•

•

Wise Business vs UK FCA EMI: Which is Better for Offshore Companies?

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Opening the right payment account is one of the most practical challenges offshore companies face. A BVI holding structure or a Seychelles IBC may be entirely legitimate — yet many payment providers decline them at onboarding, or suspend accounts without notice months later.

Wise Business is the obvious starting point for many directors. It is well-known, fast to set up, and genuinely FCA-authorised. But "FCA-authorised" does not mean "accepts all offshore structures." The gap between Wise Business and a specialist FCA-authorised EMI lies in onboarding policy, not regulatory standing — and that distinction matters more than most guides acknowledge.

This article compares Wise Business vs FCA EMI offshore company GBP EUR access on the factors that matter most: which jurisdictions each accepts, what payment infrastructure each provides, and which choice is more stable for cross-border operations.

[aa key-takeaways]

Key Takeaways

Both Wise Business and specialist FCA EMIs hold FCA authorisation under the UK Electronic Money Regulations 2011

Wise Business restricts or declines offshore jurisdictions including BVI, Seychelles, Cayman Islands and Bermuda

Specialist FCA EMIs accept offshore companies through enhanced due diligence — a deeper but one-time process

GBP accounts come with UK sort code, Faster Payments (up to £1 million, seconds) and CHAPS (same-day, unlimited)

EUR accounts come with IBAN, SEPA Credit Transfer (T+1) and SEPA Instant (under 10 seconds, €100,000 limit)

The right choice depends on jurisdiction, transaction volume and whether a stable long-term account is the priority

[aa btn]Open an Account[/aa]

[/aa]

Wise Business vs FCA EMI — What Each Offers Offshore Companies

Before comparing features, it helps to establish what both types of provider actually are. Both Wise Business and specialist FCA EMIs operate under the same UK regulatory framework. The difference is in who they serve and how they assess risk at onboarding.

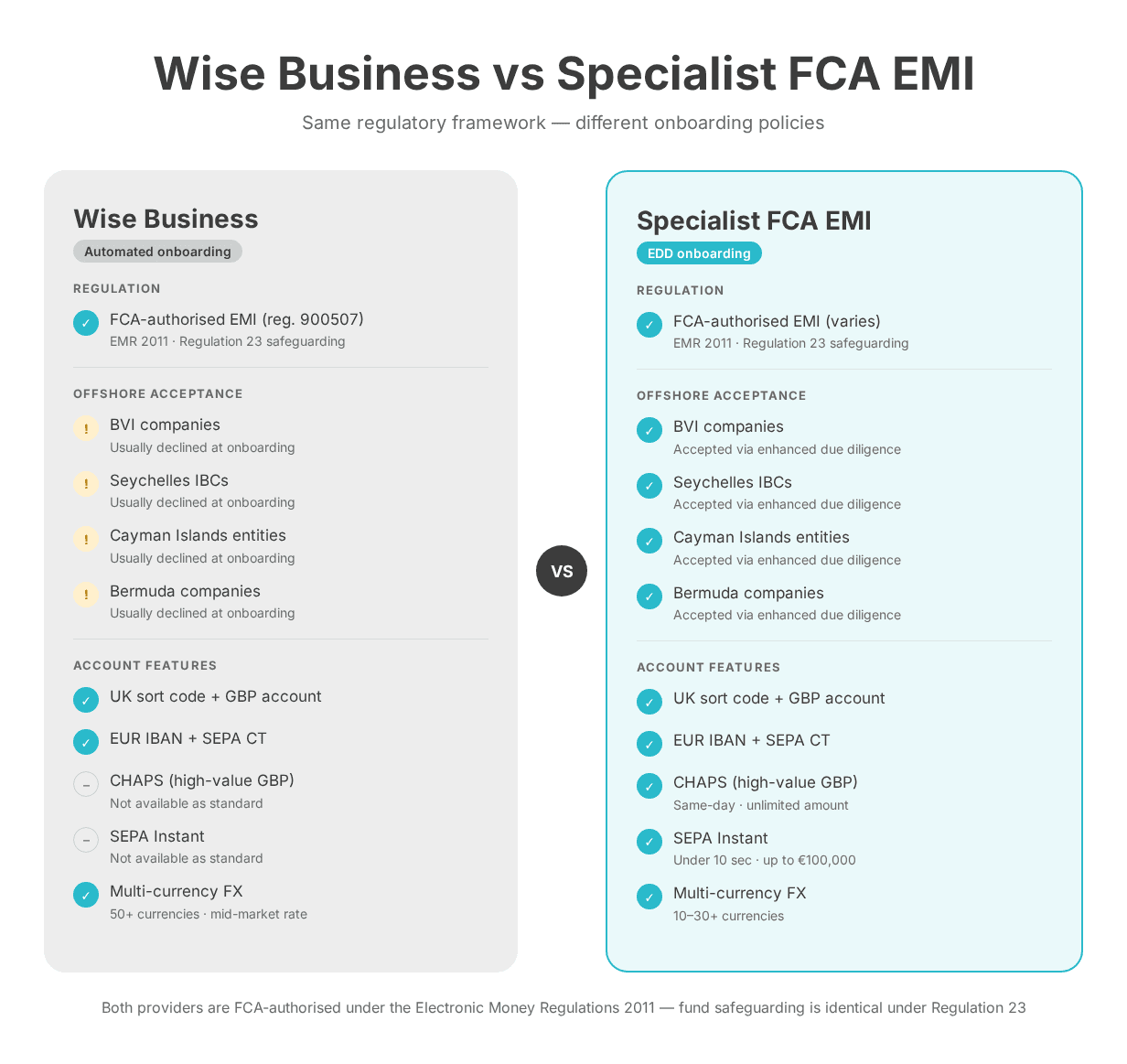

Wise Business — FCA-Authorised but Jurisdiction-Restricted

Wise Payments Limited holds FCA authorisation under registration number 900507 and operates under the Electronic Money Regulations 2011 (SI 2011/99). Client funds are safeguarded under Regulation 23, meaning they are ring-fenced from Wise's operating capital and protected in the event of insolvency.

The product is built primarily for small businesses and freelancers in mainstream jurisdictions: the UK, EU, US, Australia. Its onboarding is largely automated, which creates speed — but also means limited capacity to handle complex corporate structures.

For offshore companies, this creates a hard constraint. Wise Business applies risk-based onboarding policies that flag or decline entities from jurisdictions classified as higher-risk under the UK Money Laundering Regulations 2017. BVI, Seychelles, Cayman Islands and Bermuda all fall into this category. Some offshore companies do get approved, but account stability is a separate issue: Wise Business reserves the right to close accounts where enhanced due diligence requirements cannot be met at scale.

Specialist FCA EMIs — Built for Cross-Border and Offshore Structures

Specialist FCA EMIs are, legally, the same type of entity as Wise. Both hold FCA authorisation under EMR 2011. Both safeguard funds under Regulation 23. The difference is in their target market and onboarding infrastructure.

Specialist providers have compliance teams designed to handle offshore entities. They apply enhanced due diligence (EDD) at onboarding: requesting UBO declarations, corporate structure charts, source of funds evidence, and business activity documentation. This process is more thorough upfront, but it produces accounts that are stable and purpose-built for cross-border use.

[aa fast-fact]

Fast Fact: Both Wise Business and specialist FCA EMIs safeguard client funds under Regulation 23 of the UK Electronic Money Regulations 2011. The regulatory protection is identical — the difference is onboarding policy, not protection level.

[/aa]

Head-to-Head Comparison — Wise Business vs FCA EMI for Offshore Companies

Feature | Wise Business | Specialist FCA EMI |

|---|---|---|

FCA authorisation | Yes (reg. 900507) | Yes (varies by provider) |

Fund safeguarding | Regulation 23, EMR 2011 | Regulation 23, EMR 2011 |

BVI companies | Usually declined | Accepted with EDD |

Seychelles IBCs | Usually declined | Accepted with EDD |

Cayman Islands entities | Usually declined | Accepted with EDD |

Bermuda companies | Usually declined | Accepted with EDD |

UK sort code + GBP account | Yes | Yes |

Faster Payments Service | Yes | Yes |

CHAPS | Not standard | Yes |

EUR IBAN | Yes | Yes |

SEPA Instant | Not standard | Yes (provider-dependent) |

Multi-currency support | 50+ currencies | 10–30+ currencies |

Onboarding speed | Fast (automated) | Slower (manual EDD) |

Account stability for offshore | Variable | High |

The table captures the core trade-off: Wise Business is faster to open and offers broader currency coverage, but its offshore acceptance rate is low and long-term account stability is not guaranteed. Specialist FCA EMIs require more documentation upfront but deliver accounts designed for exactly the use case offshore companies have.

Which Offshore Jurisdictions Can Use Wise Business?

This is the question most guides answer vaguely. The breakdown by jurisdiction, based on Wise's own terms and documented industry experience, is as follows.

BVI Companies

British Virgin Islands companies are among the most common offshore structures globally. Wise Business considers them high-risk under its automated onboarding policy. Applications from BVI-incorporated entities are frequently rejected at the document verification stage, or approved initially and then flagged during periodic account review.

For BVI companies that need a UK sort code and GBP account, a specialist FCA EMI is the more reliable route. The process involves EDD — typically a corporate structure chart, UBO declaration, and source of funds documentation — but produces a dedicated UK account number that remains stable over time. The full process is covered in the guide to UK bank details for BVI companies.

Seychelles IBCs

Seychelles international business companies face similar constraints with Wise Business. Seychelles appears on EU and FATF enhanced monitoring lists, which triggers automatic risk flags in most automated onboarding systems.

Specialist FCA EMIs accept Seychelles IBCs, provided the beneficial ownership structure is fully documented and the business activity is clearly explained. EUR IBAN accounts for Seychelles structures follow the same EDD process as GBP accounts — see the guide to EUR IBAN for Seychelles companies for detail.

Cayman Islands Entities

Cayman Islands entities — holding companies, SPVs, investment structures — are similarly declined by Wise Business's automated process. The Cayman Islands was grey-listed by the FATF in 2021 and removed in 2024, but many payment providers continue to apply elevated scrutiny as a matter of internal policy.

Specialist FCA EMIs that work with Cayman entities require documentation of the ultimate beneficial owner and a clear explanation of the entity's business purpose. GBP and EUR accounts are available with the same sort code and IBAN infrastructure as any other offshore structure.

Bermuda Companies

Bermuda companies are treated as high-risk by most automated onboarding systems. Wise Business typically declines them. Specialist FCA EMIs accept Bermuda structures through EDD, which follows the same documentation process as for BVI and Seychelles entities. See the full walkthrough on UK payment accounts for Bermuda companies.

[aa cta]

Open a GBP or EUR Account for Your Offshore Company

EQWIRE is an FCA-authorised EMI that accepts BVI, Seychelles, Cayman Islands, and Bermuda companies through enhanced due diligence. UK sort code, Faster Payments, CHAPS, EUR IBAN, and SEPA access — all in one account.

[aa btn]Create Account[/aa]

[/aa]

When a Specialist FCA EMI Is the Better Choice

For offshore companies that need consistent, long-term access to UK and EU payment infrastructure, specialist FCA EMIs deliver the more appropriate solution. The specific advantages come down to how GBP and EUR accounts are structured.

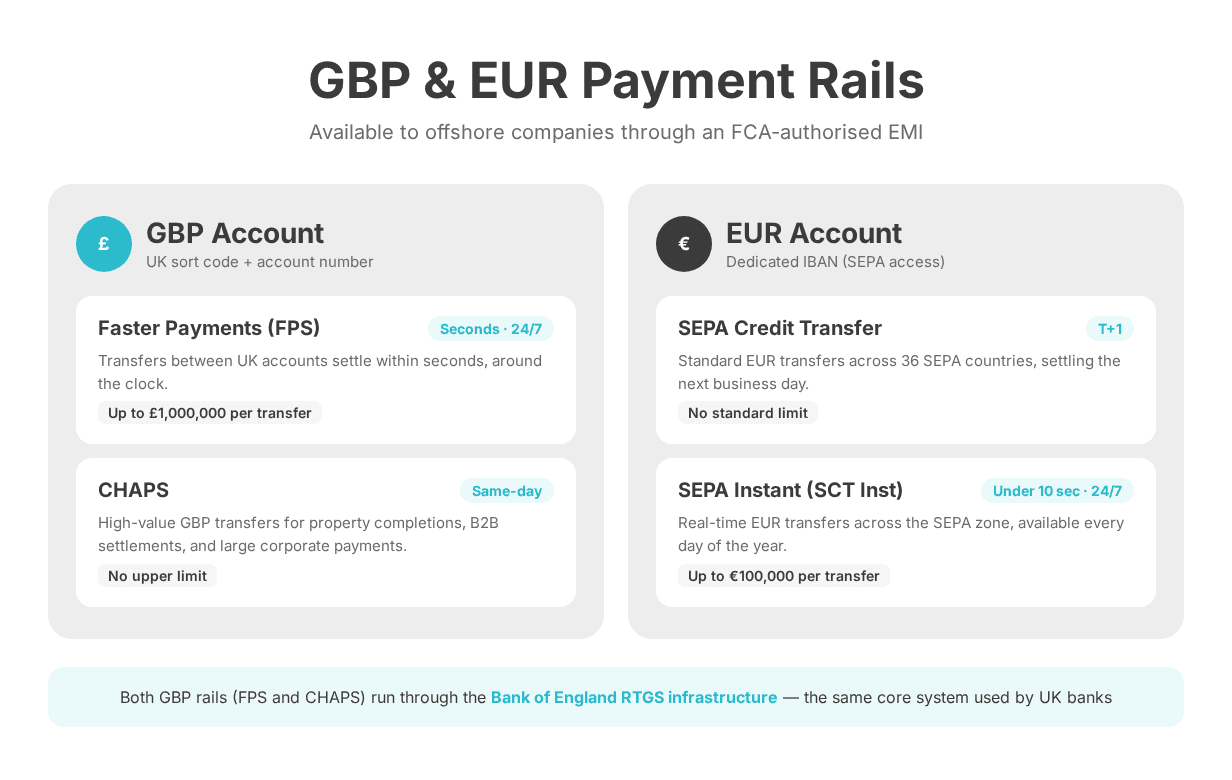

GBP Account — Sort Code, Faster Payments, CHAPS

A GBP account with a specialist FCA EMI comes with a UK sort code and account number — the same format as a standard UK business bank account. This matters for counterparty credibility: a UK sort code is immediately recognisable to UK businesses, HMRC, and payroll providers.

Payment access typically includes two rails:

Faster Payments Service (FPS): transfers up to £1 million settle within seconds, available 24/7

CHAPS: same-day high-value transfers with no upper limit, used for property transactions, large B2B settlements, and time-sensitive corporate payments

Both rails operate through the Bank of England's Real-Time Gross Settlement (RTGS) infrastructure. For offshore companies previously reliant on correspondent banking, direct access to Faster Payments and CHAPS through a specialist FCA EMI removes intermediary layers — and the fees that come with them.

EUR Account — IBAN, SEPA Credit Transfer, SEPA Instant

EUR accounts with specialist FCA EMIs come with a dedicated IBAN. Payment access typically includes two rails:

SEPA Credit Transfer (SCT): standard EUR transfers across 36 SEPA countries, settling T+1 — the next business day

SEPA Instant Credit Transfer (SCT Inst): transfers up to €100,000 settle in under 10 seconds, 24/7/365

SEPA Instant has expanded rapidly since the EU's mandatory instant payments regulation came into force for Eurozone banks in January 2025. Non-bank payment service providers, including FCA-authorised EMIs, are increasingly offering it as a standard feature rather than a premium add-on.

For offshore companies receiving EUR invoices or making EUR supplier payments, the difference between T+1 and sub-10-second settlement is material — particularly in commodity trading, services contracting, and investment fund administration.

Multi-Currency Holding and FX Conversion

Specialist FCA EMIs typically offer accounts in 10–30 currencies alongside GBP and EUR. Where Wise Business leads is in FX conversion: it uses the mid-market rate with transparent percentage fees and supports 50+ currencies. For companies with high-volume FX conversion needs across many currency pairs, Wise Business's FX pricing may be more competitive.

The practical limitation is access. If an offshore company cannot obtain a stable Wise Business account, the FX advantage is irrelevant. Most specialist FCA EMIs offer competitive FX rates for major pairs — GBP/EUR, GBP/USD, EUR/USD — and the cost difference for typical transaction volumes is modest.

Cost and Fee Comparison

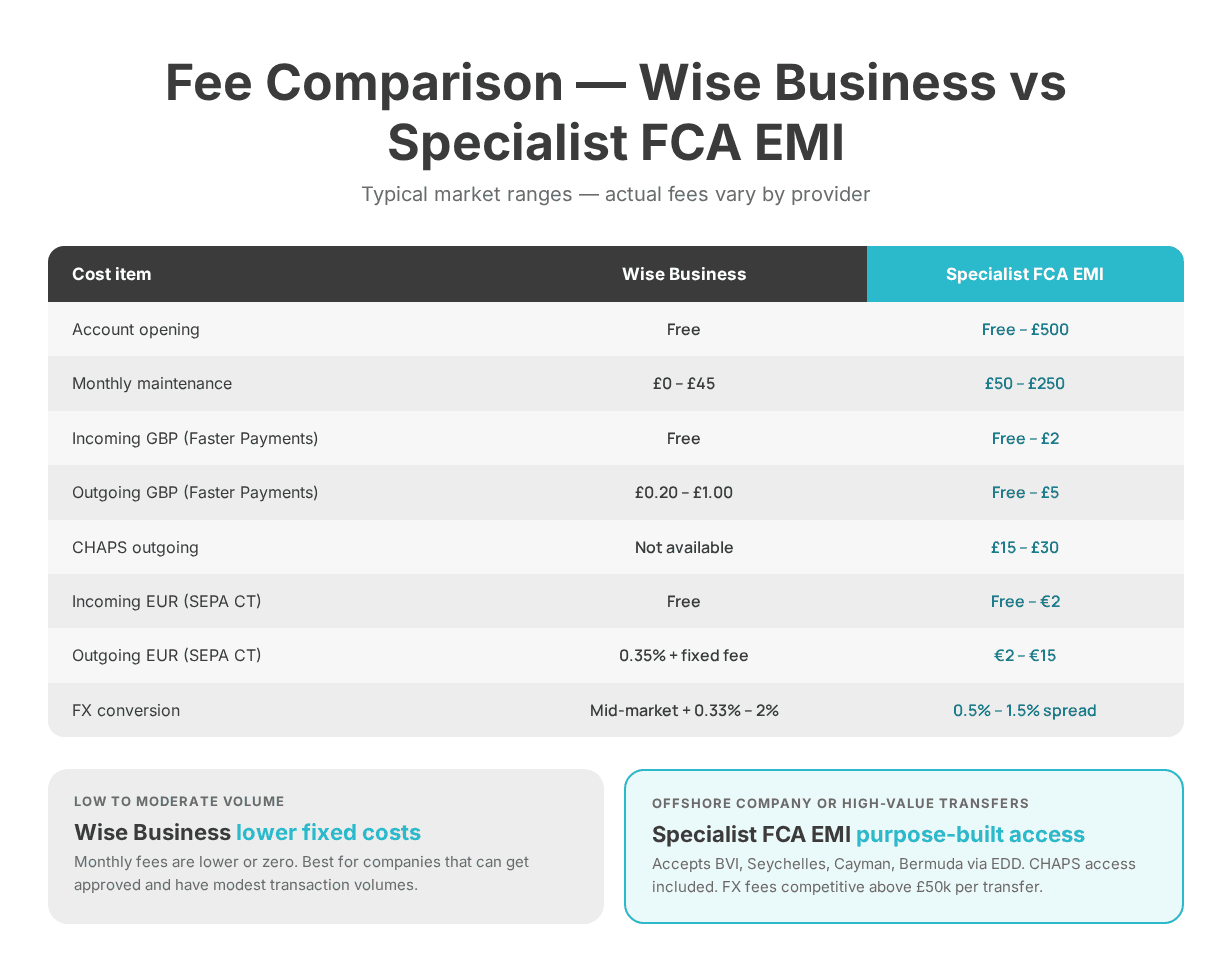

Fee structures vary by provider. The ranges below reflect typical market positioning rather than specific quotes.

Cost item | Wise Business | Specialist FCA EMI |

|---|---|---|

Account opening | Free | Free – £500 |

Monthly maintenance | £0–£45 | £50–£250 |

Incoming GBP (FPS) | Free | Free – £2 |

Outgoing GBP (FPS) | £0.20–£1.00 | Free – £5 |

CHAPS outgoing | Not available | £15–£30 |

Incoming EUR (SEPA CT) | Free | Free – €2 |

Outgoing EUR (SEPA CT) | 0.35% + fixed fee | €2–€15 |

FX conversion | Mid-market + 0.33%–2% | 0.5%–1.5% spread |

For offshore companies with low to moderate transaction volumes, the monthly fee difference is the most significant variable. A specialist FCA EMI at £150/month makes sense when it is the only viable route to account access. For companies comparing options where both providers are available, Wise Business's lower fixed costs are relevant.

The calculation shifts for high outgoing volumes. Wise Business's percentage-based FX fees exceed a specialist EMI's flat fees at transaction sizes above approximately £50,000–£100,000 per transfer.

How to Choose — Wise Business or a Specialist FCA EMI?

The decision framework is straightforward once the eligibility question is resolved.

If the company is incorporated in BVI, Seychelles, Cayman Islands, or Bermuda: a specialist FCA EMI is the practical choice. Wise Business is unlikely to approve the account, and even where approval occurs initially, long-term stability is not guaranteed. A specialist EMI accepts the structure through a one-time EDD process and provides a purpose-built account.

If the company needs CHAPS for high-value GBP transfers: a specialist FCA EMI is necessary. Wise Business does not offer standard CHAPS access, which limits it for property completions, large M&A settlements, and high-value B2B transactions.

If SEPA Instant is a requirement: check whether the specific specialist EMI offers SCT Inst. Coverage varies among providers. Wise Business does not offer it as standard, so this differentiates among specialist EMIs rather than between Wise Business and specialist EMIs as a category.

If the company is in a mainstream jurisdiction and primarily needs multi-currency FX: Wise Business is a legitimate and cost-effective option, assuming onboarding succeeds. For offshore structures specifically, a Wise Business alternative — a specialist offshore company UK FCA EMI — is the more reliable route regardless of FX pricing. For a broader comparison of FCA EMIs against traditional banking, see the guide to FCA-authorised EMI vs UK bank account. For non-UK companies in general, the guide to GBP accounts for non-UK companies covers the full option set.

[aa cta]

Get Started with EQWIRE

Open a GBP or EUR account for your offshore company online.

[aa btn]Create Account[/aa]

[/aa]

FAQ

Is Wise Business an FCA-authorised EMI?

Yes. Wise Payments Limited holds FCA authorisation under registration number 900507 and operates as an electronic money institution under the UK Electronic Money Regulations 2011. Client funds are safeguarded under Regulation 23 of those regulations. However, FCA authorisation does not determine which company structures Wise Business accepts — that is governed by its internal onboarding policy, not its regulatory status.

Wise Business vs FCA-authorised EMI: which is better for BVI, Seychelles or Cayman companies?

For BVI, Seychelles and Cayman Islands companies, a specialist FCA-authorised EMI is the better choice in most cases. Wise Business applies automated risk screening that declines most offshore structures at onboarding. Specialist FCA EMIs accept offshore companies through enhanced due diligence — a more thorough process, but one that produces stable, purpose-built accounts with UK sort code, GBP Faster Payments, CHAPS, and EUR IBAN access.

What is the difference between Wise Business and a specialist FCA EMI?

Both are FCA-authorised electronic money institutions regulated under the same framework — the UK Electronic Money Regulations 2011 — with identical fund safeguarding protections under Regulation 23. The difference is in target market and onboarding approach. Wise Business is built for mainstream businesses in established jurisdictions, using automated onboarding. Specialist FCA EMIs are designed for cross-border and complex structures, including offshore companies, using manual compliance review with enhanced due diligence.

Can a Seychelles IBC open a GBP account with Wise Business?

It is possible but not reliable. Wise Business uses automated onboarding that flags Seychelles as a higher-risk jurisdiction. Applications are frequently declined or approved temporarily and later subject to account review. A specialist FCA EMI that accepts Seychelles IBCs through enhanced due diligence is the more stable option for long-term GBP account access.

What does enhanced due diligence involve for an offshore company opening a UK payment account?

Enhanced due diligence typically requires: a certificate of incorporation and memorandum or articles of association, a UBO declaration identifying all beneficial owners above a 10–25% threshold, a corporate structure chart, proof of business activity such as contracts or invoices, and source of funds documentation. The process is more involved than standard onboarding but is a one-time exercise. Once complete, the account operates normally without repeated documentation requests.

Choosing between Wise Business and a specialist FCA EMI comes down to two questions: can the company get a stable account with Wise, and does its transaction profile require infrastructure that Wise does not offer as standard? For the majority of offshore structures — BVI, Seychelles, Cayman, Bermuda — the answer to the first question resolves the decision. A specialist FCA EMI, verified on the FCA Financial Services Register, is the appropriate provider for offshore companies that need reliable, long-term access to UK and EU payment rails.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)