•

•

Webhook Integration for Payment Reconciliation: Automating Multi-Currency Settlements

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

SaaS platforms that process payments across multiple currencies face a reconciliation problem that compounds with every new market they enter. Connecting a payment provider's API confirms that a transaction was submitted. It says nothing about when it settled, at what exchange rate, or whether the funds landed in the right account. That gap between payment initiation and confirmed settlement is where manual work accumulates. Webhook integration payment reconciliation multi-currency settlement UK EMI infrastructure closes that gap by pushing signed event notifications the moment each state change occurs — replacing end-of-day batch exports with a continuous, transaction-level data feed. This article explains how SaaS platform builders can use EMI webhook infrastructure to design automated reconciliation across GBP, EUR, and USD payment streams.

[aa key-takeaways]

Key Takeaways

Webhook-based payment reconciliation replaces polling and manual CSV exports with real-time event notifications that update ledger records the moment a payment state changes.

A UK Electronic Money Institution (EMI) that exposes IBAN-level webhooks eliminates manual payment attribution; each event is automatically scoped to the correct client account.

Multi-currency settlement across GBP, EUR, and USD generates separate FX conversion and settlement finality events; conflating them is the most common cause of reconciliation discrepancies.

Production webhook integrations must implement idempotency keys and HMAC signature verification to prevent duplicate ledger entries and spoofed event processing.

Since May 2026, FCA PS25/12 requires UK EMIs to perform and evidence daily reconciliation. SaaS platforms building on a compliant EMI inherit this infrastructure rather than building it independently.

Webhooks should be paired with a daily API report fallback: real-time events handle the primary flow, while scheduled API pulls catch any events missed during downtime.

[aa btn]Book a Call[/aa]

[/aa]

Why SaaS Platforms Need Webhook-Based Reconciliation

SaaS platforms that support embedded payments (marketplaces, payroll tools, affiliate networks, and B2B invoicing products) routinely process transactions across GBP, EUR, and USD. A payment account for SaaS companies that handles multiple currencies generates reconciliation complexity that a single-currency setup never encounters: each currency rail has a different settlement timeline, each FX conversion produces a separate financial event, and each payment failure requires a reversal entry. At modest transaction volumes, finance teams can manage this manually. As volume grows, the manual approach breaks.

The alternative to manual reconciliation is SaaS platform payment reconciliation automation driven by webhooks. Rather than exporting CSV files at the end of each business day and matching them against an internal ledger, a webhook-first integration receives a push notification for every meaningful state change: payment received, settlement confirmed, FX rate applied, and payment returned. The ledger updates continuously, not in batches. Reconciliation discrepancies, which average 5–8% in manual processes, drop below 0.1% in automated webhook-driven systems.

[aa fast-fact]

Fast Fact: According to industry benchmarking data, automated webhook-driven reconciliation reduces error rates from 5–8% in manual processes to below 0.1%, a figure that compounds significantly across high transaction volumes.

[/aa]

The Gap Between Payment Processing and Reconciliation

Most payment APIs confirm that a transaction was initiated, not that it settled. A payment initiation endpoint returns a transaction reference and an initial status of "pending" or "processing." What it does not return is a settlement finality signal: the moment the funds are irrevocably available in the receiving account. That confirmation arrives minutes, hours, or days later, depending on the payment rail, and platforms that poll the API on a fixed schedule risk missing it entirely.

Event-driven payment reconciliation addresses this directly. Instead of querying the API every few minutes and processing the same "pending" status repeatedly, the platform's endpoint receives a push notification the moment the status transitions. A five-minute polling interval means a platform can miss settlement windows for near-instant rails like Faster Payments (GBP) and accumulate a reconciliation backlog that grows with every transaction cycle.

How Multi-Currency Complexity Multiplies Reconciliation Work

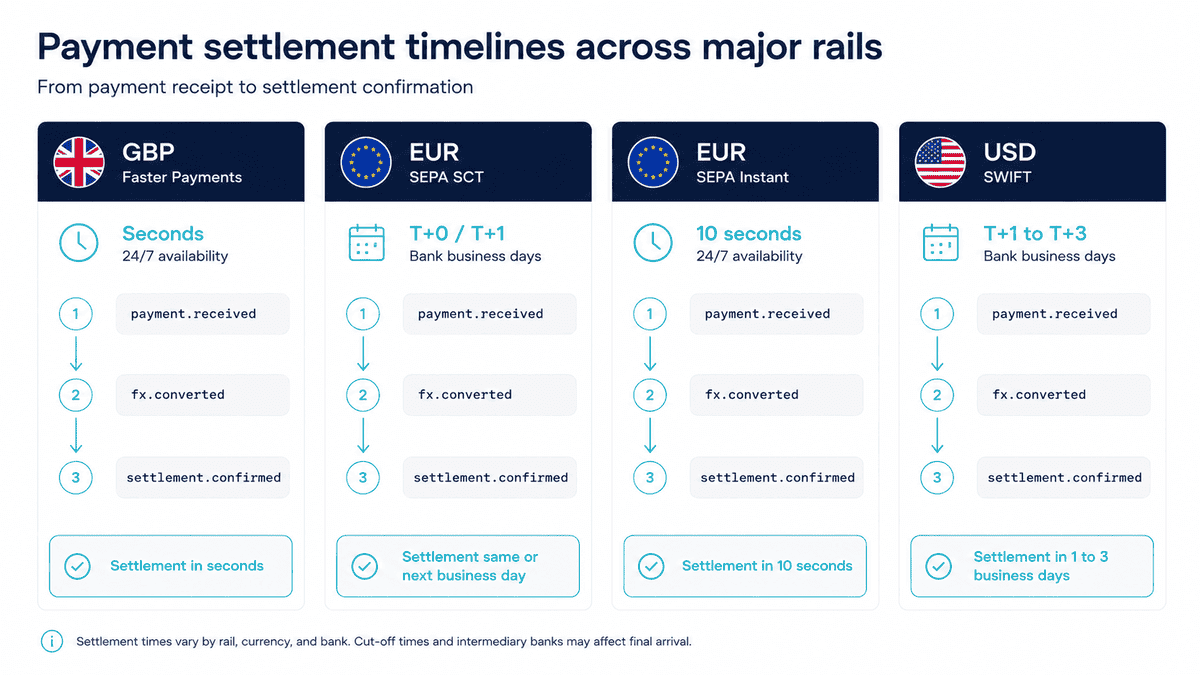

Each currency rail operates on a different settlement timeline. EUR payments via SEPA Credit Transfer (SCT) typically settle same-day or T+1 per the EPC 2025 SCT Rulebook; SEPA Instant (SCT Inst) settles within 10 seconds with a per-transaction cap of €100,000. GBP payments via Faster Payments are near-instant, available 24/7. USD payments via SWIFT clear in T+1 to T+3 depending on the correspondent banking chain involved.

A SaaS platform that handles mass payouts via Faster Payments alongside EUR SEPA transfers is simultaneously managing three distinct settlement timelines. Each currency stream needs its own event handler. A GBP payment.received event does not carry the same financial implications as a EUR fx.converted event. Multi-currency settlement automation requires the platform to process these events independently, preserving currency codes through the ledger update chain rather than converting everything to a base currency at ingestion.

What UK EMI Webhook Infrastructure Provides

A UK Electronic Money Institution (EMI) that exposes a webhook API delivers payment state changes as signed HTTP events, giving SaaS platforms a real-time feed of every settlement transition across their multi-currency accounts. This is distinct from what a generic payment processor provides. Processors typically send webhooks scoped to a transaction. An EMI scopes webhooks to dedicated IBAN accounts and emits events across the full payment lifecycle, including FX conversion, which processors rarely expose as a discrete event. Automating payment reconciliation with webhooks via a UK EMI API means the platform receives all the data it needs to run its reconciliation logic without any additional API calls.

Event-Driven Architecture vs Polling-Based Models

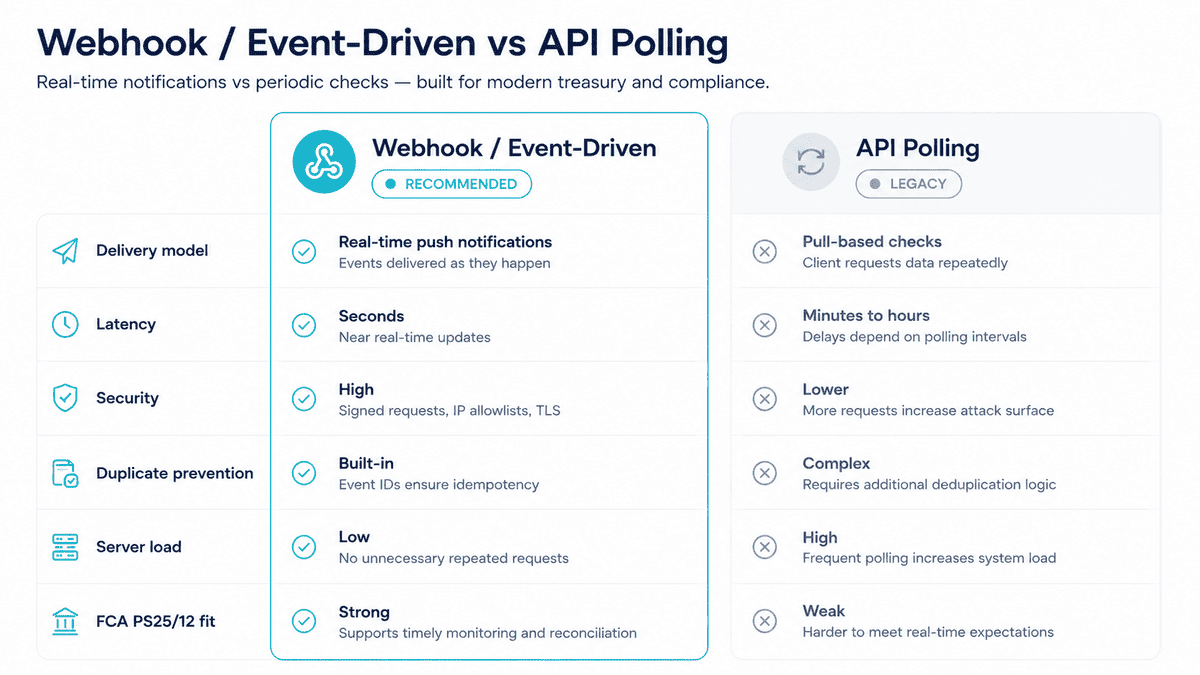

Event-driven architecture and polling-based models represent two fundamentally different approaches to monitoring payment state, and the choice between them determines how scalable a platform's reconciliation system can become.

Polling requires the platform to send an API request on a fixed schedule (every minute or every five minutes) and parse the response to detect status changes. The drawbacks compound at scale:

Latency: A five-minute polling interval means a confirmed settlement can sit unrecognised for up to five minutes before the ledger updates.

Rate limits: High-frequency polling consumes API quota. Providers that rate-limit aggressively can block reconciliation processes during peak payment periods.

False positives: Repeated requests for the same "pending" transaction add noise to application logs and increase processing overhead.

Missed transitions: If a payment moves from "processing" to "settled" to "returned" within a single polling interval, the intermediate state is never recorded.

In an event-driven setup, the EMI's webhook system pushes a signed HTTP POST to the platform's endpoint the moment each state change occurs. A mature UK EMI webhook infrastructure emits at minimum five event types relevant to multi-currency reconciliation: payment.received, settlement.confirmed, fx.converted, payment.returned, and payment.failed. Each event carries a unique event ID, currency codes, gross and net amounts, timestamps, and a cryptographic signature.

IBAN-Level Webhooks for Multi-Currency Accounts

When a UK EMI issues a dedicated IBAN per client or per currency, each webhook event is scoped to that account, making payment attribution automatic. The platform does not need routing logic to determine which client an inbound payment belongs to. The dedicated IBAN (International Bank Account Number) is the identifier, and the webhook payload carries it.

This is a structural advantage over shared-pool architectures, where an EMI or PSP receives payments into a single master account and relies on payment references or reference matching to attribute funds. Reference matching fails when corporate payers truncate references, use different formatting, or omit them entirely. IBAN-level webhook scoping avoids this failure mode entirely.

A UK EMI that issues dedicated IBANs provides per-account webhook routing across GBP, EUR, and USD accounts. Each inbound event is delivered to the platform endpoint already attributed: the accountId and currency fields in the payload identify the account without any cross-referencing.

Settlement Finality Signals and FX Rate Events

Settlement finality and FX conversion are two distinct events in a multi-currency payment flow, and a webhook-first EMI emits both. The fx.converted event fires when the exchange rate is locked and the gross amount is converted; it carries the from-currency, to-currency, the locked rate, the gross input amount, and the fee deducted. The settlement.confirmed event fires when the converted funds are credited to the receiving account.

Platforms that conflate these two events record the wrong amount in the ledger. A payment that arrives as EUR 1,000 and settles as GBP 847.30 after a 0.4% FX spread requires two ledger entries: an FX cost entry recording the spread, and a settlement credit recording the net GBP receipt. If the platform treats settlement.confirmed as the only event and derives the FX cost retroactively, rounding errors accumulate across high transaction volumes.

ISO 20022 payment messaging, which SWIFT and increasingly SEPA rails use for structured data, provides richer metadata in webhook payloads, including purpose codes, remittance information, and currency conversion details. EMIs that pass ISO 20022 fields through to their webhook payloads give SaaS platforms significantly more reconciliation data per event.

Building Automated Reconciliation Into a SaaS Platform

Connecting webhook integration payment reconciliation multi-currency settlement UK EMI infrastructure into a SaaS platform requires solving three engineering concerns in sequence: mapping event payloads to ledger operations, handling parallel currency streams without cross-contaminating balances, and building error recovery that survives real-world delivery failures.

Mapping Webhook Payloads to Platform Ledger Events

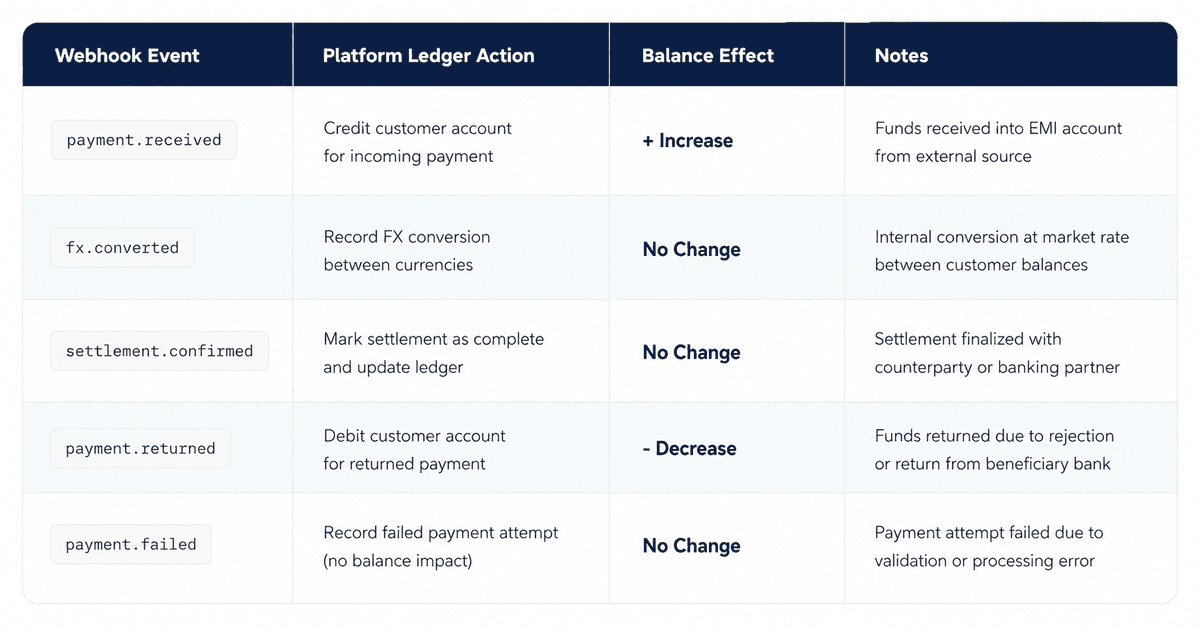

Each webhook payload from a UK EMI should map to exactly one ledger operation. The mapping should be deterministic, defined by event type alone, with no conditional logic that depends on external state or prior events. A practical mapping table for a multi-currency SaaS ledger:

payment.received→ credit the client sub-account in the event's currencyfx.converted→ record an FX cost entry (from-amount minus to-amount, with locked rate)settlement.confirmed→ mark the corresponding payment as reconciledpayment.returned→ reverse the original credit entry and record a return fee if applicablepayment.failed→ log the failure without creating a ledger entry; trigger an alert

The critical prerequisite for this mapping to work correctly at scale is the idempotency key webhook: a unique identifier assigned to each event by the EMI. Before processing any event, the platform checks whether that event ID has already been processed. If it has, the event is discarded. This prevents duplicate ledger entries when the EMI retries delivery after a timeout. SaaS platform payment reconciliation automation that skips idempotency handling will eventually double-count settled payments.

Handling Multiple Currency Streams in a Single Integration

A currency-aware ledger stores each account balance in its original currency rather than converting to a base currency at ingestion. This is the design choice that makes multi-currency settlement automation tractable. When a EUR payment arrives, the EUR sub-account balance increases. When a GBP payment settles, the GBP sub-account balance increases. FX conversion logic runs only when the platform or the client explicitly requests a conversion, not as a side effect of every inbound webhook.

Webhook payloads from a UK EMI carry explicit currency codes alongside amounts. The currency field in payment.received and settlement.confirmed events identifies the account currency; the from_currency and to_currency fields in fx.converted events record the conversion direction. A well-designed ledger update function treats these fields as authoritative and preserves them through every downstream write.

Dedicated IBAN accounts for each currency stream simplify this further. A platform that opens separate accounts for GBP, EUR, and USD receives three independent webhook streams, each with its own event sequence. The ledger update function can route each stream independently rather than parsing a mixed-currency event feed.

Error Recovery and Reconciliation Fallback Logic

Webhook delivery is not guaranteed. Network timeouts, endpoint misconfigurations, or temporary outages can cause events to go undelivered. The EMI's retry mechanism, while it reduces the risk, does not eliminate it. Production integrations must implement three layers of defence.

First, endpoint signature verification. Every inbound webhook should be validated using HMAC (Hash-based Message Authentication Code) or an equivalent signing standard before the payload is processed. Unverified webhooks are discarded. This prevents spoofed events, a particularly relevant risk for payment reconciliation systems where a fabricated settlement.confirmed could trigger an incorrect credit.

Second, idempotency checks. The event ID from each payload is stored after processing. On every subsequent delivery, the platform checks whether that ID is already in the store. Duplicate events are discarded without side effects. This is the same principle Banking Circle's webhook reconciliation documentation recommends: a reconcilable infrastructure must be idempotent.

Third, a daily API fallback pull. Webhooks should not be the sole reconciliation mechanism. A scheduled API call that retrieves all transactions from the EMI for the previous business day, similar to what batch payment exports provide. It catches any events that were missed during real-time delivery. This fallback closes the reconciliation window to a maximum of one business day even in the worst-case failure scenario.

[aa cta]

Automated Multi-Currency Reconciliation for SaaS Platforms

EQWIRE provides webhook-based EMI infrastructure with dedicated IBAN accounts, real-time settlement events, and FX conversion signals, designed for API-first integration by SaaS teams.

[aa btn]Create Account[/aa]

[/aa]

Choosing a UK EMI for Webhook-Based Reconciliation

Not all UK EMIs expose the same depth of webhook infrastructure. For SaaS platforms building UK EMI API payment reconciliation into their product, the quality of the webhook layer determines both how much custom logic the platform needs to write and how reliable that logic will be in production. The difference between a shallow webhook implementation (status updates only) and a deep one (full event taxonomy with FX, IBAN-scoped delivery, and replay capability) can represent several months of engineering work.

Key API Capabilities to Evaluate

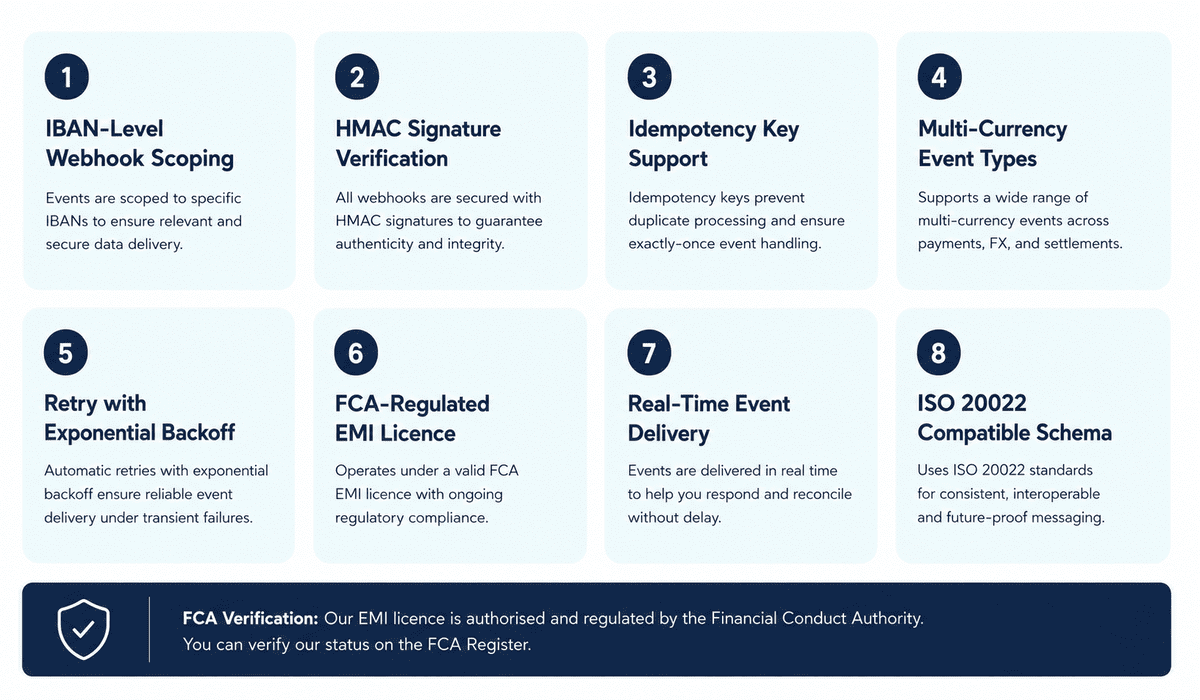

SaaS teams evaluating UK EMI providers for webhook-based reconciliation should assess eight capabilities before committing to an integration:

Event completeness: Does the EMI emit events for all five lifecycle states (received, settlement confirmed, FX converted, returned, and failed)? Providers that only send

payment_status_updatewith a status string force the platform to derive event meaning from status parsing, which breaks when statuses change.Payload signing: Is every webhook payload signed with HMAC-SHA256 or a comparable standard? Unsigned webhooks cannot be verified and should not be processed in production.

Dedicated IBAN issuance: Does the EMI issue separate IBANs per client account or per currency? Shared-pool architectures require reference matching, which fails at scale.

Sandbox with realistic event simulation: Does the sandbox generate the full event sequence, including FX events and returns, or only successful payment confirmations? A sandbox that omits edge-case events produces integrations that break on first real-world encounter.

Event replay capability: Can missed or failed events be replayed via the API? This is the safety net when the daily fallback pull is not sufficient granularity.

Multi-currency account support: Does a single integration support GBP, EUR, and USD accounts with unified webhook formatting across all three?

Rate limit and retry policy documentation: What is the retry interval after a delivery failure? How many retries before the event is abandoned? Undocumented retry behaviour makes fallback planning guesswork.

ISO 20022 field passthrough: Does the EMI pass ISO 20022 structured payment data through to webhook payloads, including remittance information and purpose codes?

FCA-Licensed EMIs and Safeguarding Compliance in 2026

Since 7 May 2026, UK Electronic Money Institutions must maintain formal daily reconciliation evidence under FCA PS25/12, a safeguarding regime published by the Financial Conduct Authority in August 2025 that significantly tightens client fund protection requirements. Under PS25/12, firms must perform internal and external safeguarding reconciliations at least once each reconciliation day. Identified shortfalls must be funded from the firm's own resources on the same business day. Monthly returns covering reconciliation data, safeguarding methods, and amounts held must be submitted to the FCA. Annual safeguarding audits are required.

For SaaS platforms building on top of a UK FCA-licensed EMI, this regime provides a structural compliance guarantee. The EMI's own reconciliation infrastructure (daily runs, shortfall detection, monthly reporting) operates at the layer below the SaaS product. Platforms that would otherwise need to build or audit this themselves instead rely on their EMI's regulatory obligations. When evaluating PSP settlement into a multi-currency EMI account options, the FCA registration status of the provider determines whether this compliance layer is in place.

EQWIRE holds FCA registration FRN 901100 and operates under PS25/12 requirements. Client funds are held in segregated safeguarding accounts with daily reconciliation against the relevant funds liability. CASS 15 (the Client Assets Sourcebook chapter governing safeguarding) applies to EQWIRE's operations.

FAQ

How do webhooks improve payment reconciliation accuracy for SaaS platforms?

Webhooks deliver state-change events in real time, allowing platforms to update ledger entries immediately rather than relying on scheduled polling or end-of-day batch imports. In polling-based systems, a payment that settles during an off-cycle window is not recorded until the next polling run, which can be minutes or hours later. In webhook-driven systems, the settlement.confirmed event reaches the platform endpoint within seconds of the funds being credited. Automated webhook reconciliation reduces error rates from 5–8% in manual processes to below 0.1%, according to industry benchmarking data, primarily by eliminating the manual matching step and reducing the window in which status mismatches can accumulate.

What webhook events should a UK EMI provide for multi-currency reconciliation?

At minimum, a UK EMI webhook infrastructure should emit five event types for complete multi-currency reconciliation: payment.received (inbound funds confirmed), settlement.confirmed (funds irrevocably credited and available), fx.converted (exchange rate locked, from-currency and to-currency amounts recorded), payment.returned (inbound payment reversed, usually within 2–5 business days of original receipt), and payment.failed (outbound payment rejected before settlement). Each event payload should carry a unique event ID for idempotency checking, explicit currency codes, gross and net amounts, a UTC timestamp, and a cryptographic signature for verification. EMIs that combine multiple state transitions into a single payment_status_update event force the platform to parse status strings rather than processing deterministic event types.

How SaaS platforms use EMI webhooks to automate multi-currency settlement reconciliation

SaaS platforms integrate EMI webhooks by mapping each event type to a deterministic ledger update function. An inbound payment.received event credits the relevant client sub-account in the event's currency; an fx.converted event records the FX spread as a cost entry; a settlement.confirmed event marks the payment as reconciled in the platform's transaction table; and a payment.returned event reverses the original credit. The key architectural requirement is that every function processes each event ID exactly once — using an idempotency key webhook stored in a deduplication table. Platforms that implement this pattern correctly can process thousands of multi-currency webhook events per minute without reconciliation gaps, provided the EMI issues IBAN-level webhooks that make currency and account attribution automatic.

What is the difference between a webhook and polling for payment reconciliation?

Polling requires the platform to send API requests to the EMI on a fixed schedule (every minute or every five minutes) to check for status changes. This approach introduces three structural problems for reconciliation: latency (a settled payment can sit unrecognised for up to one polling interval), rate-limit risk (high-frequency requests consume API quota), and missed transitions (a payment that moves through multiple statuses within one polling window leaves no intermediate record). A webhook, by contrast, is an HTTP POST notification that the EMI pushes to the platform's endpoint the moment a transaction changes state. Real-time payment reconciliation via webhooks means the ledger updates within seconds of each event, rather than within minutes or hours. For SaaS platforms reconciling multi-currency settlement across GBP, EUR, and USD, the latency difference is material. Faster Payments settles in seconds, and a five-minute polling interval misses settlement confirmation consistently.

Do UK EMIs provide sandbox environments for testing webhook reconciliation?

Most FCA-licensed UK EMIs offer a sandbox environment that simulates payment events and webhook delivery for integration testing. A production-ready sandbox should support the complete multi-currency event sequence, including fx.converted events for cross-currency payments, payment.returned scenarios, and payment.failed edge cases, rather than only simulating successful payment.received and settlement.confirmed flows. Sandboxes that omit FX events produce integrations that break on first live cross-currency transaction. When evaluating an EMI's sandbox, SaaS teams should test the full event lifecycle for each supported currency: a GBP inbound payment, a EUR-to-GBP cross-currency receipt, a USD SWIFT settlement, and at least one return scenario. Signature verification logic should also be tested in the sandbox using the EMI's published signing key before switching to production credentials.

Webhook integration payment reconciliation multi-currency settlement UK EMI infrastructure reduces reconciliation from a periodic manual exercise to a continuous automated process. The design principles are consistent regardless of transaction volume: IBAN-level event scoping removes attribution logic, deterministic event-to-ledger mapping removes ambiguity, idempotency keys remove duplication risk, and a daily fallback pull removes the residual gap that real-time delivery cannot fully close. For SaaS platforms evaluating EMI infrastructure, the webhook layer is as important as the payment rail coverage. A provider that supports GBP, EUR, and USD from a single API integration with full event taxonomy and FCA PS25/12 compliance significantly reduces both integration complexity and ongoing compliance overhead. EMI webhook integration built on a regulated, multi-currency account provider gives SaaS teams the data fidelity to offer reconciliation as a feature rather than managing it as a liability.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)