•

•

Stripe Settlement Account Alternative for UK Businesses

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

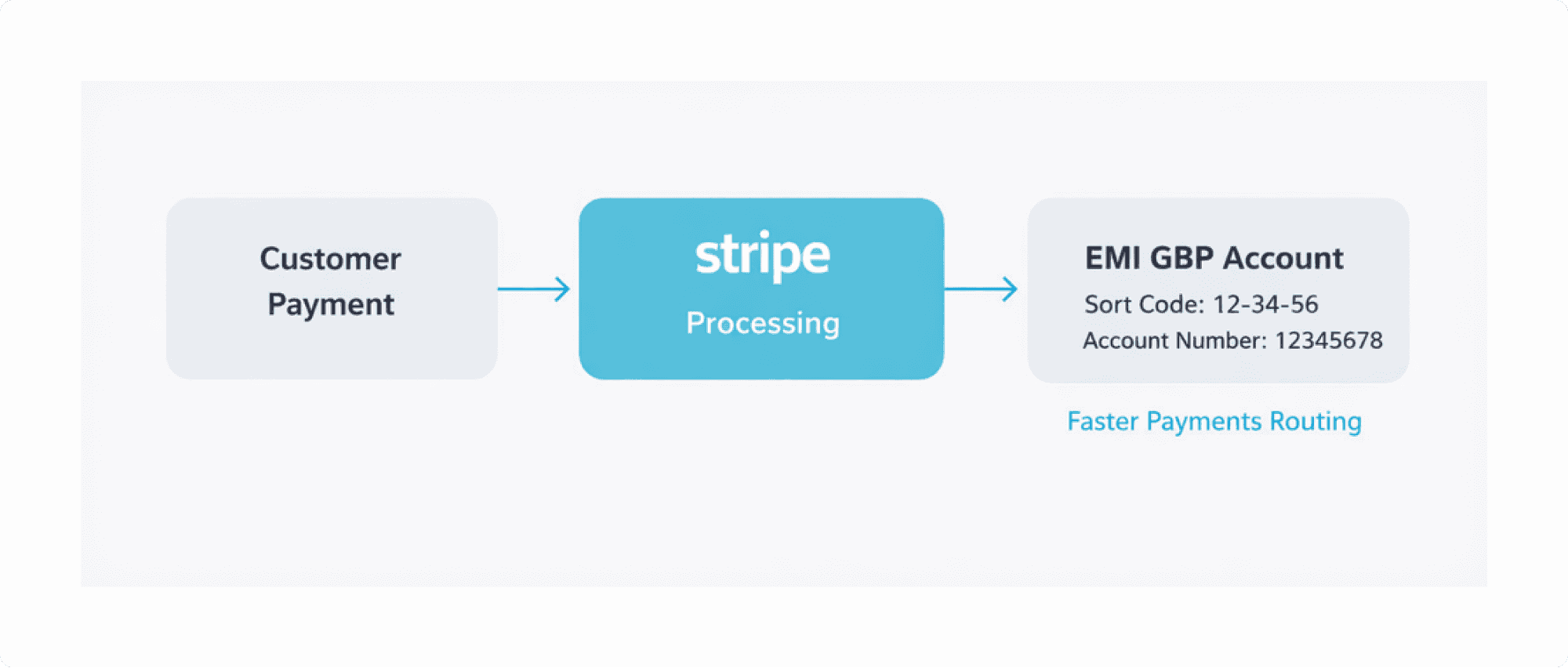

Stripe is where revenue lands. Your bank account is where it should go.

Between those two points sits a requirement that catches a surprising number of UK businesses off guard: Stripe needs an account with a valid UK sort code and account number before it will settle GBP payouts.

For businesses that can't easily access traditional UK banking — offshore-incorporated companies, newly launched e-commerce stores, SaaS platforms with complex revenue structures — that requirement creates a real cash flow bottleneck. And even for those who do hold a UK bank account, the wrong configuration triggers automatic currency conversions that quietly drain margin on every single payout cycle.

This guide covers the Stripe settlement account alternative to bank UK businesses can use — what qualifies, how the regulatory framework works, which providers compare well, and how to configure your setup so GBP payouts arrive without conversion or delay.

Key Takeaways

Stripe supports GBP payouts to any account with a valid UK sort code and account number — including accounts issued by FCA-authorised EMIs, as stated in Stripe's payout documentation (accessed March 2026).

Stripe applies a currency conversion fee of approximately 2% for UK accounts when your payout currency doesn't match your connected account's currency — a recurring cost that compounds at scale.

FCA-authorised EMI accounts are required under Regulation 20 of the Electronic Money Regulations 2011 to safeguard client funds — meaning your balance is held separately from the EMI's own funds. This is a different protection model from FSCS coverage, with its own risk considerations.

Traditional UK banks reject or delay many offshore-incorporated companies, SaaS platforms, and e-commerce businesses — EMIs typically offer remote onboarding with faster approval timelines.

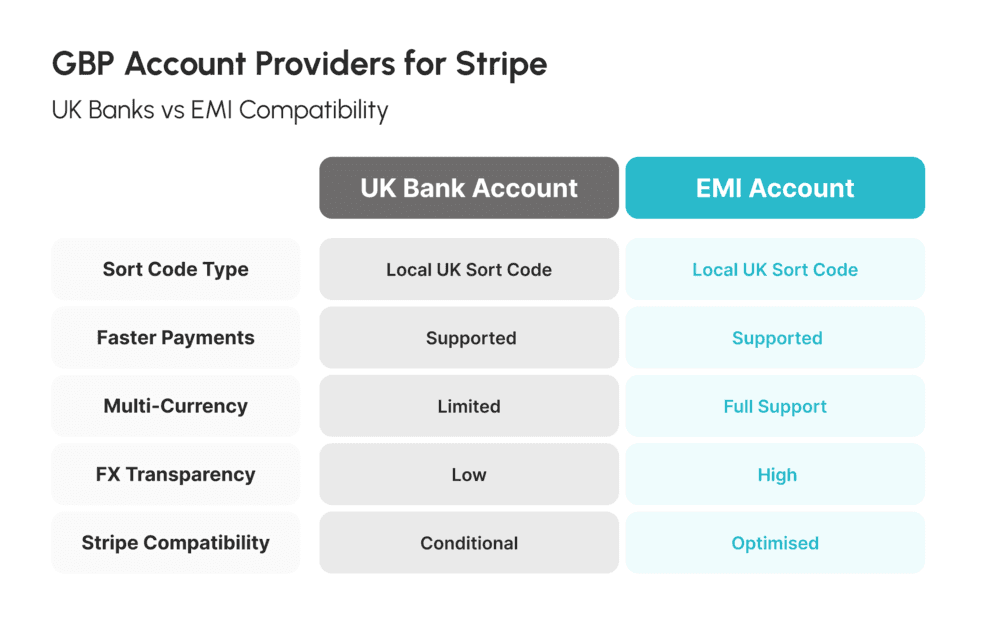

Multi-currency EMI accounts hold GBP, EUR, and USD in separate balances — eliminating automatic conversion until you choose to exchange.

Providers like Wise, Revolut Business, Airwallex, and Payoneer each serve different use cases. Choosing the wrong one introduces compatibility gaps, hidden FX costs, or payout limits.

What Is a Stripe Settlement Account Alternative to Bank UK Businesses Can Use?

What is an EMI account?

An Electronic Money Institution (EMI) is a financial provider authorised by the FCA to issue electronic money and provide payment accounts with UK sort codes — enabling businesses to send and receive payments without being a traditional deposit-taking bank. Authorised EMIs in the UK are regulated under the Electronic Money Regulations 2011 and listed on the FCA Register.

Stripe's payout documentation (March 2026) explicitly states that the platform supports payouts to "virtual bank accounts (such as N26, Revolut, and Wise)" alongside traditional bank accounts — provided those accounts hold valid local payment details in the settlement currency.

For UK GBP payouts, Stripe requires a sort code and account number capable of receiving funds via Faster Payments (FPS). FCA-authorised EMIs issue exactly this: a genuine UK sort code and account number assigned through the UK's domestic payment infrastructure.

Stripe treats an EMI-issued GBP account identically to a high-street bank account at the payout routing level.

The structural difference matters. EMIs are not authorised to accept deposits or lend money. Under Regulation 20 of the Electronic Money Regulations 2011, all authorised EMIs must safeguard funds received in exchange for e-money issued. As the FCA explains, client funds must be held separately from the EMI's own funds — via segregated accounts or insurance/guarantee methods.

This is a different protection model from the FSCS, which covers bank deposits up to £85,000. As English courts confirmed in Re Ipagoo LLP [2022] EWCA Civ 302, the EMRs do not impose a statutory trust over safeguarded funds — customers hold a priority claim over the safeguarded pool in insolvency, but recovery is not guaranteed. The FCA published CP24/20 in September 2024 proposing reforms toward a CASS-style regime, with interim rules taking effect through 2025–2026.

Bottom line: EMI accounts are Stripe-compatible, FCA-regulated, and widely used for UK GBP settlement. Understand the protection model before committing to a provider.

Why Businesses Look for a Stripe Settlement Account Alternative UK

This is not a niche problem. The friction is structural — and it hits multiple business types at once.

The Banking Wall

UK high-street banks require physical documentation, proof of UK premises, and often in-person verification. For businesses incorporated offshore — UAE, BVI, Cayman Islands — this process frequently ends in rejection. Even UK-incorporated companies with non-UK directors face due diligence timelines stretching weeks into months.

Delays in GBP accounts for non-UK companies are not an exception

Move to EQWIRE and take control of your payout speed and reliability.

EQWIRE's coverage of GBP accounts for non-UK companies shows this is a systemic pattern, not an edge case.

The Hidden Tax on Every Payout

Every forced FX conversion is a hidden tax on your revenue.

When your Stripe payout currency doesn't match your connected account's currency, Stripe converts automatically. According to Stripe's pricing page (March 2026), currency conversion fees for UK accounts run approximately 2% — applied whenever a mismatch exists.

On £60,000 of monthly GBP payout volume, that is £1,200 per month — £14,400 per year. Without visibility into the markup, you are paying a cost you never explicitly agreed to.

The Single-Currency Trap

Standard UK bank accounts are single-currency by design. Businesses collecting GBP, EUR, and USD through Stripe need either multiple banking relationships or a multi-currency account. Most banks don't offer the latter to SMBs at a practical level — so multi-currency revenue gets collapsed into one currency at whatever rate applies at settlement.

No API Access

Traditional banks rarely provide API access to e-commerce or SaaS businesses at a usable level. EMI providers are built for exactly this.

Bottom line: Delayed onboarding, forced FX conversion, currency consolidation, and no API access are the four structural problems EMI accounts solve. Each one is avoidable.

How Stripe Payouts Work in the UK — and Where They Break Down

When a customer pays through Stripe, funds land in your Stripe balance. On your chosen schedule — daily, weekly, or manual — Stripe initiates a transfer to your connected account via Faster Payments using your sort code. Funds typically arrive within hours.

Stripe's documentation is explicit: payments presented in a currency without a matching configured account "automatically convert to your default currency" — at Stripe's rate, without prompting, on every affected payout cycle.

The three most common configuration failures are:

Currency mismatch — payout currency in Stripe settings doesn't match the connected account's currency → automatic conversion at ~2%

Invalid or FPS-incompatible sort code — payout fails and returns to your Stripe balance, delaying settlement

Verification failure — account documentation gaps block payouts until resolved

Stripe Connect / marketplace accounts: Payout routing for connected accounts follows different rules — platforms manage eligibility on behalf of their users.

Restricted industries: EMI account compatibility does not override Stripe's merchant eligibility requirements.

Bottom line: The mechanism is simple. The problems are almost always configuration errors — and all three are avoidable before they touch live cash flow.

Best Account to Receive Stripe Settlements GBP UK — Comparison of Options

Not all accounts are equal for Stripe GBP settlements. The table below reflects publicly available information as of March 2026 — verify current features directly with each provider before making decisions.

Provider | Account Type | UK Sort Code | Inbound FPS | Multi-Currency | Remote Onboarding | FX Transparency |

|---|---|---|---|---|---|---|

Traditional UK Bank (e.g. Barclays, HSBC) | Deposit-taking bank | ✅ | ✅ | Limited | ❌ Often in-person | Low |

Wise Business | EMI (FCA-authorised) | ✅ | ✅ | ✅ 40+ currencies | ✅ | High — publishes mid-market rate |

Revolut Business | EMI (FCA-authorised) | ✅ | ✅ | ✅ | ✅ | Medium — markup applies off-hours |

Airwallex | EMI / Payment Institution | ✅ | ✅ | ✅ | ✅ | Medium |

Payoneer | Stored value account | ✅ Receiving only | Limited — verify before use | ✅ | ✅ | Low–Medium |

EMI (FCA-authorised, FRN 901100) | ✅ | ✅ | ✅ GBP, EUR, USD | ✅ | Transparent |

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

What the table doesn't show:

Wise Business is the most FX-transparent option — it publishes its exact markup above mid-market rate and is widely used for Stripe GBP payouts. Limitation: scope. Wise is an FX and payments tool, not a full payment operations infrastructure.

Revolut Business works well for multi-currency holding and basic API access. FX markups apply outside business hours and account limits vary by subscription tier.

Airwallex suits high-volume e-commerce and SaaS businesses with programmatic payment requirements. Its API infrastructure is robust at scale.

Payoneer is primarily designed for freelancers and marketplace payouts — its GBP account focuses on receiving, not outbound operations. Stripe compatibility varies by region; verify before relying on it for primary settlement.

EQWIRE provides GBP, EUR, and USD balances with a genuine UK sort code, inbound FPS, and SWIFT/SEPA connectivity. It is an FCA-authorised EMI (FRN 901100) subject to safeguarding requirements under the Electronic Money Regulations 2011.

Bottom line: Wise leads on FX transparency. Airwallex leads on API infrastructure. Full EMIs like EQWIRE lead on complete multi-currency payout operations. Match the provider to your use case — not just the lowest listed fee.

EMI Account for Stripe Settlement GBP UK Multi-Currency — How It Works

Multi-currency holding is the feature most businesses underestimate — until they run the numbers.

A multi-currency EMI account holds GBP, EUR, and USD in separate balances. GBP payouts from Stripe land in your GBP balance via Faster Payments. EUR and USD sit separately. No automatic conversion. No silent FX charge. No loss of control over timing.

For e-commerce businesses, this means receiving GBP from Stripe and paying UK suppliers directly in GBP — while holding EUR to pay EU-based suppliers via SEPA, converting only when the rate is right. For SaaS businesses, it means collecting multi-currency subscription revenue in separate balances rather than collapsing everything into GBP at Stripe's settlement rate — and deploying foreign currency directly to international contractors without an unnecessary conversion step.

For context on structuring GBP payment flows as a non-UK or offshore entity, see GBP Faster Payments for Offshore Companies: Same-Day Settlement Guide and How to Pay UK Suppliers from a UAE Business Account.

Receive Stripe GBP Payouts Without a UK Bank Account

EQWIRE provides FCA-authorised GBP accounts with genuine UK sort codes, Faster Payments support, and multi-currency balances — built for businesses that need operational flexibility without traditional banking barriers.

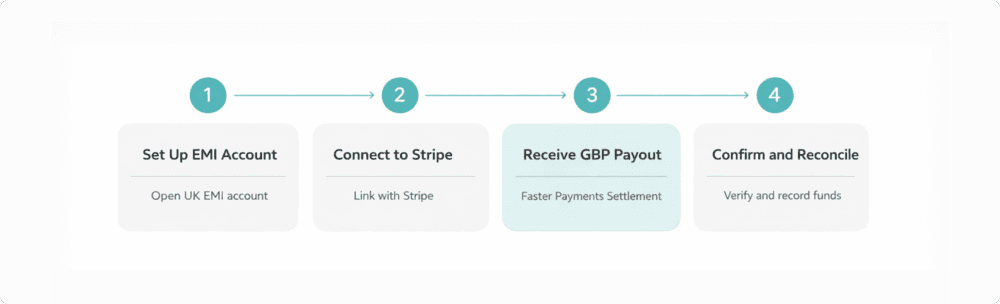

Step-by-Step: Route Stripe Settlement into a Multi-Currency EMI Account UK

Follow these four steps in order. Step 2 (documentation) and Step 3 (currency setting) are where most businesses make costly mistakes.

Step 1 — Select and verify your EMI provider

Confirm the provider holds full FCA authorisation at register.fca.org.uk. Verify two things before applying: (a) the account issues a genuine UK sort code — not a GB-prefixed IBAN routed through a foreign institution — and (b) it explicitly supports inbound Faster Payments. Have your documentation ready upfront: certificate of incorporation, director and UBO identification, proof of business address, and a business activity description. Incomplete submissions are the primary cause of onboarding delays.

Step 2 — Test your GBP account before connecting to Stripe

Once your GBP account is issued, send a small test transfer from a separate account and confirm it arrives correctly. Then navigate to Stripe Dashboard: Settings → Bank Accounts and Scheduling → Add bank account. Enter your EMI-issued sort code and account number. Stripe may initiate a small verification deposit — confirm receipt before proceeding.

Step 3 — Set payout currency explicitly to GBP

This is the step most businesses miss. In Stripe payout settings, set GBP as the payout currency for this specific account. Per Stripe's documentation, payments not matched to a configured currency account convert automatically. A wrong setting here means paying Stripe's ~2% conversion fee on every payout.

Step 4 — Activate additional currency accounts and confirm a full cycle

If your EMI supports EUR and USD balances, activate these and add them as separate Stripe payout accounts for the corresponding currencies — enabling full multi-currency routing without conversion. Run a complete payout cycle and verify the GBP amount in your EMI account matches your Stripe dashboard exactly before scaling volume.

Common Mistakes When Choosing a Stripe Payout Account

These are not theoretical edge cases. They are the mistakes that cause delayed settlements and unexpected FX costs.

Confusing a virtual IBAN for a genuine UK sort code

Some providers issue IBANs routed through European infrastructure — not a native UK sort code. A genuine UK sort code is in the format XX-XX-XX and registered in the UK domestic payment infrastructure. Verify explicitly with your provider.

Ignoring the payout currency setting in Stripe

If your Stripe payout currency is GBP but your connected account is EUR-denominated, Stripe converts automatically at approximately 2%. Match currencies exactly before going live.

Choosing a provider based on advertised fee alone

A low-fee EMI that fails Stripe's sort code verification or offers opaque FX pricing costs far more in friction than the saving justifies. Evaluate compatibility and transparency alongside pricing.

Underestimating KYC requirements

EMIs must conduct thorough FCA-mandated KYC and AML screening. Missing UBO documentation or incomplete business descriptions are the primary cause of onboarding delays — prepare everything before you start.

Not verifying jurisdiction eligibility before applying

Eligibility varies by country of incorporation. A provider that accepts UAE entities may not accept BVI or Cayman companies. Check before applying.

Skipping the test payout

Always run a small test before routing live volume. Configuration errors caught early cost nothing. Caught after the fact, they delay settlements and cost real money.

Bottom line: Most payout problems trace back to one of these six mistakes. None requires expertise to avoid — just checking before you go live.

Conclusion

For UK e-commerce and SaaS businesses, a Stripe settlement account alternative to bank UK is a fully regulated, operationally superior option for most businesses facing barriers to traditional banking or needing genuine multi-currency flexibility.

Stripe's own documentation confirms it supports EMI and virtual accounts. The FCA confirms that authorised EMIs must hold client funds separately from their own capital under Regulation 20 of the Electronic Money Regulations 2011 — a different model from FSCS coverage, with its own risk considerations worth understanding before choosing a provider.

The pricing case is equally clear: Stripe's ~2% conversion fee on mismatched payouts costs over £14,000 per year on £60,000 of monthly GBP volume. The right account infrastructure eliminates that cost, accelerates settlement, and scales with your revenue rather than working against it. Every unnecessary conversion is margin you are handing back — and it takes days, not months, to stop it.

FAQ

What is the best alternative to a UK bank for receiving Stripe GBP settlements?

An FCA-authorised EMI account with a genuine UK sort code and inbound Faster Payments support is the most practical regulated option. The best provider depends on your use case — Wise leads on FX transparency, Airwallex on API infrastructure, and full EMIs like EQWIRE on complete multi-currency payout operations.

How do I receive Stripe payouts without a traditional UK bank account?

Open an account with an FCA-authorised UK EMI, obtain your GBP sort code and account number, add those details to Stripe under Settings → Bank Accounts and Scheduling, and set your payout currency explicitly to GBP. As confirmed in Stripe's payout documentation, Stripe supports virtual and EMI accounts provided they hold valid UK payment details and match the configured payout currency.

Can I receive Stripe payouts into a UK EMI account?

Yes, in most standard configurations. Stripe explicitly names EMI-type accounts — including Revolut and Wise — as supported for payouts, provided the account holds a valid UK sort code and supports inbound Faster Payments. Businesses in restricted industries or using Stripe Connect should check Stripe's restricted businesses guidance separately.

Why does Stripe convert GBP to EUR, and how can I stop it?

Stripe converts automatically when your payout currency setting doesn't match your connected account's currency. To stop it, set your Stripe payout currency explicitly to GBP and connect a GBP-denominated account with a genuine UK sort code — a multi-currency EMI account then holds each balance separately so you control when any conversion occurs.

What is the difference between an EMI account and a UK bank account for Stripe payouts — and is an EMI account safe?

For Stripe routing, the functional difference is minimal — both use a UK sort code for Faster Payments settlement. The key distinction is protection: under Regulation 20 of the Electronic Money Regulations 2011, EMIs must hold client funds separately from their own — a different model from FSCS bank deposit protection, with its own risk considerations that businesses should review before committing to a provider.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)