a clear source-of-funds trail is meaningfully better positioned than a recently formed Cayman entity with nominee directors, no commercial activity, and no documented revenue. For a broader treatment of the no-UK-office mechanics and sort code issuance for non-UK entities, see EQWIRE's guide to GBP accounts for UAE companies with UK sort codes.

Cayman Bank vs UK Bank vs FCA EMI vs Multi-Currency Provider

The differences in Cayman eligibility, sort-code issuance, fund protection, and onboarding timeline are significant — and the right choice depends on use case, volumes, and compliance profile.

Dimension | Cayman Bank | UK High-Street Bank | FCA EMI / PSP | Multi-Currency Fintech |

|---|---|---|---|---|

UK presence required | No | Often yes | No (provider-dependent) | No (provider-dependent) |

Cayman exempted company eligible | Generally yes | Difficult | Possible — policy varies | Possible — policy varies |

UK sort code + account number | Not typically | Yes | Yes | Yes |

Faster Payments (inbound GBP) | Via correspondent | Yes | Yes | Yes |

Fund protection | Varies by institution — confirm with provider | FSCS (up to £120,000) | Safeguarding (not FSCS) | Safeguarding (not FSCS) |

Onboarding timeline | Weeks to months | Weeks to months | Days to weeks | Days to weeks |

Minimum balance | Often substantial | Varies | Low to none | Low to none |

Important clarification on Cayman bank accounts and Faster Payments: a Cayman-based account can hold GBP, but a UK payer sending GBP domestically does not pay into a Cayman bank directly. The UK payer's Faster Payments credit routes to a UK-local account. What a Cayman bank typically receives from a UK payer is a SWIFT wire, not a Faster Payments credit, unless there is a UK correspondent arrangement that bridges this. EMI and multi-currency provider models are the realistic routes for issuing UK-local details to Cayman entities.

💡 Before choosing a provider, compare four things: Cayman eligibility, UK-local GBP details, Faster Payments access model, and fund-protection structure.

Use EQWIRE's educational resources on UK sort codes and offshore company accounts, safeguarding and fund protection, and the EQWIRE regulated-status framework to build an evaluation checklist. For a wider introduction to offshore company account structures across currencies, see EQWIRE's offshore company EUR account guide.

How Does a Cayman Company Open a GBP Account With Faster Payments?

The process is consistent across most providers, though compliance depth varies with ownership complexity.

Step 1 — Confirm provider eligibility for Cayman entities

Ask explicitly whether Cayman exempted companies are within scope. Get written confirmation that the account includes a UK sort code and account number, that incoming Faster Payments are supported, and that a Confirmation of Payee-registered name will be assigned to the account.

Step 2 — Define the GBP use case and expected volumes

Providers ask about business purpose and flow volumes during onboarding. A concrete answer — "we invoice UK SaaS clients monthly and expect approximately £X in inbound GBP" — reduces compliance back-and-forth significantly.

Step 3 — Prepare corporate and beneficial-ownership documents

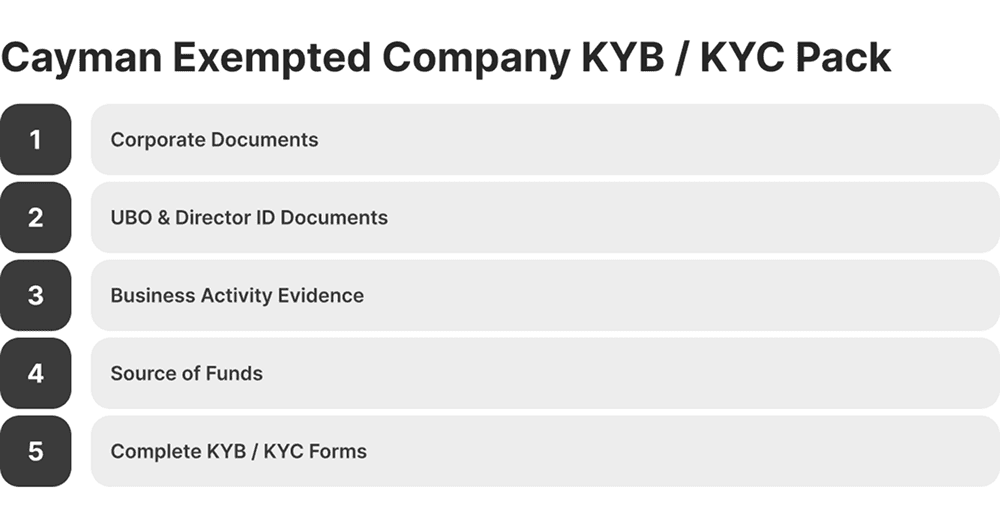

Gather all documentation before beginning the application. For a Cayman exempted company, standard requirements include: certificate of incorporation, memorandum and articles of association, register of directors and shareholders, certificate of incumbency or good standing (usually within six to twelve months), and Beneficial Ownership register details in line with the Cayman Islands Beneficial Ownership Transparency Act 2023. For each director and beneficial owner: certified passport copy, proof of residential address (within three months), and source-of-funds or source-of-wealth declaration.

Step 4 — Complete KYB/KYC including ownership structure review

Cayman exempted companies routinely attract enhanced due diligence. Prepare a clear group structure chart showing all entities and natural persons up to the ultimate beneficial owner. Where ownership passes through trusts, further offshore layers, or nominee arrangements, documentation of the underlying beneficiaries is typically required. The most common stall point is an incomplete or unclear ownership chain.

Step 5 — Verify which local details and rails are issued

Once the account is opened, confirm in writing: the sort code, the account number, and which payment rails are enabled for inbound transfers. Use Pay.UK's sort code checker to verify that the sort code can receive Faster Payments, Bacs Direct Credits, and CHAPS. This tool, updated weekly, checks against the Extended Industry Sort Code Directory (EISCD) and takes less than a minute.

Also confirm what name is registered on the account for Confirmation of Payee purposes. Pay.UK states that for business accounts, payers should use the registered business name or a trading name registered to the account — and that a close match is a valid outcome that still allows the payer to proceed after reviewing the displayed name. The goal is to avoid a "no match" result, which triggers a fraud warning and is likely to delay or prevent the first transfer. If the company trades under a different name from its registered name, confirm with the provider which name is registered for CoP and whether the trading name can also be added.

Step 6 — Test with a live inbound Faster Payment

Before redirecting clients to the new details, run a small test transfer via Faster Payments from a UK bank account. Confirm: the credit arrives, the CoP name check returns a match (or a close match with the correct name displayed), the reference data is intact, and the funds appear in the account balance. This step takes minutes and prevents a large payment failing silently on a new account.

What Documents and Compliance Checks Should a Cayman Company Expect?

Onboarding a Cayman exempted company at an EMI or payment provider is document-intensive — closer to enhanced due diligence than standard digital onboarding.

Corporate documents:

Certificate of incorporation from the Cayman Islands General Registry

Memorandum and Articles of Association

Register of directors and register of shareholders

Certificate of incumbency or certificate of good standing

Beneficial Ownership register details per the Beneficial Ownership Transparency Act 2023

Per director and beneficial owner:

Certified passport copy (valid, typically at least six months remaining)

Proof of residential address — bank statement or utility bill, within three months

Source-of-funds or source-of-wealth declaration for controlling shareholders

Business activity evidence:

Recent bank statements showing trading activity (three to twelve months)

Sample invoices or contracts with UK counterparties

Company website and service documentation

Business plan or operational description if recently formed

For layered structures: each corporate layer up to the UBO typically requires the same documentation set. Nominee arrangements and trust structures require documentation of the underlying beneficiaries, not the nominees.

The most common rejection triggers are: dormant-company optics with no commercial substance; weak or absent source-of-funds explanation; incomplete ownership documentation; and inability to explain clearly why UK-local GBP collection is operationally needed.

How Fast Are GBP Receipts — Can a Cayman Company Receive GBP the Same Day?

Same-day receipt is typical for an account already live with incoming Faster Payments enabled — but it is not a blanket guarantee.

Faster Payments operates 24/7, and the central infrastructure responds to the sending bank within 15 seconds. In practice, funds are typically available almost immediately, though receipt can occasionally take up to two hours depending on sending and receiving institutions.

Scheme timing and provider controls are separate layers. The rail is fast; individual providers may apply internal review on specific payment types:

First-time or high-value credits from new counterparties may trigger a short internal review.

Transaction monitoring thresholds are applied on all FCA-regulated accounts.

Newly opened accounts may carry a brief enhanced-monitoring period on initial inflows.

Pay.UK notes that a very small number of UK accounts do not accept Faster Payments — another reason to verify the sort code before relying on it for live operations.

For a Cayman entity using a well-configured EMI account with incoming FPS enabled, routine receipts from established UK payers will typically settle the same day, usually within seconds. First payments or unusual flows may take slightly longer.

How to Verify the Account Actually Supports UK Domestic Rails

Three checks before going live — each takes under five minutes and prevents operational failure.

Check 1: FCA Register — verify the regulated entity, not just the brand Confirm the provider is FCA-authorised and holds the appropriate permissions — either as an Authorised Payment Institution (API) or an Authorised Electronic Money Institution (EMI). Search the FCA Register by the legal entity name or Firm Reference Number (FRN), not by brand name. The FCA explicitly notes that some providers operate under trading names that differ from the authorised entity shown on the Register — a firm brand may not appear in a direct search. If in doubt, ask the provider for their FRN and verify it directly. A provider that is not FCA-authorised cannot lawfully issue UK payment accounts or access UK payment rails on your behalf.

Check 2: Pay.UK sort code checker Once the sort code is issued, enter it into Pay.UK's sort code checker. Updated weekly against the Extended Industry Sort Code Directory (EISCD), the tool confirms whether the sort code can typically receive Faster Payments, Bacs Direct Credits, and CHAPS. Pay.UK notes the checker is provided for informational purposes only — only the provider can confirm the exact services available on a specific account. If Faster Payments does not show as supported, query this with the provider before going live.

Check 3: Confirmation of Payee name test Ask the provider to confirm the account name registered for CoP purposes. Then run a CoP check from a UK bank account by adding the Cayman entity as a new payee. A "match" or "close match" result means the payment can proceed — Pay.UK notes that for business accounts, a close match is a valid outcome where the payer is shown the registered name to confirm before continuing. A "no match" or "unavailable" result should be resolved with the provider before giving the details to UK clients, as a no-match warning on the payer's screen is likely to delay or prevent the first transfer.

What Are the Most Common Mistakes Cayman Companies Make?

Most failure points are avoidable with the right preparation.

Assuming Cayman exempted company status blocks UK-local rails. The rail does not screen for jurisdiction — provider policy does. The two are different.

Not confirming provider eligibility before preparing documents. Eligibility confirmation should be the first step, not a discovery made mid-application.

Choosing providers based only on fees. Eligibility, sort-code issuance, and Faster Payments access matter more than fee schedules.

Not checking whether the sort code supports FPS before going live. A sort code that does not appear in the EISCD as Faster Payments-enabled cannot receive Faster Payments credits.

Ignoring Confirmation of Payee. A name mismatch causes a fraud warning on the UK payer's screen, which is the most common reason a first inbound transfer fails despite correct sort code and account number.

Confusing EMI safeguarding with FSCS deposit protection. The protection frameworks are materially different. Finance teams need to understand this distinction before placing operational GBP balances.

Submitting incomplete documentation. Cayman exempted company applications will stall in compliance review if ownership structure, source of funds, or business purpose is unclear or undocumented.

Before Choosing a Provider: What Should a Cayman Company Compare?

Six dimensions determine whether a provider is operationally right — not just commercially convenient.

1. Cayman exempted company eligibility. Written confirmation from the provider before preparing documentation, not an assumption from a generic international business page.

2. UK-local details issued. A dedicated UK sort code and account number, confirmed as allocated to the entity — not a pooled address shared across multiple clients.

3. Faster Payments, Bacs, and CHAPS support for inbound GBP. Verify which domestic rails are enabled. UK payers use different rails for different purposes: Faster Payments for standard transfers, CHAPS for high-value same-day payments, and Bacs Direct Credit for bulk payroll-style credits. Confirm all are supported where needed, and verify via the Pay.UK sort code checker.

4. Fund protection model. Bank deposit accounts carry FSCS protection up to £120,000 per eligible customer (as of December 2025). EMI accounts use safeguarding — client funds are segregated at a regulated credit institution and cannot be lent out. From 7 May 2026, the FCA's CASS 15 supplementary regime (PS25/12) introduces daily reconciliation requirements, monthly FCA reporting, mandatory annual safeguarding audits, and resolution pack obligations for EMIs and payment institutions, strengthening the existing safeguarding framework further. See the FAQ below for a full comparison of safeguarding versus FSCS. Both models provide meaningful protection but differ in mechanisms and recovery timelines — finance teams should understand the distinction before placing significant operational balances.

5. Transaction limits and monitoring approach. Confirm per-payment and monthly limits align with expected GBP volumes. Understand what triggers internal review.

6. Accounting integration and multi-currency capability. If the Cayman entity also needs EUR, USD, or other currencies, or requires API or accounting software integration, confirm this upfront.

💡 Finance teams redesigning GBP collection for Cayman structures: review the mechanics before committing to a route.

EQWIRE's guidance on safeguarded EMI infrastructure and fund protection, UK sort code mechanics and local payment rails, and offshore company account models covers the operational considerations across provider types. Understanding the tradeoffs before approaching any bank, EMI, or fintech reduces onboarding delays and avoids selecting a setup that does not meet the actual operational requirement.

Conclusion: The Real Question Is Infrastructure, Not Incorporation

A Cayman exempted company can often receive GBP via Faster Payments — but only through a UK-local account that is configured to receive Faster Payments, held at a provider connected to the scheme, with a completed compliance review and a Confirmation of Payee-registered name that UK payers can match against.

Cayman incorporation shapes the onboarding risk assessment that providers apply. It does not determine whether the payment rail is accessible. What matters is whether the Cayman entity can qualify for a UK-local account at a provider that participates in FPS — and that is determined by provider policy and compliance review, not by jurisdiction.

For Cayman exempted companies collecting GBP from UK counterparties, the operational path is clear: confirm provider eligibility, verify UK-local details and Faster Payments support via the Pay.UK sort code checker, register the correct account name for CoP, and prepare documentation that reflects the entity's actual commercial activity and ownership structure.

The infrastructure exists. The question is whether the company can qualify for it.

FAQ

Is it possible for a Cayman Islands company to use UK Faster Payments?

Yes, with the right account setup. A Cayman exempted company can receive GBP via Faster Payments if it holds a genuine UK sort code and account number through a bank or FCA-authorised EMI or payment provider connected to the Faster Payment System, and the account is configured to receive Faster Payments. Cayman incorporation itself does not create or block access — provider eligibility policy and compliance review are the practical gatekeepers. Use Pay.UK's sort code checker to verify the sort code before relying on it for live payments; Pay.UK notes the checker is informational only and only the provider can confirm the exact services available on a specific account.

How does a Cayman company open a GBP account with Faster Payments?

The process involves confirming provider eligibility for Cayman entities; defining the GBP use case and expected volumes; preparing corporate documents, UBO identification, and source-of-funds evidence; completing KYB/KYC review; verifying which domestic rails are enabled on the issued account via the Pay.UK sort code checker; confirming the CoP-registered account name; and testing the setup with a live Faster Payment before going live. Onboarding at EMIs and payment institutions typically takes days to several weeks depending on ownership structure complexity.

Can a Cayman exempted company get UK bank details without a UK registered office?

Often yes, through FCA-authorised EMI or payment provider models. Many regulated EMIs and multi-currency payment providers issue UK-local GBP details to non-UK entities without requiring UK incorporation, a UK-registered office, or a UK-resident director — though this depends on the provider's eligibility policy. Traditional UK high-street banks are typically more restrictive. Confirming eligibility in writing before preparing any documentation is the essential first step.

Can a Cayman exempted company receive GBP same day through a UK EMI?

In most cases, yes. Faster Payments operates 24/7 and the central infrastructure responds within 15 seconds. Funds typically settle almost immediately for routine transfers, though receipt can occasionally take up to two hours. Providers apply internal transaction monitoring, which can add a short review window on first-time or high-value credits. Pay.UK notes that a small number of UK accounts do not accept Faster Payments — verify the sort code before going live.

Does a Cayman company need a UK bank account, or can an EMI work?

An EMI account can work for Faster Payments access and UK-local GBP collection. The key difference between a bank account and an EMI account is not the payment rails — both can issue sort codes and support Faster Payments inbound — but the fund protection model. UK bank deposits are protected by the FSCS up to £120,000 per eligible customer. EMI accounts use safeguarding: client funds are held separately at a regulated credit institution and cannot be lent out, but the protection mechanism differs from FSCS and recovery in an insolvency may take longer. Both provide meaningful protection, but finance teams should understand the distinction before placing significant operational balances.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)