•

•

FX Conversion for Business: How to Get Competitive Rates Without Hidden Markups

If your team processes regular supplier payments in EUR or USD, there's a reasonable chance you're overpaying on every FX conversion — often by several thousand pounds per year — with no breakdown on your bank statement to show it.

Most UK businesses accept the rate their bank quotes without benchmarking it against the mid-market rate. Traditional banks embed their margin directly inside the exchange rate, with no separate line for the cost. The result: the markup is invisible until you look for it.

This guide sets out a practical four-step process for identifying hidden FX markups, benchmarking your current conversion costs, and accessing transparent FX pricing on a UK business account.

[aa key-takeaways]

Key Takeaways

UK high-street banks typically add 2.5–3.5% above the interbank rate on currency conversions — a cost that does not appear as a fee on statements.

Benchmarking your rate takes less than five minutes using ECB reference data and can reveal thousands in annual overspend.

Spread-based FX pricing discloses the margin upfront as a fixed percentage above mid-market — making the cost calculable before you transact.

Holding GBP, EUR and USD in a multi-currency account eliminates conversion costs on same-currency transactions entirely.

Most currency conversion errors are avoidable with a short checklist applied before each large transfer.

[aa btn]Book a Call[/aa]

[/aa]

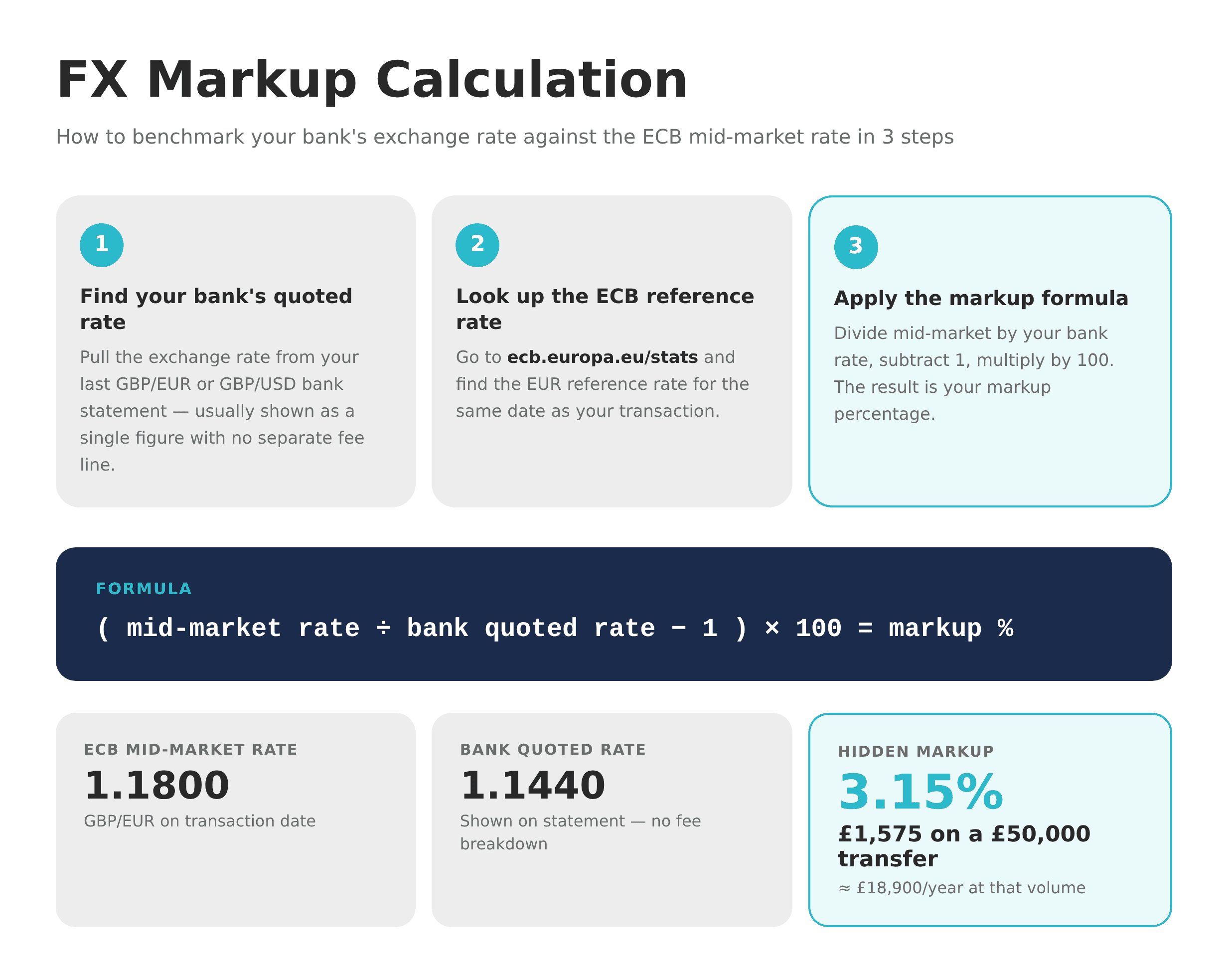

Step 1 — Benchmark Your Current FX Conversion Rate Against Mid-Market

Before changing anything, calculate exactly how much your bank is charging on each conversion.

The mid-market rate — also called the interbank rate — is the midpoint between the buy and sell price of a currency pair on global markets. It's published daily by the ECB for EUR pairs and by the Bank of England for a wider range of currencies. Every provider adds a margin on top of this rate — the question is how large that margin is.

Here's how to calculate your FX conversion rates on a business account UK:

Find the exchange rate shown on your last bank statement for a GBP/EUR or GBP/USD conversion.

Look up the ECB reference rate (for EUR) or a market data feed for the same date.

Apply this formula: (mid-market rate ÷ bank quoted rate − 1) × 100 = markup percentage.

Worked example:

ECB reference rate at time of conversion: GBP/EUR 1.1800

Bank quoted rate: GBP/EUR 1.1440

Markup: (1.1800 ÷ 1.1440 − 1) × 100 = 3.15%

On a £50,000 conversion, that 3.15% markup equals £1,575 in a single transaction. At £50,000 in monthly FX volume, the annual cost at that rate is around £18,900.

[aa fast-fact]

Fast Fact: According to BIS triennial FX market data, the GBP/EUR pair is among the most actively traded currency pairs globally — yet UK businesses converting via traditional bank accounts routinely pay 2.5–3.5% above interbank rates on every transaction.

[/aa]

Step 2 — Identify Hidden Markup in Your Bank Statements

Once you've run the calculation, the next question is why your bank doesn't show this cost separately. Understanding how to avoid hidden FX markup on your business account UK starts with knowing where to look for it.

Under the Payment Services Regulations 2017, payment service providers must disclose the exchange rate applied to a transaction — but they are not required to display the markup as a separate percentage. The rate is disclosed. The margin embedded within it is not.

Here's where the cost hides.

Three Common Markup Hiding Techniques

1. Rate embedded in the exchange rate

The bank quotes a composite rate that includes its margin. The statement shows one exchange rate — not a spread above mid-market. Without cross-referencing the ECB or a live market data feed at the time of the transaction, the markup is invisible.

2. "Zero commission" or "no transfer fee" language

Some banks advertise cross-currency transfers with no transaction fee. This is technically accurate. Revenue comes entirely from the rate margin. The advertising is factually correct but structurally misleading.

3. Weekend and off-hours surcharges

Many UK banks apply a wider spread on conversions processed outside normal market hours — typically Friday afternoon through Monday morning. This surcharge is rarely disclosed prominently. A payment triggered automatically on a Friday by accounting software may cost 0.5–1% more than the same conversion on a Wednesday.

Practical step: For any conversion above £10,000, request written confirmation of the spread percentage above the interbank rate. If your bank cannot supply this as a specific percentage, the markup is embedded in the quoted rate with no way to isolate it without manual benchmarking.

How to avoid hidden FX markup on a business account UK, in short: ask for the spread in writing before transacting, not after.

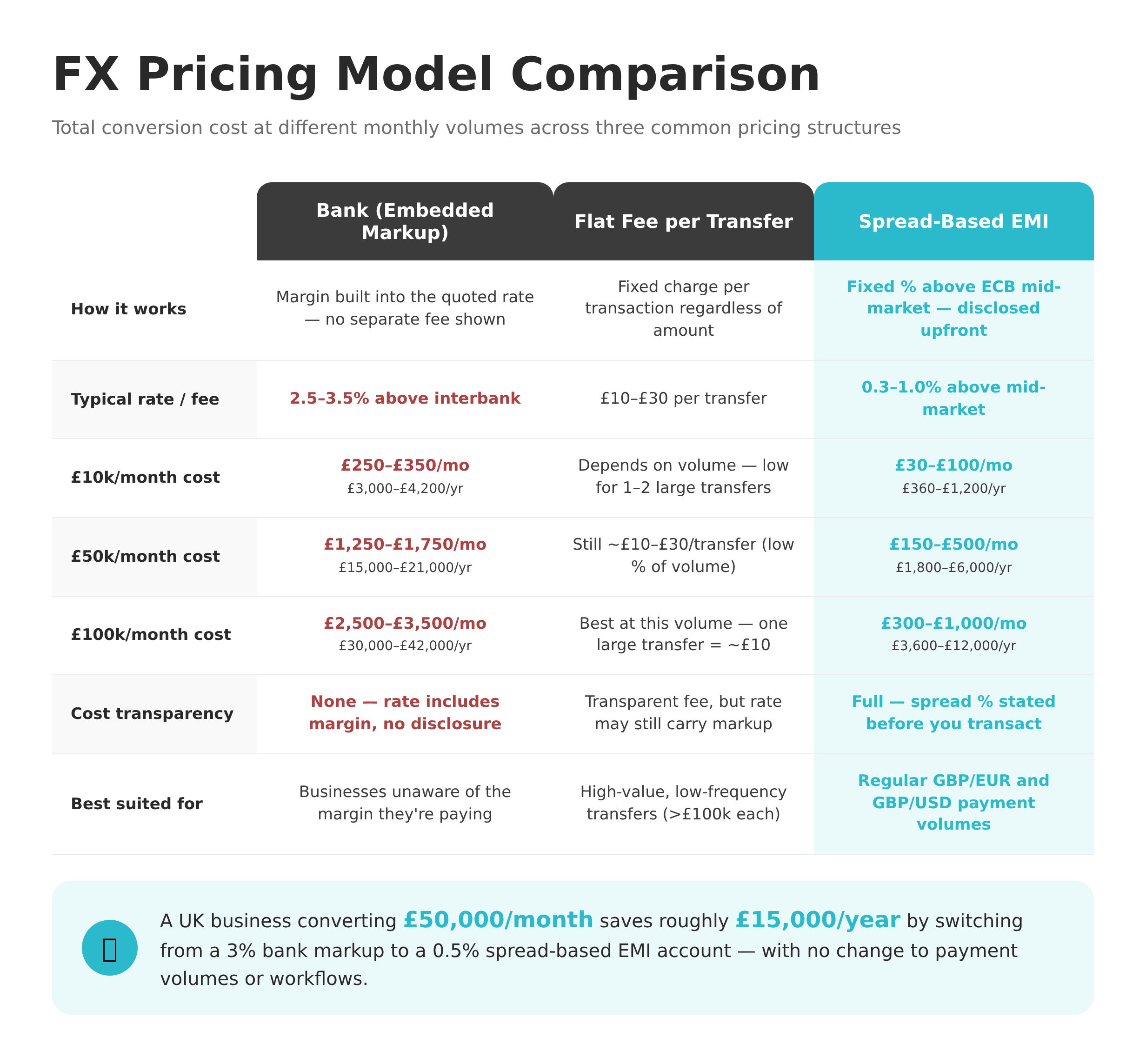

Step 3 — Compare FX Pricing Models: Spread vs Flat Fee vs Tiered

Not all FX pricing works the same way. Understanding the three main models is essential when evaluating competitive conversion options for GBP, EUR, and USD business payments.

Spread-based pricing

The provider applies a fixed percentage above mid-market, disclosed upfront. This is the standard model for most FCA-authorised EMI accounts. What is spread-based FX pricing for business accounts? It means you're told — before transacting — that a GBP/EUR conversion costs mid-market plus, say, 0.5%. As defined in BIS research on FX market microstructure, the bid-ask spread is the difference between the rate at which a currency is bought and sold; with spread-based pricing, that difference is stated as a fixed percentage before the transaction. Typical EMI spreads on major pairs: 0.3–1%.

Flat fee per transaction

A fixed charge applies regardless of amount. For a £200,000 conversion, a £10 flat fee is negligible. For a £500 conversion, it's proportionally significant. This model suits businesses with high-value, low-frequency FX needs.

Tiered / volume-based pricing

The spread narrows as monthly conversion volume increases. Useful for predictable, high-volume FX flows. The baseline tier is rarely competitive without active negotiation.

How spread-based FX works on a UK multi-currency EMI account vs bank markup is straightforward: the EMI publishes a spread of 0.3–1% for major pairs, applied above the real mid-market rate. The bank builds 2.5–3.5% into the quoted rate with no disclosure. For a business converting £50,000 per month, the difference between these two models is approximately £1,250–£1,750 per month.

[aa fast-fact]

Fast Fact: A UK business running £50,000/month in GBP/EUR conversions pays roughly £18,000/year at a 3% bank markup. The same volume on a 0.5% spread-based EMI account costs approximately £3,000/year — a saving of £15,000 without changing payment volumes or workflows.

[/aa]

Step 4 — Switch to a Multi-Currency Business Account with Transparent FX Pricing

Once you have benchmarked your current cost and identified which pricing model fits your volumes, the account setup is straightforward. Here is how to compare FX rates EMI vs bank on a UK business account and make the switch with confidence.

Four things to verify before opening:

Confirm FCA authorisation. Check that the provider holds a licence under the Electronic Money Regulations 2011. This is the primary regulatory framework for EMI accounts operating in the UK.

Get the spread in writing. Ask specifically: "What percentage above the ECB reference rate do you apply for GBP/EUR?" A provider that cannot give a specific figure is pricing via embedded markup.

Check for weekend and threshold charges. Some EMIs apply a 0.5–0.8% weekend premium or a minimum conversion fee. Confirm both before opening.

Verify multi-currency balance structure. The account must hold GBP, EUR and USD as separate balances — not just convert on receipt. This is the feature that allows paying EUR suppliers from a EUR balance with no conversion triggered.

Compare FX rates: UK EMI vs high street bank for GBP EUR USD conversion, and the most significant gap is not the rate on any single transaction — it's the compounding cost over 12 months of consistent FX volume.

For a full breakdown of the regulatory differences, see FCA-Authorised EMI vs Bank UK: Key Differences for Business Accounts.

[aa cta]

Set Up a Multi-Currency Account with Transparent FX Rates

Hold GBP, EUR and USD in one place. Spread-based pricing, no hidden markup.

[aa btn]Open Account[/aa]

[/aa]

Common Currency Conversion Mistakes UK Businesses Make

Even with the right account in place, operational habits erode savings. These are the five most common errors in UK SMBs managing regular GBP/EUR and GBP/USD payments.

Mistake 1: Converting on the day the invoice is due

Waiting until a payment deadline means accepting whatever rate is available at that moment. Businesses that hold a target currency balance — or convert when rates are favourable rather than when invoices fall due — avoid this entirely. A multi-currency account holding GBP, EUR and USD removes the time pressure on individual transactions.

Mistake 2: Not benchmarking before large transactions

On conversions above £25,000, the difference between a 0.5% and a 3% rate is material. A 30-second check — comparing the provider's quoted rate against the ECB reference rate — confirms whether the spread is within the agreed range.

Mistake 3: Using the same bank for domestic and international payments

UK business current accounts are structured for domestic GBP payments. Using the same account for GBP/EUR and GBP/USD conversions means accepting the bank's FX terms with no alternative pricing available. Separating international FX into a dedicated account gives full visibility into conversion costs.

Mistake 4: Missing the Friday afternoon surcharge

Automated payments triggered by accounting software late on Thursday or on Friday may fall within the weekend surcharge window. For providers that apply a premium after 4pm Friday, scheduling large conversions mid-week reduces exposure by 0.5–1%.

Mistake 5: Overlooking minimum conversion thresholds

Some providers apply a flat minimum fee — for example, £15 on any conversion below £1,000. For businesses running small, frequent FX payments, this adds up across a quarter. Batching smaller conversions into a single weekly transaction avoids threshold fees. Paying EU suppliers via SEPA from a EUR balance bypasses the GBP/EUR conversion entirely — see SEPA Transfers from a UK Business Account: How to Pay EU Suppliers for how this works in practice.

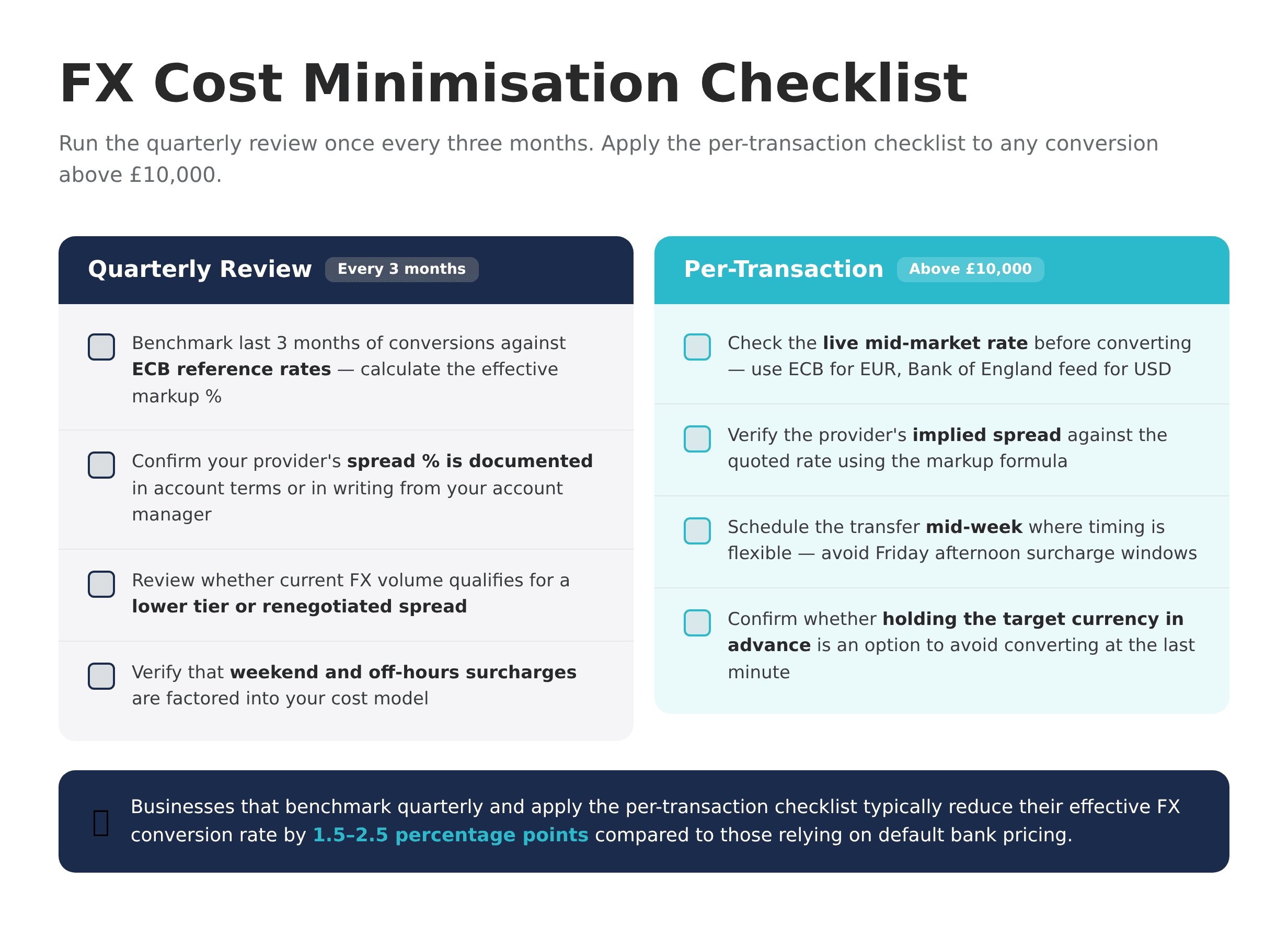

Checklist — Minimise FX Costs on GBP, EUR and USD Conversions for UK Business

Step-by-step: minimise FX costs on GBP EUR USD conversions for UK business by working through this two-part checklist — once per quarter and before each large individual transaction.

Quarterly review checklist:

Benchmark your last three months of conversions against ECB reference rates — calculate the effective markup percentage

Confirm your provider's spread percentage is documented in your account terms or in writing from your account manager

Review whether your current FX volume qualifies for a lower tier or renegotiated spread

Verify that weekend and off-hours surcharges are factored into your cost model

Per-transaction checklist (amounts above £10,000):

Check the live mid-market rate before converting

Verify the provider's implied spread against the quoted rate

Schedule mid-week where timing is flexible

Confirm whether holding the target currency in advance is an option

Low FX spreads on a business account UK reduce the base cost per transaction — but operational discipline determines whether those savings are consistently captured. Businesses that benchmark quarterly and apply the per-transaction checklist typically reduce their effective FX conversion rate by 1.5–2.5 percentage points compared to those relying on default bank pricing.

[aa fast-fact]

Fast Fact: Holding a EUR balance and paying EU suppliers directly from it — rather than converting GBP on each invoice — eliminates the GBP/EUR conversion cost on those payments entirely.

[/aa]

FAQ

How do I find the hidden FX markup on my UK business account?

Pull up the ECB reference rate for GBP/EUR at the time of your last conversion. Compare that rate to what appears on your bank statement. Divide the mid-market rate by the bank rate, subtract 1, and multiply by 100 — the result is the markup percentage. UK high-street banks typically charge 2.5–3.5% above interbank on GBP/EUR and GBP/USD conversions, but this cost does not appear as a separate line item on statements.

What is spread-based FX pricing for business accounts?

Spread-based FX pricing means the provider charges a fixed percentage above the mid-market rate on each conversion, stated upfront before the transaction. For example, a 0.5% spread on a GBP/EUR transaction at mid-market 1.1800 produces a rate of 1.1741. Because the spread is disclosed in advance, the full cost is calculable before transacting — unlike a bank's embedded markup, which is only identifiable by benchmarking the quoted rate against ECB data after the fact.

How do I get competitive FX rates on a business account UK?

Request your provider's spread percentage in writing and compare it against the ECB reference rate for GBP/EUR or a market feed for GBP/USD. A spread of 0.5–1% on major pairs is competitive for UK business accounts. If your provider cannot give a specific spread percentage, the margin is embedded in the quoted rate — typically 2.5–3.5% for UK high-street banks. Switching to an FCA-authorised EMI with transparent spread-based pricing on a business account UK is the most direct way to reduce the base conversion cost.

How do I compare FX rates EMI vs bank for a UK business account?

Obtain the explicit spread or margin percentage from both providers. Benchmark each against the ECB reference rate for GBP/EUR or a live feed for GBP/USD. Factor in all additional charges: per-transaction fees, weekend surcharges, and minimum conversion thresholds. The total cost per transaction is the sum of all these components — not just the headline exchange rate. Note that FCA-authorised EMI accounts — regulated under the Electronic Money Regulations 2011 — do not offer FSCS deposit protection; that protection applies only to banks licensed under FSMA 2000.

Can I avoid currency conversion costs entirely on my UK business account?

Yes. A multi-currency business account that holds separate GBP, EUR and USD balances allows the business to pay EUR invoices from the EUR balance and USD invoices from the USD balance, with no conversion triggered on same-currency transactions. This removes conversion cost entirely on those payments. SEPA transfers from a EUR balance to EU suppliers are a practical example — euros are transferred directly without triggering a GBP-to-EUR conversion.

[aa cta]

Get Transparent FX Rates for Your UK Business

Hold GBP, EUR and USD. Spread-based pricing with no hidden markup or weekend surcharges.

[aa btn]See FX Pricing[/aa]

[/aa]

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)