•

•

Revolut Business vs EMI Account: Key Differences for International SMEs

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Most comparisons treat Revolut Business and an EMI account as two different products. They are not. Revolut Business has always run on an electronic money institution (EMI) model, so for an international SME weighing Revolut Business vs an EMI account for GBP and EUR, the real choice is between a bundled fintech platform and a dedicated FCA-authorised EMI account. That distinction decides three things that matter to a growing company: which businesses get accepted, how foreign exchange is priced, and how client funds are protected. This guide sets out the difference between Revolut Business and an EMI account so finance decision-makers can match the right multi-currency business account for GBP and EUR to their company structure.

[aa key-takeaways]

Key Takeaways

Revolut Business and a standalone EMI account both operate as electronic money products, so neither sits on the same footing as a traditional current account by default.

Fund protection runs through safeguarding, not the Financial Services Compensation Scheme (FSCS), for any money held on an e-money entity.

Revolut Business bundles cards, expense tools and a monthly no-fee FX allowance; a dedicated EMI focuses on named GBP and EUR account details plus direct payment rails.

Eligibility is the most common dividing line, and non-UK or offshore-registered companies are where applications most often stall.

Company structure and FX volume usually settle the decision more than feature lists do.

[aa btn]Book a Call[/aa]

[/aa]

Revolut Business vs EMI Account at a Glance

The main difference between Revolut Business and a dedicated EMI account is scope: Revolut Business is a broad financial platform built around bundled tools, while a dedicated FCA-authorised EMI account concentrates on multi-currency accounts, named GBP and EUR details, and cross-border payment rails. Both are regulated as electronic money institutions, and both let an international SME hold and move several currencies from one place.

An EMI account for international SMEs is a payment account provided by an electronic money institution rather than a bank. The provider issues e-money against deposited funds, supplies account details and access to payment rails such as Faster Payments for GBP, and safeguards the balance under regulatory rules. It supports day-to-day receiving, holding and sending across currencies, without offering the lending or interest-bearing deposit products that define a traditional bank. For most companies focused on cross-border collection and payment, that distinction has little operational effect.

The table below compares the two models on the points that change an SME decision.

Side-by-Side Comparison Table

Feature | Revolut Business | Dedicated FCA-authorised EMI account |

|---|---|---|

Regulatory model | E-money (EMI), with retail migration to a UK bank entity underway in 2026 | Electronic money institution (e-money) |

Fund protection | Safeguarding (FSCS only once a customer sits on the bank entity) | Safeguarding under the Electronic Money Regulations 2011 |

Primary focus | Bundled platform: cards, expense management, FX allowance | Multi-currency accounts, named GBP/EUR details, payment rails |

GBP and EUR access | Local GBP and EUR details on supported plans | Named GBP and EUR account details and IBANs |

FX pricing | No-fee monthly allowance, then a percentage fee above it | Flat published spread on conversions |

Payment rails | Faster Payments, SEPA, SWIFT | Faster Payments (FPS), SEPA, SWIFT, BACS, CHAPS |

Best suited to | UK-based SMEs wanting an all-in-one app | International and non-UK companies needing dependable rails |

A UK software company billing clients across the EU often does well on a bundled platform. A holding company registered outside the UK, by contrast, tends to care far more about acceptance and account details than about expense cards. The model has to fit the company, which is why the next section breaks down the three differences that actually move the decision.

[aa cta]

Need GBP and EUR Details That Accept Your Structure?

EQWIRE is an FCA-authorised EMI offering multi-currency accounts for international and non-UK companies, with named GBP and EUR details from day one.

[aa btn]Open an Account[/aa]

[/aa]

The Differences That Change the Decision

Three factors separate Revolut Business from a dedicated EMI account in practice: who gets accepted, what foreign exchange costs once volumes rise, and how money is protected if a provider fails. Each one affects a different type of international SME.

Eligibility and Accepted Company Types

Eligibility is the first wall many applicants hit. Revolut Business for a non-UK company is possible in several markets, yet acceptance depends heavily on where the company is registered, the nature of its activity, and its ownership chain. Companies tied to higher-risk jurisdictions or complex structures see the most friction.

A dedicated EMI account for international SMEs is often built around exactly these cases, with onboarding teams that expect cross-border ownership. The trade-off is documentation. Offshore companies face additional AML checks when opening UK accounts, regardless of provider.

Applications most often stall on:

Registration in a jurisdiction outside the provider's accepted list

Beneficial owners spread across multiple countries

Business activity that falls into a restricted category

Thin documentation on the source of funds

In practice, a consultancy incorporated in a low-tax jurisdiction but operating from the EU will often pass identity checks yet stall on the source-of-funds review. The fix is rarely a different provider. It is a cleaner evidence pack: incorporation documents, a clear ownership chart, and contracts or invoices that explain where revenue comes from. Providers that specialise in international SMEs tend to signal their accepted jurisdictions and required documents upfront, which shortens the back-and-forth and lowers the chance of a late rejection.

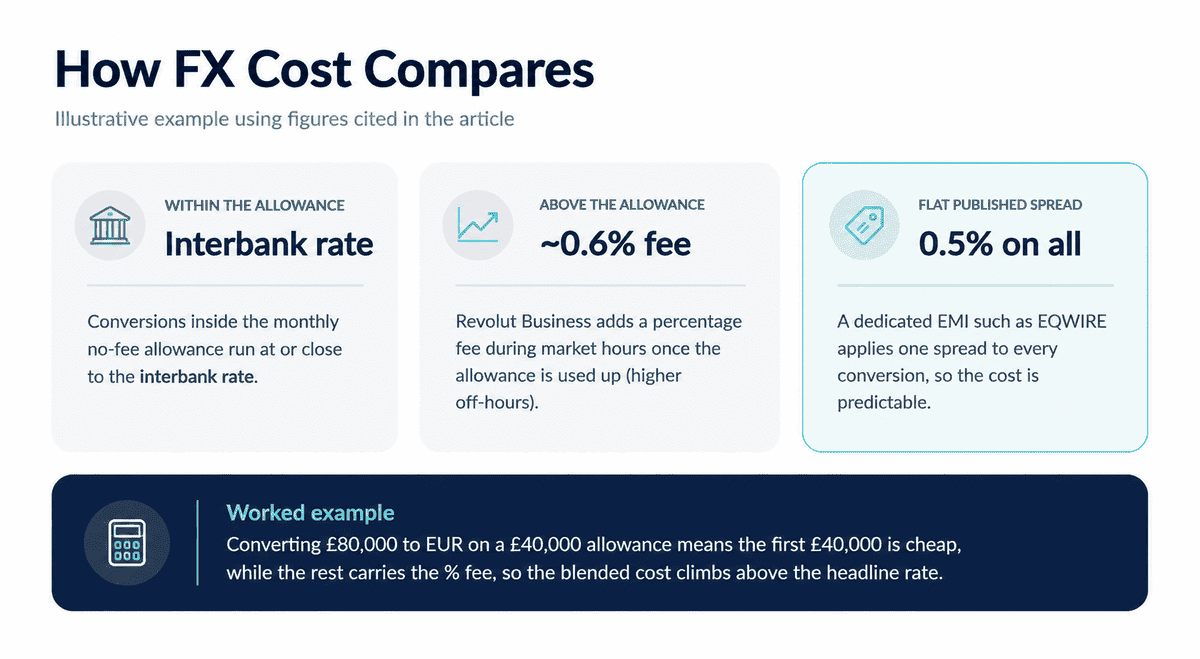

FX Pricing and the Allowance Ceiling

Revolut Business prices foreign exchange through a monthly no-fee FX allowance set by plan. Conversions within that allowance run at or close to the interbank rate. Above it, a percentage fee applies, reported at around 0.6% during market hours and higher outside them, according to Revolut's 2026 pricing pages. A dedicated EMI account for international SMEs more often applies a single published spread on every conversion, such as EQWIRE's 0.5%.

The two models suit different volumes. A worked example shows why.

Consider a company converting £80,000 into euros each month on a plan with a £40,000 allowance. The first £40,000 converts cheaply. The remaining £40,000 carries the percentage fee, so the blended cost climbs well above the headline rate. A flat-spread account charges the same rate on the full £80,000, which becomes more predictable once monthly conversions consistently exceed the allowance.

Seasonality complicates the picture further. A business that stays within its allowance for most of the year, then spikes during a peak quarter, pays the percentage fee exactly when cash flow is tightest. Forecasting that cost is harder than applying one published spread to every conversion. Businesses comparing EMI accounts typically model a low month and a peak month side by side, rather than relying on an annual average, before settling on a pricing model.

[aa fast-fact]

Fast Fact: Incoming transfers in GBP, EUR, USD and CHF are typically free on Revolut Business, so the cost question centres on conversions and outbound transfers rather than receipts.

[/aa]

Fund Protection and Safeguarding

Neither Revolut Business nor a standalone EMI account is FSCS-protected by default; both safeguard client funds under the Electronic Money Regulations 2011. Safeguarding means customer money is held in segregated accounts at a credit institution or invested in secure liquid assets, kept apart from the provider's own funds and returned ahead of general creditors if the firm fails. The FSCS, by contrast, covers eligible deposits held with an authorised bank.

A 2026 nuance matters here. Revolut Bank UK Ltd exited its mobilisation phase and launched as a full UK bank in March 2026, with bank deposits covered by FSCS, as reported by Reuters. Yet customers onboarded from that point may still sit on the e-money entity, Revolut Ltd, with migration to the bank handled gradually. FSCS protection attaches only once an account sits on the bank entity, so a business should confirm which entity holds its money rather than assume bank-grade cover.

A dedicated FCA-authorised EMI account removes that ambiguity. Funds stay safeguarded as e-money throughout, with the protection model stated plainly in the account terms. EQWIRE, for instance, is an FCA-authorised EMI (firm reference number 901100) that holds client money in segregated safeguarding accounts, so the basis of protection does not shift with a migration timetable.

For an international SME, the practical question is less about which scheme sounds stronger and more about certainty. Safeguarding and FSCS protect money through different mechanisms, and the right answer depends on the entity named in the account documentation. A finance team that records which legal entity holds its balance, and on what basis, removes the main source of confusion in this comparison.

Which One Fits Your Company Profile

The clearest way to choose is to match each model to a company profile. Four profiles cover most international SMEs.

UK-registered SME with Moderate FX

A UK company with straightforward ownership and conversions that stay within a monthly allowance usually fits Revolut Business well. The bundled cards, expense controls and team permissions add day-to-day value, and the FX allowance keeps conversion costs low at that scale.

Non-UK Company Needing GBP and EUR Details

A company registered outside the UK that needs dependable GBP and EUR account details often finds a dedicated EMI a stronger match. Even a non-UK entity can still access UK and EU rails through an FCA-authorised provider that expects cross-border applicants. Named account details in both currencies let the company invoice and get paid like a local counterpart.

Offshore or Holding Structure

For founders asking the practical version of the question, Revolut Business vs FCA EMI account: which works for offshore and non-UK registered companies, the answer turns on acceptance and consistency. Offshore and holding structures are precisely where bundled platforms apply the tightest eligibility filters, and where a dedicated EMI that underwrites complex ownership tends to provide a more stable home for funds. A Revolut Business alternative for an international company under UK FCA EMI rules is worth shortlisting when structure is the obstacle.

High-volume Cross-border Payer

A company moving large, regular volumes across currencies should model FX cost first. Once conversions routinely exceed any allowance, a flat published spread becomes easier to forecast. Firms managing several currencies at once, such as import-export businesses, often value predictable pricing and direct SEPA and Faster Payments access over bundled software.

A Simple Decision Framework

A short set of if-then rules turns the comparison into a decision. If the company is UK-registered with simple ownership and modest FX, a bundled platform such as Revolut Business is a reasonable default. If the company is registered outside the UK or has an offshore or holding structure, a dedicated FCA-authorised EMI account usually clears onboarding more reliably. If monthly conversions consistently exceed any no-fee allowance, a flat spread is easier to budget. If fund-protection clarity is a priority, confirm which legal entity holds the money before committing.

That last point is where the Revolut Business vs EMI account international SME GBP EUR question becomes concrete rather than theoretical. Before opening any account, a finance team should read how an FCA-authorised EMI protects client funds and check it against the provider's stated entity and terms. The same trade-off appears when comparing Wise Business with a dedicated FCA EMI account, so the framework applies well beyond a single brand.

[aa cta]

Compare on Your Own Terms

Open a multi-currency account built for international SMEs, with named GBP and EUR details and a published FX spread.

[aa btn]Get Started[/aa]

[/aa]

FAQ

What is the difference between Revolut Business and an EMI account?

The difference between Revolut Business and an EMI account is mainly one of framing, because Revolut Business is itself built on an electronic money institution model. The practical contrast is between a bundled platform that adds cards and expense tools and a dedicated FCA-authorised EMI account that concentrates on multi-currency accounts, named GBP and EUR details, and direct payment rails. Both safeguard client money rather than relying on FSCS by default.

Is there a Revolut Business alternative for an international company under UK FCA EMI rules?

Yes. Several FCA-authorised electronic money institutions offer multi-currency business accounts that serve as a Revolut Business alternative for an international company under UK FCA EMI rules. These providers supply named GBP and EUR account details, SEPA and Faster Payments access, and onboarding teams that expect cross-border ownership. The main checks to run are accepted jurisdictions, the published FX spread, and the safeguarding arrangement.

Can a non-UK registered company open Revolut Business?

A non-UK registered company can open Revolut Business in several markets, though acceptance depends on the country of registration, the business activity, and the ownership structure. Companies with offshore or multi-jurisdiction ownership see the most friction and the highest rejection rates. Where eligibility is the obstacle, a dedicated EMI that underwrites complex structures is often the more dependable route.

Revolut Business vs FCA EMI account: which works for offshore and non-UK registered companies?

For offshore and non-UK registered companies, a dedicated FCA-authorised EMI account generally works more reliably than Revolut Business, because acceptance is the deciding factor. Bundled platforms apply tight eligibility filters to complex structures, while specialist EMIs build onboarding around cross-border ownership. Documentation requirements still apply, including source-of-funds evidence and AML checks, regardless of which provider a company chooses.

Which is cheaper for GBP to EUR transfers?

Cost depends on volume. Revolut Business is cheaper for GBP to EUR conversions that stay within its monthly no-fee allowance, while a flat-spread EMI account becomes cheaper once conversions consistently exceed that allowance. A company should estimate its monthly conversion volume, compare it against the allowance, and add any percentage fee that applies above the threshold before deciding.

Choosing between Revolut Business and a dedicated EMI account comes down to fit rather than a single winner. UK-based SMEs with modest FX often gain from a bundled platform, while international, offshore and high-volume companies tend to value broad eligibility, named GBP and EUR account details, and predictable FX pricing. The Revolut Business vs EMI account international SME GBP EUR decision rewards companies that match the model to their structure and confirm how their funds are protected. EQWIRE, an FCA-authorised electronic money institution, offers multi-currency accounts designed for exactly these cross-border cases, and businesses can review the options and open an account at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)