•

•

Digital KYC and KYB Onboarding for UK Business Accounts: What to Expect

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Opening a business payment account in the UK involves a mandatory verification process that many finance teams underestimate. Digital KYC — the online identity checks applied to directors and beneficial owners — is only one layer. The other, often more document-intensive layer is KYB: the verification of the business entity itself. FCA-authorised EMIs are legally required to conduct both before any account can be opened.

Understanding how these two processes work, what documents they require, and what can delay them is the difference between a one-week onboarding and several rounds of follow-up requests.

[aa key-takeaways]

Key Takeaways

Digital KYC checks the identity of directors and ultimate beneficial owners (UBOs) online — no branch visits required

KYB verifies the business entity itself: registration status, ownership structure, and UBO declaration

UK FCA-authorised EMIs apply a risk-based onboarding approach — higher-risk entities undergo Enhanced Due Diligence

A complete document pack submitted at first application typically brings verification time down to 1–5 business days

Common delays stem from incomplete UBO information, mismatched addresses, and complex multi-layer ownership structures

[aa btn]Open a Business Account[/aa]

[/aa]

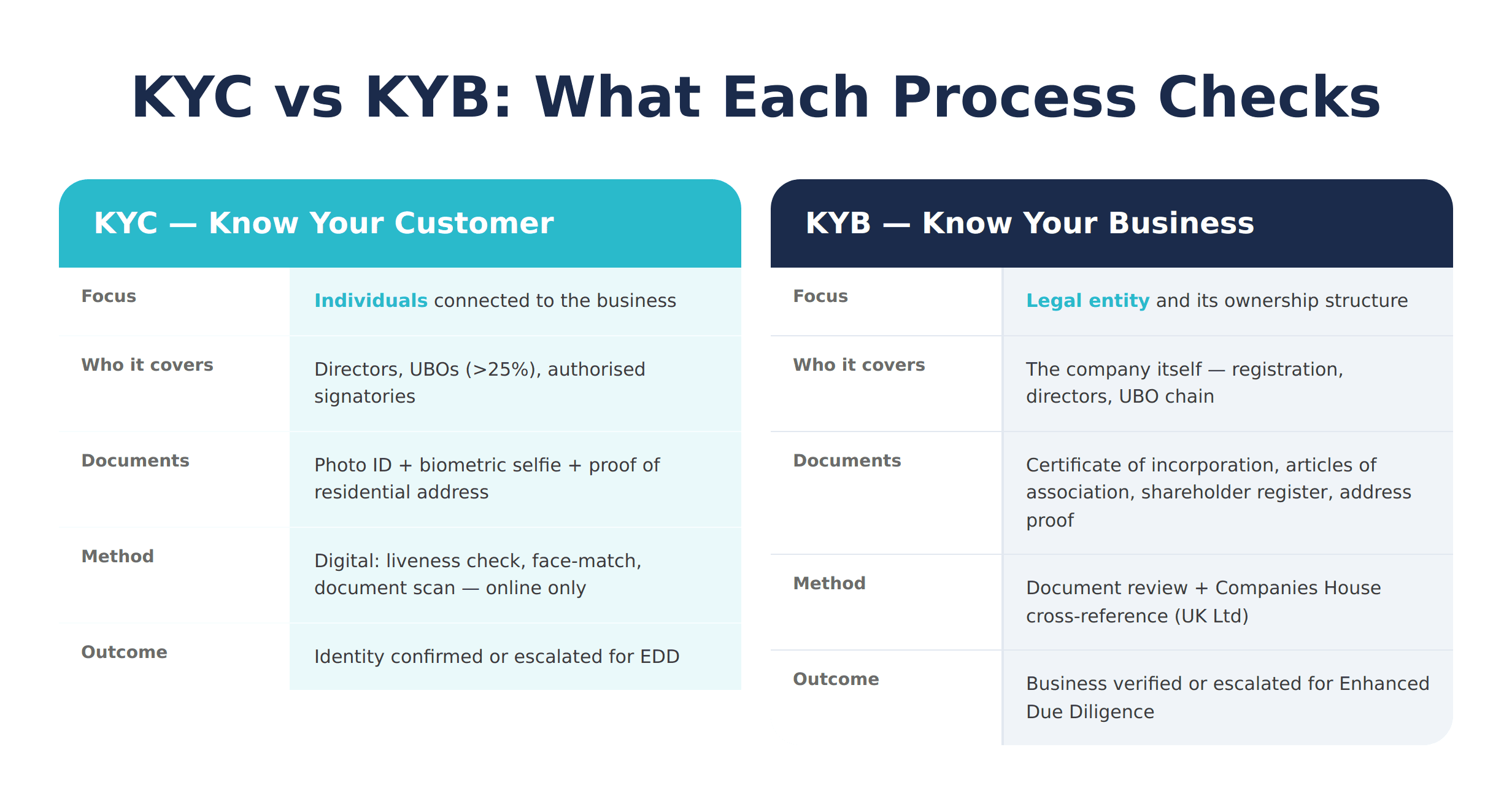

What Is Digital KYC — and How Does It Differ from KYB?

KYC asks: who are the people behind this business? KYB asks: what is this business, and is it legitimate? Both are legally required under the UK Money Laundering Regulations 2017 before any payment account can be opened.

KYC: Verifying the People Behind the Business

KYC — Know Your Customer — applies to the individuals connected to the account: company directors, ultimate beneficial owners (shareholders with more than 25% ownership), and any authorised signatories. Each person is verified digitally.

The process involves submitting a government-issued photo ID, followed by a biometric liveness check — a live selfie matched against the document photo. Proof of residential address (utility bill or bank statement dated within 90 days) is also required. This is what makes a digital KYC business account UK online application different from a traditional bank: the entire flow runs through a secure portal. No branch visit required.

KYB: Verifying the Business Itself

KYB — Know Your Business — shifts focus to the legal entity. The EMI checks that the company is properly registered, its ownership structure is transparent, and the declared UBOs are verifiable.

For UK-registered limited companies, EMIs cross-reference submitted documents against Companies House records automatically. For foreign-registered entities, equivalent company registry documentation from the country of incorporation is required.

The standard KYB document set includes: certificate of incorporation, articles of association, proof of registered business address, and a full shareholder register or UBO declaration for all individuals above 25%.

Why UK EMIs Must Conduct Both

EMIs operating under FCA authorisation carry the same AML obligations as banks. Under the Electronic Money Regulations 2011, FCA-authorised EMIs must apply customer due diligence equivalent to that required of banks. KYC and KYB are legal prerequisites — not optional steps.

As explained in what distinguishes an FCA-authorised EMI from a traditional bank, the compliance framework is comparable — the onboarding process is simply faster and fully digital.

[aa fast-fact]

Fast Fact: Under the UK Money Laundering Regulations 2017, EMIs must verify the identity of any individual owning or controlling more than 25% of a business — even if that individual is not a director or signatory on the account.

[/aa]

The Regulatory Framework: FCA, AML, and Risk-Based Onboarding

Understanding the legal basis for KYC/KYB checks clarifies why certain document requests appear and what happens when submitted information is incomplete.

FCA Authorisation and EMI Obligations

The FCA's guidance on financial crime and money laundering sets out the due diligence standards authorised firms must meet. For EMIs, this means maintaining documented onboarding policies, conducting customer due diligence at account opening, and applying ongoing monitoring throughout the account relationship.

FCA-authorised EMIs are subject to periodic inspections. Non-compliance — including inadequate KYC or KYB procedures — can result in fines or licence revocation. This regulatory exposure is why EMIs are thorough in their document requests.

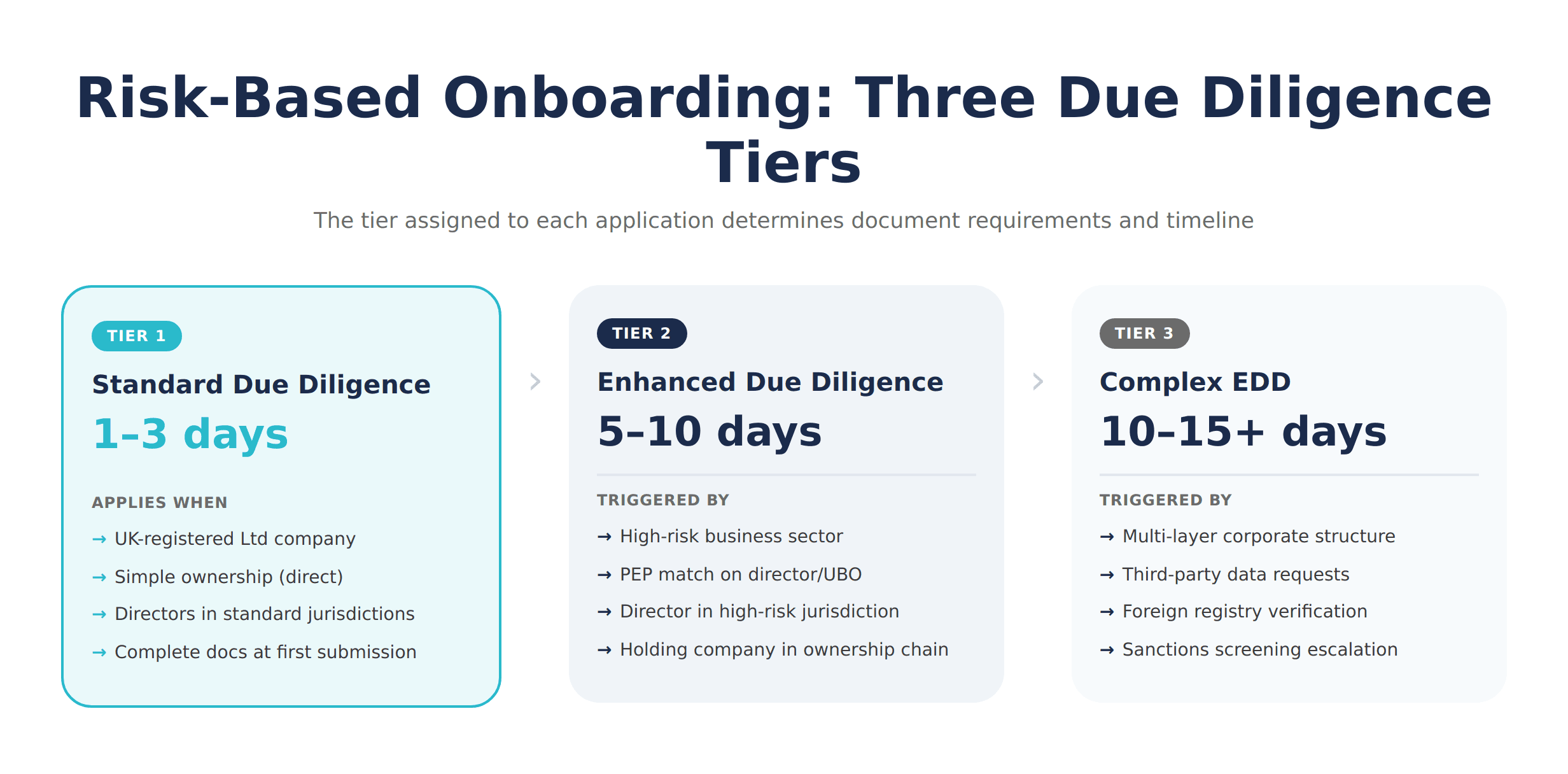

Risk-Based Approach Explained

The UK MLR 2017 mandates a risk-based onboarding approach: scrutiny is proportionate to the risk profile of each applicant, not uniform. For UK business EMI applicants, this means the risk-based onboarding UK business EMI framework sorts applications into tiers.

Risk factors that increase scrutiny:

Business type (crypto services, gambling, money services businesses rank higher risk)

Jurisdiction of directors or UBOs (certain countries trigger enhanced checks)

Ownership complexity (holding companies, trusts, multi-layer corporate groups)

Anticipated transaction volumes at account opening

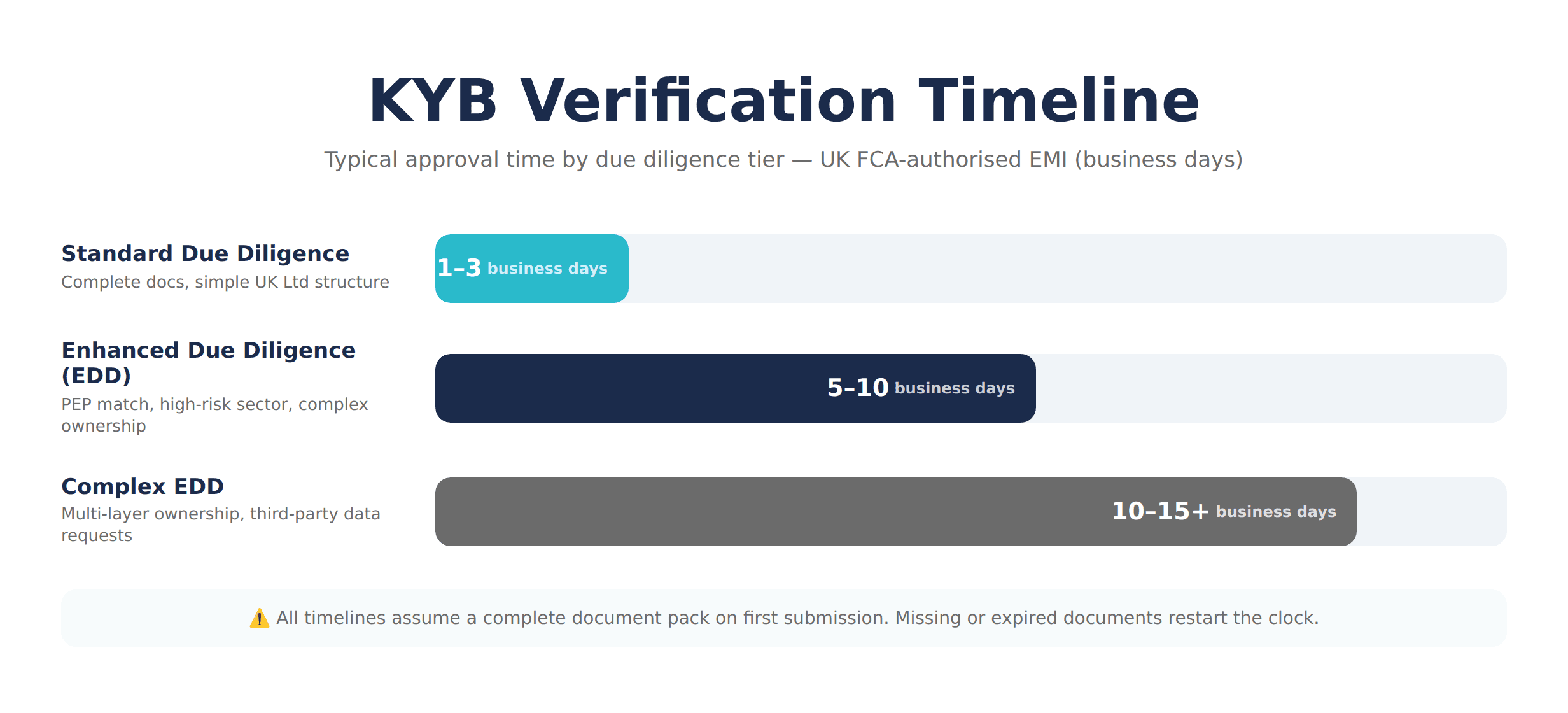

Businesses with low-risk profiles move through standard due diligence quickly. Higher-risk profiles are escalated to Enhanced Due Diligence (EDD).

How Risk Tier Affects Onboarding Timeline

How long KYB takes UK EMI account approval depends almost entirely on which due diligence track the application enters:

Due Diligence Track | Trigger | Typical Timeline |

|---|---|---|

Standard Due Diligence | Low/medium risk | 1–3 business days |

Enhanced Due Diligence | High-risk factor present | 5–10 business days |

Complex EDD | Multi-layer ownership, PEP match | 10–15+ business days |

These timelines assume a complete document pack on first submission. Missing or expired documents restart the clock.

Step-by-Step: How Digital KYC and KYB Work for UK Business Account Opening

How does digital KYC and KYB work for UK business account opening in practice? The process runs through three stages: identity verification, business verification, and risk assessment.

Step 1 — Identity Verification (KYC)

Every director and UBO above 25% completes the identity verification flow. The applicant submits a photo ID through the EMI's secure portal, followed by a biometric liveness check. Automated face-matching compares the biometric data against the document photo. Address verification follows.

Most individuals complete their KYC check in under 10 minutes.

Step 2 — Business Verification (KYB)

Business verification runs alongside KYC. The applicant uploads incorporation documents, articles of association, registered address proof, and the shareholder register. For UK-registered companies, the EMI cross-references key data against Companies House automatically — which speeds up the process.

The shareholder register must show all individuals above 25%. If shares are held through a holding company, the ownership chain must be traced to the ultimate beneficial owner at the natural-person level.

Step 3 — Risk Assessment and Decision

Once documents are received, the compliance team runs the combined data through automated screening — PEP checks and sanctions screening against OFAC, UN, EU, and UK HM Treasury lists. A risk score is assigned.

Possible outcomes: approved, approved with conditions, declined, or escalated for EDD. An EDD request is not a rejection. It is a request for additional information before a final decision.

What this means in practice: applicants who receive an EDD request should respond promptly with the documents requested. That is the fastest path to approval.

[aa fast-fact]

Fast Fact: PEP status does not automatically disqualify a business. It triggers Enhanced Due Diligence — a longer review process — not an automatic rejection.

[/aa]

What Documents Do You Need for KYB Onboarding?

Knowing what documents do I need for KYB onboarding UK EMI account — and having them ready before submission — is the single most effective way to reduce onboarding time.

Standard Document Requirements

Company documents:

Certificate of incorporation

Articles of association

Proof of registered business address (dated within 3 months)

Full shareholder register or UBO declaration (all individuals above 25%)

Director and UBO documents (per individual):

Valid government-issued photo ID (passport or national identity card)

Proof of residential address (utility bill or bank statement, dated within 90 days)

Once all checks are complete, businesses receive a named IBAN for their UK payment account, enabling GBP and multi-currency transactions.

Enhanced Due Diligence: When Extra Documents Are Required

EDD is triggered when the risk assessment flags specific conditions:

Source of funds declaration: A written explanation of the business's capital origin, with supporting evidence (audited accounts, investment agreements)

Audited financial statements: For companies with significant anticipated transaction volumes or those in higher-risk industries

Corporate structure diagram: A visual chart tracing ownership from the operating company to each ultimate beneficial owner

Beneficial ownership declarations per layer: Each intermediate holding entity may need to submit its own verification documents

What to expect during KYB business verification for a UK multi-currency EMI account: straightforward applications move from document submission to approval in 1–5 business days. Complex structures involving holding companies or overseas directors should budget 5–15 business days depending on the jurisdictions and complexity involved.

[aa cta]

Ready to Open a UK Business Account with Full Digital Onboarding?

EQWIRE is FCA-authorised — complete the full KYC and KYB verification process entirely online, with no branch visits or in-person appointments required.

[aa btn]Start Your Application[/aa]

[/aa]

How Long Does KYB Take for a UK Business Account?

How long does KYB take for UK business account EMI applications depends on two variables: the risk tier assigned and the completeness of the first submission.

For straightforward UK Ltd companies — single-layer ownership, all directors in standard jurisdictions, full document pack at first submission — verification typically takes 1 to 3 business days.

EDD extends the timeline to 5 to 10 business days. Complex structures requiring third-party data may take 10 to 15 or more business days.

"Business days" means UK working days, excluding weekends and bank holidays. An application submitted Friday afternoon begins processing Monday morning.

Common Reasons for KYB Delays — and How to Avoid Them

KYB onboarding UK business account fast completion is achievable — most delays are preventable. Here are the five most frequent causes.

Incomplete UBO Information

The shareholder register must account for 100% of the ownership structure. If it lists a corporate shareholder without identifying the individuals behind it, the compliance team cannot complete the UBO check. Trace the ownership chain to natural persons and include a declaration for every individual above 25%.

Mismatched Company Addresses

The registered address on the certificate of incorporation, articles of association, and proof-of-address document must match exactly. A minor discrepancy — even a postcode format difference — flags an inconsistency requiring manual review.

Expired Identity Documents

Passports and national ID cards must be valid at the time of application. An expired document fails the automated check immediately. Check expiry dates for all directors and UBOs before starting.

Directors or UBOs in Higher-Risk Jurisdictions

If a director or UBO holds a passport from a jurisdiction on the FATF grey list, EDD is triggered automatically. Prepare source-of-funds documentation in advance rather than waiting to be asked.

Missing Corporate Structure Chart

For businesses with shares held through a holding company or trust, a visual ownership diagram accelerates compliance review significantly. Without it, the compliance team reconstructs the structure manually — which adds days.

Businesses using their account for international cross-border payments should also ensure their stated business purpose and anticipated transaction volumes are consistent across all submitted documents.

Digital KYC and KYB: The Foundation for a Fast Account Opening

The digital KYC process is not a bureaucratic obstacle — it is a legally mandated compliance requirement that every FCA-authorised EMI must complete before any funds move. KYB is equally mandatory. Both exist because UK AML law — specifically the Money Laundering Regulations 2017 — requires payment institutions to know precisely who they are dealing with.

For finance managers and CFOs preparing an application: prepare a complete, consistent document pack before starting. Identify every director and UBO above 25%, check document expiry dates, and map the ownership chain. A thorough first submission almost always results in a faster approval than a partial one.

Verify any EMI's authorisation status on the FCA's public register before submitting an application. The FCA's electronic money institution supervision page sets out the obligations that apply to all FCA-authorised EMIs operating in the UK.

FAQ

How does digital KYC and KYB work for UK business account opening?

When opening a business account at a UK FCA-authorised EMI, the provider runs two parallel verification processes. KYC verifies the identity of each director and UBO using government-issued ID and biometric selfie matching. KYB verifies the legal entity using company registration documents, shareholder registers, and ownership structure data. Both processes are completed entirely online. For standard applications with a complete document pack, approval typically takes 1 to 5 business days.

What documents do I need for KYB onboarding UK EMI account?

For company verification: certificate of incorporation, articles of association, proof of registered address, and a full shareholder register or UBO declaration. For each director and UBO above 25%: a valid government-issued photo ID and proof of residential address dated within 90 days. Complex ownership structures may additionally require a corporate structure diagram, source-of-funds declaration, or audited financial statements.

How long does KYB take for UK business account EMI applications?

For straightforward UK-registered companies with a complete document pack, KYB verification at an FCA EMI typically takes 1 to 3 business days. If Enhanced Due Diligence is triggered — due to a complex ownership structure, a PEP match, or a high-risk industry — the process may take 5 to 10 business days or longer. All timelines refer to UK business days, excluding weekends and bank holidays.

How risk-based onboarding works UK EMI business account applications?

FCA-authorised EMIs apply a risk-based approach to onboarding as required by UK AML regulations. Each application receives a risk tier based on business type, director and UBO jurisdictions, ownership complexity, and anticipated transaction volumes. Lower-risk applicants proceed through standard due diligence. Higher-risk profiles trigger Enhanced Due Diligence, with additional document requirements and a longer manual compliance review.

What is the difference between KYC and KYB for UK business account applications?

KYC (Know Your Customer) refers to identity verification of individuals connected to the business — primarily directors and UBOs above 25%. KYB (Know Your Business) refers to verification of the company itself: legal registration, ownership structure, and trading legitimacy. Both are required simultaneously when opening a UK business account at an FCA-authorised EMI. One cannot substitute for the other.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)