•

•

How to Pay 3PL Suppliers Directly from Stripe GBP Settlements

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

Key Takeaways

Stripe settling in GBP does not mean your 3PL invoices are in GBP — settlement currency and supplier payout currency are different decisions.

Holding GBP after settlement and converting only when a EUR invoice is due tends to reduce repeated FX conversion costs compared to converting on every automatic payout cycle.

Stripe Global Payouts and Connect handle specific payout scenarios well, but are optimised for platform-disbursement models, not invoice-matched supplier payments across multiple 3PLs.

A UK multi-currency account adds the most value when you have recurring mixed-currency invoices, multiple fulfilment partners, or a need to control when GBP converts into EUR.

Reconciliation matters as much as FX savings — unmatched Stripe batch references and 3PL invoice numbers create accounting problems that compound across reporting periods.

The right routing model depends on your supplier currency mix, invoice cadence, and how many fulfilment partners you manage in the UK and Europe.

Introduction

Customer revenue lands in Stripe. Stripe settles in GBP. Then the warehouse invoice arrives — in GBP, EUR, or both, depending on where your fulfilment partners operate. The gap between receiving settled funds and actually paying your 3PL suppliers is where most of the operational friction lives.

For UK e-commerce brands using Stripe as their primary processor, this workflow is a real cost centre. If Stripe payouts are automatically converted and forwarded without deliberate routing, you are likely losing margin on repeated FX conversions, missing invoice timing windows, and making reconciliation harder than it needs to be.

This article covers what happens after Stripe settles: how to move GBP efficiently, when to convert into EUR, and how to route outbound supplier payments to UK and European 3PL partners without unnecessary leakage or operational risk.

Quick answer: You can pay 3PL suppliers from Stripe GBP settlements, but the supplier payment is a separate event that happens after Stripe pays out to your nominated account. UK 3PLs can then be paid in GBP via domestic rails. EU fulfilment partners typically require a EUR balance, created either within a supported Stripe payout flow or after conversion in a multi-currency account.

What Does It Mean to Pay 3PL Suppliers from Stripe GBP Settlements?

Paying 3PL suppliers from Stripe GBP settlements means routing settled customer funds — after Stripe's payout cycle — into outbound payments to warehouse, fulfilment, and logistics partners. Three distinct stages are involved: collecting customer funds in Stripe, settling those funds into a GBP-capable account, and then paying suppliers in the correct currency at the right time.

The confusion in practice usually comes from conflating three different concepts:

Stripe balance — funds held inside Stripe from customer transactions, before payout

Stripe payout — the transfer of settled funds from your Stripe balance to an external bank account (Stripe docs: multi-currency settlement)

Supplier payment — the separate outbound transaction from your operating account to a 3PL partner

These are not the same event. Understanding this distinction determines whether you use Stripe-native payout tools for both steps, or route settled GBP into a dedicated multi-currency account before making supplier payments.

UK example: A DTC apparel brand collects customer payments through Stripe. Stripe settles GBP daily into the brand's UK account. The brand initiates a weekly bank transfer to its UK warehouse in GBP, covering storage and pick-pack charges.

European example: The same brand also uses a Dutch fulfilment centre for its EU customer base. That warehouse invoices in EUR monthly. The GBP arriving from Stripe needs to be converted before payment — but when, and through which account, affects the total cost.

Can You Pay 3PL Suppliers Directly from Stripe?

Yes, but with important caveats about how "directly" works in practice. Stripe offers Global Payouts for paying third parties in local currencies, and Stripe Connect for cross-border payouts to connected accounts. Whether either tool fits your 3PL payment workflow depends on your supplier structure and Stripe account configuration.

For most UK e-commerce operators, paying a 3PL is not a "Stripe payment" in the strict sense. It is a separate treasury workflow that starts after Stripe settles funds to your nominated account. Payout timing, currency conversion, and supplier payment rails each affect cost, reconciliation, and control differently.

Step 1. Map the Actual 3PL Payment Workflow Before Changing the Payout Setup

Before adjusting any Stripe settings or opening new accounts, document exactly who gets paid, in what currency, on what schedule, and against which invoice logic. Finance teams that skip this step often build a new workflow around the wrong assumptions.

Common 3PL charges to map:

Storage fees (monthly, per pallet or SKU)

Pick-and-pack fees (per order, weekly or monthly billing)

Shipping label charges (per dispatch, often weekly)

Return handling and restocking fees

Customs administration or duty advances

Monthly retainers for dedicated fulfilment staff or systems

Each charge type may have a different billing currency, billing frequency, and payment deadline. Once mapped, you can answer a foundational question: what share of your total supplier obligations is in GBP, what share is in EUR, and does your current Stripe settlement routing match those obligations?

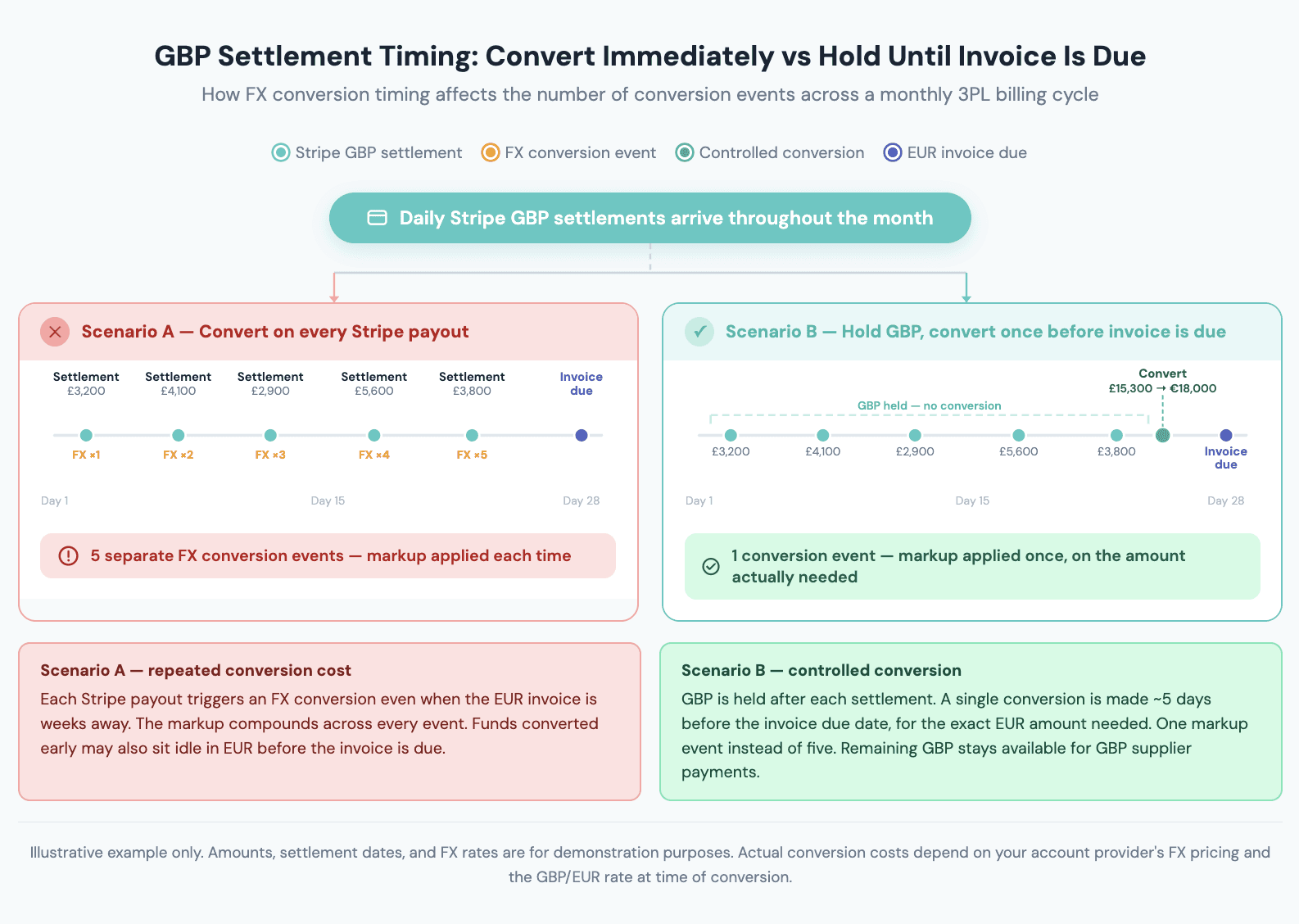

Step 2. Decide Whether GBP Should Be Held or Converted Immediately

Holding GBP after settlement and converting into EUR only when a supplier invoice is due tends to reduce unnecessary FX conversion costs compared to converting automatically on every Stripe payout. This is typically the highest-impact decision in the workflow.

Most businesses using automatic Stripe payouts into a standard UK current account convert GBP into EUR at the point each payout hits — even when the EUR invoice is not due for another three weeks. That creates repeated conversion events on funds that may not need to move into EUR for some time.

Scenario | Hold GBP | Convert Earlier |

|---|---|---|

UK warehouse billed weekly in GBP | ✓ | — |

EU 3PL billed monthly in EUR | ✓ Hold until ~5 days before due | — |

EU 3PL with short payment terms (<5 days) | — | ✓ Convert on receipt |

Volatile GBP/EUR rate, want certainty | — | ✓ Convert in advance |

Predictable EUR charges, strong GBP | ✓ | — |

Worked example:

A UK brand settles £45,000 from Stripe in a given week:

£12,000 is owed to a Nottingham warehouse (GBP) on Friday → no conversion needed

€18,000 equivalent (~£15,300 at an illustrative 1.18 rate) is owed to a Dutch 3PL at month-end → convert GBP to EUR mid-month, not on each daily payout

If the brand converts on every daily payout at a 0.6% FX markup instead, the cost on the EUR portion alone across a year adds up to several thousand pounds in avoidable conversion charges. The precise impact will depend on your volumes, timing, and the FX rates and fees your account provider applies.

💡 Does your current setup give you control over when GBP converts into EUR? If Stripe payouts land in a single-currency account with automatic conversion, you may be losing margin on every payout cycle. EQWIRE is an FCA-authorised UK EMI offering GBP, EUR, and USD account capability with safeguarded funds for eligible businesses that need more control over settlement timing and supplier payments.

Safeguarded funds are held separately under the Electronic Money Regulations 2011 and are not FSCS-protected. Account eligibility is subject to EQWIRE's onboarding requirements.

See whether your current Stripe payout setup is creating avoidable FX and reconciliation friction →

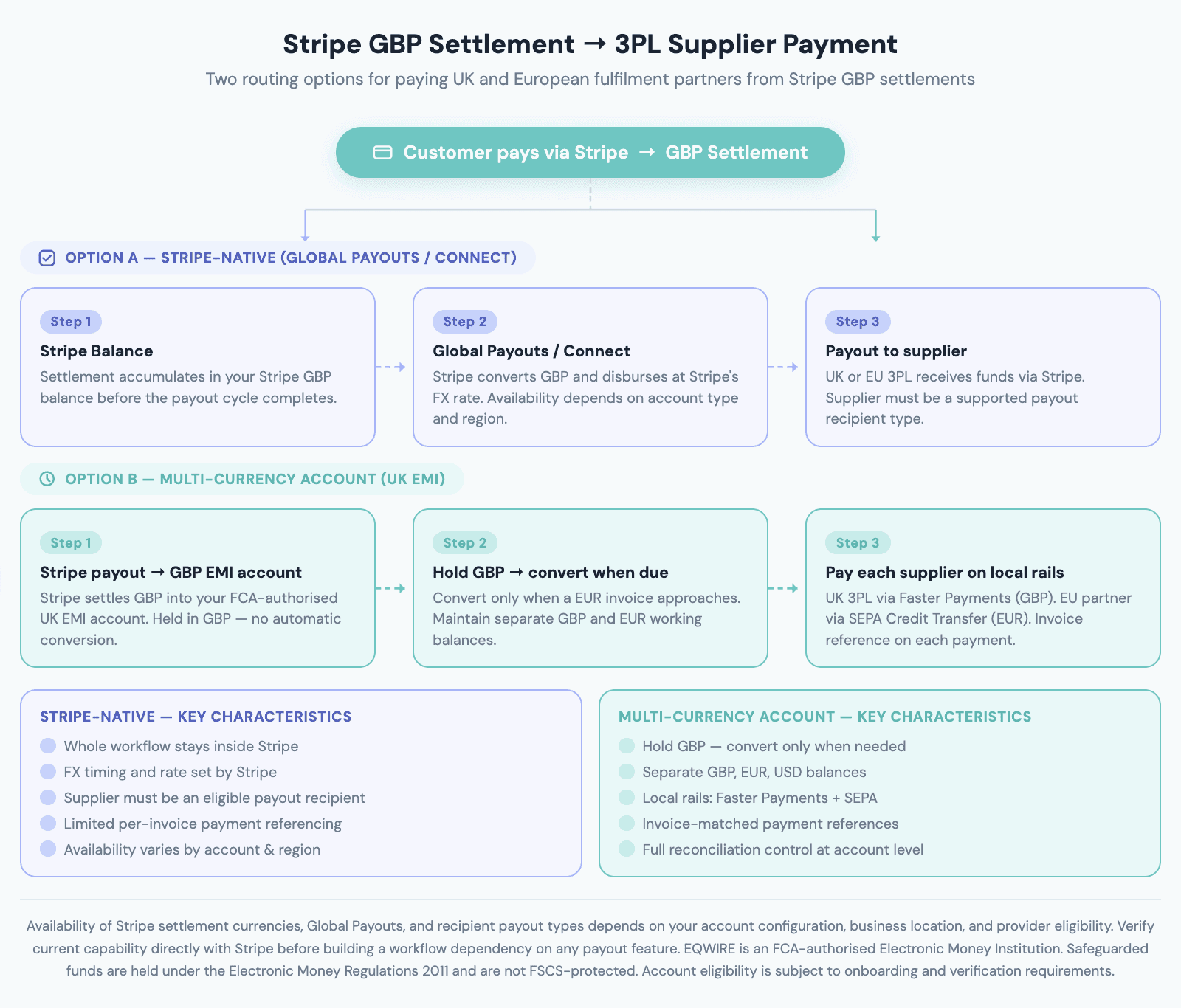

Stripe Global Payouts vs External Multi-Currency Account: Which Route Fits Your 3PL Workflow?

The right routing model depends on whether your supplier payments need to happen inside Stripe's infrastructure, or whether you need more treasury control over balances, conversion timing, and local payment rails after settlement.

Stripe-Native Route (Global Payouts / Connect) | External Multi-Currency Account | |

|---|---|---|

Best for | Platform-to-recipient disbursements; supplier is a Stripe-connected entity | Recurring invoice-matched supplier payments; multi-currency 3PL base |

GBP control | Limited — payout triggers conversion at Stripe's rate | Hold GBP until conversion is needed |

EUR capability | Available where supported (Stripe docs) | Maintain a EUR balance separately; convert when due |

Payment rail | Stripe-managed | Faster Payments (GBP) / SEPA (EUR) — local rails |

Reconciliation | Inside Stripe dashboard | Separate account statements matched to invoices |

Invoice matching | Batch-level | Invoice-by-invoice payment references |

Suitable for multiple 3PLs | Depends on payout model fit | Yes — each supplier paid separately |

Setup complexity | Low if already using Stripe payouts | Requires additional account opening |

Option A: Stripe-Native Route

Stripe Global Payouts allows businesses to pay third parties in local currencies where supported. Stripe Connect supports cross-border payouts to connected accounts and service providers. These tools work well when the business wants payout workflows to stay inside Stripe and when the supplier or payment-recipient model matches Stripe's payout structure.

The practical limitation: Stripe's payout tools are built around platform disbursement models. Paying a UK warehouse or a German fulfilment partner on a weekly invoice cycle — with named beneficiary matching and payment references tied to specific invoice numbers — sits outside the primary design intent of these products. Availability of payout features also depends on your Stripe account configuration, region, and business type. Always verify current capability directly with Stripe before building a workflow dependency on it.

Option B: Stripe Settlement to External Multi-Currency Account

Many e-commerce finance teams receive Stripe payouts into a GBP-capable EMI (Electronic Money Institution) account, then manage warehouse and fulfilment payments from there. This provides:

Ability to hold GBP without converting immediately

Separate EUR and USD balance management

Local payment rails for UK suppliers (Faster Payments in GBP) and European suppliers (SEPA Credit Transfer in EUR)

Invoice-by-invoice payout timing rather than batch disbursement logic

A consolidated view of settlement receipts and outbound supplier payments

The trade-off is an additional account layer. For businesses with one or two UK-only GBP suppliers, this may not be necessary. For businesses with recurring GBP and EUR invoices across multiple 3PLs, the operational control typically justifies the added setup.

Step 3. Route UK 3PL Payments Locally in GBP

Paying UK warehouse partners in GBP on domestic rails is typically faster, cheaper, and easier to reconcile than routing the same payment through cross-border infrastructure.

Faster Payments in the UK generally processes within seconds to a few hours for eligible transactions between participating banks and payment service providers, though timing can vary depending on the sending and receiving institutions involved. There are no correspondent banking intermediaries, which means the amount sent is typically the amount received — removing the invoice shortfall risk that cross-border wires can introduce.

Practical controls for UK warehouse payments:

Use the supplier's exact legal entity name as the beneficiary

Reference the specific invoice number in the payment reference field

Confirm sort code and account number match the invoice header

Align payment timing to the warehouse's cut-off for that week's billing cycle

Example weekly cycle: Stripe settles GBP Monday through Thursday. The finance team batches those settlements and initiates GBP Faster Payments to the UK warehouse by Friday at noon, before the warehouse's end-of-week billing cut-off. The warehouse receives the full invoiced amount with a matching reference — no shortfall, no dispute.

Step 4. Pay European Fulfilment Partners in EUR from a GBP-Led Workflow

It is possible to pay European 3PL suppliers in EUR using funds that originated as Stripe GBP settlements. The practical workflow depends on where the GBP-to-EUR conversion happens and when.

UK 3PL (GBP) | EU 3PL (EUR) | |

|---|---|---|

Source funds | Stripe GBP settlement | Stripe GBP settlement |

Conversion needed? | No | Yes — GBP → EUR |

Where conversion happens | N/A | Inside Stripe (where supported) or in external multi-currency account |

Payment rail | Faster Payments | SEPA Credit Transfer |

Typical timing | Same day or hours | 1 business day (SEPA Credit Transfer) |

Invoice reference | Sort code / account + reference | IBAN + BIC + payment reference |

FX timing control | N/A | Low (Stripe-native) vs High (external account) |

For monthly EUR invoices: Convert a controlled amount of GBP into EUR three to five business days before the invoice due date. Keep conversion records matched to specific invoice IDs for month-end close.

For weekly EUR invoices: Build a small EUR working balance to cover known weekly charges, then replenish from GBP conversion each Monday based on that week's expected EUR outflows.

Note: the ability to hold a EUR balance and send SEPA payments depends on your account provider's capabilities and configuration. Verify SEPA sending capability before committing to this workflow with a European supplier.

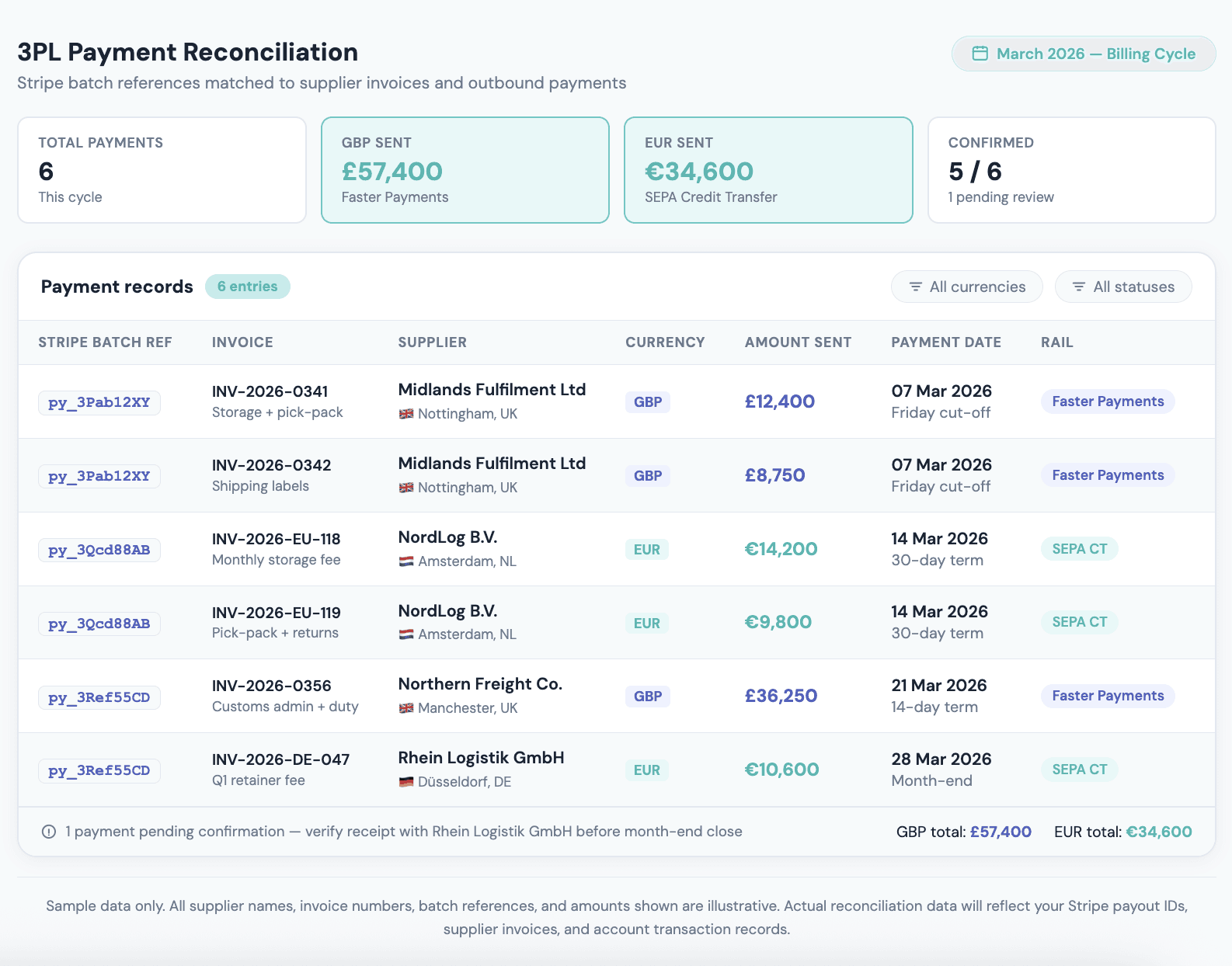

Step 5. Build Controls for Reconciliation, Invoice Matching, and Payout Timing

Reconciliation gaps between Stripe settlements, outbound supplier payments, and 3PL invoices are one of the most common — and underreported — operational costs in e-commerce finance. Most competing guides miss this section. The cost of poor reconciliation can outweigh any FX savings made earlier in the workflow.

For a multi-3PL operation, the minimum reconciliation layer should include:

Field | Source | Notes |

|---|---|---|

Stripe batch reference | Stripe payout ID | Ties each settlement batch to a received amount |

Supplier invoice number | 3PL invoice | The specific invoice being settled by this payment |

Beneficiary entity name | Supplier registration | Must match the account name exactly |

Currency and amount | Invoice | Confirmed — not estimated from batch totals |

Payment date and rail | Bank statement | Faster Payments, SEPA, or SWIFT |

Confirmation status | Receipt or account statement | Confirms funds received at supplier end |

A practical internal control: the person who initiates the supplier payment is not the same person who approves it. Even in small teams, a two-step review on outbound payments reduces the risk of duplicates, incorrect beneficiaries, or mis-referenced invoices.

Step 6. Compliance and Counterparty Checks Before Paying Warehouse Partners

Basic counterparty due diligence is standard treasury practice before adding a new 3PL supplier to your outbound payment workflow — not optional overhead. This applies equally to UK and European fulfilment partners.

Minimum checks to build into supplier onboarding:

Verify the supplier's full legal entity name and registered address against their invoice header

Confirm bank account details on a signed, dated instruction from the supplier — not via informal email

Check that the beneficiary country is not subject to relevant payment restrictions or sanctions

Retain invoice copies against each outbound payment for AML record-keeping

Flag any change in bank account details for manual approval before the next payment

On APP fraud risk: Payment fraud targeting supplier accounts — authorised push payment fraud — frequently involves a fraudulent account change notification that mimics legitimate supplier communication. A confirmation call to a known contact at the supplier when bank details change is a widely recommended safeguard. The Payment Systems Regulator's guidance on APP fraud provides useful context for businesses managing supplier payment controls.

If using a UK EMI account for outbound payments, review the account terms that apply to your specific arrangement before building payment workflows. See EQWIRE's UK client terms and conditions for the obligations applicable to EQWIRE account holders.

Common Mistakes When Paying 3PL Suppliers from Stripe-Originated Settlements

Treating Stripe settlement currency as supplier payout currency. GBP settling in Stripe does not mean your 3PL invoices are in GBP. Check every supplier's billing currency before configuring payouts.

Converting too early and too often. Automatic conversions on every daily Stripe payout create repeated FX costs even when EUR invoices are weeks away.

Paying UK warehouses through cross-border wires when local rails are available. GBP payments via Faster Payments to UK suppliers are typically faster, cheaper, and generate cleaner reconciliation data.

Ignoring invoice timing and warehouse cut-off dates. A payment arriving after a warehouse's weekly cut-off creates disputes and damages the supplier relationship.

Using one workflow for UK and EU suppliers without checking the currency logic. Domestic GBP payments and EUR cross-border payments require different rails, different accounts, and different timing.

Failing to match Stripe batches to specific 3PL invoices. Batch-level reconciliation without invoice references creates audit gaps and slows month-end close.

Assuming every supplier-payment use case belongs inside Stripe. Stripe's payout tools are optimised for platform-to-recipient disbursements, not invoice-matched multi-currency supplier operations.

When Does a UK Multi-Currency Account Become the Better Operating Model?

A UK multi-currency account adds the most value when your supplier workflow involves recurring mixed-currency invoices, multiple 3PL partners, or a clear need to control when GBP converts into EUR. The decision is operational — it is about control and simplicity, not just fee comparison.

Use this diagnostic to assess your current setup:

[ ] You have more than one active 3PL with different billing currencies

[ ] Some invoices are in GBP and others in EUR, requiring separate payment events

[ ] Stripe payouts currently land in a single-currency account with automatic conversion

[ ] You cannot see EUR and GBP working balances separately

[ ] Month-end reconciliation between Stripe settlements and supplier payments takes more than one day

[ ] You have experienced invoice shortfalls or timing disputes with warehouse partners in the past 12 months

[ ] You are planning to expand into a new European market and will add a EUR-denominated 3PL

If three or more of these apply, the case for a dedicated multi-currency account layer is worth evaluating properly.

EQWIRE is an FCA-authorised UK EMI offering GBP, EUR, and USD account capability with safeguarded funds for eligible businesses operating in this space. Account opening is subject to business verification and eligibility requirements. Review EQWIRE's UK terms for the full scope of what is and is not included.

For broader context on GBP account access for non-UK companies, see how to open a GBP account for a non-UK company and GBP Faster Payments for offshore companies.

💡 Paying suppliers in both GBP and EUR from Stripe settlements?

Before redesigning your payout workflow, review three things: your current Stripe settlement currency settings, your supplier invoice currency mix, and how much FX conversion is currently happening automatically each month.

If you are paying UK 3PLs in GBP and EU fulfilment partners in EUR — and your current setup does not let you hold GBP or manage EUR separately — it is worth comparing your existing arrangement against a safeguarded multi-currency account built for this workflow.

Check whether your Stripe-to-3PL payout setup is creating avoidable cost and reconciliation friction

EQWIRE offers GBP, EUR, and USD accounts with local payment rails and safeguarded funds for eligible UK-based and international businesses paying suppliers across currencies.

Conclusion

The goal of a well-structured Stripe-to-3PL payment workflow is not simply to "pay from Stripe." It is to build a settlement-to-supplier process that preserves margin, reduces FX timing risk, and keeps warehouse relationships operating predictably — whether your fulfilment partners are in the UK, Germany, the Netherlands, or elsewhere in Europe.

To pay 3PL suppliers from Stripe GBP settlements effectively, businesses need to be clear on three questions: when settled GBP should be held versus converted, which payment route fits their supplier base and invoice structure, and how outbound payments will be reconciled against Stripe batch data and 3PL invoices. Getting those three elements right separates a workflow that scales from one that compounds operational cost over time.

For adjacent reading on cross-border supplier payment structures, see how to pay UK suppliers from a UAE business account and the EQWIRE service overview.

FAQ

How do I pay a 3PL warehouse from Stripe GBP settlements in the UK?

The core sequence is: receive your Stripe GBP settlement into a GBP-capable account, decide whether to hold GBP or convert to EUR based on your supplier invoice currency, then initiate the outbound payment using the appropriate rail. For UK warehouse partners billed in GBP, Faster Payments is generally the most efficient route. For European fulfilment partners billed in EUR, you need a EUR balance — either within a supported Stripe payout flow or in an external multi-currency account — before initiating a SEPA transfer. Always include the supplier's invoice number in the payment reference.

Can I pay a European 3PL in EUR using my Stripe GBP payouts?

Yes, though the steps depend on where the GBP-to-EUR conversion happens. If you use Stripe Global Payouts for EUR-denominated recipients (where supported for your account and region), Stripe handles the conversion. If you route Stripe GBP into an external multi-currency account first, you control when and how much is converted before sending a SEPA payment. The latter approach gives more control over conversion timing, which matters when EUR invoices follow a predictable monthly schedule. Verify current Stripe payout availability for your account configuration before relying on either route.

Do I need Global Payouts or Connect to pay warehouse partners from my Stripe account?

Not necessarily. Stripe Global Payouts and Connect are designed for specific payout models — primarily platform-to-recipient disbursements and marketplace flows. If your warehouse payment workflow involves ad hoc supplier invoices, named beneficiaries, mixed GBP and EUR obligations, and invoice-matched payment references, those tools may not fit cleanly. Many businesses find it more practical to receive Stripe payouts into an external multi-currency account and manage supplier payments separately, using local payment rails for each currency.

What is the best setup for 3PL payments through a UK multi-currency account?

The best setup matches your recurring supplier currency needs, payout timing, and reconciliation requirements. In practice, this typically means an account that holds GBP, EUR, and USD separately; sends GBP payments via Faster Payments to UK suppliers; and sends EUR payments via SEPA to European fulfilment partners. The account should provide enough transactional detail — payment confirmations, balance statements, and reference data — to reconcile cleanly against Stripe settlement batches and 3PL invoices each month.

Can I pay a 3PL in local currency from a Stripe settlement account in the UK?

For UK-based 3PL partners, GBP payments from a GBP-settled Stripe payout are straightforward — no conversion needed. For EUR-based 3PL partners, you will usually need access to a EUR balance before sending payment. Depending on your Stripe configuration and the settlement options supported for your account, that may happen inside your existing payments setup or after converting GBP in a separate multi-currency account. The key is controlling when conversion occurs rather than allowing it to happen automatically on each payout cycle.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)