•

•

CNY Business Account for Non-Chinese Companies: Receive Chinese Yuan Without a China Bank

[aa disclaimer] Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions. [/aa]

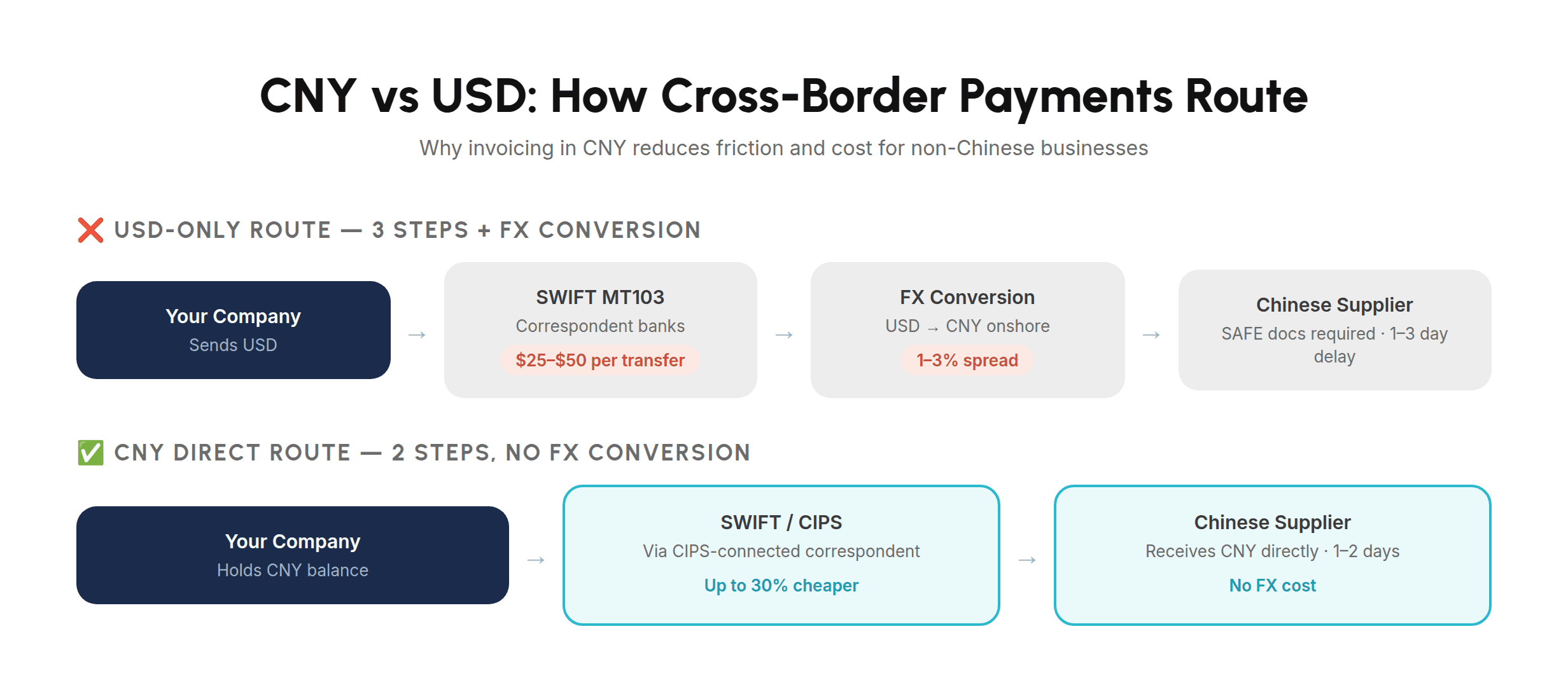

A UK-registered import business receives an invoice from a Shenzhen manufacturer denominated in CNY. Paying in USD means the funds travel via SWIFT MT103 through one or more correspondent banks, triggering an FX conversion on the Chinese side, adding fees, documentation obligations, and 1–2 business days of delay before the supplier actually receives usable yuan. For businesses with recurring China payables, this friction compounds with every cycle.

Cross-border payments using RMB surged 21.1% year-on-year in the first eight months of 2024, reaching approximately 41.6 trillion yuan, reflecting how deeply CNY invoicing has taken root in global trade. Yet the prevailing assumption that receiving CNY requires a bank account inside mainland China is wrong. A CNY business account for non-Chinese companies is available through regulated offshore multi-currency account providers, with no China entity, no physical branch visit, and no six-week waiting period. This guide explains how that works, who qualifies, and when it makes commercial sense.

[aa key-takeaways]

Key Takeaways

Non-Chinese companies (including UK Ltd, BVI IBC, and Cayman entities) can open a CNY business account through an FCA-regulated Electronic Money Institution without establishing a legal presence in mainland China.

CNY payments from China arrive via SWIFT or CIPS-connected correspondent banks; the Chinese sender is responsible for SAFE compliance and providing a payment purpose code.

The key distinction: CNY is the onshore yuan regulated by the PBOC; CNH is the offshore yuan traded freely in Hong Kong and global financial centres. Offshore accounts hold CNH-equivalent balances.

USD-only payments to China add 1–3% in FX conversion costs per transaction cycle; holding CNY eliminates that step for businesses with recurring China payables.

Offshore CNY accounts cannot be used for onshore China tax payments or salary obligations. A local Chinese bank account remains necessary for those functions.

[aa btn]Book a Call[/aa] [/aa]

Why Non-Chinese Companies Need a CNY Business Account

A CNY business account for non-Chinese companies addresses a structural problem in cross-border trade with China: the cost and complexity of settling in USD when suppliers invoice in yuan. Chinese manufacturers and service providers increasingly prefer CNY invoicing, reducing their own FX exposure. For the non-Chinese buyer or recipient, this shift means USD-denominated payments are no longer the default, and USD-only payment infrastructure creates measurable friction.

The Problem with USD-Only Payments to China

When a non-Chinese company pays a Chinese supplier in USD, the payment travels via SWIFT MT103 through one or more correspondent banks before converting to CNY onshore. Typical SWIFT fees range from $25 to $50 per transfer from the sender's bank alone, before correspondent bank deductions. The Chinese supplier must then register the incoming foreign currency with the SAFE (State Administration of Foreign Exchange), which requires filing documentation within five days of receipt, as required under SAFE regulations, before the funds can be converted to yuan for domestic use. For high-frequency suppliers, this creates recurring administrative overhead on both sides.

The FX conversion itself adds cost. Depending on the bank and the size of the transfer, the USD-to-CNY conversion applies a spread of 1–3% on top of the mid-market rate. For a business making $500,000 in China payments annually, that represents $5,000–$15,000 in conversion costs before accounting for wire fees. The CIPS (Cross-Border Interbank Payment System), launched by the People's Bank of China in 2015, was designed to reduce exactly this friction for CNY-denominated cross-border flows, but only where the receiving account already holds CNY.

How a CNY Account Reduces FX Costs for Import-Export Businesses

Businesses that hold an offshore yuan account can pay Chinese suppliers directly in yuan, removing the USD-to-CNY conversion step entirely. The Chinese supplier receives CNY, files their standard SAFE documentation for a domestic RMB receipt, and the non-Chinese company avoids both the correspondent bank chain and the FX spread. For import-heavy businesses paying suppliers on a 30–60 day cycle, the savings are compounded across each payment run.

CIPS processes cross-border RMB payments at lower cost than SWIFT-routed USD transfers; estimates suggest CIPS fees can be up to 30% cheaper for CNY-denominated transactions, according to analysis by PNC's cross-border RMB guide. Businesses using a CNY multi-currency account access these savings without joining CIPS directly; payments route through CIPS-connected correspondent banks to the recipient's offshore account.

What Is a CNY Business Account and How Does It Work Offshore?

A Chinese yuan business account for offshore companies functions as a named currency balance held within a regulated multi-currency account outside mainland China. The account is issued by a licensed payment institution (typically an Electronic Money Institution, or EMI) that holds CNY-equivalent funds that can be used to receive inbound transfers from China, make outbound payments to Chinese counterparties, or convert to another currency at the company's discretion.

CNY vs CNH: Understanding the Two Markets

CNY refers to the Chinese yuan traded within mainland China, regulated by the PBOC (People's Bank of China), which sets a daily reference rate and allows trading within a ±2% band. CNY is the currency of domestic Chinese commerce, used for local supplier payments, tax obligations, payroll, and most onshore financial activity. Foreign businesses operating in China use CNY for all mainland transactions.

CNH is the offshore yuan, traded outside mainland China, primarily in Hong Kong but also in Singapore, London, and other global financial centres. CNH was introduced in 2009 as part of China's strategy to internationalise the renminbi while maintaining domestic capital controls. Because CNH trades freely on offshore markets, its exchange rate can differ slightly from CNY depending on demand conditions. In practice, when a Chinese company initiates a cross-border payment via CIPS or SWIFT, the settlement converts at near parity; the practical difference for standard trade payments is minimal. Offshore multi-currency accounts hold CNH-equivalent balances; the distinction matters primarily for treasury teams managing large FX positions.

How Offshore CNY Balances Are Held and Safeguarded

For businesses using a UK FCA-authorised Electronic Money Institution, CNY balances are held in segregated safeguarding accounts in compliance with the Electronic Money Regulations 2011. Under Regulation 21 of the EMR 2011, client funds must be kept separate from the institution's own operating funds, held at an authorised credit institution and not lent out or invested. EQWIRE, authorised by the Financial Conduct Authority (FRN 901100), applies this framework to all supported currencies, including CNY. This is not a bank deposit and is not protected by the Financial Services Compensation Scheme, but the safeguarding requirement provides structural protection for client balances.

Who Is Eligible to Open a CNY Business Account Without a China Entity?

An RMB account for foreign companies is available to businesses registered outside mainland China, Hong Kong, Macau, and Taiwan, subject to standard KYC (Know Your Customer) and AML (Anti-Money Laundering) checks. No Chinese business licence, registered address in China, or local director is required.

Company Structures Accepted: UK Ltd, BVI IBC, Cayman, LLP

The following entity types are typically eligible to open an offshore CNY business account with an FCA-regulated EMI:

UK Limited Company (Ltd) — the standard structure for UK-registered businesses. Full FCA jurisdiction; straightforward onboarding.

BVI International Business Company (IBC) — a common offshore holding and trading structure. Accepted by EMIs that have appetite for offshore entities, subject to enhanced due diligence on UBO (Ultimate Beneficial Owner) and business purpose. As noted in EQWIRE's guidance on UK bank account for BVI companies, BVI entities can access UK payment infrastructure through an FCA-regulated EMI without a UK office or UK-incorporated entity.

Cayman Islands company — typically used for investment vehicles, fund structures, and international holding companies. Accepted at EMI discretion; economic substance documentation may be required.

LLP (Limited Liability Partnership) — eligible where the LLP is registered in a supported jurisdiction and operates a legitimate business with identifiable beneficial partners.

Singapore Pte Ltd — accepted by most UK and EU-regulated EMIs, subject to standard KYC.

H3: Onboarding Requirements: KYC, UBO, and Business Purpose Documentation

Regardless of entity type, the application process for an offshore CNY business account typically requires:

Certificate of incorporation (or equivalent formation document)

Company register or equivalent showing directors and shareholders

UBO documentation: proof of identity and address for all beneficial owners holding 25% or more

Source of funds declaration: explanation of the business's revenue model and anticipated CNY flows

Business plan or transaction narrative: where funds come from, who the Chinese counterparties are, and the purpose of CNY transactions

Proof of registered address for the entity

For offshore structures such as BVI IBCs, EMIs typically apply enhanced due diligence. Multi-layer ownership chains require full tracing to the natural person beneficial owner. The compliance review, not the technical account opening, is the primary variable in the onboarding timeline, typically 5–14 business days for straightforward applications.

[aa fast-fact] Fast Fact: Opening a corporate bank account with a mainland Chinese bank typically requires physical presence at a branch, a registered entity inside China, and 3–5 weeks of processing, often longer for foreign-invested enterprises. An FCA-regulated EMI completes the process fully online, typically within 5–14 business days for eligible applicants. [/aa]

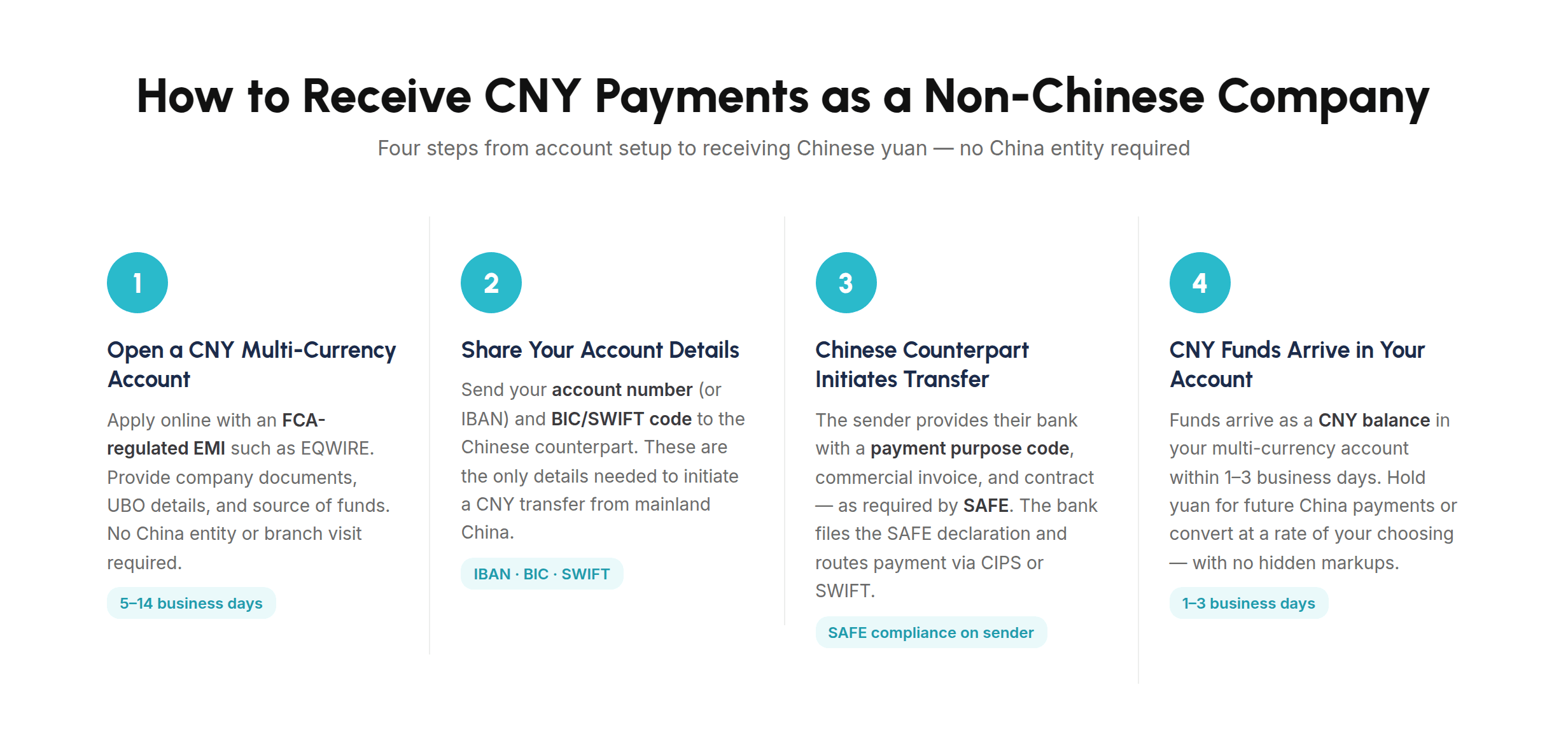

How to Receive CNY Payments as a Non-Chinese Company

Understanding how to receive Chinese yuan as a foreign company requires knowing which payment infrastructure the sender in China will use (CIPS or SWIFT) and what the Chinese counterpart must do to initiate the transfer correctly.

Payment Routes: SWIFT MT103 and CIPS

Two payment routes carry CNY transfers out of mainland China to offshore accounts:

SWIFT MT103 is the international wire transfer message format used by the global SWIFT network. A Chinese bank initiates a cross-border payment via SWIFT by sending an MT103 message through correspondent banks to the recipient's institution. SWIFT MT103 is the most widely used route for cross-border CNY transfers, particularly to EMI accounts in the UK or EU. Settlement typically takes 1–3 business days depending on correspondent chain length.

CIPS (Cross-Border Interbank Payment System) was launched in 2015 by the PBOC as dedicated infrastructure for cross-border RMB clearing and settlement. As of November 2025, CIPS has 190 direct participants and 1,567 indirect participants across 124 countries, supporting what the BIS describes as a growing shift toward dedicated cross-border payment infrastructure. Unlike SWIFT, which is a messaging network, CIPS provides both messaging and settlement for RMB transactions onshore, reducing reliance on offshore clearing arrangements. CIPS operates on a 5×24 + 4-hour schedule, extending the effective processing window beyond CNAPS (China National Advanced Payment System), which handles domestic onshore RMB flows only.

Non-Chinese businesses do not join CIPS directly; access is interbank only. CNY payments from a CIPS-connected Chinese bank route through the CIPS infrastructure and arrive at the offshore recipient's institution via the institution's correspondent bank network. For businesses using EQWIRE, inbound CNY arrives via SWIFT from CIPS-connected correspondent banks.

What Your Chinese Counterpart Needs to Initiate a CNY Transfer

The sender in China is responsible for SAFE compliance when initiating a cross-border CNY payment. Specifically, the Chinese counterpart must provide their bank with:

A valid payment purpose code — required by the PBOC for all cross-border CNY transfers to offshore accounts. Valid codes include GOD (goods trade), SER (services trade), CAP (capital transfers), and others defined by SAFE.

A commercial contract supporting the transfer — the underlying trade agreement or service contract between the two parties.

A commercial invoice — matching the payment amount and purpose.

The recipient's account details — account name, account number (IBAN or equivalent), BIC/SWIFT code of the receiving institution.

Transfers exceeding the equivalent of USD 50,000 may be subject to additional SAFE review, which can extend the processing window. The Chinese sender's bank files the SAFE declaration on behalf of their client once documentation is verified. For recurring payments from the same Chinese counterpart, most banks streamline the documentation process after the first transfer.

[aa cta]

Open a CNY Multi-Currency Account for Your Business

EQWIRE supports CNY alongside GBP, EUR, USD, AED, and HKD, with fully online onboarding and no China entity required. Eligible businesses can be up and running in days.

[aa btn]Create Account[/aa] [/aa]

Holding CNY vs Converting to GBP or USD: When Each Makes Sense

Once CNY funds arrive in a CNY multi-currency account, finance teams face a decision: hold the balance in yuan or convert to the company's functional currency (GBP, USD, EUR). The right answer depends on the company's payment cadence with Chinese counterparties and its FX risk tolerance.

FX Timing Strategy for Import-Heavy Businesses

For businesses that pay Chinese suppliers on a 30–60 day cycle, holding CNY in the account is typically the lower-cost approach. The company receives CNY from a Chinese client or subsidiary, holds the balance, and uses it to fund the next supplier payment, avoiding two FX conversions (CNY→GBP on receipt, then GBP→CNY on payment). Each avoided conversion saves the applicable FX spread, which typically ranges from 0.3% to 1.5% per conversion depending on the provider and the transaction size.

For businesses with infrequent or one-off CNY receipts, converting to the functional currency on receipt removes ongoing FX exposure. A BVI holding company receiving annual CNY royalties from a Chinese subsidiary, for example, may prefer to convert immediately rather than hold yuan on the balance sheet.

How to Manage CNY Balance Risk Without a Hedging Programme

Most SMBs and offshore holding companies do not run formal FX hedging programmes. For these businesses, the practical approach is to match CNY receipts to CNY payments where possible, structuring payment timing so that incoming yuan funds outgoing yuan obligations within the same 30–60 day window. Where this is not possible, converting CNY to USD (rather than directly to GBP or EUR) may provide better liquidity, given USD's deeper FX market for CNY pairs. Businesses using EQWIRE's CNY multi-currency account can see the prevailing FX rate and confirm the conversion before executing, with no hidden markups applied after confirmation.

Practical Scenarios: Import-Export, E-Commerce, and Consulting

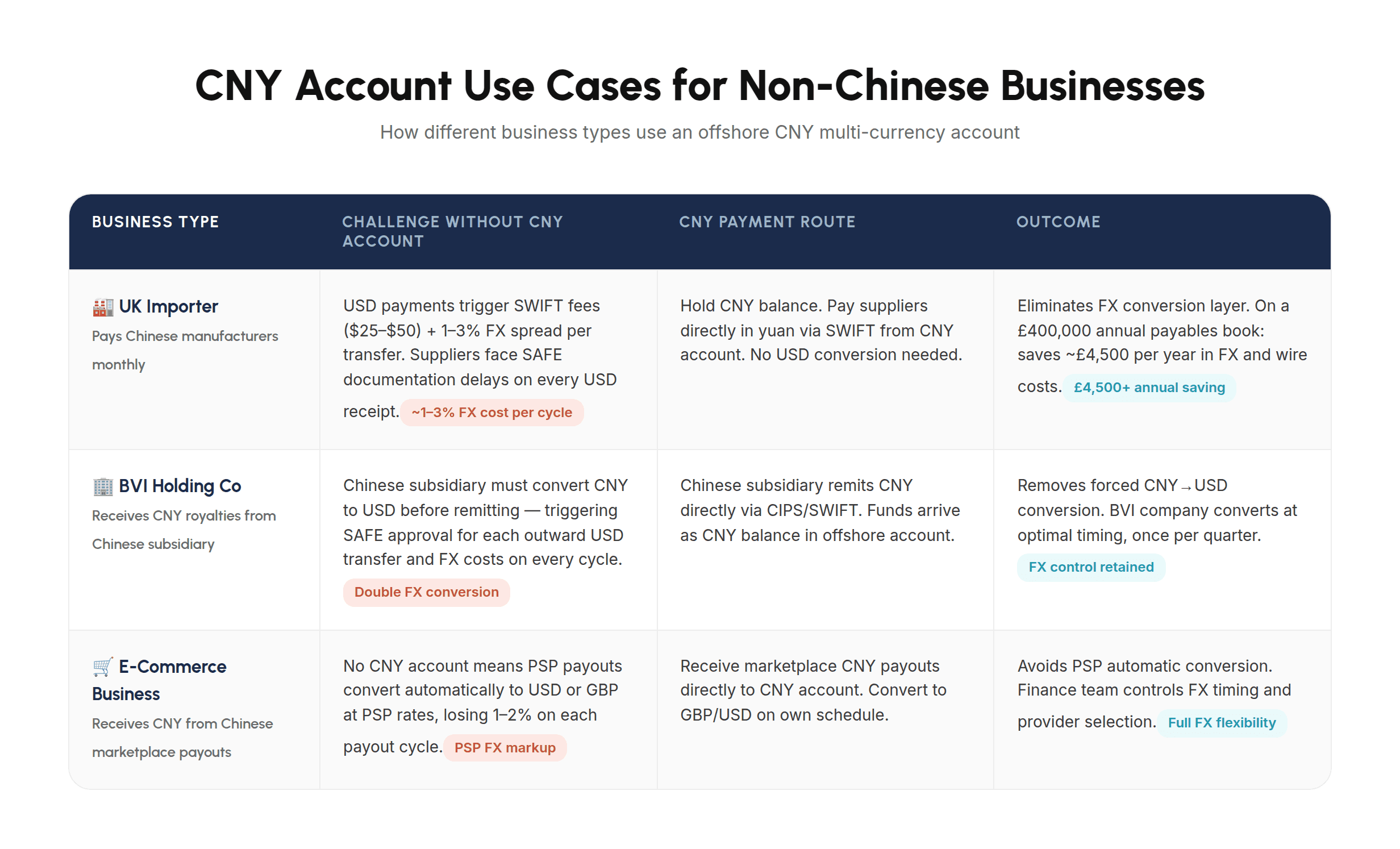

Scenario 1: UK Importer Paying Chinese Manufacturers in CNY

A UK-registered import company sources textiles from three manufacturers in Guangdong, paying monthly. Previously, the company paid in USD; each payment incurred a $35 SWIFT fee and a 1.5% FX conversion spread applied by the sending bank. The Chinese manufacturers also faced SAFE documentation requirements on each receipt, occasionally delaying confirmation that funds had cleared.

After opening a CNY business account for non-Chinese companies through EQWIRE, the UK importer holds a CNY balance topped up from its GBP earnings. Monthly payments route directly in yuan via SWIFT, the Chinese manufacturers receive CNY domestically, and the USD conversion step is removed entirely. The company's total annual payment cost on a £400,000 China payables book drops from approximately £8,000 (fees + FX spread) to under £3,500 in FX costs, a saving driven primarily by eliminating the cross-currency conversion layer.

Scenario 2: BVI Holding Company Receiving CNY Royalties from a Chinese Subsidiary

A BVI international business company holds intellectual property licensed to a wholly owned Chinese subsidiary. The subsidiary pays quarterly royalties denominated in CNY. Previously, the BVI company had no CNY account, so the Chinese subsidiary converted to USD before remitting, triggering onshore FX costs and a SAFE approval process for each outward USD transfer.

By establishing an offshore CNY account (see EQWIRE's guidance on offshore companies accessing UK payment rails), the BVI holding company now receives royalties directly in yuan via SWIFT from a CIPS-connected bank. The Chinese subsidiary remits in CNY as a domestic-equivalent transfer, avoiding the USD conversion entirely. The BVI company holds CNY until a favourable conversion rate to USD emerges, converting once per quarter rather than four times per year.

[aa cta]

Manage CNY Payments Without Opening a China Bank Account

Finance teams at UK and BVI companies use EQWIRE to hold CNY balances, receive CIPS/SWIFT transfers, and convert at competitive FX rates, all from one account.

[aa btn]Create Account[/aa] [/aa]

FAQ

Can a UK or BVI company receive CNY payments without opening a Chinese bank account?

Yes. A UK or BVI company can receive CNY payments without a Chinese bank account by opening a multi-currency account with an FCA-regulated Electronic Money Institution that supports CNY as a balance currency. The payment routes from the Chinese sender via CIPS or SWIFT to the offshore account. The receiving company does not need a China-registered entity, a Chinese bank account, or physical presence in mainland China. Businesses can open a CNY business account for non-Chinese companies fully online, with onboarding typically completed within 5–14 business days for eligible applicants.

What is the difference between CNY and CNH for business payments?

CNY is the onshore Chinese yuan traded within mainland China under PBOC (People's Bank of China) regulation, with the daily reference rate set by the central bank and trading permitted within a ±2% band. CNH is the offshore yuan traded freely in Hong Kong and other global financial centres. For most cross-border trade payments, the practical difference is minimal. CIPS settles cross-border RMB transfers at near parity between CNH and CNY. Finance teams managing large FX positions may see rate differences of 0.1–0.5% between the two, depending on market conditions. Offshore accounts hold CNH-equivalent balances; a company invoicing in CNY will receive CNH in their offshore account, which settles to the Chinese supplier's CNY account onshore at near 1:1 via CIPS.

How does CIPS work for cross-border yuan transfers?

CIPS (Cross-Border Interbank Payment System) is China's dedicated infrastructure for clearing and settling cross-border RMB transactions, operated under the oversight of the PBOC. Launched in 2015, it processes both the messaging and settlement of yuan payments across borders, unlike SWIFT, which only handles messaging. As of November 2025, CIPS has 1,567 indirect participants across 124 countries. Businesses and individuals cannot access CIPS directly; transfers route through participating banks. A Chinese company initiates a CNY payment to an overseas recipient via their CIPS-connected bank; the payment settles onshore and routes outward to the recipient's institution via correspondent banking. For standard B2B trade payments, CIPS-routed transfers typically complete within 1–2 business days.

When should a non-Chinese company invoice in CNY vs USD?

A non-Chinese company should consider invoicing in CNY when it has recurring payables to Chinese suppliers; the CNY receipts can be held and used directly for supplier payments, eliminating two FX conversions per cycle. CNY invoicing is also worth considering when Chinese counterparties apply a better rate or pricing concession for yuan-denominated contracts, which is common in manufacturing and logistics. Invoice in USD when the relationship is one-off, when the Chinese counterpart is a large export-oriented business already familiar with USD settlement, or when the company has no CNY payment obligations to net against receipts. Consulting a qualified financial adviser is advisable before changing the currency denomination of long-term commercial contracts.

What documents does a Chinese sender need to initiate a CNY transfer to an offshore account?

The sender in China must provide their bank with a valid payment purpose code (as defined by PBOC/SAFE), a commercial contract covering the trade relationship, and a commercial invoice matching the transfer amount. For transfers exceeding the equivalent of USD 50,000, additional SAFE review and documentation may apply, potentially extending processing time. The Chinese sender's bank files the SAFE declaration on the sender's behalf. The non-Chinese recipient does not file SAFE documentation. SAFE compliance sits entirely with the Chinese party initiating the outbound payment.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)