•

•

How to Open a GBP Account for a Non-UK Company

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

rstand safeguarding and

Quick answer: Can a non-UK company open a GBP business account with a UK sort code?

Yes — in many cases. Many foreign-registered businesses can access UK local GBP payment details through an FCA-authorised EMI or regulated payment institution, without setting up a UK company first. Eligibility depends on jurisdiction, ownership transparency, business activity, and the provider's compliance policy. Approval is not guaranteed and is assessed case by case.

Who This Guide Is For (and Not For)

This guide is likely useful if:

Your company is incorporated outside the UK and you invoice UK clients or pay UK suppliers

You need a UK sort code and account number to receive GBP on domestic rails

You are evaluating whether an EMI-issued payment account meets your needs, or whether a full UK bank account is actually required

This guide is less relevant if:

You are incorporating a new UK entity (a different process with different requirements)

You are an individual seeking a personal UK account

Your business is in a sector typically outside EMI risk appetite, such as crypto or certain regulated financial services — you may need specialist advice

Introduction

Foreign-registered businesses frequently need to receive or send GBP without setting up a UK company. A SaaS platform billing UK enterprise clients, an import/export company paying UK suppliers, or a consultancy invoicing UK-based customers all face the same practical challenge: how do you handle pounds efficiently when your company is registered in Dubai, Singapore, the BVI, Delaware, or anywhere else outside the United Kingdom?

For many businesses, learning how to open a GBP account for a non-UK company does not require opening a full UK bank account. FCA-authorised Electronic Money Institutions can issue UK local GBP payment details — including a sort code and account number — to eligible foreign-registered companies. This means payments from UK clients may arrive on domestic rails, potentially avoiding SWIFT deductions, correspondent banking delays, and the conversion friction that comes with international wires.

Why this matters commercially: UK customers typically expect to pay a local GBP account. Providing domestic details can reduce payment friction, simplify reconciliation, and remove questions from client finance teams about unfamiliar SWIFT references or foreign bank names.

This guide explains the structure of the account being opened, how UK sort codes function in an EMI context, what documents providers typically require, and when a full UK bank relationship remains the more appropriate choice.

Can a Non-UK Company Open a GBP Business Account with Sort Code?

Yes, often — but eligibility is not universal, and the route that works depends on the company's structure, jurisdiction, and compliance profile.

FCA-authorised EMIs and regulated payment institutions may offer a GBP account with a UK sort code to foreign-registered companies, assessed on a case-by-case basis. Traditional UK high-street banks generally require stronger local substance — UK registration, a UK business address, and often in-person identity verification. GOV.UK guidance on registering as an overseas company acknowledges that overseas companies may need to provide a UK business plan, a UK-registered address, and in some cases have a representative travel to the UK for in-person verification before a full bank account is opened.

FCA-authorised EMIs assess eligibility differently, typically evaluating the company's compliance profile, beneficial ownership transparency, business activity, and jurisdiction. In practice, approval usually turns less on "non-UK" status and more on whether the provider can quickly verify three things: who ultimately owns the company, what the business actually does, and why GBP flows are commercially expected. A UAE software company invoicing UK clients on annual subscriptions is a considerably easier compliance case than a holding structure spanning multiple jurisdictions with no clear operating entity, no customer contracts, and vague source-of-funds explanations.

Jurisdiction matters. Not all foreign-registered companies are assessed identically. Providers typically distinguish between:

Standard profiles — companies in major financial centres (UAE, Singapore, Hong Kong, US, EU member states) with transparent ownership and clear commercial activity. UAE-incorporated businesses, for example, can often access a GBP account with a UK sort code through an EMI without the friction associated with traditional bank onboarding.

Enhanced due diligence profiles — offshore jurisdictions such as BVI, Cayman Islands, Seychelles, or Delaware LLCs used as holding vehicles, where additional documentation and longer review times are common. BVI-incorporated companies face a specific set of documentation expectations when obtaining UK bank details without UK presence.

Outside risk appetite — certain jurisdictions, sectors, or ownership structures that a given provider does not accept at all

Confirming provider eligibility criteria before submitting an application is the most efficient use of preparation time.

💡 Evaluating GBP alongside EUR or USD? Before deciding between a bank route and a payment-account route, review EQWIRE's multi-currency account overview to understand local collection and outbound payment capability across currencies, and to assess whether your company profile is likely to be eligible. Review EQWIRE's account overview

Best GBP Account Option for a Non-UK Company: EMI vs UK Bank vs International Bank

The right structure depends on what the business needs to do with GBP, not just on which option is most accessible.

EMI / payment account | UK bank account | International bank with GBP capability | |

|---|---|---|---|

UK entity required | No | Often yes (or strong UK substance) | No |

Local GBP sort code + account | Yes (provider/sort-code specific) | Yes | Sometimes (varies by bank) |

Faster Payments / Bacs | Yes, where rail-enabled | Yes | Rarely |

CHAPS | Some providers | Yes | Rarely |

Client fund protection | Safeguarding (not FSCS) | FSCS up to £120,000 | Varies by jurisdiction |

Lending / overdraft | No | Yes | Varies |

Onboarding friction | Lower for foreign companies | Higher — may require UK presence / in-person | Moderate |

Best fit | Foreign companies needing GBP local collection or outbound payments | Companies establishing formal UK presence | Companies needing GBP as secondary currency |

Bottom line: Most foreign-registered companies that need to collect GBP locally or pay UK suppliers do not need a full UK bank account. An EMI-issued payment account meets those needs for many profiles. A full bank becomes relevant when the company is formally entering the UK market, needs credit products, or faces institutional requirements that specify a bank account specifically.

What Is a UK Payment Account for a Foreign Registered Company?

A UK payment account issued by an EMI gives a foreign-registered business a sort code, account number, and access to UK domestic payment rails — but it is not a bank account and is regulated differently.

How UK sort codes work

A sort code is a six-digit identifier that routes payments through UK clearing systems to the correct payment service provider. Sort codes are allocated to PSPs — not to individual account holders — and registered for use within specific payment schemes. Pay.UK, which operates Bacs and the Image Clearing System, and Faster Payments Scheme Limited each maintain sort code registration separately.

This means the sort code on an EMI-issued account will typically not match any recognisable high-street bank branch. In practice, this rarely affects routine payment flows. However, rail availability is provider- and sort-code-specific. Before using a GBP account for collections or payouts, confirm that the sort code is enabled for the specific payment types required — Faster Payments, Bacs, CHAPS, or Direct Debit.

EMI regulation versus bank regulation

An EMI authorised by the FCA operates under the Electronic Money Regulations 2011 and the Payment Services Regulations 2017. These require EMIs to safeguard relevant funds — meaning client money must be held separately from the EMI's own funds, in a protected account with a credit institution or invested in qualifying low-risk liquid assets.

Safeguarding is not the same as FSCS deposit protection. FSCS protection covers eligible deposits at UK-authorised banks, building societies, and credit unions — the current limit is £120,000 per eligible depositor. Payment and e-money firms are explicitly outside FSCS deposit protection; in an insolvency event, safeguarded funds are ringfenced and returned through an administration process.

For most routine GBP payment flows — collecting from clients, paying suppliers, maintaining an operating balance — the distinction does not affect daily functionality. It becomes most relevant for companies holding large GBP balances over time, those subject to treasury policies that specify deposit protection, or those whose auditors or regulators require a bank account specifically.

Note: The FCA strengthened its safeguarding rules for payment firms and e-money institutions, with the Supplementary Regime coming into force on 7 May 2026. Businesses should review a provider's current safeguarding disclosures directly. See the FCA's PS25/12 policy statement and safeguarding requirements page for current requirements.

Feature | UK Bank Account | EMI GBP Payment Account |

|---|---|---|

Onboarding Friction | Often higher | Often lower |

Local GBP Details | Yes | Often yes |

Fund Protection | FSCS protection for eligible deposits | Safeguarding of relevant funds |

Payment Rails | Rail availability varies by provider | Rail availability varies by provider |

Lending Access | Available | Not available |

Best Fit For | UK presence, lending, or FSCS-eligible deposit protection needs | Foreign businesses with GBP collection or payment needs |

Features vary by provider, jurisdiction, and payment rail availability.

Why Are Traditional UK Banks Harder for Foreign-Registered Companies?

The additional requirements traditional UK banks apply to overseas companies reflect standard due diligence practice and, in some cases, the practical limits of remote onboarding for relationship banking products.

GOV.UK guidance on registering as an overseas company acknowledges that overseas companies seeking a full UK bank account may need to provide proof of UK registration, a UK business address, a detailed UK business plan, and in some cases send a representative to the UK for an in-person meeting. Those requirements are manageable if the company is actively establishing a UK presence — but they are impractical for a foreign-registered business that simply needs to invoice UK clients or pay UK suppliers without first creating a UK entity.

The FCA-authorised EMI and regulated payment institution market developed partly in response to this structural gap. Remote KYC, digital onboarding, and technology-driven compliance review make it possible for a cross-border operating company to access a UK payment account for a foreign registered company without the logistical barriers that traditional bank mandates can impose. That does not mean EMI onboarding is simple or that all applications succeed — compliance standards at regulated providers can be rigorous — but country of incorporation is no longer the primary barrier it once was.

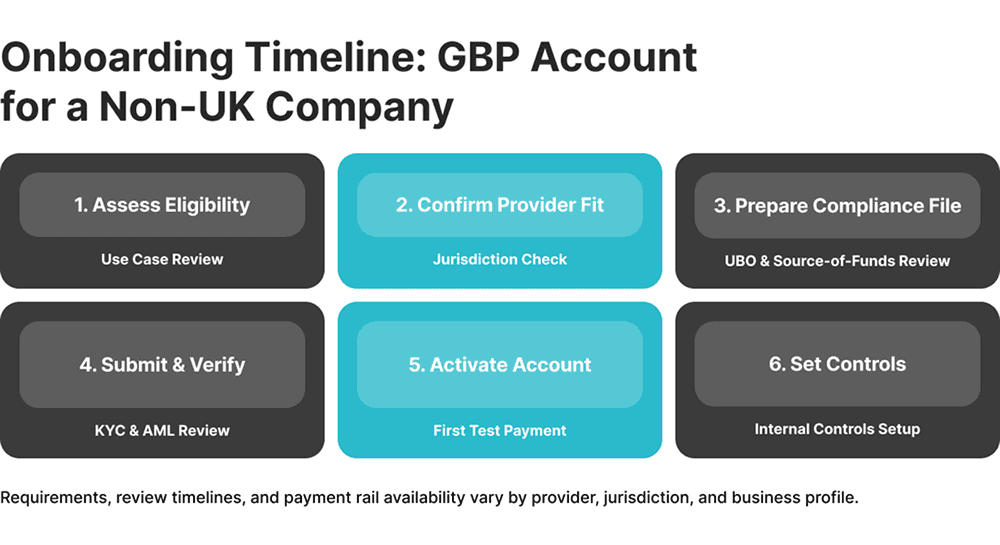

How to Open a GBP Account for a Non-UK Company: Step-by-Step

Step 1. Clarify the actual use case

The required setup differs significantly depending on whether the objective is:

Local GBP collection only — receiving inbound payments from UK clients through Faster Payments or Bacs, avoiding SWIFT routing

Local outbound payments — paying UK suppliers or contractors in GBP using domestic rails

Multi-currency treasury — holding GBP alongside EUR, USD, or other currencies within a single operating account

Formal UK establishment — supporting UK payroll, institutional payments, or a UK banking relationship

Mapping the use case first avoids opening an account that handles inbound flows but cannot make outbound local payments, or one that lacks the specific rail the business needs.

Use an EMI if: you need local GBP collection, outbound supplier payments, or multi-currency operating infrastructure — without requiring credit facilities or formal UK banking relationships.

Consider a UK bank if: you are incorporating a UK entity, need lending products, or face institutional requirements that specify a bank account rather than a payment account.

Expect enhanced due diligence if: your company is incorporated in an offshore or high-scrutiny jurisdiction (BVI, Cayman, Seychelles), has layered ownership, or operates in a sector with higher compliance thresholds.

Step 2. Check provider fit before applying

Not every regulated provider accepts every business profile. Confirming eligibility before preparing documentation saves significant time. Key factors:

Jurisdiction of incorporation — some jurisdictions are accepted as standard; others trigger enhanced due diligence or fall outside a provider's risk appetite

Beneficial ownership transparency — layered structures with multiple holding entities require more documentation and review time

Business activity — certain sectors face higher compliance thresholds or are excluded entirely

Transaction profile — high-value or high-frequency flows require a more detailed source-of-funds narrative

Step 3. Prepare the compliance file

Most application delays stem from incomplete or inconsistent documentation, not from the concept of the account itself. A well-prepared compliance file — submitted completely the first time — is the most reliable way to reduce elapsed time from application to approval.

See the next section for a breakdown of what providers typically request.

Step 4. Submit the application and complete KYC/AML checks

The provider's compliance team will review the application against internal policy and regulatory obligations. Simple structures with complete documentation typically progress faster. Complex profiles — layered ownership, sanctions-adjacent jurisdictions, regulated business sectors — commonly require follow-up and take longer.

The process of opening a GBP account for a non-UK registered company via an FCA EMI typically involves document submission, automated screening, and manual compliance review. Some providers request a video call or written beneficial ownership confirmation before issuing account details.

Step 5. Receive local GBP details and test the first transfer

Once approved, the provider issues a sort code, account number, and access credentials. Before updating payment instructions across all counterparties:

Confirm which payment rails the sort code supports (Faster Payments, Bacs, CHAPS, Direct Debit)

Confirm inbound and outbound transaction limits

Set up user access and permissions for finance team members

Send a small test transfer and confirm receipt

Step 6. Set internal controls for ongoing use

Internal controls worth establishing from the outset:

Approval thresholds for outbound payments

Reconciliation processes aligned with existing accounting systems

Clear instructions to counterparties on whether to use local GBP details or SWIFT

Treasury policy for GBP balance holding versus sweeping to a primary operating currency

Reporting processes for large or unusual transactions

What Documents Does a Foreign Company Need to Open a GBP Account UK?

Providers assess four categories of documentation. Completeness and coherence — especially in the business-evidence category — is what separates a fast application from a slow one.

Category | Commonly requested documents | Why it matters |

|---|---|---|

Company documents | Certificate of incorporation, constitutional documents (articles/charter), certificate of good standing (where relevant), company register extracts | Confirms the entity exists, is in good standing, and its legal structure is understood |

Ownership documents | Full beneficial ownership structure, shareholder registry, UBO declarations (typically 25%+ threshold), corporate structure chart for multi-entity groups | Confirms who ultimately owns and controls the business — the central question in AML compliance |

Individual verification | Valid passport/national ID for each director and UBO, proof of residential address (typically within 3 months) | Identity verification and sanctions/PEP screening for individuals with control |

Business evidence | Company website, sample invoices or contracts, source-of-funds explanation, existing bank statements | Confirms the business is real, commercially coherent, and that GBP flows are commercially expected |

The business-evidence category is where most weak applications fall short. A complete file for a SaaS company invoicing UK enterprise clients would include a sample subscription agreement, a recent invoice, a brief explanation of the billing model, and confirmation of where GBP revenue originates. A file that correctly identifies directors but omits any commercial context will typically generate multiple follow-up requests before review can proceed.

"Opaque ownership" in practice means a structure where the individuals who ultimately own or control the business cannot be quickly identified from the documents submitted. This commonly occurs when shares are held through nominee arrangements, where a holding company sits between the individual and the operating entity without documentation of who owns the holding company, or where a trust structure is involved without disclosure of the settlor and beneficiaries.

A weak source-of-funds explanation is one that describes what the business does without explaining why the specific payment flows being proposed are commercially expected. "We are a technology company" is insufficient. "We are a UAE-incorporated SaaS platform with 40 UK-based enterprise clients on annual GBP contracts; inbound payments are typically £5,000–£50,000 from UK corporate accounts on 30-day invoice terms" is a source-of-funds explanation that a compliance reviewer can verify and close.

How Does a Non-UK Business Get a UK Sort Code and Account Number via EMI?

A sort code is allocated to the payment service provider, not to the individual business. When an EMI issues a GBP account to a foreign-registered company, the business receives an account number under a sort code the provider already holds.

Sort codes are registered with the relevant payment scheme operators — Pay.UK for Bacs and the Image Clearing System, Faster Payments Scheme Limited for Faster Payments — and each sort code is registered only for the payment types it participates in. EMIs access the payment schemes either through direct membership or through a sponsored access model, where a scheme member processes transactions on behalf of the EMI.

From the account holder's perspective: inbound and outbound payments route using that sort code and account number exactly as they would for a bank-issued account. UK counterparties typically have no visibility into whether the underlying provider is a bank or a regulated EMI.

Rail availability is not automatic. Not every sort code supports every payment type. Before relying on a GBP account for a specific payment type, confirm that the sort code is enabled for:

Faster Payments — near-instant transfers up to scheme limits

Bacs — batch processing including Direct Credit and Direct Debit

CHAPS — same-day high-value settlement (not universally available from EMIs)

For more detail on how Faster Payments works for offshore structures and what settlement timelines apply, see GBP Faster Payments for Offshore Company: Same-Day Settlement Guide.

Which Route Fits Your Business? A Decision Framework

Rather than comparing providers on headline fees, match the account structure to the business's actual requirements:

If the business needs… | Likely best fit |

|---|---|

Receive GBP from UK clients on domestic rails | EMI payment account with Faster Payments / Bacs |

Pay UK suppliers in GBP without SWIFT routing | EMI with outbound local payment capability |

Hold GBP balances with FSCS deposit protection | UK-authorised bank deposit account |

UK entity setup, payroll, lending, or credit | Full UK bank account |

GBP + EUR + USD in one operating account | Multi-currency EMI account |

Institutional counterparty requires a named UK bank | Full UK bank account |

Offshore holding company (BVI, Cayman, Seychelles) with operating flows | EMI — but expect enhanced due diligence and longer review |

Questions to ask any provider before applying:

Do you accept companies incorporated in [jurisdiction]?

Which payment rails are available — Faster Payments, Bacs, CHAPS, Direct Debit?

Are there transaction or balance limits that apply to new accounts?

How are client funds safeguarded, and is the platform FCA-authorised?

What is the typical timeline from application submission to account issuance for a profile like ours?

What business sectors or ownership structures fall outside your risk appetite?

When Does a Company Need a Full UK Bank Account Instead of a GBP Payment Account?

An EMI-issued payment account meets the requirements of most foreign-registered businesses needing local GBP collection or outbound UK payments. But there are specific scenarios where a full UK bank account is the more appropriate route.

A full UK bank account is typically more relevant when:

The company is formally establishing a UK presence — incorporating a UK entity, opening a UK office, or taking on UK employees changes the context and may require a banking relationship

Lending or credit facilities are required — EMIs do not offer overdrafts, business loans, or trade finance; those require a bank

Institutional counterparties specify a bank account — some auditors, regulators, landlords, or large corporate counterparties may require payments to come from a recognised UK bank rather than a payment account

FSCS deposit protection is a specific requirement — treasury policies or regulatory obligations that specify FSCS-protected deposits cannot be met by an EMI account

Specific banking services are required — letters of credit, foreign exchange lines, and certain trade finance products are not available from most EMIs

GOV.UK guidance on registering as an overseas company notes that overseas companies establishing a UK presence may face additional requirements when opening full bank accounts, including UK registration, a UK business plan, and in-person verification. Many foreign-registered businesses find that a GBP payment account meets their needs while UK operations are limited to receivables and payments; a full banking relationship becomes relevant as the business establishes more formal UK presence.

💡 Understand safeguarding and eligibility before applying Review EQWIRE's Important Information and How We Protect Your Money pages to assess regulatory structure, customer fund protection model, and eligibility context before submitting an application.

Common Reasons GBP Account Applications Are Delayed or Declined

Incomplete UBO documentation — the most common cause of delay. If the chain of ownership cannot be traced to named individuals in the documents submitted, review pauses.

Weak or absent source-of-funds narrative — identifying directors is not the same as explaining the business. Compliance reviewers need to understand why GBP flows are commercially expected, not just who is involved.

Mismatched business evidence — a company website that does not match the described business activity, or invoices that are inconsistent with the stated transaction profile, will generate follow-up questions.

Applying to the wrong provider — some providers do not accept certain jurisdictions or sectors, regardless of documentation quality. Checking eligibility criteria before applying is more efficient than a declined application.

Assuming inbound and outbound are both available — some accounts support local GBP collection but have limited or no outbound local payment capability. Confirm both directions if both are needed.

Treating the application as an admin task — providers are assessing whether the business is real, commercially coherent, and consistent with the proposed payment flows. Applications that reflect this — with a complete, well-contextualised file — progress faster.

Overlooking future multi-currency needs — opening a GBP-only account when EUR or USD local details will also be needed within twelve months creates unnecessary account migration later. Raising multi-currency requirements upfront is more efficient.

Next Steps for Businesses That Need UK Local GBP Collection

For foreign-registered companies that have identified a genuine need for UK local GBP payment details, the practical next step is to assess whether the business profile fits an EMI-led payment account route — or whether a full UK bank relationship is more appropriate for the specific requirements involved.

EQWIRE operates as an FCA-authorised multi-currency payment account environment, supporting GBP, EUR, and USD local payment details for eligible foreign-registered businesses. Regulatory context, safeguarding arrangements, eligibility criteria, and policy documentation are available on-site before any application is submitted.

Eligible non-UK companies may access local GBP, EUR, and USD details through a single multi-currency account — best fit for companies needing operating infrastructure across currencies rather than a single-currency collection setup.

Before applying, review:

EQWIRE's product overview — multi-currency account capability and GBP payment infrastructure

Important Information — regulatory and policy context

How We Protect Your Money — safeguarding structure and customer fund protection

GBP Faster Payments for Offshore Company: Same-Day Settlement Guide — infrastructure and settlement detail

Not sure whether you need an EMI account or a full UK bank? Use the eligibility checklist to assess which route fits your company's structure, payment needs, and compliance profile — before submitting an application.

Element | UK Local Payment Rails | SWIFT International Transfer |

|---|---|---|

Payer | UK Client | UK Client |

First route step | Faster Payments / Bacs | SWIFT Transfer |

Receiving provider | FCA-authorised EMI | Correspondent / intermediary banking chain |

Account details used | UK sort code and account number | International SWIFT wire details |

Typical flow | UK Client → EMI with UK local details → Foreign-registered company GBP account | UK Client → SWIFT network → Correspondent bank → Intermediary bank → Foreign-registered company GBP account |

Intermediaries | Fewer | Multiple |

Main visual message | More direct domestic routing | More intermediated international routing |

FAQ

Can a non-UK company open a GBP business account with sort code?

In many cases, yes. FCA-authorised EMIs and regulated payment institutions may issue a GBP account with a UK sort code and account number to eligible foreign-registered businesses, without requiring UK company registration. Eligibility depends on the provider, the jurisdiction of incorporation, the beneficial ownership structure, and business activity. Traditional UK high-street banks typically impose more onerous requirements — including UK registration and sometimes in-person verification — making the EMI or payment-institution route more practical for many foreign-registered companies. Approval is not guaranteed and is assessed on a case-by-case basis.

What documents does a foreign company need to open a GBP account UK?

Providers commonly assess four categories: company documents (certificate of incorporation, constitutional documents, register extracts), ownership documents (full UBO structure, shareholder registry, corporate structure chart), individual verification (passports and proof of address for directors and UBOs), and business evidence (website, sample invoices or contracts, source-of-funds explanation, bank statements). The business-evidence category — particularly the source-of-funds explanation — is the factor most likely to determine whether an application is approved promptly or requires multiple rounds of follow-up. Identity documents alone are not sufficient; providers need to understand that the business is real and that the proposed GBP flows are commercially expected.

How does a non-UK business get a UK sort code and account number via EMI?

The sort code is held by the EMI or payment service provider, not allocated directly to the individual business. The EMI registers the sort code with the relevant payment scheme operators and issues account numbers to clients within that sort code structure. When UK counterparties make a payment using that sort code and account number, funds route to the EMI and are credited to the business's account. The EMI accesses payment rails through direct scheme membership or a sponsored access model. From the account holder's perspective, the account functions identically to a bank-issued sort code and account number for routine GBP payment flows — but rail availability should be confirmed, as not every sort code supports every payment type.

How long does it take to open a GBP account for a non-UK company?

Timelines vary significantly by provider and profile complexity. A company with straightforward single-jurisdiction ownership, a clear commercial activity, and a complete compliance file can expect a faster review than a company with layered ownership, multiple jurisdictions, or operations in a sector that requires enhanced due diligence. GOV.UK guidance on registering as an overseas company notes that overseas companies opening traditional bank accounts may face longer timelines due to additional verification requirements; digital payment providers typically position their onboarding as faster, but complex profiles will extend the review regardless. Preparing a complete file before submitting — rather than responding to follow-up requests sequentially — is the most reliable way to reduce elapsed time.

Is a UK payment account for a foreign registered company the same as a bank account?

No. A GBP payment account issued by an FCA-authorised EMI provides a sort code, account number, and access to UK payment rails, but it is not a bank account and is not subject to the same regulatory framework. EMIs are required to safeguard eligible client funds by holding them separately from the EMI's own funds in ringfenced accounts. This differs from FSCS deposit protection, which covers eligible deposits at UK-authorised banks up to £120,000 per eligible depositor. In an EMI insolvency event, safeguarded funds are returned through an administration process — meaningfully different from the FSCS guarantee. For most routine GBP payment flows, this distinction does not affect daily functionality. It matters most for companies holding large balances over time, or those subject to treasury or audit policies that specify deposit protection or a recognised UK bank specifically.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)