•

•

IBAN Validator Tool: Check Your EUR IBAN Before Sending a SEPA Payment

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A single wrong character in a EUR IBAN can route a SEPA payment to the wrong bank or bounce it back several days later. For finance teams paying suppliers across the eurozone, that turns into a late invoice, a chased refund, and an awkward call with the beneficiary. An IBAN validator tool checks a EUR IBAN for SEPA payment errors in seconds, before any money leaves the account. This guide explains what such a tool actually checks, how the MOD-97 algorithm catches typos, and the one thing validation can never confirm on its own. It also covers Verification of Payee, the name-matching step that became mandatory for euro payments in October 2025.

[aa key-takeaways]

Key Takeaways

An IBAN validator confirms a EUR IBAN's country, length, format, and check digits before a SEPA payment leaves the account.

The MOD-97 algorithm (ISO 7064) catches more than 98% of single-character typos and almost all transposed digits.

A structurally valid IBAN is not proof that the account exists or belongs to the intended payee.

Verification of Payee adds a beneficiary-name check and has been mandatory for euro SEPA transfers since 9 October 2025.

Validation belongs at the start of the payment workflow, where fixing an error costs minutes instead of days.

[aa btn]Book a Call[/aa]

[/aa]

What Is an IBAN Validator Tool?

An IBAN validator tool is software that checks whether an International Bank Account Number is correctly formed before a payment is sent. It confirms the IBAN follows the rules set by the ISO 13616 standard: the right country code, the right length, and check digits that add up. For a business about to send a EUR SEPA payment, that check runs in seconds and catches the errors behind most failed transfers.

A validator typically reports four things at once:

The country the IBAN belongs to, read from the first two letters

Whether the length matches that country's fixed format

Whether the check digits pass the mathematical test

The bank and branch the account sits with, where the data is available

Most online checkers are free and require no login. A finance manager can paste a supplier's EUR IBAN into an EUR IBAN checker, read the result, and correct a typo before it ever reaches the payment file.

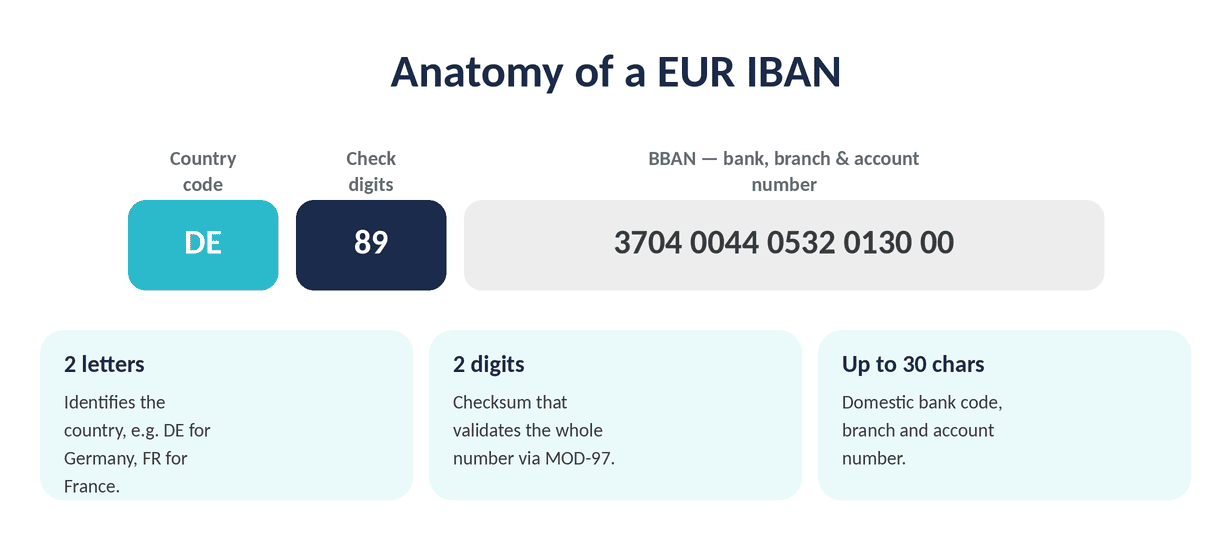

IBAN Structure: Country Code, Check Digits, and BBAN

Every IBAN follows the same template. The first two letters are the country code, such as DE for Germany or FR for France. The next two characters are the check digits, a built-in test value calculated from the rest of the number. Everything after that is the BBAN (Basic Bank Account Number), which holds the domestic bank code, branch code, and account number in a layout each country sets for itself.

The full IBAN can run up to 34 characters. That fixed structure is what lets a validator inspect any IBAN from any SEPA country using one consistent set of rules.

What "EUR IBAN" and SEPA Mean in Practice

A EUR IBAN is an account number at a bank or electronic money institution that can receive euros over the SEPA network. SEPA, the Single Euro Payments Area, covers more than 30 European countries and standardises euro transfers so a payment to Lisbon clears the same way as one to Berlin. The European Central Bank oversees how the area operates.

Businesses that check EUR IBAN before SEPA payment details go out avoid the most frequent reason transfers fail: a beneficiary number entered or copied incorrectly. The check is cheap. The failure is not.

How an IBAN Validator Checks a EUR IBAN

An IBAN validator runs four tests in order: the country code, the total length, the character format, and the MOD-97 check digits. An IBAN that passes all four is structurally valid and safe to place in a payment file. One that fails any test is flagged before it can cause a returned payment.

Format and Length per Country

IBAN length is fixed for each country. A German IBAN is 22 characters, a French IBAN is 27, a Spanish IBAN is 24, and a Dutch IBAN is 18. A validator compares the entered IBAN against the registered length for its country code, so a German IBAN with only 21 characters fails on the spot. These lengths come from the ISO 13616 standard and the national registries that sit under it.

This single check removes a common error: a digit dropped while retyping an IBAN from an emailed invoice.

The MOD-97 Check-Digit Test

The core of IBAN validation is a checksum defined by ISO 7064, known as MOD-97. The test runs in three steps:

Move the first four characters (the country code plus the two check digits) to the end of the string.

Replace every letter with two digits, where A becomes 10 and the sequence runs through to Z as 35.

Divide the resulting number by 97. A remainder of exactly 1 means the IBAN is valid.

A short worked example shows why it is reliable. Take the German sample IBAN DE89 3704 0044 0532 0130 00. Moving DE89 to the end, converting D to 13 and E to 14, and dividing the resulting number by 97 leaves a remainder of 1, so the IBAN passes. Drop or swap any single digit and the remainder stops equalling 1, which is the error a validator reports.

Because the check digits are calculated from the whole account number, any change to one character changes the result. That is why a validator can spot an error without ever contacting a bank.

[aa fast-fact]

Fast Fact: The MOD-97 checksum catches more than 98% of single-character errors and almost every case where two adjacent digits are swapped.

[/aa]

BIC and Bank Identification

Beyond the checksum, most tools read the bank code held inside the BBAN and return the matching BIC (Bank Identifier Code), the SWIFT code that identifies the recipient bank and branch. Confirming the BIC alongside a valid IBAN helps route a SEPA Credit Transfer (SCT) to the correct institution.

For a business that wants to validate IBAN for a SEPA transfer at scale, the BIC lookup also flags when an account sits with a provider that cannot receive euro payments, which a plain format check would miss.

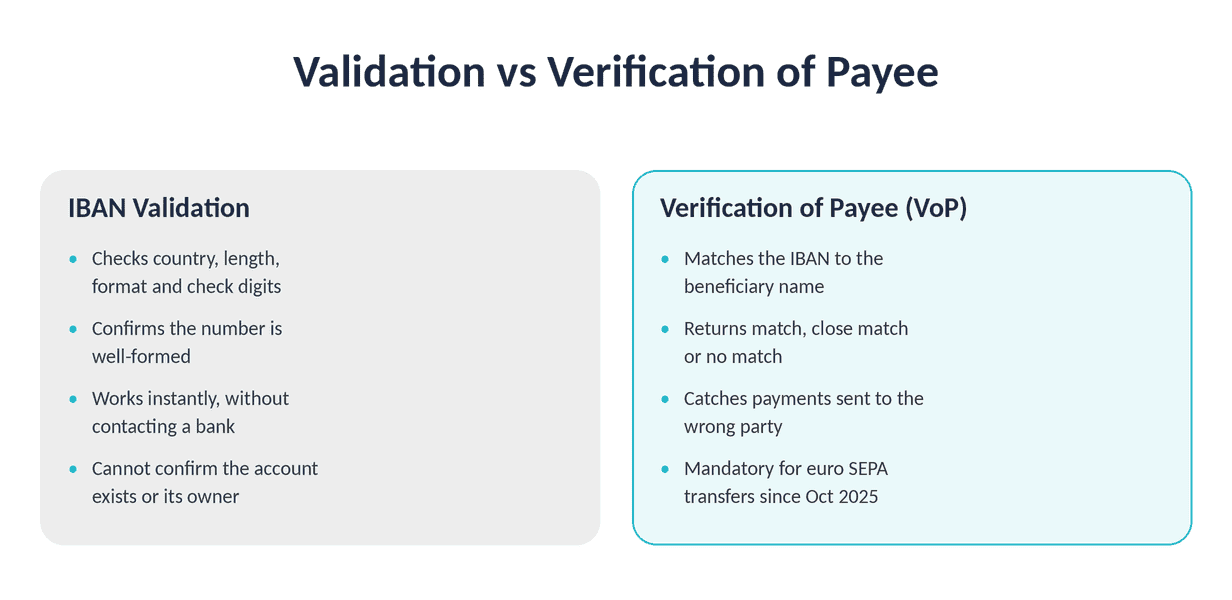

What an IBAN Validator Does Not Confirm

A valid IBAN is not proof that the account exists or that it belongs to the intended payee. Validation confirms the number is well-formed. It says nothing about who sits behind it at the other end.

Validity, Existence, and Ownership

There are three separate questions a payer needs answered, and a format check only answers one.

Validity means the IBAN passes the format, length, and checksum tests.

Existence means a real, open account sits behind the number.

Ownership means that account belongs to the supplier named on the invoice.

A free online checker confirms validity. It cannot see inside the receiving bank, so it cannot confirm existence or ownership. An IBAN can be perfectly valid and still point to the wrong company, which is exactly how invoice-redirection fraud succeeds.

Where Verification of Payee Comes In

Verification of Payee (VoP) closes the ownership gap. Before a euro payment is sent, the payer's provider passes the beneficiary IBAN and name to the payee's provider, which replies with a match, a close match, or no match. The payer then decides whether to release the transfer. The scheme is run by the European Payments Council.

The response is not a simple yes or no. A close match flags a small difference, such as a trading name set against a registered company name, and leaves the final call with the payer. A no match is a clear signal to pause and confirm details with the supplier before releasing funds. For finance teams, that converts a silent risk into a visible checkpoint inside the payment screen.

Under the EU Instant Payments Regulation, VoP became mandatory for euro SEPA Credit Transfers and SEPA Instant payments on 9 October 2025. The United Kingdom runs a comparable check called Confirmation of Payee (CoP). Both add the name match that an IBAN validator on its own can never provide, and the European Banking Authority supervises how providers apply the rules.

[aa cta]

Send EUR Payments With Fewer Failed Transfers

EQWIRE's multi-currency accounts let businesses hold and send euros, with beneficiary checks built into the payment flow before a SEPA transfer goes out.

[aa btn]Create Account[/aa]

[/aa]

Why This Matters for EUR SEPA Payments Specifically

A misrouted EUR SEPA payment is slow and awkward to recover. SEPA Credit Transfers usually settle the same day or the next business day, and SEPA Instant settles in under 10 seconds for amounts up to €100,000. Once funds land in a valid but incorrect account, recovery depends on a stranger's bank agreeing to return them, and there is no guarantee it will.

The cost is rarely just the payment. A returned transfer delays the supplier, triggers a second payment run, and ties up a finance team in reconciliation work. Industry coverage from outlets such as Finextra has tracked how name-matching checks were introduced specifically to cut this kind of misdirected-payment loss across the euro area.

Consider a UK importer paying a German supplier €18,000 over SEPA. An accounts clerk copies the IBAN from a PDF invoice and drops one digit while retyping it. The number still looks plausible, yet it fails the MOD-97 check the moment it is pasted into a validator. The clerk fixes the digit, the payment clears the next business day, and the supplier ships on schedule. Skip that check and the transfer either bounces after two days or settles into a valid but unrelated account.

A free IBAN validation tool for businesses checking EUR IBANs before sending SEPA transfers removes the most common cause of these failures at the point of entry. It is the cheapest control in the whole payment chain.

For businesses comparing where to hold euros, the choice of provider shapes how easy these checks are. A regulated EUR business account for international payments can validate beneficiaries inside the payment screen, rather than leaving staff to paste numbers into a separate website. The same applies when weighing how an FCA-regulated EMI handles EUR and GBP against a high-street bank. Teams running higher volumes can go further by automating multi-currency settlement so validation and reconciliation happen without manual steps.

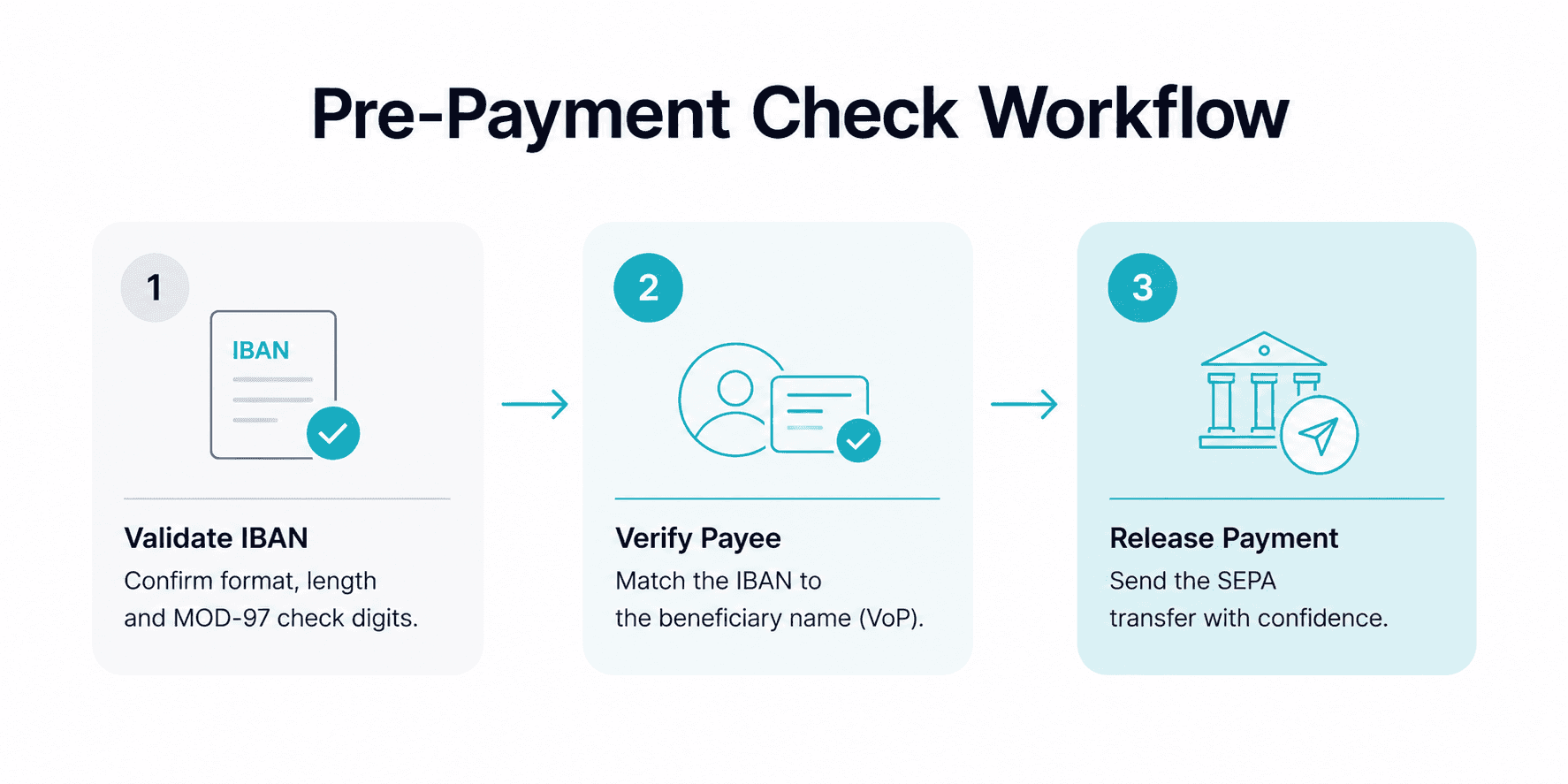

Where IBAN Validation Fits in the Payment Workflow

Validation works best as the first gate in the payment process. For a single payment, a finance manager checks the IBAN before saving the beneficiary. For a payment run, the same logic applies in bulk, where many teams validate every IBAN in a file before uploading it, so fifty euro payments are screened in one pass instead of failing one transfer at a time.

The order matters. A format check comes first and is instant. Verification of Payee follows and confirms the name behind a valid number. Running both before release means an error costs seconds at the desk rather than days in recovery. That sequence is also what turns a manual habit into a repeatable control a finance team can audit.

FAQ

How does a free IBAN validation tool for businesses check EUR IBANs before sending SEPA transfers?

A free IBAN validation tool checks the country code, length, character format, and MOD-97 check digits of each EUR IBAN, then reports whether the number is structurally valid. Most tools also return the BIC and bank name read from the IBAN. The check happens locally against the ISO 13616 rules, so it works without contacting the receiving bank and takes only a second per IBAN.

Is there a way to validate an IBAN with a SEPA payment tool online?

Yes. To validate an IBAN with a SEPA payment tool online, a business pastes the beneficiary IBAN into the checker, which confirms the format and check digits and identifies the bank. This catches typos and transposed digits before the IBAN enters a payment file. For confirmation that the account belongs to the right payee, the business still needs Verification of Payee, which a format-only validator does not perform.

Can a valid IBAN still be the wrong account?

Yes. A valid IBAN only proves the number is correctly structured and passes the checksum. It does not prove the account exists or belongs to the intended supplier. An IBAN can be valid and still point to a different company, which is how invoice-redirection fraud works. Verification of Payee, mandatory for euro SEPA transfers since October 2025, adds the beneficiary-name check that closes this gap.

What is the difference between IBAN validation and Verification of Payee?

IBAN validation checks that the account number is correctly formatted using the ISO 13616 standard and the MOD-97 checksum. Verification of Payee checks that the IBAN and the beneficiary name belong to the same account holder. Validation prevents formatting errors. Verification of Payee prevents paying the wrong party. A complete pre-payment check uses both.

Does an IBAN checker confirm the recipient's bank?

An IBAN checker identifies the recipient's bank by reading the bank code inside the BBAN and returning the matching BIC. That confirms which institution the IBAN routes to, which helps a SEPA Credit Transfer reach the correct bank. It does not confirm the individual account holder, so an EUR IBAN checker is best used alongside a name-matching step.

EUR payments fail most often for one preventable reason: a beneficiary number entered incorrectly. An IBAN validator tool removes that risk in seconds by confirming a EUR IBAN is well-formed before a SEPA payment is sent, and Verification of Payee now adds the name match that validation alone cannot give. Used together at the start of the payment workflow, the two checks turn a costly multi-day recovery into a one-second correction. For finance teams sending regular euro payments, holding funds with a regulated provider that builds these checks into the payment screen keeps suppliers paid on time. EQWIRE's multi-currency accounts are built for exactly that. Businesses can open an account at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)