•

•

Named IBAN Business Account in the UK: What It Is and How to Get One

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

A named IBAN account gives your business its own IBAN for receiving payments, instead of sharing a pooled account that depends on references for attribution. For UK companies receiving EUR, that usually means cleaner reconciliation, stronger audit trails, and better SEPA payment handling.

But the term "named IBAN" is used loosely in the UK market — by banks, EMIs, and fintech platforms — to describe account structures that work quite differently under the surface. Understanding what you are actually buying, and whether it fits your operational and compliance requirements, is the decision this guide is designed to support.

Key Takeaways

A named IBAN is an IBAN allocated exclusively to one business, not shared across multiple clients through a pooled structure — but the market term covers both directly allocated accounts and virtual IBAN arrangements.

The UK remains a non-EEA SEPA country according to the EPC's current SEPA country list, but actual SEPA product support depends on the specific provider.

UK EMIs safeguard client funds under FCA rules — they do not offer FSCS deposit protection, which now covers eligible deposits up to £120,000 at UK-authorised banks.

The EPC's Verification of Payee scheme now checks payee name against IBAN on SCT and SCT Instant transfers — making business-name consistency in your account setup operationally important from 2025 onwards.

Provider fit, documentation quality, and a clearly stated EUR use case matter more than the label on the product.

What Is a Named IBAN Account for Business in the UK?

A named IBAN account is an IBAN allocated to one specific business or customer — not pooled with other clients — so that incoming payments are attributed directly to that business without depending on payment references.

"Named IBAN" is a commercial term, not a regulatory category. Providers use it to signal that the IBAN belongs to one account holder, but the underlying infrastructure varies. Some institutions issue a directly allocated account with its own sort code and account number, generating a GB IBAN from that base. Others deliver the same commercial experience through virtual IBAN (vIBAN) infrastructure: a unique IBAN linked to a master account, where your receiving details are distinct but funds settle into a shared ledger behind the scenes.

One thing named IBAN does not mean: your company name encoded inside the IBAN string itself. IBANs follow a fixed format — country code, check digits, sort code, account number — and carry no embedded name data. The "named" element refers to exclusive allocation, not encoding.

The distinction between named, dedicated, pooled, and virtual structures has regulatory weight, not just operational weight. The EBA's report on virtual IBANs notes there is currently no EU-level legal definition of vIBANs, and highlights material risks alongside the reconciliation benefits — including AML/CFT transparency concerns and potential confusion about which entity actually holds the funds. That context matters when evaluating any provider's "named IBAN" product.

How Does a Named IBAN Business Account Work in the UK?

A UK business with a named IBAN can receive EUR payments into account infrastructure registered to that business, hold the balance, and send EUR outbound via SEPA or SWIFT — without routing through a shared collection pool.

The operational flow is straightforward. You issue an invoice to a European client, listing your EUR IBAN as the beneficiary. The client's bank initiates a SEPA Credit Transfer. The payment arrives attributed to your business, reconciles against the invoice, and sits in your EUR balance. You can then pay EUR suppliers, convert to GBP, or transfer onward via SWIFT.

Here is what that looks like for a concrete business scenario:

A UK e-commerce business receives a weekly EUR settlement from a German marketplace. The settlement arrives into the business's named EUR IBAN. Finance matches the payment against the expected figure without chasing remittance advice. The same account sends EUR to a Spanish logistics supplier two days later.

The same account typically supports GBP local rails — Faster Payments and CHAPS — alongside EUR SEPA, depending on the provider. That is what makes a named IBAN business account EUR UK setup operationally efficient: one environment covers domestic GBP activity and cross-border EUR flows, without managing two separate banking relationships.

Some providers issue a single company-level EUR IBAN. Others offer multiple virtual collection IBANs routing to a consolidated EUR balance. Either can work — provided you understand which structure you hold and what it means for attribution, statement clarity, and Verification of Payee compliance.

Named IBAN vs Pooled IBAN UK Business: What Is the Difference?

Named or dedicated structures assign distinct receiving details to one business, so attribution is automatic. Pooled structures share one account across multiple clients and depend on payment references for attribution — which fails regularly in practice.

The difference between named IBAN and pooled IBAN UK business account setups becomes most visible at scale: with multiple EUR payers, a missing or incorrect reference in a pooled account creates manual matching workload, reconciliation errors, and potential reporting delays.

Feature | Named / Dedicated IBAN | Pooled / Reference-Based IBAN | Virtual IBAN (vIBAN) |

|---|---|---|---|

Attribution | Automatic | Reference-dependent | Automatic (if properly configured) |

Reconciliation effort | Low | High | Low to medium |

Audit trail | Direct and clean | Dependent on reference accuracy | Depends on provider ledger design |

Counterparty confidence | High | Lower | High, with caveats |

EBA risk flagging | Not applicable | Not applicable | Yes — transparency and AML risks noted |

Best for | Recurring EUR counterparties, multi-payer operations | Simple, single-sender, low-volume | High-volume reconciliation at platform scale |

Virtual IBANs can deliver a named experience — a unique receiving IBAN assigned to your business — even when settlement sits within a master account. But the EBA has flagged that vIBAN arrangements can obscure which legal entity actually holds the funds, create AML/CFT transparency gaps, and confuse customers about their protection status. For a UK SMB choosing between account structures, this means the question is not only whether the IBAN feels named — it is whether the provider can demonstrate how attribution, settlement, and safeguarding actually work under the surface.

Where a pooled arrangement is still acceptable: low-volume operations with a single, reliable EUR counterparty who consistently includes correct payment references.

Why Does a UK Business Need a Named EUR IBAN With SEPA Access?

The operational case is cleaner EUR collections, easier reconciliation, more reliable counterparty relationships, and better financial visibility — not prestige or branding.

Four business scenarios where the difference is material:

SaaS platforms billing European subscribers in EUR need each inbound payment to reconcile automatically against the correct customer account. A pooled structure with reference-based attribution creates errors at scale.

E-commerce businesses receiving weekly EUR marketplace settlements need a stable named IBAN that European platforms can pay reliably — without treating the destination as a third-party intermediary.

Consultancies and IT service providers invoicing EU clients on retainer need payment infrastructure that signals financial credibility. A named EUR IBAN with SEPA access carries more operational weight with European finance teams than a shared collection account.

Import/export businesses paying EUR suppliers regularly need outbound SEPA capability from the same account as inbound EUR collections — eliminating conversion steps before each supplier payment.

In each case, how a named IBAN improves compliance and audit-readiness for a UK business comes down to the same principle: clean attribution, traceable payment flows, and statements that reconcile without manual intervention.

Verification of Payee: Why Business-Name Consistency Now Matters More

Since 2024, the EPC's Verification of Payee (VoP) scheme checks the payee's name against the IBAN before a SEPA Credit Transfer or SEPA Instant payment is processed — making the name registered to your account operationally important in a way it was not before.

For UK businesses receiving EUR, this has a practical consequence: the name on your named IBAN should match the name your European clients will enter when they initiate a SEPA transfer. If your trading name differs from your registered legal name, or if your account is registered to a holding entity rather than the operating business, VoP checks may return a mismatch — causing payment delays or rejection on the sender's side.

What to check before going live with a named EUR setup:

Confirm the exact business name registered to the IBAN with your provider

Ensure invoices and contracts use the same name

Ask your provider whether their VoP implementation covers SCT, SCT Instant, or both

Consider how the name appears to a European sender initiating a payment through their bank

The EPC's Verification of Payee Scheme Rulebook sets out how name matching works across scheme participants. Not all providers have implemented VoP at the same pace — confirming your provider's current status is a practical step before migrating live payment flows.

💡 Is your current EUR setup truly named — and is the registered name consistent with how counterparties will pay you? Mismatched names and pooled collection structures are two of the most common causes of EUR payment delays for UK businesses. Review whether your current setup supports clean attribution and passes Verification of Payee checks. Explore EQWIRE's multi-currency account structure →

Can a UK EMI Provide a Named IBAN Account With SEPA Access?

Yes — an FCA-authorised UK EMI can support EUR and SEPA-reachable structures, including named IBAN setups — but product capability varies by institution, and the protection model is materially different from a bank.

An EMI is not a bank. It holds an FCA authorisation to issue electronic money and provide payment services, but not a banking licence. The protection difference is significant:

At a UK-authorised bank, building society, or credit union, eligible deposits are now protected up to £120,000 per person per firm by the FSCS — a limit that increased from £85,000 on 1 December 2025.

At a UK EMI, funds are not FSCS-protected. Instead, the EMI is required to safeguard client funds: holding them in a segregated account at a credit institution or investing them in secure low-risk assets, separate from the EMI's own money.

Safeguarding means you should receive most of your money back if the EMI fails — but return may be delayed and could be reduced by administration or liquidation costs. The FCA has also introduced stronger safeguarding rules taking effect on 7 May 2026, raising the operational standard EMIs must meet. For a UK business choosing between routes, the question is not which protection model is "better" in the abstract — it is which model fits your risk tolerance and balance-holding requirements.

In operational terms, many UK EMIs offer EUR IBANs with SEPA Credit Transfer access, and some also support SEPA Instant, SWIFT, and GBP Faster Payments from one environment. But product capability is not uniform. Before assuming a named IBAN account with SEPA access UK EMI covers your exact requirements, confirm which rails are live, not just listed.

See EQWIRE's regulatory information page for an example of how a UK EMI should disclose its regulatory status and safeguarding arrangements.

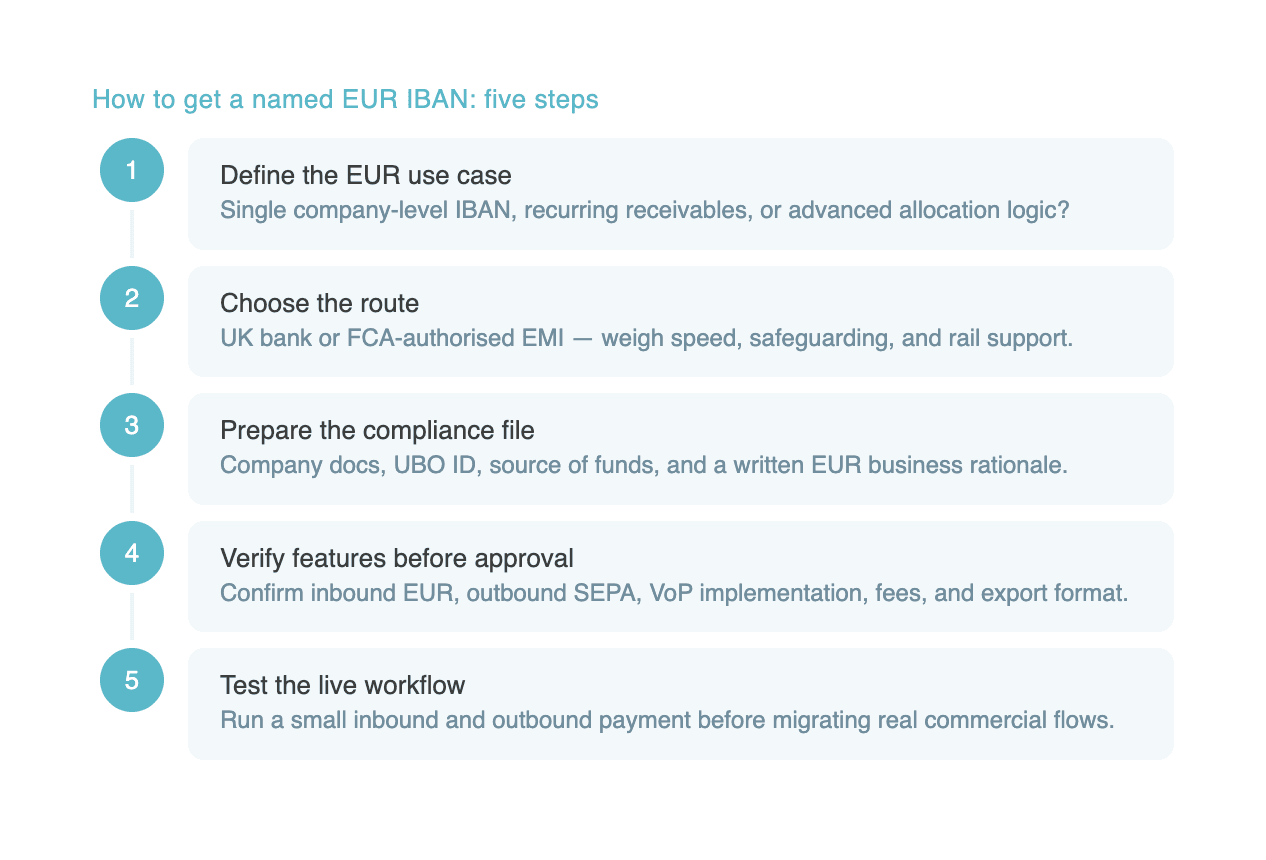

How to Get a Named EUR IBAN for Business in the UK

Getting a named EUR IBAN is a structured process that depends on use-case clarity, provider selection, documentation preparation, feature verification, and post-go-live testing — in that order.

Here is the step-by-step process for getting a named EUR IBAN with SEPA access via a UK FCA EMI account or bank route.

Step 1. Define the Exact EUR Use Case

Before approaching any provider, clarify what the account needs to do. Receiving EUR from a single European client is a different operational requirement from managing EUR payables to multiple suppliers, or handling high-volume marketplace settlements. The answer determines whether a single company-level named IBAN is sufficient or whether you need virtual collection IBANs for more advanced attribution logic.

Step 2. Decide Whether a Bank or UK EMI Route Is More Realistic

UK banks offer FSCS protection and established credibility, but onboarding for newer or non-standard businesses can be slow and restrictive. UK FCA-authorised EMIs are typically faster to onboard, more flexible on business type, and better suited to multi-currency operating needs — but operate under safeguarding rather than FSCS protection. The right route depends on your business structure, balance-holding requirements, and how quickly the account needs to be operational.

Step 3. Prepare the Compliance File Before Applying

Incomplete applications are the most common cause of avoidable delays. Providers conducting KYB and KYC checks need to verify business legitimacy, ownership transparency, and genuine EUR payment need. Prepare:

Company incorporation certificate and articles of association

Certificate of good standing (for companies over 12 months old)

Directors' identification — passport or national ID, proof of residential address

UBO identification and ownership structure chart for any beneficial owner holding 25% or more

Proof of registered business address

Source-of-funds documentation — bank statements, audited accounts, or investor confirmation

Commercial EUR evidence — website, client contracts, invoices, or counterparty correspondence

A written EUR business rationale covering use case, expected volumes, and counterparty profile

The written EUR rationale is frequently the document that separates approved applications from delayed ones. Providers need to understand the payment use case before approval to meet their own regulatory obligations.

Step 4. Confirm Operating Features Before Approval

Do not assume "named IBAN" includes everything your business requires. Before completing an application, confirm: inbound EUR via SEPA Credit Transfer, outbound EUR via SEPA, GBP local rail support, statement export format, user access controls, and the fee schedule for EUR transactions and FX conversion. Also confirm whether the provider has implemented Verification of Payee and how the registered account name will appear to sending banks.

Step 5. Test the Workflow After Go-Live

Once the account is open, run a small inbound EUR test payment from a known counterparty and verify it arrives with correct attribution. Make a small outbound EUR payment and confirm it processes within the expected timeframe. Check that the statement export aligns with your accounting system format. Treat the setup as fully operational only after confirming the end-to-end workflow.

For businesses with offshore or multi-jurisdiction EUR account requirements, the EQWIRE guide on opening a SEPA business account for a Caribbean company covers how the same compliance logic applies in a different operating context.

What Documents and Eligibility Checks Are Usually Required?

Expect business verification, ownership transparency, identity checks, and evidence of genuine commercial EUR activity — not just a registration number and a passport scan.

Standard documentation across UK banks and EMIs offering named EUR IBAN accounts includes:

Company incorporation certificate — confirming legal existence and registered jurisdiction

Certificate of good standing — for companies more than 12 months old

Articles of association — confirming ownership and governance structure

Director identification — passport or national ID, residential address proof

UBO identification and ownership chart — for any beneficial owner holding 25% or more

Proof of business address — utility bill, lease agreement, or official correspondence

Source-of-funds documentation — bank statements, audited accounts, or investor confirmation

EUR commercial activity evidence — website, client contracts, invoices, counterparty correspondence

Written EUR business rationale — use case summary, expected monthly volumes, counterparty profile

Providers ask for the written rationale because it supports their own regulatory obligations under UK AML and payment-services rules. A vague or absent rationale is one of the most common reasons for delayed or rejected applications.

Can a Founder Use a Named Personal IBAN Account in the UK Instead?

A personal IBAN may receive EUR payments in practice, but using one for business trading activity creates bookkeeping complexity, potential provider policy violations, and weaker audit-readiness — and is not a substitute for a business-grade named structure.

For occasional low-value EUR receipts, a personal multi-currency account may function. But as volume increases, the limitations surface quickly: mixed personal and business transactions create reconciliation work, breach most providers' terms of service, and produce statements that do not support clean financial reporting. European clients and suppliers paying into a personal IBAN may also raise compliance questions on their end when matching payments to corporate counterparties. For any business with recurring EUR income, a business-grade named structure is the operationally sounder choice.

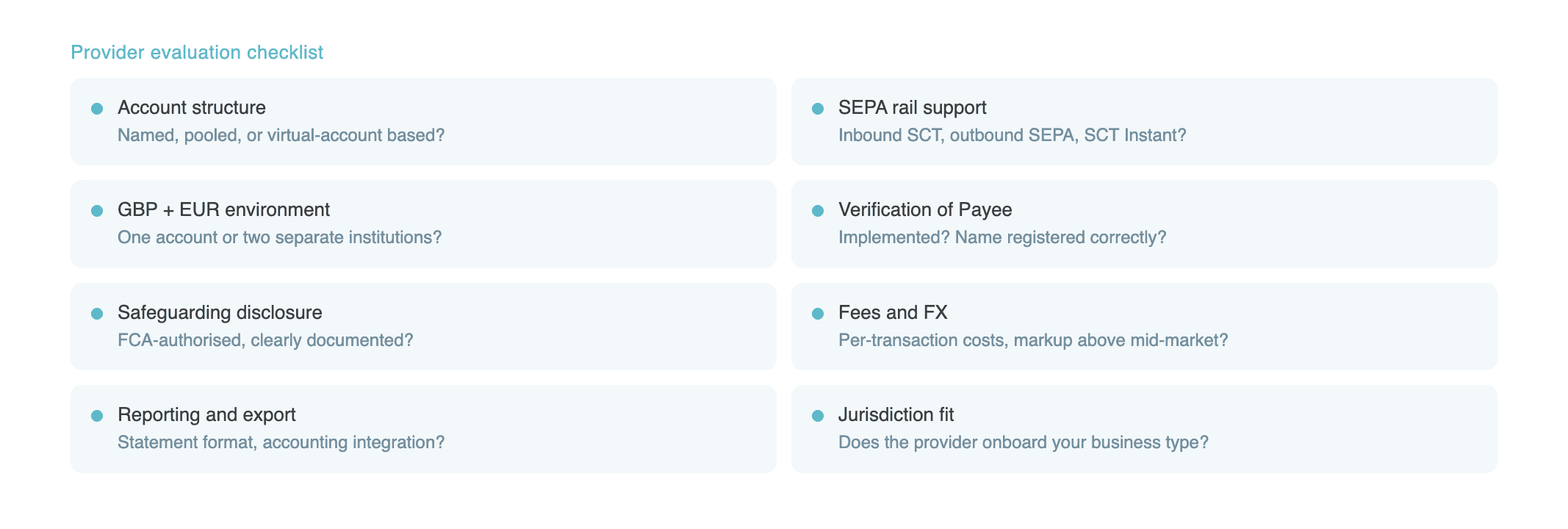

What Should a UK Business Check Before Choosing a Provider?

Provider selection is a structure-and-control decision — the question is not what the product is called, but how it behaves operationally for your specific use case.

Before committing to any provider, check:

Account structure: Is the IBAN named to your business specifically, pooled across clients, or virtual-account based? If virtual, confirm how attribution, settlement, and safeguarding work in practice — and whether the EBA's flagged risks around transparency and protection apply.

SEPA reachability: Does the account support inbound SEPA Credit Transfer? SEPA Instant? Outbound SEPA? Confirm each rail individually, not just from a product description.

GBP and EUR from one environment: Can you manage domestic GBP flows and cross-border EUR from the same account without transferring between institutions?

Safeguarding and regulatory status: Is the provider FCA-authorised? Is safeguarding documented clearly and independently verifiable?

Verification of Payee: Has the provider implemented VoP? What name will appear on the payee lookup when your counterparty initiates a SEPA transfer?

Fees and FX: Per-transaction fees for inbound EUR, outbound EUR, and GBP/EUR conversion. Is the FX rate marked up above mid-market?

Reporting and export capability: Statement export in CSV or PDF, accounting system integration, payment history access.

User access and approval controls: Team permissions, outbound payment approval workflows, multi-user access.

Jurisdiction fit: Does the provider onboard businesses in your registered jurisdiction? What is the typical support response time for operational queries?

For multi-currency businesses handling GBP, EUR, and USD simultaneously, the EQWIRE guide on e-commerce operating accounts covers how these requirements interact across currency rails.

Common Mistakes When Choosing a Named IBAN Setup

Assuming every IBAN product is named — many "business account with IBAN" products are pooled or reference-based. Confirm attribution model explicitly.

Treating virtual as automatically equivalent to named — vIBANs can deliver a named experience, but the EBA flags transparency and AML risks that a named direct account does not carry. Ask how the provider addresses them.

Ignoring the EMI-versus-bank protection difference — safeguarding and FSCS protection up to £120,000 are not equivalent. Understand which applies before deciding where to hold operational balances.

Applying without a clear EUR business rationale — vague applications create delays and rejections.

Not checking Verification of Payee before go-live — a name mismatch between your account registration and your invoices can cause SEPA payment failures on the sender's side.

Using a personal account for business trading flows — creates bookkeeping problems, policy breach risk, and weak audit trails.

Failing to test the full payment workflow after account opening — a successful onboarding does not confirm that inbound and outbound EUR flows work as expected.

💡 Need a named EUR IBAN or just better EUR collections? Find out whether your business actually needs a named structure, what documents are required for onboarding, and whether a UK bank or EMI route is the better fit for your operations and protection requirements. Check your eligibility and account structure options → | Review EQWIRE's regulatory status and safeguarding arrangements →

Conclusion: When a Named IBAN Account Makes Sense for a UK Business

A named IBAN account makes sense for a UK business when cleaner attribution, reliable SEPA access, and audit-ready EUR records are operationally necessary — not just aspirationally useful.

If your business regularly receives EUR from multiple European counterparties, operates on a recurring billing cycle, needs finance-team-ready reconciliation, or wants European clients and suppliers to pay into account infrastructure clearly registered to your business, a named EUR IBAN with SEPA access is the appropriate structure.

Pooled or lighter-weight setups can still work for simple, low-volume, single-sender scenarios — but they introduce attribution risk at scale and create compliance friction as EUR activity grows. Virtual IBAN arrangements can deliver a named experience efficiently, but require due diligence on how the provider handles transparency, safeguarding, and Verification of Payee — areas the EBA has specifically flagged as risk points in the current market.

Provider fit matters more than product label. Whether a setup delivers reliable attribution, the payment rails your business requires, name consistency for Verification of Payee, and the reporting tools your finance team needs is determined by the institution's actual infrastructure — not by how the product is marketed.

For businesses evaluating offshore or multi-jurisdiction EUR account structures, the EQWIRE guide on EUR IBAN access for Seychelles companies covers how the same structural evaluation logic applies in a different operating context.

FAQ

What is a named IBAN business account and how does it work in the UK?

A named IBAN business account is an IBAN allocated exclusively to one business, rather than shared with other clients through a pooled collection structure. It allows a UK business to receive EUR payments into account infrastructure registered to that business, hold EUR balances, and send outbound EUR via SEPA or SWIFT. "Named" refers to exclusive allocation — not to any name encoded inside the IBAN string itself, which follows a fixed technical format.

How do I get a named EUR IBAN for business in the UK?

The process involves five steps: define your exact EUR use case; decide whether a UK bank or FCA-authorised EMI route is more suitable for your business type and protection requirements; prepare a complete compliance file including company documents, UBO identification, and a written EUR business rationale; confirm that the account supports your required rails, VoP implementation, and reporting features; and test the full inbound and outbound workflow before migrating live commercial payment flows.

Is the UK still in SEPA for EUR transfers?

Yes. The EPC's current SEPA country list confirms the UK remains a non-EEA SEPA country, meaning UK PSPs can participate in SEPA schemes. However, actual provider participation and product support vary by institution — confirming SEPA reachability at provider level remains a necessary step before applying.

Is a named IBAN the same as a pooled IBAN?

No. A named or dedicated IBAN is assigned exclusively to one business, so incoming payments are attributed automatically without reference dependency. A pooled IBAN is shared across multiple clients, and attribution depends on the sender including a correct payment reference — which fails regularly in practice, creating reconciliation workload and potential reporting errors.

Can a UK EMI offer a named IBAN account with SEPA access?

Yes in principle, but the protection model differs materially from a bank. At a UK-authorised bank, eligible deposits are now protected up to £120,000 per person per firm by the FSCS. At a UK EMI, client funds are safeguarded under FCA rules rather than FSCS-covered — meaning you should receive most of your money back if the EMI fails, but return may be delayed and reduced by administration costs. Stronger FCA safeguarding rules also take effect on 7 May 2026. Specific product capability — which rails are supported, whether VoP is implemented — still varies by provider.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)