•

•

SEPA Transfers from a UK Business Account: How to Pay EU Suppliers

[aa disclaimer]

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A UK technology company wins a contract with a German manufacturer. The supplier invoices in euros and lists a standard eurozone IBAN. The UK finance team enters the details into their banking portal — and discovers that the high-street bank has routed it as a SWIFT international wire, charging £25 with a three-day delivery window. The German supplier received €940 instead of €980 after correspondent fees.

This is more common than most finance managers realise.

SEPA transfers from a UK business account follow a different path than domestic or SWIFT payments — and the distinction has material consequences for cost, timing, and compliance. Since Brexit, the UK is no longer part of the Single Euro Payments Area. But SEPA Credit Transfers remain the most cost-effective route for paying EU suppliers in euros, provided the account and setup are correct.

This guide explains how SEPA works from a UK originating account, what the technical requirements are, how T+1 settlement applies in practice, and how to structure the right account to pay European suppliers reliably.

[aa key-takeaways]

Key Takeaways

The UK is no longer a SEPA participant after Brexit, but UK businesses can send SEPA Credit Transfers through FCA-authorised EMI accounts with native SEPA connectivity via a eurozone entity.

BIC/SWIFT codes are mandatory for UK-originated SEPA transfers — unlike intra-EU payments, where BIC has been optional since 2016.

Standard SEPA Credit Transfer (SCT) settles by end of the next TARGET2 business day (T+1); SEPA Instant (SCT Inst) settles within 10 seconds, 24/7.

FX conversion at a traditional bank adds 1–3% in margin above mid-market; FCA-regulated EMIs typically offer rates close to mid-market with a stated fee.

Routing through an account without native SEPA access defaults the payment to a SWIFT correspondent chain — slower, more expensive, and less predictable.

[aa btn]Book a Call[/aa]

[/aa]

What Are SEPA Credit Transfers?

SEPA (Single Euro Payments Area) is a payment integration initiative governed by the European Payments Council (EPC) that standardises euro-denominated credit transfers across its member countries. As of 2024, SEPA covers 36 countries — the 27 EU member states plus Iceland, Liechtenstein, Norway, Switzerland, Andorra, Monaco, San Marino, Vatican City, and several others.

The legal framework is anchored in EU Regulation 260/2012, which established common technical standards for euro credit transfers and direct debits.

Two payment types exist within SEPA:

The standard SEPA Credit Transfer (SCT) settles by end of the next TARGET2 business day (T+1). SEPA Instant (SCT Inst), introduced in 2017, settles within 10 seconds, 24/7/365. Since October 2025, EU PSPs above a volume threshold are required to offer SCT Inst at no extra charge. Both require EUR denomination and IBAN as the account identifier.

Is the UK Still Part of SEPA?

Short answer: no — and this matters practically.

The UK participated in SEPA as a third-country adherent through the EPC's open access policy, even after leaving the EU in January 2020. However, the EPC updated its scheme rulebooks in 2023 and the UK was not carried forward as a recognised SEPA country. UK IBANs are no longer listed in the official SEPA country code registry.

What this means in practice:

UK banks and payment institutions are not SEPA Scheme Participants directly. They must access the SEPA network through European correspondent banks or through a licensed European subsidiary with active SCT scheme membership.

IBAN discrimination rules under EU Regulation 260/2012 — which prevent EU creditors from refusing SEPA-zone IBANs — do not extend to UK IBANs after Brexit.

The effect is asymmetric: it primarily affects the UK-originated outbound leg.

As a result, a standard GBP current account with a GB IBAN cannot originate a SEPA Credit Transfer. UK businesses that need to initiate a SEPA Credit Transfer UK-side must use an account issued by, or connected to, an institution with active SEPA scheme participation.

SEPA Transfers from a UK Business Account

Despite the UK's third-country status, SEPA transfers from UK business account setups remain accessible and cost-effective. The route you take determines the cost, timing, and reliability of every payment.

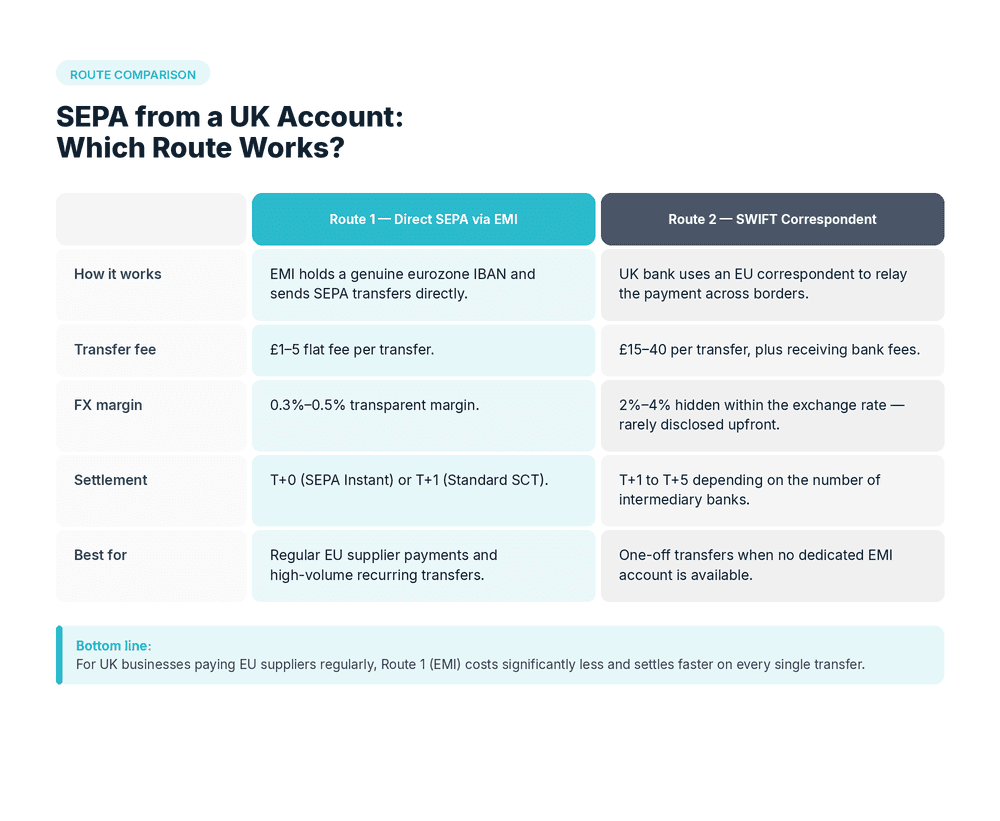

Route 1: FCA-Authorised EMI with Direct SEPA Connectivity

This is the correct approach for businesses paying EU suppliers regularly.

A growing number of FCA-authorised electronic money institutions operating in the UK maintain direct SEPA connectivity through European subsidiaries or through agency arrangements with SEPA Scheme Participants. These accounts issue a eurozone IBAN — typically carrying an IE (Ireland), NL (Netherlands), or LT (Lithuania) country prefix — while the business maintains an account relationship under UK FCA regulatory oversight.

When a UK business SEPA payment is initiated through such an account, the payment instruction enters the SEPA infrastructure directly. From the EU supplier's perspective, the inbound credit is indistinguishable from any other SCT — it arrives with a clean euro amount, an ISO 20022-compliant message, and T+1 settlement timing.

This is the correct approach for businesses looking to pay EU suppliers from UK accounts reliably. The routing is predictable, the settlement timeline is fixed, and the cost structure is transparent.

Route 2: SWIFT Correspondent with SEPA Last Mile

This is where UK businesses quietly lose money — on every single payment.

Most UK high-street banks don't have direct SEPA access. When you send a EUR payment to a European IBAN, it goes out via SWIFT to a eurozone correspondent, which then drops it into SEPA at the other end.

Here's what that journey actually costs:

Transfer fee: £15–£30, deducted before your supplier sees a cent

FX margin: 1.5–2.5% above mid-market, baked into the exchange rate

Settlement: T+2 to T+3 — not T+1

Your German logistics provider invoices €5,000. They receive €4,972 and wonder why you're shorting them.

If your business runs regular international supplier payment UK cycles — freight, SaaS subscriptions in EUR, European manufacturers on 30-day terms — you're absorbing this cost on every single payment. Individually it looks small. Across a year's worth of invoices, it adds up to a number worth caring about.

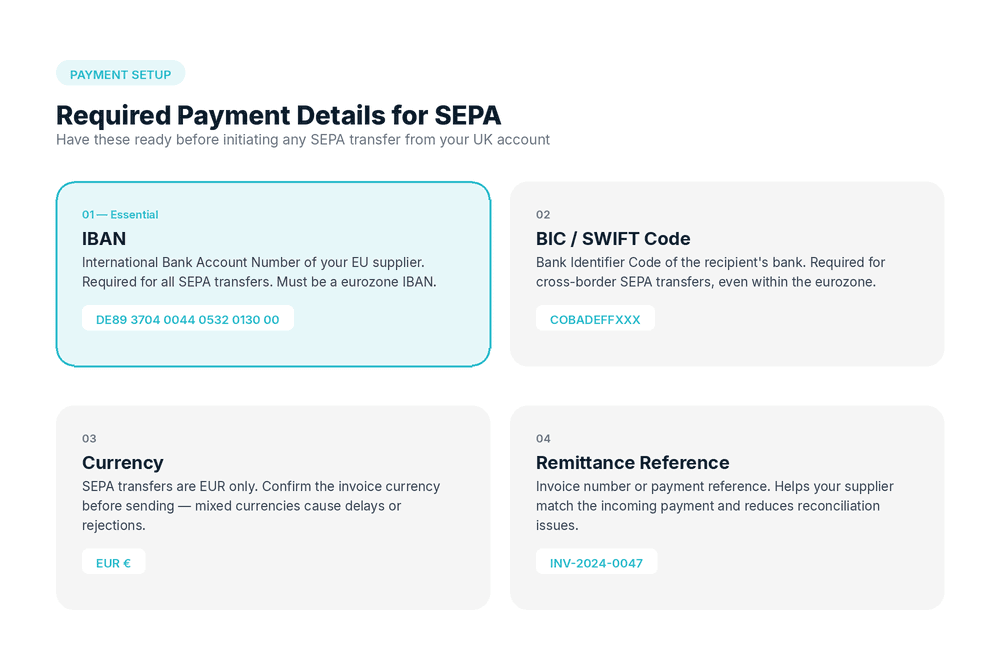

Required Payment Details

Before the first payment goes out, your finance team needs four things from every EU supplier. Get any one of these wrong and the transfer bounces — or worse, lands in the wrong account.

Field | Requirement | Why it matters |

|---|---|---|

IBAN | Validate check digits before sending | Invalid IBAN = immediate return, sometimes with a fee |

BIC (SWIFT code) | Mandatory for UK-originated transfers | Optional inside EU since 2016 — not from UK accounts |

Currency | EUR only | GBP amount triggers FX conversion at account level |

Remittance reference | Up to 140 characters (ISO 20022) | Invoice number + PO needed for supplier reconciliation |

[aa cta]

Paying EU suppliers from a UK account

Open an EQWIRE euro business account with native SEPA connectivity and send euro payments to EU suppliers at the mid-market rate — no SWIFT fees, no hidden FX margins.

[aa btn]Create Account[/aa]

[/aa]

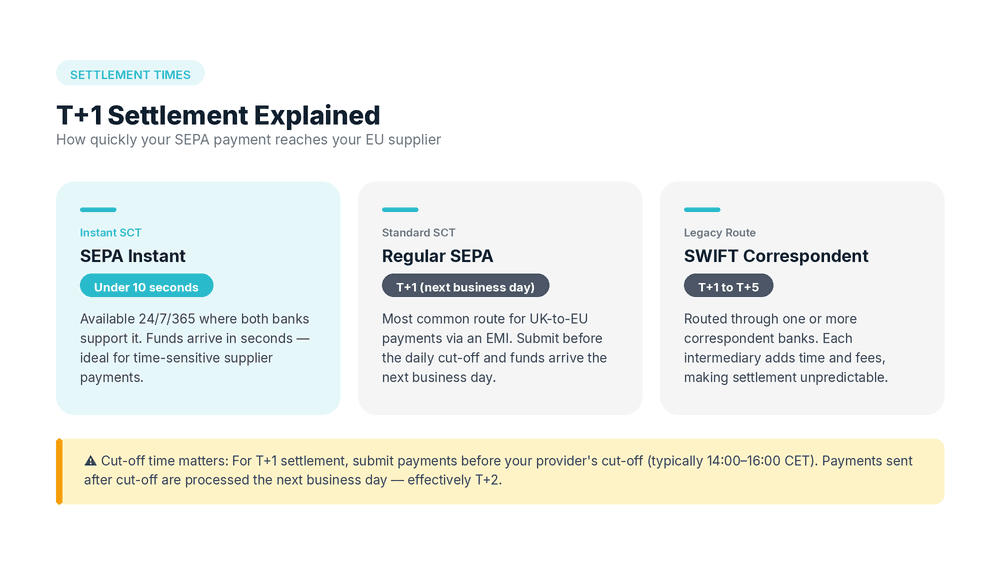

SEPA T+1 Settlement: What UK Businesses Need to Know

SEPA T+1 settlement means your EU supplier's bank must receive the funds by the end of the next TARGET2 business day after you submit the instruction. The European Central Bank operates TARGET2 on its own calendar — not the UK's — which matters more than most UK finance teams expect.

Three variables affect whether the payment actually arrives on time:

Cut-off time is the most common culprit. Most SEPA-connected accounts stop processing somewhere between 14:00 and 16:00 CET. Miss that window and you've added a full day — paying German suppliers on a Friday afternoon becomes a Monday problem.

Calendar differences add another variable. A UK bank holiday delays T from starting at all. ECB closing days (around 10 per year) delay the EU-side settlement regardless of when you sent the instruction.

The pre-SEPA leg is where UK businesses lose time with traditional banks. For a natively connected EMI account, this leg is near-instantaneous. For a SWIFT-routed bank, it can add 24–48 hours before T+1 even begins.

SEPA Instant eliminates all three issues. SCT Inst processes in under 10 seconds, any time of day, including weekends.

For SEPA T+1 settlement UK business workflows, the SEPA payment processing time from a natively connected EMI account is functionally identical to intra-SEPA once the instruction enters the infrastructure. The variable is the pre-SEPA leg — near-instantaneous for a direct EMI account, 24–48 hours added for a SWIFT-routed bank.

[aa fast-fact]

As of October 2025, all EU-based payment service providers processing more than 2.5 million payment transactions per year are required to offer SEPA Instant Credit Transfer at no extra cost compared to standard SCT — a mandate established under EU Instant Payments Regulation 2024/886.

[/aa]

FX Costs on Cross-Border Euro Payments from UK Accounts

Here's where UK businesses quietly lose money: FX margins.

Most UK businesses hold GBP — which means every cross-border euro payment UK involves a conversion. Compare your bank's rate to the Bank of England's reference rate for that same currency pair. The difference — often 1.5% to 3% — is pure margin your bank is keeping.

On a £50,000 supplier payment, that's up to £1,500 lost. Instantly. On every transfer.

FCA-authorised EMIs offering a euro business account UK work differently:

Apply a rate close to mid-market

Charge a transparent, stated fee — usually a small percentage or fixed amount

Show you exactly what you're paying before you confirm

For businesses running regular EUR supplier payments, that difference in FX treatment is often the largest single cost saving versus a traditional bank.

The smartest approach: eliminate conversion entirely. If your business receives EUR from EU clients, hold it in a multi-currency account alongside GBP and USD and pay your EU suppliers directly from the EUR balance. No conversion on the outbound leg. For companies with matched EUR inflows and outflows, the FX cost drops to zero.

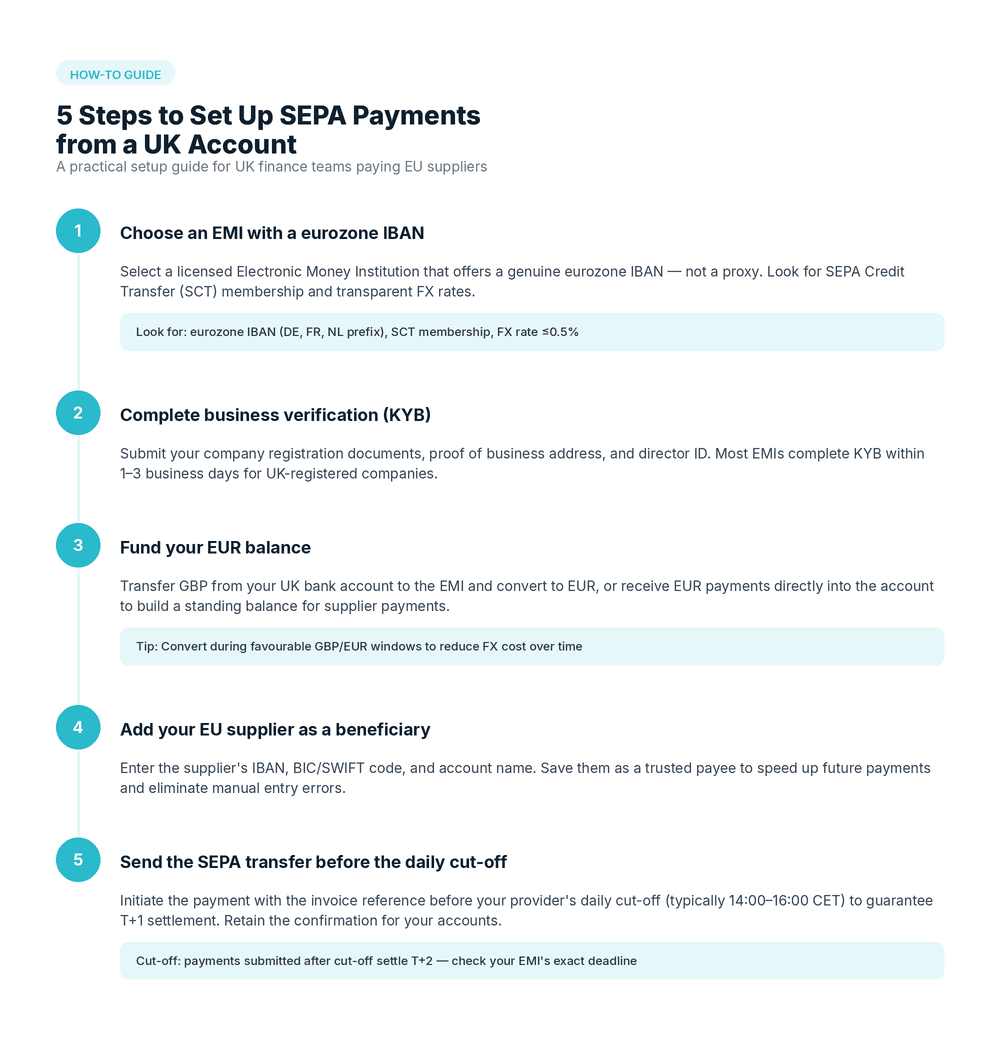

How to Set Up SEPA Eurozone Payments: Step by Step

Establishing a working SEPA payment workflow from a UK business involves five sequential steps. Understanding how to send SEPA payment from UK accounts correctly at each stage prevents the most common errors: wrong IBAN format, missing BIC, and post-cut-off submission.

Step 1: Open a SEPA-Reachable Euro Business Account

The originating account must have native SEPA scheme access. The indicator is the IBAN prefix: a eurozone IBAN (IE, NL, LT, DE, or similar) signals the account is on the SEPA infrastructure.

A GB IBAN won't route as SEPA without a SWIFT conversion step. A UK FCA EMI SEPA-connected account gives the business a genuine eurozone identifier under FCA regulatory oversight.

Step 2: Collect and Validate Recipient Details

For each EU supplier: full legal name, IBAN (validate check digits before sending — a single wrong character causes immediate return), BIC/SWIFT code, and the payment reference format they need for their reconciliation.

Step 3: Verify SEPA Reachability

Before sending for the first time, confirm that the recipient's institution is reachable as a SEPA Scheme Participant. The EPC list of SEPA Scheme Participants is updated regularly — the vast majority of eurozone banks are listed; some non-bank institutions may not be direct participants.

Step 4: Initiate the SEPA Credit Transfer

In the account portal, select SEPA Credit Transfer as the payment type. Enter the recipient IBAN, BIC, EUR amount, and remittance reference. If converting from GBP, review the applied rate before confirming. Submit before the account's daily cut-off to ensure same-day processing.

For businesses sending regular payments to multiple EU counterparties, a bulk SEPA payment workflow using batch file upload processes multiple instructions simultaneously and eliminates per-payment manual entry.

Step 5: Confirm Settlement and Retain Records

The beneficiary's PSP must credit the account by end of T+1. Retain the UETR (Unique End-to-End Transaction Reference) for every outbound payment — it satisfies UK record-keeping obligations and is the primary reference for tracing.

For recurring multi-supplier cycles, batch payment automation preserves SEPA settlement speed across the full supplier base without individual SWIFT routing.

SEPA Transfer Requirements UK Businesses Should Verify

Three things to confirm before your first payment goes live. None of them are complicated — but all of them cause delays if you hit them unprepared.

Sanctions screening happens automatically on both sides. Your institution checks the UK Consolidated Sanctions List before the payment leaves; the recipient bank runs its own EU-side check on arrival. Flagged counterparties get held for manual review. A basic check on new EU suppliers during onboarding is faster than chasing a held payment three days later.

Purpose codes are optional for most B2B supplier payments under the SCT scheme. Some EU banks request an ISO 20022 purpose code for AML reporting — particularly on higher-value transactions. Missing one when a specific recipient bank requires it causes delays that are entirely avoidable.

Record-keeping: retain international payment records for at least five years. Every SEPA Credit Transfer generates a UETR — that reference plus the payment confirmation is your primary audit evidence.

For teams operating how to pay European suppliers using SEPA from a UK business account as a routine workflow, the overhead is low once documented. SEPA transfers from a UK business account settle cleanly in euros — the supplier receives the full amount, no correspondent deductions, when the payment routes through native SEPA infrastructure.

FAQ

How long does a SEPA transfer take from a UK business account?

A SEPA Credit Transfer from a UK account with direct SEPA connectivity settles by the end of the next TARGET2 business day (T+1). SEPA Instant settles within 10 seconds. Payments routed through a UK bank without native SEPA access — via SWIFT as transit — may take T+2 to T+3 before the SEPA T+1 clock begins.

What information is needed to send a UK business SEPA payment?

The originator needs the recipient's IBAN, BIC (SWIFT code), the payment amount in euros, and a remittance reference. BIC is mandatory for UK-originated SEPA transfers — unlike intra-EU payments, where BIC has been optional since 2016.

How to make SEPA credit transfer from UK business account?

Open an account with a eurozone IBAN from an FCA-authorised EMI or a UK bank with direct SEPA access. Enter the recipient IBAN and BIC, set the amount in EUR, and submit before the daily cut-off. The payment enters the SCT scheme at submission and is credited by end of T+1. For bulk payments, a batch file upload processes multiple recipients in a single instruction cycle.

What is SEPA T+1 settlement and does it apply to UK businesses?

SEPA T+1 settlement means the recipient's PSP must credit their account by the end of the next TARGET2 business day after the instruction is received. UK businesses using a SEPA-connected account get T+1 under the same conditions as EU-based senders. The clock starts when the instruction enters the SEPA infrastructure — delays on the UK-to-SEPA leg add to total processing time.

Is sending SEPA from UK cheaper than SWIFT for EU supplier payments?

When routed correctly, SEPA from UK is cheaper. Native SEPA routing carries no correspondent banking fee and settles at T+1, whereas SWIFT wires typically cost £15–£30 and take T+2 to T+3. FX costs vary by provider: EMIs apply mid-market rates with a stated fee; high-street banks use a proprietary rate with a 1.5–3% margin built in.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)