•

•

E-Commerce Operating Account Holding GBP, EUR and USD in the UK

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

You open the settlement report. Stripe paid out in GBP — again.

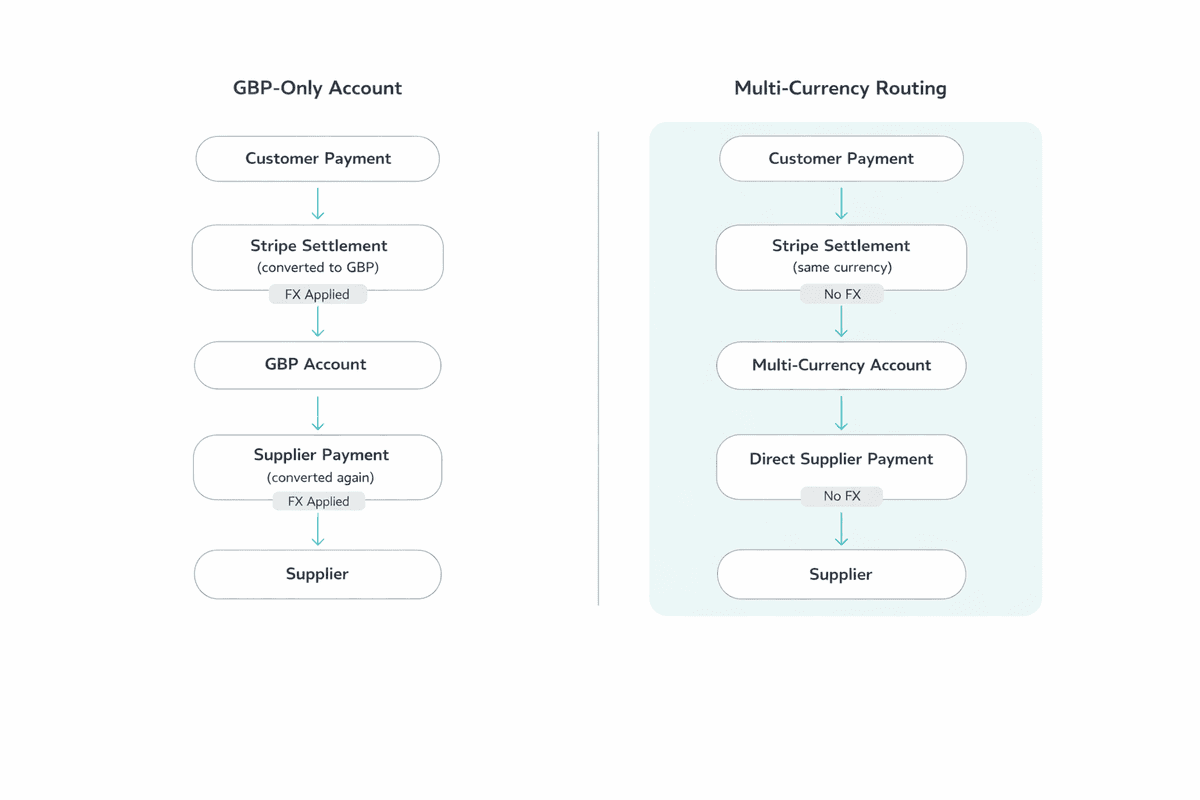

The EUR from German customers got converted at Stripe's rate. The USD from US buyers got converted too. By the time funds hit your bank, you have already lost 2% on the way in. Then you convert GBP back to EUR to pay your Polish supplier. Another 2% gone.

That is 4% of revenue disappearing on currency round-trips — before you spend a penny on operations.

Setting up a proper e-commerce operating account GBP EUR USD UK stops this. It holds each currency separately, routes PSP payouts without conversion, and lets you pay suppliers directly from matching currency balances.

This guide explains exactly how to set it up.

Key Takeaways

An e-commerce operating account GBP EUR USD UK lets online businesses hold three currencies in one place — no separate accounts per market.

Forced FX conversion by PSPs and traditional banks costs merchants 2–4% per transaction. At scale, that is not a fee — it is a structural margin leak.

A multi-currency account for e-commerce UK lets merchants receive PSP payouts in the original currency and pay suppliers in matching denominations — zero unnecessary conversion.

FCA-regulated EMI infrastructure provides statutory fund safeguarding and direct access to FPS, SEPA, and SWIFT — without the onboarding friction of a traditional bank.

The most effective setup connects PSP inflows, currency holding, and supplier payments within one account structure.

Disabling PSP auto-conversion is the single highest-return configuration change available to any UK e-commerce business operating across currencies.

What Is a Multi-Currency Account for E-Commerce?

A multi-currency e-commerce account is a business payment account that maintains separate balances in GBP, EUR, and USD simultaneously — without automatic conversion — and provides independent local receiving details for each currency.

This is not a foreign currency account at a high-street bank. Those still convert on receipt.

It is not a PayPal balance either. PayPal applies its own FX rate whenever you withdraw.

A genuine ecommerce business account UK GBP EUR USD no FX structure means:

EUR received stays in EUR until you move it

USD received stays in USD until you move it

You initiate every conversion — at a rate you can see, compare, and time

In the UK, these accounts are issued primarily by Electronic Money Institutions (EMIs) authorised by the Financial Conduct Authority (FCA).

Providers including Wise, Revolut Business, and Airwallex operate under this framework, each with different fee structures, currency coverage, and payment rail access.

Why UK Online Sellers Lose Margin on Every Settlement

The Currency Mismatch That Costs You Every Cycle

You receive EUR from European buyers. You receive USD from North American customers. You pay EUR for EU-sourced goods. You pay USD for SaaS tools, Meta Ads, US logistics.

A GBP-only account forces conversion at every single touchpoint — inbound and outbound.

💰 Revenue Impact: The round-trip FX cost using traditional UK banking infrastructure can exceed 4–6% of transaction value. On £500,000 annual cross-border turnover, that is up to £30,000 per year leaving your business invisibly.

For context on how this plays out for businesses managing international payment rails, see our article on GBP Faster Payments for offshore companies.

Three Problems a Standard UK Account Cannot Solve

Problem 1 — FX losses on PSP settlement

Stripe allows merchants to configure payout currency. Most don't.

Without a matching currency account, Stripe defaults to GBP conversion — adding a 2% currency conversion fee on top of standard processing charges. That fee hits every single EUR and USD settlement, every cycle.

⚠️ Hidden Cost: On £200,000 in EUR Stripe payouts per year, Stripe's 2% conversion fee alone costs approximately £4,000 annually — before your bank takes its own FX margin on any subsequent conversion.

Problem 2 — Fragmented account management

Some businesses try to solve this by opening a GBP account here, a EUR account there, a USD account somewhere else.

The result: three reconciliations, three fee structures, three providers to chase when something goes wrong. Administrative overhead rises with every payment cycle.

Problem 3 — Delayed working capital

Converting EUR → GBP on receipt, then GBP → EUR to pay a supplier adds days to the settlement cycle.

You are not just losing money on FX. You are losing time — and working capital tied up in unnecessary conversion queues.

✅ What to Do: A properly configured e-commerce account GBP EUR USD UK eliminates all three problems by unifying currency holding within one operational infrastructure.

How to Hold Multiple Currencies in a UK Business Account

The Sub-Wallet Model — How It Works

FCA-regulated EMI providers structure multi-currency accounts using a sub-wallet model.

Each currency is a separate balance with its own local receiving details:

Currency | Receiving Details | Payment Rails |

|---|---|---|

GBP | UK sort code + account number | Faster Payments (FPS), CHAPS |

EUR | European IBAN | SEPA Credit Transfer, SEPA Instant |

USD | US routing + account number | ACH, SWIFT |

Each wallet is independent. EUR received via SEPA stays in the EUR wallet. USD received via ACH stays in the USD wallet. Nothing converts automatically.

For businesses that need to understand GBP receiving infrastructure for non-UK entities, our guide on how to open a GBP account for a non-UK company covers the relevant account types and requirements.

When You Do Need to Convert

When conversion is genuinely needed — say, moving surplus USD to GBP for payroll — you initiate it inside the account dashboard.

The best EMI providers apply the mid-market rate with a transparent stated markup. No opaque spread, no guessing what rate you actually got.

That is a fundamentally different experience from discovering your bank converted funds at an undisclosed rate three days ago.

How to Avoid FX Fees With Stripe, PayPal, and Adyen

What Forced Conversion Actually Costs — The Numbers

Forced FX conversion occurs when a financial institution automatically converts received foreign currency into the account's base currency — at a rate it sets, without instruction from you.

The cost is never a visible fee. It is embedded in the exchange rate.

⚠️ Hidden Cost: Where the live mid-market EUR/GBP rate is 0.8550, a bank applying a 2.5% spread converts at 0.8335. On £500,000 annual EUR turnover, that difference alone is approximately £10,750 per year — invisible in your P&L, real on every settlement.

Step-by-Step: Disabling Forced FX in Stripe, PayPal, and Adyen

Stripe

Go to Dashboard → Settings → Bank accounts and scheduling

Add your EUR IBAN and USD routing number as separate payout destinations

Assign each currency to its matching account

Stripe routes EUR → EUR wallet, USD → USD wallet — unconverted

The 2% Stripe conversion fee is eliminated entirely once matched-currency routing is active.

PayPal Business

Go to Account Settings → Money, banks and cards

Add the EUR IBAN and USD routing number as separate withdrawal destinations

In Automatic Transfers settings, disable automatic conversion to GBP

Configure each currency to transfer to its matching external account

Adyen

In the Balance Platform, configure settlement accounts per currency

Each currency balance settles to the corresponding external account

EUR → EUR IBAN, USD → US routing number — no cross-currency settlement margin triggered

💰 Revenue Impact: A UK merchant processing £300,000/year in EUR through Stripe, without matched-currency routing, pays approximately £6,000/year in Stripe's conversion fee alone — before bank FX margins on any further conversion.

Is your business ready to go global?

Manage GBP, EUR, and USD from one place. Send and receive international payments with full transparency — and scale without the friction of traditional banking.

Paying Global Suppliers From the Same Account

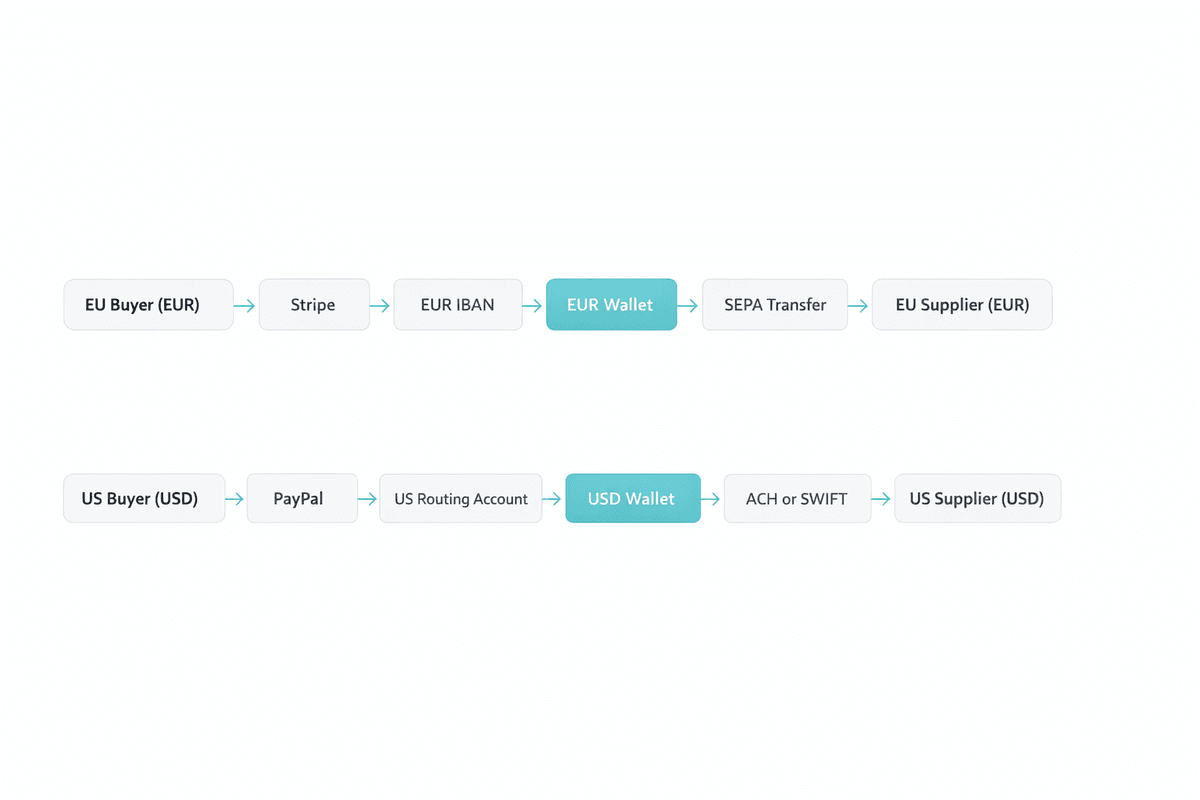

The Zero-Conversion Supplier Payment Cycle

Here is how a fully optimised payment cycle looks for a UK e-commerce merchant sourcing goods from Europe and running US ad spend:

EUR cycle:

EU buyer pays → EUR via Stripe → EUR IBAN → EUR wallet → SEPA to EU supplier Conversions: zero.

EU buyer pays → EUR via Stripe → EUR IBAN → EUR wallet → SEPA to EU supplier Conversions: zero.

USD cycle:

US buyer pays → USD via PayPal → US routing number → USD wallet → ACH to US ad platform Conversions: zero.

The currency never leaves its denomination at any stage of the cycle.

When conversion is needed — to cover GBP payroll or domestic UK costs — you initiate it once, deliberately, at a competitive rate. That is the only conversion that happens.

✅ What to Do: Configure PSP payout destinations before your next settlement cycle. One afternoon of setup removes a structural cost that otherwise compounds indefinitely.

UK businesses that also need to pay UK-based suppliers from foreign-currency accounts may find useful context in our guide on how to pay UK suppliers from a UAE business account.

Reconciliation: One Statement, Not Three

When GBP, EUR, and USD all flow through one account, month-end reconciliation is one dashboard, one statement, one provider.

Idle balances become visible. Upcoming supplier payment needs become trackable. Cash flow management across currencies becomes a clear operational decision rather than a guessing game spread across multiple logins.

For businesses operating through offshore structures that need SEPA access, our article on how to open a SEPA account for a Caribbean company covers the relevant access routes.

FCA EMI Accounts vs Traditional UK Banks: What E-Commerce Operators Should Know

An Electronic Money Institution (EMI) is not a bank.

It is a regulated entity licensed to issue electronic money and provide payment services — supervised by the Financial Conduct Authority under the Electronic Money Regulations 2011.

⚠️ Important: EMI accounts are not covered by the FSCS, which protects UK bank deposits up to £85,000. However, FCA-regulated EMIs must safeguard client funds in a dedicated segregated account at a credit institution, or secure equivalent insurance. Your funds are ring-fenced from the EMI's own capital.

For most e-commerce operators, the practical implication is straightforward: an EMI account is built for exactly what you need it to do.

EMI vs Bank — Side-by-Side Comparison

FCA-Regulated EMI | Traditional UK Bank | |

|---|---|---|

Account opening | Days (remote, digital) | Weeks to months |

Multi-currency holding | Separate wallets per currency | GBP only (typically) |

FX fee transparency | Stated markup over mid-market | Embedded spread, often opaque |

SEPA Instant access | Standard | Inconsistent |

FPS / CHAPS access | Standard | Standard |

SWIFT outbound | Standard | Standard |

Fund safeguarding | Segregated accounts (EMR 2011) | FSCS up to £85,000 |

Designed for | Payment throughput | Deposit holding and lending |

💰 Revenue Impact: The structural advantage of an EMI is not about lower fees alone — it is about access. Access to separate currency wallets, to SEPA Instant, to mid-market FX. Traditional banks are optimised for loans and deposits. EMIs are optimised for moving money — which is what e-commerce payment infrastructure actually needs to do.

Common Mistakes When Managing Multi-Currency Funds

Mistake 1 — Leaving Auto-Conversion Active in PSP Settings

Stripe, PayPal, and Adyen all default to converting foreign currency to GBP unless actively reconfigured.

Most merchants never change this setting. Opening a multi-currency account without updating PSP payout destinations means funds are still converted by the PSP before they reach you. The account provides zero benefit.

✅ Fix: Configure payout destinations the same day you open the account. Do not wait for the next settlement cycle.

Mistake 2 — Running Three Disconnected Accounts

Opening a separate account per currency at different providers feels like a solution. It is not.

The result is three reconciliations, three fee structures, inconsistent FX rates across providers, and no single view of total cash position across currencies.

✅ Fix: Use one account that natively holds GBP, EUR, and USD with independent wallets. One provider, one statement, one dashboard.

Mistake 3 — Converting Foreign Currency Immediately on Receipt

Some merchants open a multi-currency account but convert every EUR or USD receipt to GBP immediately — treating it like a faster bank account rather than a currency management tool.

This eliminates the entire operational advantage.

✅ Fix: Hold EUR for EUR supplier payments. Hold USD for USD ad spend and software costs. Convert only the surplus — when the rate is in your favour, not because settlement arrived.

Mistake 4 — Evaluating Accounts Only on Monthly Fees

A £10/month account fee difference is irrelevant if one provider offers a 0.35% FX markup and another charges 2%.

⚠️ Hidden Cost: At £500,000/year in conversions, the difference between 0.35% and 2% is £8,250 per year — dwarfing any monthly fee comparison.

✅ Fix: Always request the FX rate for EUR/GBP and USD/GBP before committing to a provider. Compare the markup against the live interbank rate.

Simplify Your Cross-Border Payment Infrastructure

One account. GBP, EUR, and USD held separately, with local payment details per currency. PSP payouts routed directly — no forced conversion, no fragmented reconciliation.

Conclusion

An e-commerce operating account GBP EUR USD UK is not a product reserved for large enterprises.

It is the infrastructure layer that any UK online business selling internationally should have in place — and the gap between having it and not having it compounds with every settlement cycle that passes.

The three decisions that matter:

Choose a provider that holds each currency independently without forced conversion

Configure PSP payout settings to route funds to the correct currency wallet — not to a GBP default

Evaluate FX rate quality, not just account fees, when comparing providers

The merchant who sets this up this quarter will recover thousands in previously invisible FX costs. The one who does not will keep funding their bank's margins indefinitely.

For more context on international payment infrastructure for UK businesses, visit the EQWIRE News section.

FAQ

How do I hold GBP EUR and USD in one UK e-commerce account?

You need a multi-currency account from an FCA-regulated EMI — not a standard UK business current account. Each currency wallet holds its balance independently and comes with local receiving details: a sort code and account number for GBP, a European IBAN for EUR, and US routing details for USD. Configure your PSPs to pay out in the original transaction currency to the matching wallet, rather than defaulting to GBP conversion on settlement.

What is the best multi-currency account for UK e-commerce businesses receiving PSP payouts?

The right account depends on your currency volumes, payment rail requirements, and conversion frequency. Key criteria: genuine currency holding without auto-conversion; transparent FX markup over mid-market; access to SEPA Instant, FPS, and SWIFT; API integration capability; and FCA regulatory standing. Wise, Airwallex, and Revolut Business each offer multi-currency infrastructure with different fee models suited to different transaction volumes.

Can an ecommerce account hold multiple currencies without forced FX in the UK?

Yes — but only with specific provider types. Standard UK business bank accounts convert foreign currency on receipt. FCA-regulated EMI accounts hold each currency in a separate balance without automatic conversion. You control when and how much to convert. PSP payout settings also need active configuration to route funds to currency-specific receiving details rather than a GBP default.

How do I receive PSP payouts and pay global suppliers from the same multi-currency UK account?

Configure your PSP — Stripe, PayPal, or Adyen — to pay out in the original transaction currency: EUR to your EUR IBAN, USD to your US routing number. Funds settle into the matching currency wallet. Initiate supplier payments directly from that wallet — EUR via SEPA, USD via SWIFT or ACH. No conversion occurs when inflow and outflow currencies match, making this a zero-FX-cost cycle for aligned flows.

Is money held in a UK EMI account protected if the provider fails?

EMI accounts are not covered by the FSCS, which protects bank deposits up to £85,000. However, FCA-regulated EMIs must safeguard customer funds under the Electronic Money Regulations 2011 — in a segregated account at a credit institution or through equivalent insurance. This ring-fences your funds from the EMI's own capital. Verify the specific safeguarding arrangement with your chosen provider and refer to the FCA's guidance on EMI safeguarding for current requirements.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)