•

•

HKD Business Account for Non-Hong Kong Companies: Receive Payments in Hong Kong Dollars

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Hong Kong settles over HK$600 billion in daily foreign exchange turnover and remains the primary gateway for mainland China trade. Yet most non-resident companies cannot open a traditional Hong Kong bank account. The barrier is structural: Hong Kong banks require local ID holders, physical branch visits, and minimum deposits starting at HK$10,000 — with enhanced due diligence that effectively screens out offshore entities.

An HKD business account for a non-HK company is now accessible through a different route. UK-authorised Electronic Money Institutions issue multi-currency accounts with HKD capability to internationally incorporated businesses — remotely, without a Hong Kong banking relationship. This guide explains how the mechanism works, what the regulatory framework looks like, and what non-Hong Kong companies need to prepare before applying.

[aa key-takeaways]

Key Takeaways

Non-Hong Kong companies can receive HKD payments without opening a local Hong Kong bank account — a UK-authorised EMI provides HKD capability remotely

Traditional Hong Kong banks require physical presence, HK ID holders, and minimum balances of HK$50,000+ — most offshore applicants are rejected

HKD is received via SWIFT inbound and held as a dedicated balance within a multi-currency account alongside GBP, EUR, and USD

FCA safeguarding rules protect client funds in EMI accounts under the Electronic Money Regulations 2011 — a different model from bank deposit protection

Document preparation and UBO verification are the primary variables in onboarding speed — typical approval takes 5–15 business days

[aa btn]Open HKD Account[/aa]

[/aa]

Why Non-Hong Kong Companies Need HKD Payment Capability

Hong Kong's Role in Asia-Pacific Trade

Hong Kong is the world's 8th largest trading economy. Total merchandise trade exceeded HK$8.3 trillion in 2023, with the territory functioning as the primary intermediary for trade flows between mainland China and international markets.

The Hong Kong dollar is pegged to the US dollar within a narrow band of HK$7.75–7.85 per USD, maintained by the Hong Kong Monetary Authority since 1983. This peg provides foreign exchange stability that few Asian currencies can match — making HKD a practical settlement currency for companies trading across the region.

For businesses billing Hong Kong clients, receiving dividends from Hong Kong subsidiaries, or settling with Hong Kong-based suppliers, a dedicated Hong Kong dollar business account eliminates the forced currency conversion that erodes margin on every transaction.

The Cost of Not Having a Dedicated HKD Account

Without a dedicated HKD account, payments from Hong Kong arrive via international SWIFT wire. Each inbound SWIFT transfer carries correspondent banking fees of £15–£30 per transaction, plus intermediary bank deductions that reduce the received amount unpredictably.

The real cost compounds further. HKD received into a non-HKD account triggers automatic currency conversion — typically at a spread of 1–3% above mid-market rate. On a monthly HKD inflow of HK$500,000, that conversion cost alone ranges from HK$5,000 to HK$15,000.

[aa fast-fact]

Fast Fact: A company receiving HK$500,000 monthly without a dedicated HKD account loses HK$5,000–15,000 per month in forced FX conversion — up to HK$180,000 annually.

[/aa]

Settlement speed adds a third layer of friction. SWIFT transfers from Hong Kong take 2–5 business days to clear, depending on intermediary routing. For businesses managing cash flow across multiple currencies, that delay creates real operational drag.

Why Traditional Hong Kong Banks Reject Non-Resident Applications

Physical Presence and KYC Requirements

Most Hong Kong banks require at least one director or authorised signatory to attend a branch in person during the account opening process. HSBC, Hang Seng Bank, Bank of China (Hong Kong), and Standard Chartered all maintain this requirement for non-resident applicants, though some offer video verification for Hong Kong-incorporated entities with local ID holders.

Online applications at banks like DBS Hong Kong are limited to companies incorporated in Hong Kong with directors holding HK Permanent ID Cards. For a UK-incorporated company, a BVI holding entity, or a UAE-registered business, the digital onboarding path simply does not exist at traditional Hong Kong banks.

Minimum Balance and Fee Structures

The financial requirements create a second barrier. HSBC's BusinessVantage account requires a minimum balance of HK$50,000 to waive monthly service fees. Hang Seng Bank sets the waiver threshold at HK$50,000–100,000 depending on account type, with monthly fees of HK$200 charged when the balance falls below.

Bank of China (Hong Kong) charges a Company Search Fee of up to HK$10,000 for overseas companies — a non-refundable due diligence cost incurred before any approval decision. Combined with potential in-person travel costs, the total upfront investment for a non-resident applicant can exceed HK$20,000 before a single HKD payment is received.

Enhanced Due Diligence for Offshore Structures

Here is where most non-Hong Kong companies hit a wall. Banks apply enhanced due diligence to entities incorporated in offshore jurisdictions — BVI, Cayman Islands, Seychelles, and similar. Multi-layered ownership structures trigger additional scrutiny. Companies without existing Hong Kong trading history face the highest rejection rates.

The underlying driver is risk appetite, not regulatory prohibition. The FCA has published guidance acknowledging that financial institutions increasingly exit relationships with offshore clients rather than invest in the compliance infrastructure to manage them. Hong Kong banks follow the same pattern — it is cheaper to decline the application than to resource the enhanced review.

Requirement | Traditional HK Bank | UK-Authorised EMI |

|---|---|---|

Physical presence in HK | Required (branch visit) | Not required |

HK ID holder needed | Yes (for online apps) | No |

Minimum deposit | HK$10,000–50,000 | None (typical) |

Monthly balance requirement | HK$50,000–500,000 | None (typical) |

Onboarding timeline | 2–8 weeks | 5–15 business days |

Offshore entities accepted | Rarely | Yes (subject to compliance) |

HKD inbound method | Local FPS + SWIFT | SWIFT |

How an HKD Business Account Works Through a UK EMI

What Is a UK-Regulated Electronic Money Institution

An Electronic Money Institution is a financial services provider licensed under the Electronic Money Regulations 2011 and supervised by the Financial Conduct Authority. EMIs are authorised to issue electronic money, provide payment services, and hold client funds — but they are not banks in the traditional sense.

The key regulatory distinction: EMIs do not take deposits and do not offer credit facilities, overdrafts, or interest on balances. Client funds are not covered by the Financial Services Compensation Scheme. Instead, EMIs must safeguard client funds by holding them in segregated accounts at authorised credit institutions, completely separate from the EMI's own operating capital.

Any company can verify an EMI's authorisation status on the FCA Financial Services Register before opening an account.

How HKD Is Received and Held in a Multi-Currency Account

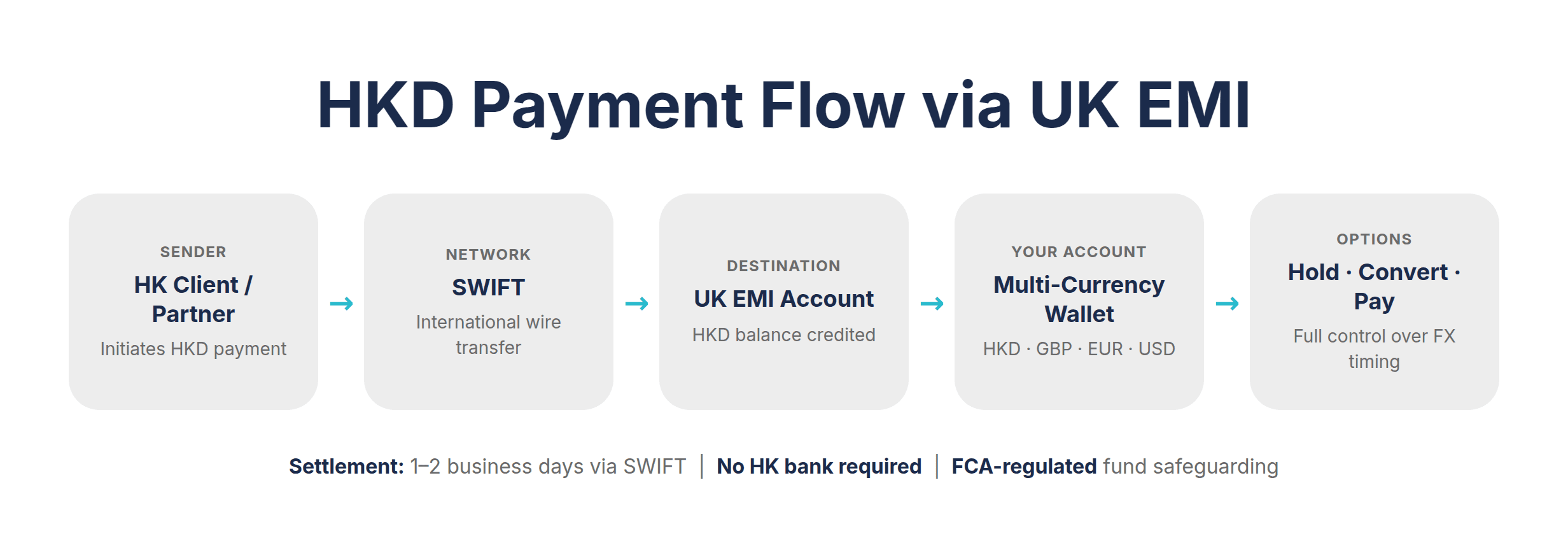

A UK EMI with HKD capability assigns the client company a dedicated account that supports multiple currencies — typically GBP, EUR, USD, and HKD — under a single login. HKD received via SWIFT inbound settles directly into the HKD balance within this multi-currency account.

The account is issued in the company's registered name. Payers in Hong Kong send HKD to the account using standard SWIFT payment instructions, including the EMI's SWIFT BIC and the dedicated account reference. From the payer's perspective, the process is identical to sending a SWIFT wire to any international bank account.

What this means in practice: a BVI-incorporated company can hold an HKD balance, receive HKD from Hong Kong clients, and manage that balance alongside GBP, EUR, and USD — all without a Hong Kong bank account or any physical presence in Hong Kong.

Payment Rails — SWIFT, FPS, and Currency Conversion

HKD inbound payments arrive via SWIFT. This is the standard international payment network connecting banks and financial institutions across 200+ countries. For HKD payment accounts held by non-resident entities, SWIFT is the primary receipt channel.

An important distinction: Hong Kong's local Faster Payment System (FPS) is not directly accessible through UK-based EMIs. FPS enables real-time HKD transfers between Hong Kong bank accounts, but access requires a direct connection to the HKMA-operated clearing system. For non-Hong Kong companies receiving HKD from overseas, SWIFT remains the standard and most widely used channel.

Currency conversion is available within the multi-currency account. HKD balances can be converted to GBP, EUR, or USD at competitive spreads — typically tighter than the 1–3% markup applied by traditional banks on automatic conversions. The conversion is initiated by the account holder, not triggered automatically, which means the company controls the timing and rate.

[aa cta]

Ready to receive HKD without a Hong Kong bank account?

Open a multi-currency EQWIRE account and start accepting Hong Kong dollar payments remotely — with FCA-regulated fund safeguarding.

[aa btn]Open Account[/aa]

[/aa]

Documentation and Onboarding for Non-HK Companies

Corporate Documents Required

The document package for opening an HKD business account via a UK EMI follows a standard corporate KYC framework. Required documents typically include:

Certificate of Incorporation (or equivalent registration document)

Articles of Association or Memorandum of Association

Certificate of Good Standing (for companies older than 12 months)

Register of directors and shareholders

Proof of registered office address

Proof of business activity — contracts, invoices, or a business plan outlining expected transaction volumes

Documents not in English generally require certified translation. Bermuda-registered entities and other offshore-incorporated companies follow the same document framework — the jurisdiction of incorporation does not change the core requirements, though it may affect the compliance review timeline.

UBO Verification and Compliance Screening

Every individual who ultimately owns or controls 25% or more of the applicant company must be individually verified — regardless of how many corporate layers exist between the ultimate beneficial owner and the entity.

Each UBO must provide a government-issued photo ID (passport preferred) and proof of residential address dated within three months. The EMI's compliance team runs AML screening against international sanctions lists and PEP databases, combined with a risk assessment based on the business model, expected transaction volumes, and source of funds.

Incomplete UBO documentation is the single most common cause of application delays. Preparing the full document package — including certified translations where necessary — before submitting the application significantly reduces review time.

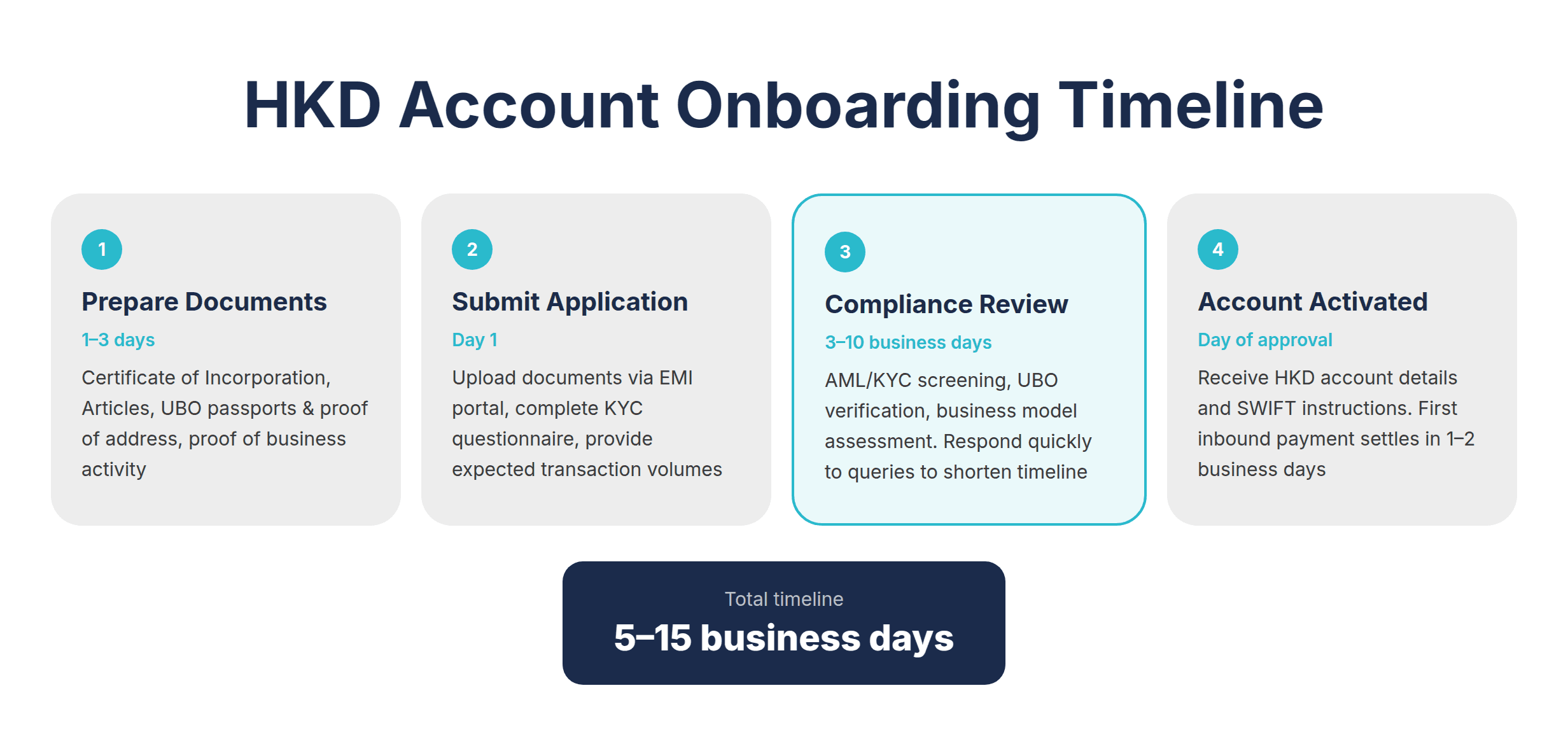

Timeline — Application to First HKD Receipt

Typical onboarding takes 5–15 business days from completed application submission. The primary variable is not the EMI's processing speed — it is the applicant's response time to compliance queries and the completeness of the initial document package.

For companies with straightforward ownership structures and complete documentation, approval can come within the first week. Complex multi-layered structures or jurisdictions that require additional due diligence may extend the timeline toward the upper end.

Once the account is activated, inbound SWIFT payments in HKD typically settle within 1–2 business days, depending on the sending bank's processing time. The first HKD receipt can arrive within 24 hours of account activation for senders using same-day SWIFT.

Regulatory Framework — FCA Authorisation and Fund Safeguarding

The question that matters most for any company evaluating this route: how are funds protected?

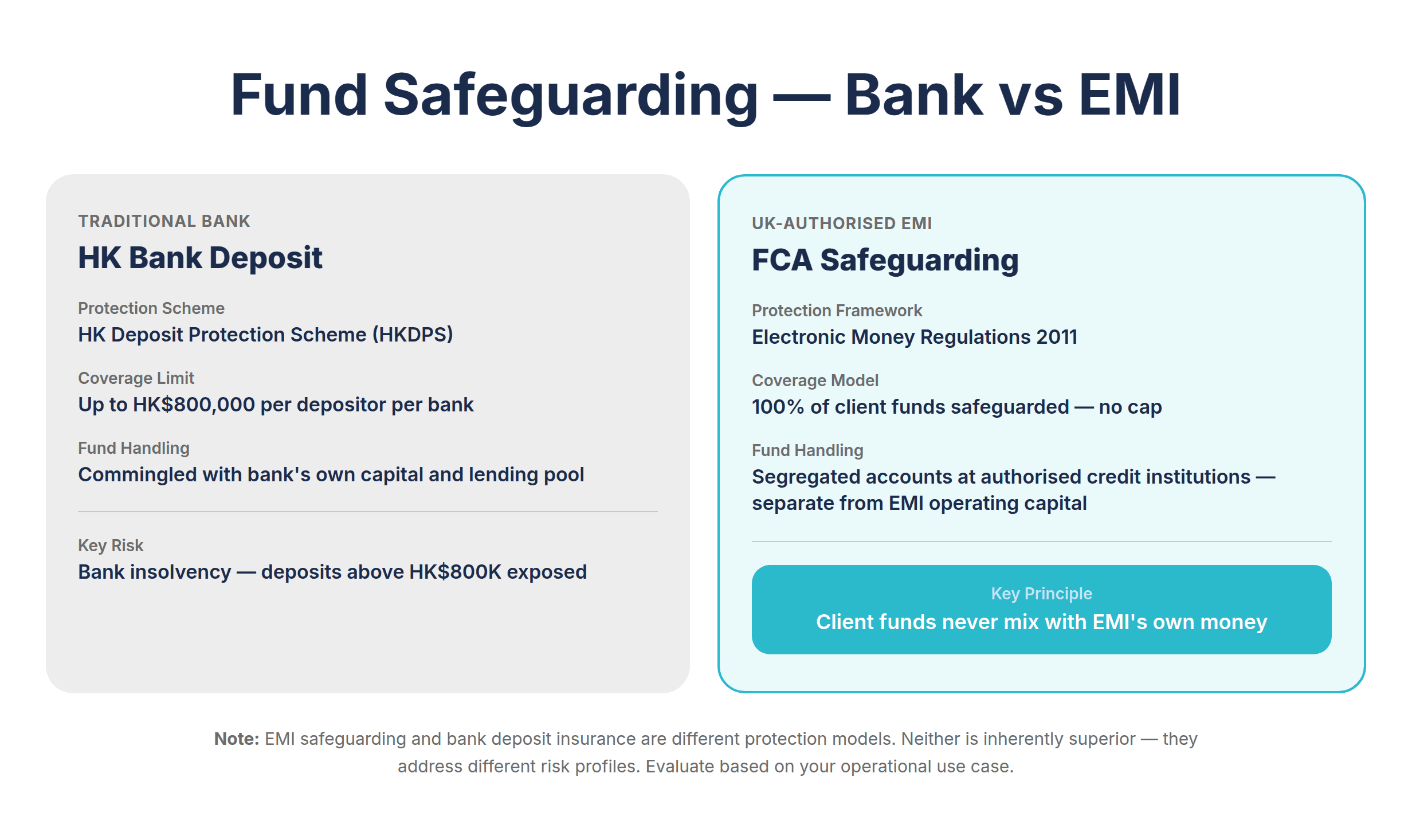

FCA-authorised EMIs operate under a specific safeguarding regime defined in the Electronic Money Regulations 2011. Client funds must be held in segregated accounts at authorised credit institutions — ring-fenced from the EMI's own operating capital. If the EMI were to become insolvent, client funds held in segregated accounts would not form part of the EMI's estate.

This is a different protection model from bank deposit insurance. Hong Kong's Deposit Protection Scheme covers bank deposits up to HK$800,000 per depositor per bank. The UK's FSCS covers eligible deposits up to £85,000. EMI accounts are not covered by either scheme — instead, the protection comes from the structural separation of funds.

For businesses using a multi-currency payment infrastructure alongside GBP settlement, understanding this distinction matters. The safeguarding model is robust for operational payment flows — holding funds in transit, receiving and converting currencies, paying suppliers — but it is not a substitute for a long-term deposit relationship at a bank.

Can a BVI company receive HKD without a Hong Kong bank account via a UK EMI? Yes — and the regulatory framework supporting that access is the same FCA authorisation and safeguarding regime that applies to GBP and EUR accounts issued by the same institution.

[aa fast-fact]

Fast Fact: FCA-authorised EMIs must hold client funds in segregated accounts at authorised credit institutions — separate from operating capital — under the Electronic Money Regulations 2011.

[/aa]

An HKD business account for a non-HK company through a UK-authorised EMI removes the structural barriers that traditional Hong Kong banks impose on offshore and internationally incorporated entities. The trade-off is clear: no local HK FPS access, no deposit insurance — but remote onboarding, dedicated HKD balances, SWIFT inbound capability, and FCA-regulated fund protection. For companies that need to receive Hong Kong dollars without establishing a Hong Kong banking relationship, this is the most direct regulated path available.

[aa cta]

Start receiving HKD payments in days, not weeks

EQWIRE provides FCA-authorised multi-currency accounts with HKD support for non-Hong Kong companies. Remote onboarding. No minimum balance. Segregated fund safeguarding.

[aa btn]Create Account[/aa]

[/aa]

FAQ

Can a BVI company receive HKD without a Hong Kong bank account via UK EMI?

Yes. A BVI-incorporated company can open a multi-currency account with a UK-authorised EMI that supports HKD. The account is opened remotely — no Hong Kong presence, Hong Kong bank relationship, or HK business registration is required. HKD payments arrive via SWIFT from Hong Kong-based payers. The EMI is regulated by the FCA under the Electronic Money Regulations 2011, and client funds are held in segregated accounts.

What documents does an offshore company need to open an HKD business account?

The standard document package includes a Certificate of Incorporation, Articles of Association or equivalent constitutional documents, a Certificate of Good Standing (for companies older than 12 months), a register of directors and shareholders, and proof of business activity such as contracts or invoices. Each ultimate beneficial owner with 25% or more ownership must provide a passport and proof of residential address dated within three months.

How long does it take to receive HKD payments after account approval?

Once the HKD business account is activated, inbound SWIFT payments in HKD typically settle within 1–2 business days, depending on the sending bank's processing time. Account activation itself takes 5–15 business days from completed application submission — the primary variable is document completeness and UBO verification speed.

Is HKD held in an EMI account protected the same way as a bank deposit?

No. The protection model is different. Bank deposits in Hong Kong are covered by the Deposit Protection Scheme up to HK$800,000 per depositor per bank. EMI accounts are not deposit accounts and are not covered by the FSCS or HKDPS. FCA-authorised EMIs must instead safeguard client funds under the Electronic Money Regulations 2011 — funds are held in segregated accounts at authorised credit institutions, separate from the EMI's operating capital.

Can a non-Hong Kong company send HKD payments to Hong Kong suppliers from an EMI account?

This depends on the specific EMI's outbound payment capabilities. Some UK-authorised EMIs support outbound SWIFT payments in HKD to Hong Kong bank accounts, while others focus on inbound receipt and currency conversion. Confirm outbound HKD payment capability with the provider before opening the account if supplier payments in HKD are a core business requirement.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)