•

•

SME International Banking: A Guide to Cross-Border Business Payments

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

Your invoice says £8,500. Your German supplier's bank statement shows €9,150 — after an unexpected SWIFT correspondent fee and a 2.1% FX margin your UK bank applied without warning. The supplier emails asking why the amount is short. You spend 40 minutes tracing the payment through two intermediary banks.

That's not an edge case. SME international banking is routinely more expensive, slower, and more opaque than it should be — because the infrastructure was built for large corporates, not businesses moving £20,000 to a supplier in Warsaw or paying a SaaS contractor in Dublin.

This guide covers how cross-border business payments actually work, where costs are hidden, and what account structure genuinely reduces friction for UK SMEs managing recurring international payment cycles.

[aa key-takeaways]

Key Takeaways

International transfers can cost UK SMEs 5–10x more than domestic payments once SWIFT correspondent fees and FX margins are factored in.

SEPA Credit Transfers settle in T+1 for EUR payments within the SEPA zone — bypassing SWIFT entirely for EU suppliers.

A multi-currency account holding GBP, EUR, and USD eliminates forced conversion on the majority of common payment corridors.

FCA-regulated EMIs offer UK payment rail access (Faster Payments, SEPA) without requiring a traditional banking relationship.

Correspondent banking adds 1–3 intermediary banks to each SWIFT transfer — each charging £10–£30 per pass.

Payment Services Regulations 2017 require all UK payment providers to disclose fees before a transaction is executed.

[aa btn]Create Account[/aa]

[/aa]

What Is SME International Banking — and Why Is It Different?

SME international banking covers the account infrastructure, payment rails, and compliance frameworks that enable businesses to send and receive money across borders.

It sounds straightforward. In practice, it's operationally more complex than personal transfers for three reasons.

First, the amounts are larger. A B2B international payment is typically in the thousands, not hundreds — which means correspondent bank fees (charged as flat amounts, not percentages) hit proportionally harder on lower-value transactions.

Second, the frequency is higher. An SME paying five EU suppliers every two weeks generates 130 individual cross-border payments per year. Each one is a fee event, an FX conversion decision, and a compliance check.

Third, the business risk is real. If a supplier payment is delayed or short-settled, it affects the commercial relationship — not just a personal inconvenience.

[aa fast-fact]

Fast Fact: Banks processed 92% of total B2B cross-border payment flows — but their share dropped to 76% for SME transactions specifically, as specialised providers captured share with lower-cost alternatives. (Edgar, Dunn & Company)

[/aa]

How Cross-Border Business Payments Actually Work

To understand where costs are buried, you need to understand the infrastructure.

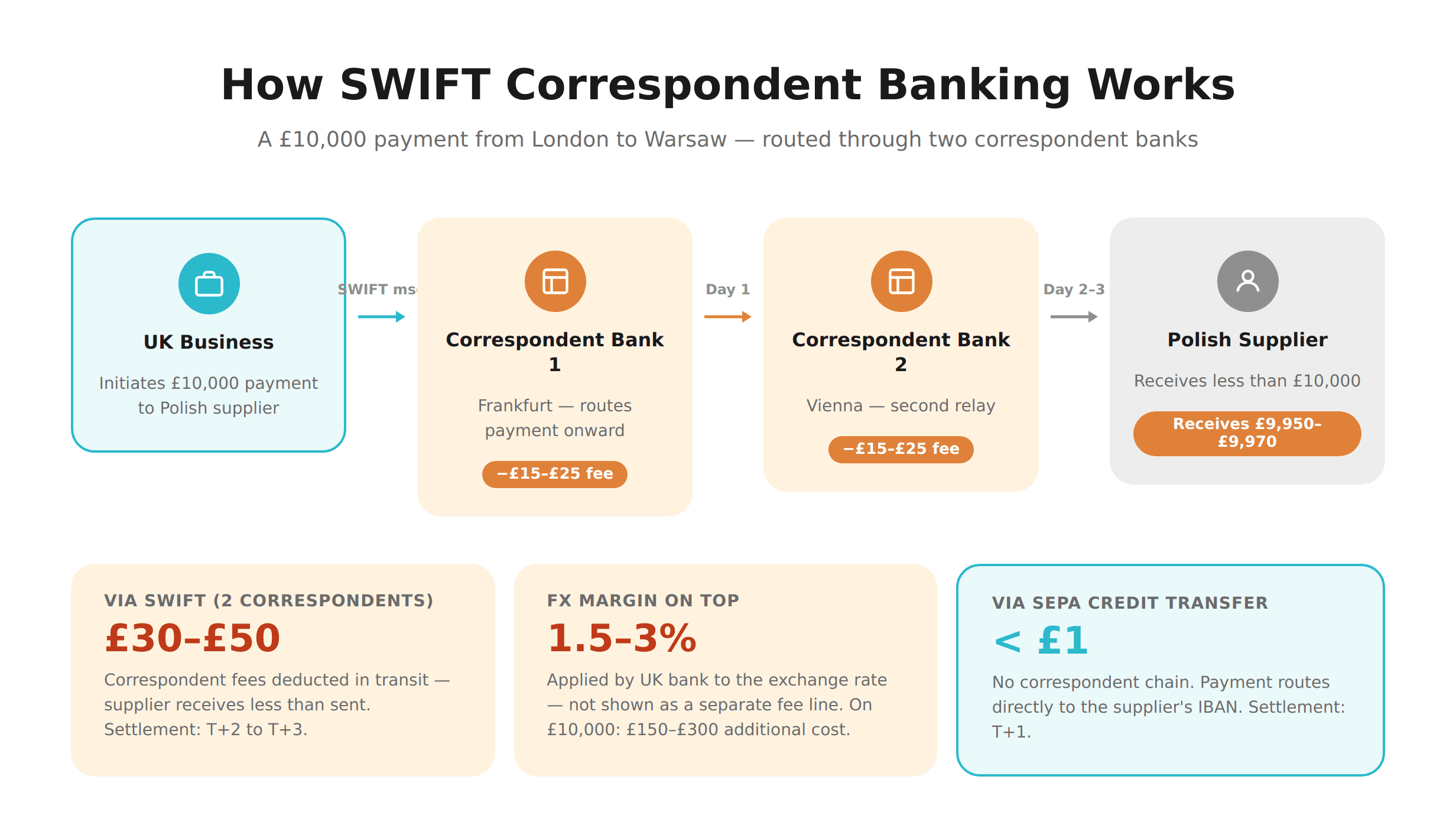

The SWIFT Correspondent Banking Model

SWIFT is a secure financial messaging network — not a payment scheme itself. When your UK bank sends a payment to a supplier in Poland, it issues a SWIFT message instructing a series of correspondent banks to move the funds.

If your bank has no direct relationship with the recipient bank, the payment routes through one or more intermediary correspondent banks. Each intermediary charges a fee — typically £10–£30 per pass — and the fees are deducted from the payment amount in transit. Your supplier receives less than you sent.

This correspondent chain adds T+2 to T+3 settlement time for most SWIFT payments. The funds are "in flight" and unusable during that window, creating cashflow planning problems for finance teams.

SEPA: The Lower-Cost Alternative for EUR Payments

For payments within the SEPA zone — 36 countries including all EU member states plus Norway, Switzerland, Liechtenstein, Iceland, and the UK — a different rail exists.

SEPA Credit Transfer (SCT) settles in T+1. The payment routes directly, without correspondent intermediaries, using the recipient's IBAN as the primary identifier. Fees are flat and low — typically under £1 per transaction on specialist platforms.

For a UK SME paying EU suppliers in EUR, SEPA Credit Transfer is structurally cheaper than SWIFT. The catch: you need a EUR account with SEPA access, which traditional UK banks provide inconsistently for SME accounts.

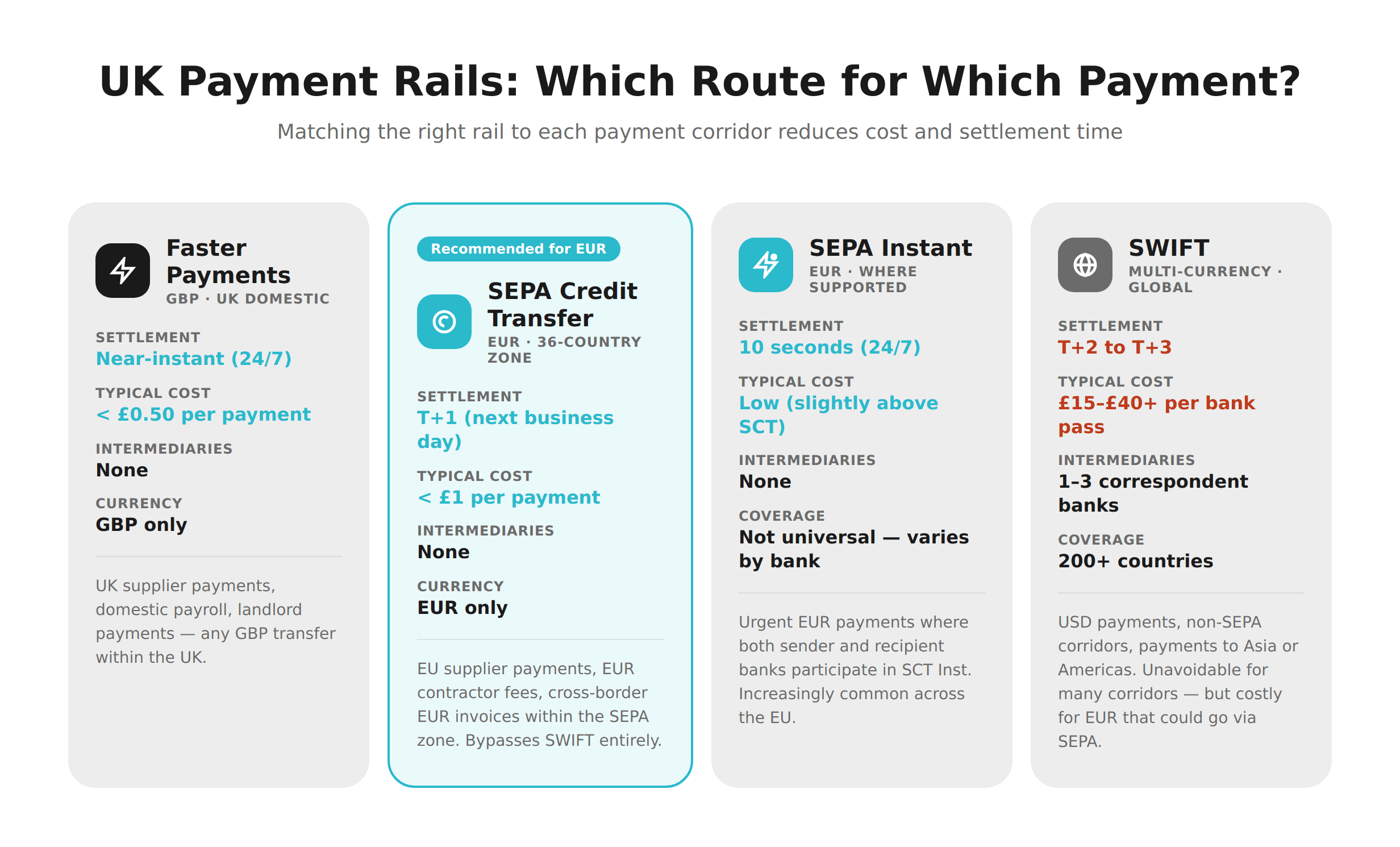

Payment Method | Settlement | Typical Cost | Intermediaries | Best for |

|---|---|---|---|---|

SEPA Credit Transfer | T+1 | < £1 | None | EUR within SEPA zone |

SWIFT | T+2–3 | £15–£40 + FX | 1–3 banks | Non-SEPA corridors, USD |

Faster Payments | Near-instant | < £0.50 | None | Domestic GBP |

BACS | T+3 | Low | None | UK payroll, direct credits |

The FX Margin Problem

SWIFT fees are visible. FX margins often aren't — until after the payment settles.

Traditional UK banks apply an FX margin of 1.5–3% over the mid-market rate on international transfers. On a £50,000 supplier payment, that's £750–£1,500 added to the cost of the transaction — not shown as a line item, simply embedded in the exchange rate applied.

Under the Payment Services Regulations 2017, UK payment providers must disclose exchange rates and fees before a transaction is executed. But disclosure requirements don't cap the margin — they require it to be visible.

[aa fast-fact]

Fast Fact: International transfers can cost up to 10x more than domestic transfers and take up to five days when routed through multiple correspondent banks, according to The Payments Association.

[/aa]

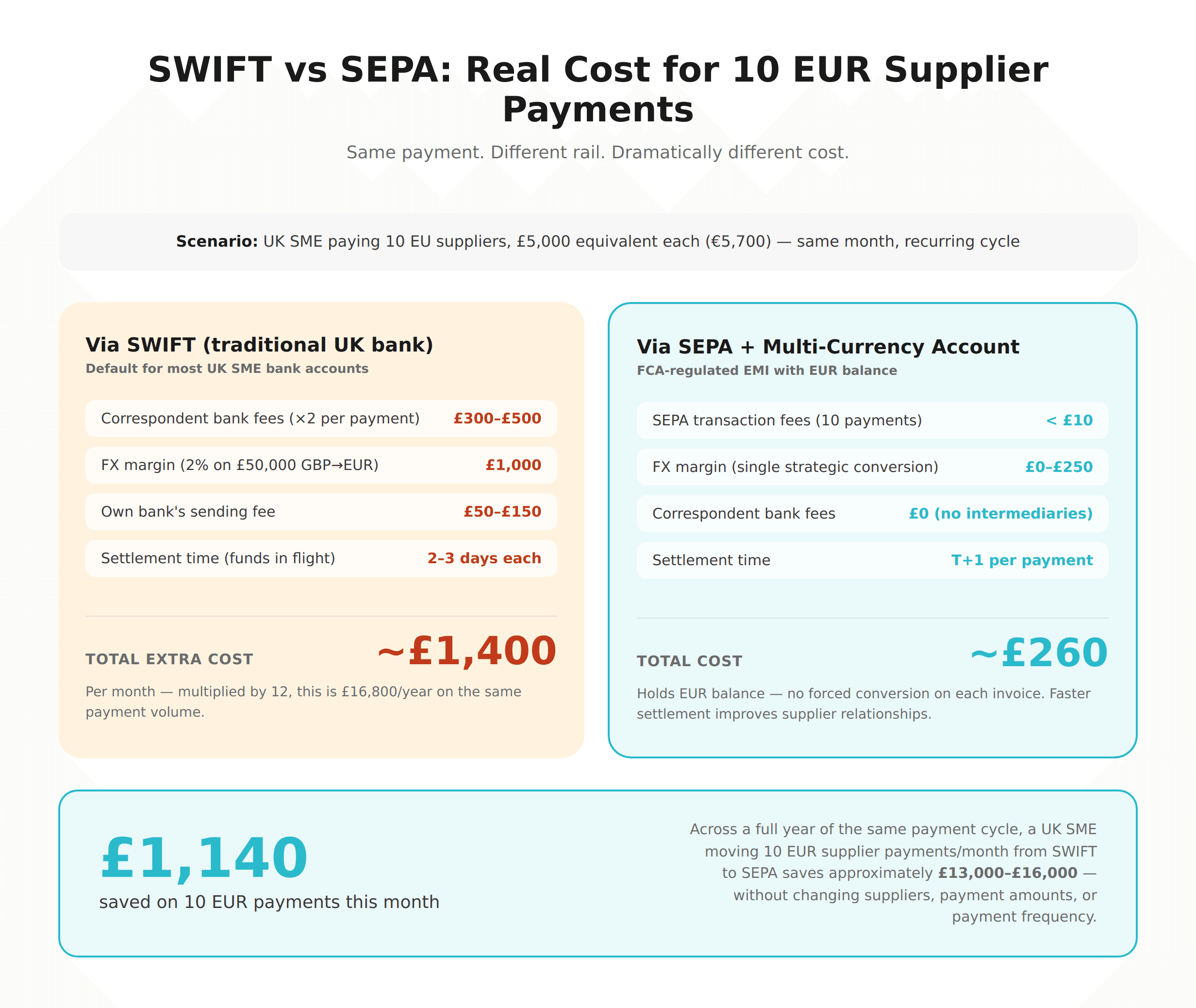

The Account Structure That Reduces Cross-Border Costs

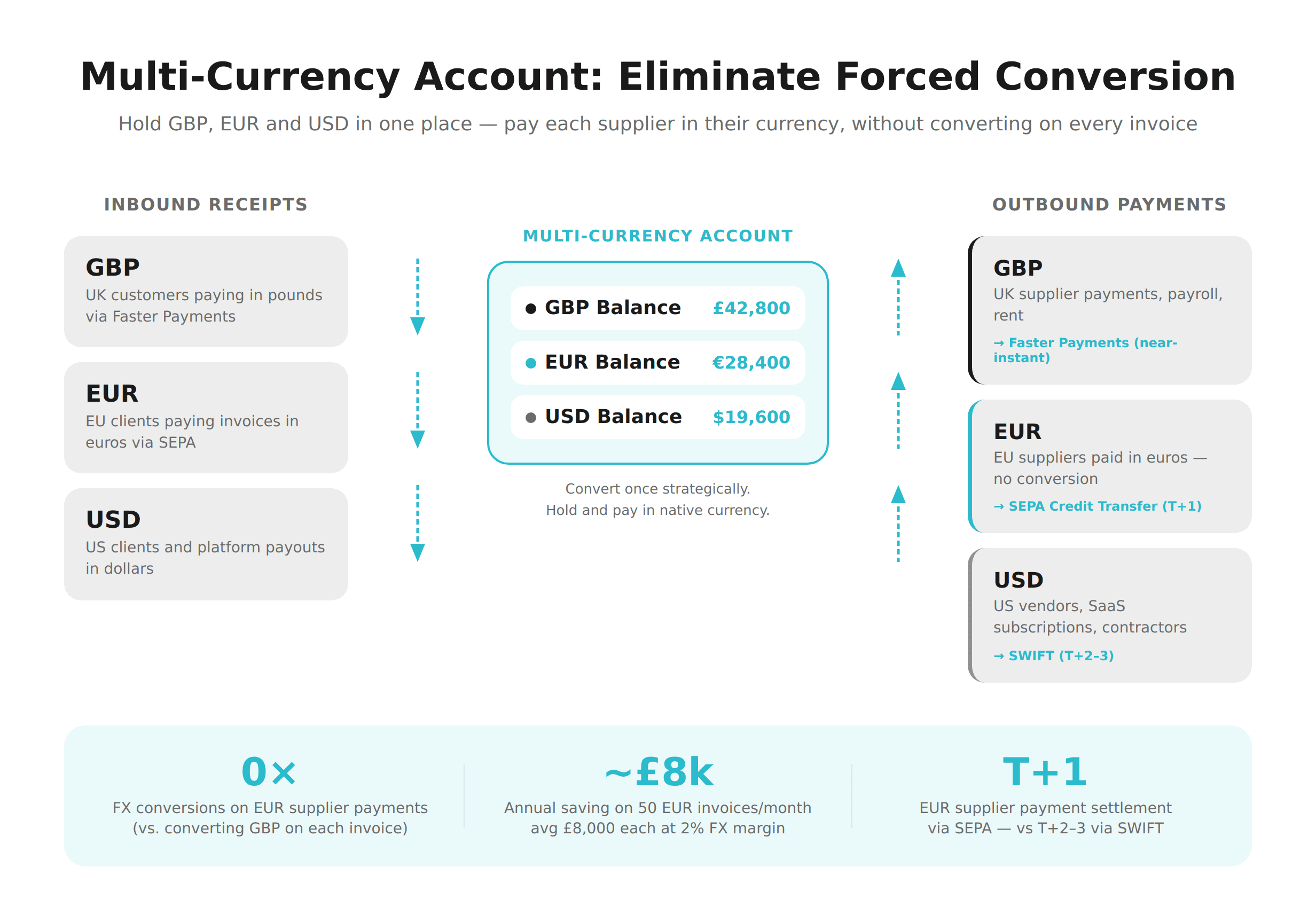

Most of the cost in SME international banking comes from avoidable conversion events. You convert GBP to EUR to pay a supplier, then your supplier converts EUR back to PLN to pay their own costs.

A multi-currency account holding GBP, EUR, and USD removes the first conversion event on the majority of common payment corridors.

How a Multi-Currency Account Works

Instead of holding one currency and converting on each payment, a multi-currency account holds separate balances in each currency. You convert once — when the rate is favourable — and then hold EUR to settle EUR invoices directly, with no per-transaction conversion.

For an import/export business paying suppliers in EUR and receiving in GBP: receive GBP from UK customers → hold EUR from a single strategic conversion → settle 10–15 EUR supplier invoices with no additional FX cost per payment.

A business settling 50 EUR invoices per month at an average of £8,000 each, saving 2% per transaction by eliminating repeat conversions, saves approximately £8,000 annually — before accounting for settlement speed gains.

EMI Accounts vs Traditional Business Bank Accounts

FCA-regulated Electronic Money Institutions (EMIs) provide payment infrastructure without operating under a full banking licence. For UK SMEs, the practical differences are:

EMIs typically offer multi-currency accounts with SEPA and Faster Payments access as standard

Traditional banks offer these features inconsistently, often behind enterprise pricing tiers

EMI accounts are not covered by the FSCS in the same way as bank deposits — funds are safeguarded under the Electronic Money Regulations 2011, held in segregated accounts separate from the EMI's own funds

For a detailed breakdown, see FCA-Authorised EMI vs Bank UK: Key Differences for Business Accounts.

[aa cta]

Ready to reduce your cross-border payment costs?

Open an EQWIRE multi-currency account and pay EU suppliers via SEPA Credit Transfer — settled in T+1, without SWIFT correspondent fees.

[aa btn]Create Account[/aa]

[/aa]

Key Payment Rails UK SMEs Need to Understand

Understanding which rail a payment moves through determines both cost and timing.

Faster Payments (GBP, Domestic)

Faster Payments is the UK's real-time domestic payment network — 24/7, near-instant settlement, low cost. For GBP-to-GBP transfers within the UK, it's the default. Its limitations are currency (GBP only) and geography (UK domestic).

SEPA Credit Transfer (EUR, SEPA Zone)

SEPA SCT is the standard rail for EUR payments within the 36-country SEPA zone. Settlement is T+1. The European Payments Council (EPC) governs the scheme. For UK businesses, SEPA access is available through SEPA-participant banks and EMIs — it was not affected by Brexit in terms of payment scheme participation.

SEPA Instant (SCT Inst) extends this to near-real-time settlement, available where both sender and recipient banks support the scheme.

SWIFT (International, Non-SEPA)

For payments outside the SEPA zone — USD to a US contractor, payments to Asia, or EUR payments where the recipient bank isn't SEPA-connected — SWIFT remains the dominant infrastructure. It's slower and more expensive than SEPA, but it reaches 200+ countries.

Compliance Requirements for UK SMEs Sending International Payments

Cross-border payments attract more regulatory scrutiny than domestic transfers. Finance teams need to understand three areas.

Anti-Money Laundering (AML) Checks

Every international payment is screened against sanctions lists maintained by HM Treasury and international bodies. Payments to flagged jurisdictions or entities can be delayed, returned, or reported. For SMEs, this means payments to higher-risk corridors may require additional documentation: invoices, supplier contracts, or source-of-funds confirmation.

Verification of Payee (VoP)

The UK's Confirmation of Payee (CoP) service checks whether the account name matches the sort code and account number on domestic transfers. This reduces misdirected payments and APP fraud risk. For international transfers, equivalent verification is less standardised — though the EU's Verification of Payee regulation (effective 2025) is extending account-name checking across SEPA.

Payment Services Regulations 2017

All UK-regulated payment providers — banks and EMIs — must comply with the Payment Services Regulations 2017 (implementing PSD2). This means: fee disclosure before execution, T+1 credit to the recipient's bank for SEPA payments, and access to redress mechanisms for disputed transactions.

[aa fast-fact]

Fast Fact: 40% of SMEs resort to domestic-only payment solutions due to the complexity and cost of cross-border alternatives — even when international options would be cheaper for their actual payment corridors. (Mastercard)

[/aa]

How to Structure International Payments to Reduce Costs

Operational decisions made before a payment is initiated determine the final cost.

Convert strategically, not reactively. Businesses that hold target-currency balances convert less frequently, at larger amounts, reducing total FX cost.

Use the correct rail for each corridor. EUR payments to EU suppliers should route via SEPA, not SWIFT. Using SWIFT for a Germany payment because it's the bank's default adds cost with no benefit.

Consolidate payments where possible. The per-transaction cost is fixed — fewer transactions reduce total fees.

Use named IBANs for inbound. A named IBAN business account linked to your account name reduces payment misdirection and simplifies reconciliation.

For supplier batch payment operations, see How to Run Weekly Supplier Batch Payments Without SWIFT and Bulk SEPA Payments from a UK EMI Account.

What to Look for When Choosing an International Banking Provider

Not all providers offer the same infrastructure. These are the features that matter operationally for UK SMEs.

Multi-currency accounts (GBP + EUR + USD minimum). Anything less forces repeated conversion on common payment corridors.

SEPA Credit Transfer access. If your payment provider only routes EUR payments via SWIFT, you're overpaying for every EU supplier payment.

Named IBANs. Shared-pool IBANs create reconciliation complexity. A named IBAN assigned directly to your business simplifies inbound payment matching.

Faster Payments connectivity. Real-time GBP settlement is the standard — not a premium feature.

FCA authorisation. Verify the firm reference number on the FCA register before opening an account.

Transparent fee structure. Your provider should disclose whether they deduct correspondent fees or pass them through — and what FX margin they apply.

FAQ

What is SME international banking?

SME international banking refers to the account infrastructure, payment rails, and compliance frameworks that enable small and medium-sized businesses to send and receive payments across borders. It typically includes multi-currency accounts, access to SEPA and SWIFT payment networks, FX conversion services, and compliance tools for AML screening. Unlike large-corporate banking, SME international banking is generally focused on lower-value, higher-frequency payments across a defined set of currency corridors — most commonly GBP, EUR, and USD.

How do cross-border business payments UK work for SMEs?

UK SMEs sending international payments typically use one of two routes: SEPA Credit Transfer for EUR payments within the SEPA zone (36 countries, T+1 settlement, low cost), or SWIFT for payments in other currencies or to non-SEPA destinations (T+2 to T+3, £15–£30+ per correspondent bank pass). Most traditional UK banks route EUR payments via SWIFT by default unless the account has dedicated SEPA access. FCA-regulated EMIs often provide SEPA access as standard with a multi-currency account.

What is the best international banking solution for UK SMEs paying global suppliers?

The best solution depends on which currencies and corridors your suppliers use. For UK SMEs primarily paying EUR suppliers, a multi-currency account with direct SEPA access eliminates correspondent bank fees and reduces FX costs. The key criteria are: named IBANs, Faster Payments connectivity, transparent FX pricing, and FCA authorisation. Specialist EMIs often offer this combination at lower cost than traditional business bank accounts.

How do SMEs manage cross-border payments UK without SWIFT fees?

The primary route is SEPA Credit Transfer for EUR payments within the SEPA zone — this bypasses SWIFT entirely and settles T+1 at near-zero transaction cost. For GBP domestic payments, Faster Payments provides real-time, low-cost settlement. Holding target-currency balances — converting GBP to EUR once rather than on each payment — eliminates the per-transaction FX margin on EUR invoices.

What is an international operating account for SME UK GBP EUR USD?

An international operating account for a UK SME is a multi-currency business account holding separate balances in GBP, EUR, and USD within a single platform. It allows the business to receive payments in each currency without forced conversion, hold balances for future payments, and send outbound payments via the appropriate rail for each currency: Faster Payments for GBP domestic, SEPA for EUR within the SEPA zone, and SWIFT for USD and non-SEPA corridors.

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)