•

•

Multi-Currency Account for Digital Nomads: Hold GBP, EUR, USD and AED in One Place

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Remote professionals working across the UK, EU, US, and UAE increasingly face the same practical problem: income arrives in four different currencies, but most banking infrastructure is built for one. A freelancer invoicing UK clients in GBP, EU clients in EUR, US clients in USD, and receiving a retainer from a Dubai employer in AED cannot manage those balances efficiently from a single home-country account. The result is forced conversion at the point of receipt, accumulating FX costs, and the administrative overhead of maintaining accounts across multiple providers.

A multi-currency account digital nomad professionals use solves this by holding each currency in a separate balance — allowing remote workers to receive GBP, EUR, USD and AED into the same account without triggering an automatic exchange. This guide covers how such accounts work, how to choose a regulated provider, how to open one remotely, and how to set up payment details for each of the four major currencies most digital nomads need.

[aa key-takeaways]

Key Takeaways

A multi-currency account holds GBP, EUR, USD and AED in separate balances with no forced conversion on receipt.

FCA-authorised Electronic Money Institutions (EMIs) offer regulated accounts to individuals and expats, with client funds held in segregated safeguarding accounts.

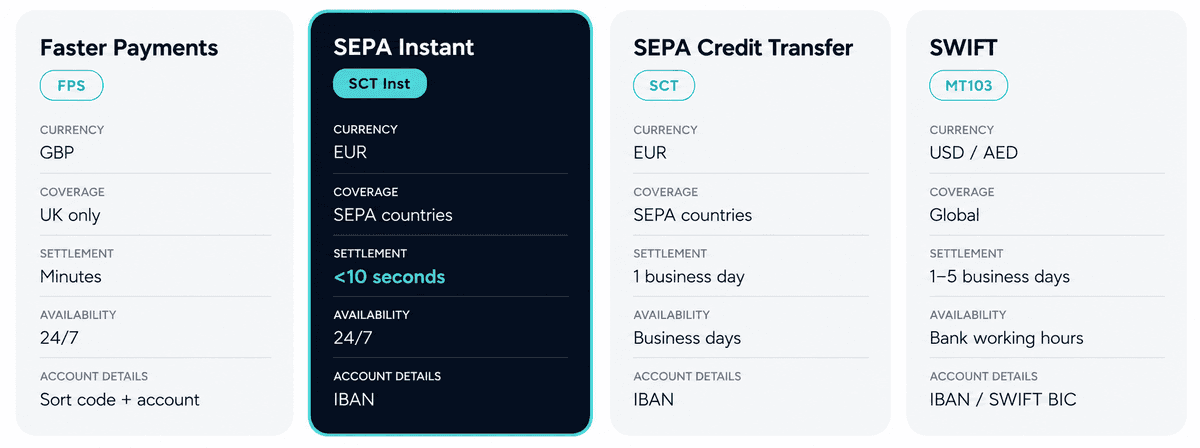

Each currency uses a different payment rail: GBP via Faster Payments, EUR via SEPA, USD and AED via SWIFT.

Remote account opening is standard for most FCA-authorised EMIs; a passport and proof of address are typically sufficient.

SEPA Instant Credit Transfer settles in under 10 seconds end-to-end; SWIFT transfers to UK accounts typically arrive in 1–5 business days.

[aa btn]Book a Call[/aa]

[/aa]

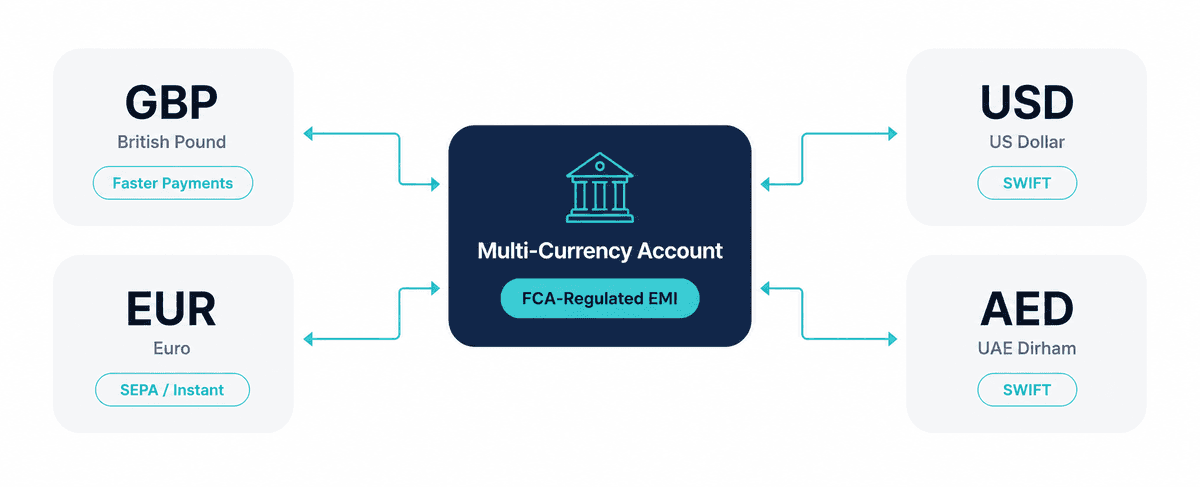

What Is a Multi-Currency Account and How Does It Work for Digital Nomads

A multi-currency account for digital nomads is a payment account that holds funds in two or more currencies simultaneously, with each currency kept in a separate balance. Unlike a standard bank account that converts incoming foreign payments into the account's base currency automatically, a multi-currency account preserves each currency until the account holder chooses to convert. For a remote professional receiving income from four different countries, this distinction determines whether they pay FX costs on every receipt or only when they actually need to exchange.

The mechanics are straightforward: each currency balance functions as a sub-account with its own set of payment details. A GBP balance comes with a UK sort code and account number. An EUR balance carries an IBAN (International Bank Account Number) and BIC. USD and AED balances receive funds via SWIFT, using the account's SWIFT/BIC identifier. Clients and employers in each country send payments through the payment rail native to that currency. The funds arrive in the corresponding balance without triggering a conversion.

Separate Currency Balances vs. Traditional Foreign Currency Accounts

A traditional foreign currency account at a high street bank allows holders to maintain a balance in a second currency, but typically only one. These accounts often require branch visits to open, carry monthly maintenance fees, and restrict outbound payment types. A multi-currency account for expats, by contrast, holds four or more currencies simultaneously, supports multiple outbound payment rails (SEPA, SWIFT, Faster Payments), and (when offered by an FCA-authorised Electronic Money Institution) can be opened entirely online by individuals regardless of UK residency.

[aa fast-fact]

Fast Fact: SEPA Instant Credit Transfer, governed by the European Payments Council (EPC), settles end-to-end in under 10 seconds. The 2025 SCT Inst rulebook, effective October 2025, updated processing precision requirements and raised the scheme-level maximum transfer amount significantly from the previous €100,000 cap.

[/aa]

Which Currencies Matter Most: GBP, EUR, USD and AED Explained

For most digital nomads working globally, four currencies cover the majority of income and expense flows. GBP handles UK client invoices, UK tax obligations, and expenses during time in the UK. EUR covers income from EU-based clients, SEPA-zone rent and subscriptions, and cost-of-living in the eurozone. USD is the dominant currency for US tech clients, SaaS platforms, and global freelance marketplaces. AED is the relevant currency for UAE employers, Dubai-based retainer arrangements, and Gulf region living costs.

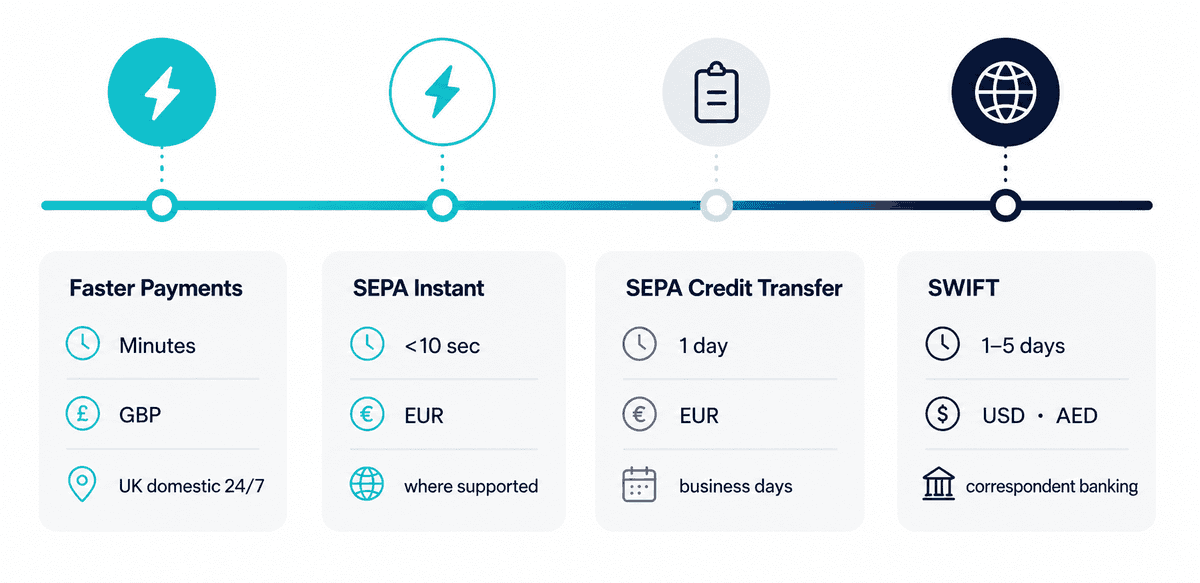

Each currency reaches a UK multi-currency account via a different payment system. GBP arrives via the Faster Payments Service (FPS), which processes domestic UK transfers typically within minutes. EUR arrives via SEPA: either as a standard Credit Transfer (T+1 settlement) or, where supported by both sending and receiving institutions, as a SEPA Instant Credit Transfer (under 10 seconds). USD and AED arrive via SWIFT, which routes through a correspondent banking chain and typically settles in 1–5 business days.

How to Choose the Right Multi-Currency Account

FCA-regulated Electronic Money Institutions (EMIs) offer digital nomad multi-currency account UK FCA EMI access to individuals and expats without requiring a business registration or UK residency. An EMI is not a traditional bank: it does not lend client funds or maintain fractional reserves. Instead, under the FCA's safeguarding rules — most recently updated under Policy Statement PS25/12, with new requirements effective 7 May 2026. EMIs are required to hold client funds in segregated accounts with approved credit institutions, separate from the firm's own operational money. This means client balances are ring-fenced even if the EMI encounters financial difficulties.

FCA-Regulated EMI vs. Neobank vs. Traditional Bank

The three main categories of multi-currency account providers differ significantly in regulation, fund protection, and payment infrastructure:

FCA-authorised EMI: Holds client funds in segregated safeguarding accounts. Can be verified on the FCA register. Offers direct access to FPS, SEPA, and SWIFT. No lending of client funds. Annual safeguarding audit now required under PS25/12.

Consumer neobank (e.g., Wise, Revolut): Typically regulated (Wise is FCA-authorised; Revolut holds an EU banking licence). Consumer-oriented features including spending analytics, crypto, and card controls. Often limited on inbound business payment support and professional-grade SWIFT access for non-consumer currencies like AED.

Traditional high street bank: FSCS-protected up to £85,000 (deposit insurance). Suited to permanent UK residents with established address history. Branch-based onboarding, typically limited foreign currency options, and high international transfer fees via SWIFT correspondent chains.

For remote professionals who need reliable inbound SWIFT support for AED alongside EUR and GBP, an FCA-authorised EMI with direct SWIFT access is the most operationally practical choice.

Key Features to Look For: Payment Rails, Currencies, Remote Opening

When evaluating a borderless bank account for freelancers and nomads, four capabilities determine whether the account works in practice. First, the account must support inbound payments via SEPA, SWIFT, and Faster Payments across all three rails in a single account. Second, separate currency balances must be available for at least GBP, EUR, USD, and AED. Third, the provider must offer remote onboarding without requiring a UK address or in-person verification. Fourth, the account must be offered by a regulated entity (FCA-authorised or equivalent) so client funds carry statutory protection.

[aa cta]

Open a Multi-Currency Account for GBP, EUR, USD and AED

EQWIRE is a UK Electronic Money Institution authorised and regulated by the Financial Conduct Authority, offering individual multi-currency accounts with access to Faster Payments, SEPA, and SWIFT, with fully remote onboarding for professionals worldwide.

[aa btn]Create Account[/aa]

[/aa]

How to Open a Multi-Currency Account Remotely

Most FCA-authorised EMIs offer fully remote account opening; the entire process completes online without visiting a branch or presenting physical documents in person. For digital nomads and expats without a fixed UK address, this is a practical requirement. Eligibility is typically based on identity verification and source of funds, rather than country of residence.

Document Requirements for Individuals and Expats

The documentation required to open a multi-currency account for expats remotely is consistent across FCA-authorised EMIs. A valid government-issued photo ID (passport, national identity card, or driver's licence) as the primary identity document. Proof of address, typically a utility bill or bank statement from the past three months, establishes current residence. Some providers accept digital versions or certified copies. For individuals earning from multiple countries, a brief description of income sources may be requested during enhanced due diligence.

Non-UK residents can open accounts with UK FCA-authorised EMIs, provided the jurisdiction of residence is not on a restricted list. The account is issued under UK regulation regardless of where the account holder lives or works.

What to Expect During Online Verification

The verification process for a digital nomad banking account typically follows a standard sequence. Identity documents are uploaded through the provider's application portal. An automated identity check, typically powered by a specialist verification provider, runs within minutes. A liveness check (a short selfie video) confirms the applicant is the person in the ID document. In most cases, account approval arrives within one to three business days. Some providers offer faster processing for straightforward applications.

Once approved, the account holder receives their payment details: a UK sort code and account number for GBP, an IBAN and BIC for EUR, and SWIFT details for USD and AED. These are the credentials sent to clients for payment instructions.

[aa cta]

Ready to Open a Multi-Currency Account Online?

Remote professionals and expats can apply to EQWIRE and set up GBP, EUR, USD and AED accounts without visiting a branch. The application is fully online.

[aa btn]Create Account[/aa]

[/aa]

Setting Up Payment Details in Each Currency

Knowing the correct payment details for each currency balance is the step that connects the account to real income. Each currency follows the conventions of its native payment system. Clients expect to see the format they're used to. Using the wrong format (e.g., sending an IBAN to a US client who expects ACH routing details) delays payment.

The UK bank details framework is the same whether the account belongs to a company or an individual; FCA-authorised EMIs issue the same payment infrastructure to both.

GBP Account: Sort Code, Account Number, Faster Payments

A GBP account at a UK EMI comes with a sort code and account number, following the same six-digit / eight-digit format used by all UK high street banks. Payments sent to this account from any UK bank or payment institution arrive via the Faster Payments Service (FPS), which processes transfers typically within minutes and operates around the clock. UK clients invoiced in GBP can send payment from their own current accounts directly to the sort code and account number, with no international transfer required and no currency conversion involved.

To open a GBP account with a UK EMI, no UK address or UK citizenship is required; the account is issued under UK regulation and the payment details are indistinguishable from a standard UK bank account from the perspective of the payer.

EUR Account: IBAN, BIC, SEPA Access

An EUR account is identified by an IBAN (International Bank Account Number) and BIC (Bank Identifier Code), also known as a SWIFT code. The IBAN structure follows ISO 13616: a two-letter country code, two check digits, and the Basic Bank Account Number (BBAN) of up to 30 characters. EU and EEA clients invoice payers by providing their IBAN and BIC. Any bank or payment institution in the SEPA zone (spanning 36 European countries) can send a SEPA Credit Transfer to that IBAN, with standard settlement in one business day.

A named IBAN account issued by a UK FCA-authorised EMI is functionally identical to an IBAN issued by a European bank for the purpose of receiving SEPA payments. The IBAN is reachable from all 36 SEPA-member countries. EUR income from EU-based clients, marketplace platforms, or employer payroll can be credited directly to this balance without conversion.

USD Account: Routing Number and SWIFT Details

USD transfers into a UK EMI account route via SWIFT, using the account's SWIFT/BIC code and the account number. Unlike domestic US transfers (which use ABA routing numbers and ACH), SWIFT is the standard for international USD wires from non-US banks. A US client sending USD from a US bank account to a UK multi-currency account initiates a SWIFT wire transfer using the recipient's SWIFT code, account number, and the intermediary bank details provided by the EMI. Funds typically arrive in 1–3 business days, though correspondent banking chains can occasionally extend this to five business days depending on the sending institution's SWIFT relationships.

Receiving AED via SWIFT

AED payments from UAE-based clients, employers, or local payroll providers arrive via SWIFT, the same mechanism used for USD. The UAE dirham is not part of any regional instant payment scheme equivalent to SEPA, so SWIFT is the only practical rail for AED transfers into a UK multi-currency account. A nomad working under contract for a UAE employer provides the employer's finance team with the SWIFT/BIC code, account number, and IBAN or account reference. The transfer routes through the correspondent banking chain and arrives in the AED balance within 1–5 business days. Fees on the sending side vary by the UAE bank; some apply a fixed SWIFT fee, others apply a percentage of the transfer amount.

SEPA does not cover AED. SEPA is limited to EUR-denominated transfers within the EU and EEA. This is a limitation worth stating plainly: AED income always arrives more slowly and with variable fees compared to EUR or GBP.

[aa fast-fact]

Fast Fact: SWIFT operates a correspondent banking network covering over 200 countries and territories. An AED wire from a UAE bank to a UK EMI account may pass through one or two correspondent banks before reaching the destination; each hop can add processing time and, in some cases, intermediate fees.

[/aa]

How to Receive Income From International Clients

Remote professionals invoicing clients in different countries receive payment via the payment rail native to each currency. The account holder's job is to provide the correct payment details for each currency when issuing invoices, and to understand what to expect in terms of timing and costs.

Invoicing Clients in GBP, EUR, USD and AED

Invoice format for each currency follows the payment system convention. For GBP invoices to UK clients, the payment details section includes: Account Name, Sort Code, Account Number, Bank Name. For EUR invoices to EU clients: Account Name, IBAN, BIC/SWIFT. For USD invoices to US clients: Account Name, SWIFT/BIC, Account Number, Bank Name, and the intermediary bank details. For AED invoices to UAE clients: Account Name, SWIFT/BIC, Account Number, Bank Name, and IBAN if the account has one.

Currency invoicing reduces or eliminates FX friction: a UK client paying GBP into the GBP balance transfers in their own currency without paying a conversion fee. The EMI account receives the exact amount invoiced. Converting to another currency only happens when the account holder actively initiates it.

How Long Transfers Take by Payment Rail

Settlement times vary significantly by payment system. Faster Payments (GBP): typically within minutes, 24/7. SEPA Credit Transfer (EUR): one business day. SEPA Instant Credit Transfer (EUR): under 10 seconds end-to-end, where both sender and recipient institutions support it. SWIFT (USD, AED): 1–5 business days depending on the correspondent banking chain and the sending bank's processing schedule.

For clients who need fast EUR settlement, SEPA Instant is the most efficient option. Not all payment institutions offer SEPA Instant for inbound transfers; this is worth confirming with the account provider before relying on it.

Managing, Converting and Sending Your Funds

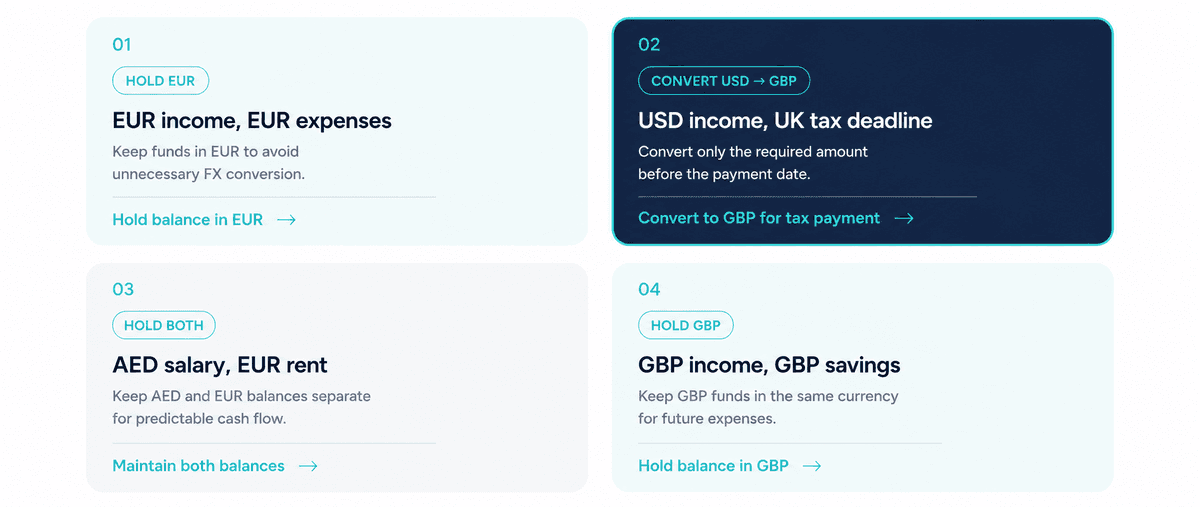

Holding funds in their received currency avoids conversion costs at the point of receipt, a direct saving for freelancers paid in multiple currencies who do not need to spend every inbound payment immediately. The strategic question is when to convert, and for which purpose.

When to Convert Currencies (and When to Wait)

The practical approach for digital nomad banking is to hold each currency until there is a specific spending need in that currency or a favourable exchange rate presents itself. A freelancer who receives USD from a US client but pays EUR rent in Berlin converts USD to EUR when the rent payment is due, not automatically on receipt. A nomad earning AED from a Dubai employer but spending GBP in London converts AED to GBP when the GBP balance runs low, not on the day of salary receipt.

Holding multiple currencies in one account makes this possible without maintaining accounts at four separate institutions. The account holder sees all balances in a single interface, converts only what is needed, and avoids conversion fees on the remainder.

Sending Money Internationally From a Single Account

Outbound international transfers from a multi-currency account for expats follow the same payment rails as inbound receipts. EUR payments to EU landlords, payroll providers, or vendors go via SEPA SCT. USD payments to US suppliers or contractors go via SWIFT. GBP payments within the UK go via Faster Payments. AED payments to UAE recipients also route via SWIFT.

A single account with balances in four currencies means outbound transfers originate from the correct currency balance, with no conversion required if the destination currency matches an existing balance. This is the operational advantage over maintaining a single-currency account and converting every transfer.

FAQ

What is a multi-currency account for digital nomads?

A multi-currency account for digital nomads is a payment account that holds funds in two or more currencies in separate balances, allowing the account holder to receive, hold, and send money in different currencies without forcing a conversion on each receipt. Each currency balance has its own payment details: a sort code and account number for GBP, an IBAN and BIC for EUR, SWIFT details for USD and AED. Remote professionals use these accounts to consolidate income from multiple countries into a single, regulated platform while retaining control over when currency conversion occurs.

How do digital nomads working globally hold GBP EUR USD and AED without opening multiple bank accounts?

The most practical way digital nomads working globally hold GBP EUR USD and AED without opening multiple bank accounts is through a multi-currency account offered by an FCA-authorised Electronic Money Institution. These accounts provide separate currency balances for each supported currency, each with their own inbound payment details. GBP arrives via the UK Faster Payments Service using a sort code and account number. EUR arrives via SEPA using an IBAN and BIC. USD and AED arrive via SWIFT. All four balances are held within a single account, accessible through one platform, with no requirement to open accounts in four different countries or maintain separate provider relationships for each currency.

Can I use a UK EMI account if I don't live in the UK?

Yes. FCA-authorised UK EMIs can offer accounts to individuals who are not UK residents, provided the applicant's country of residence is not on a restricted jurisdiction list. The account is issued under UK regulation, meaning client funds are subject to the FCA's safeguarding rules, with funds held in segregated accounts with approved credit institutions. Non-UK residents typically apply online, submitting a passport and proof of current address. The GBP sort code, EUR IBAN, and SWIFT details issued are fully functional for international use, regardless of where the account holder is physically located when making or receiving payments.

What documents do I need to open a multi-currency account online?

Most FCA-authorised EMIs require a government-issued photo ID (passport, national identity card, or driver's licence) and proof of current address, such as a bank statement or utility bill dated within the past three months. Some providers also request a brief description of income sources as part of standard anti-money laundering checks. The documents are uploaded digitally, and the identity verification process typically runs within minutes. No in-person appointment, branch visit, or certified paper document is usually required. Account approval for straightforward individual applications typically takes one to three business days.

What is the difference between SEPA and SWIFT transfers?

SEPA (Single Euro Payments Area) covers EUR-denominated transfers between payment accounts in EU and EEA member states, covering 36 countries in total. It is administered by the European Payments Council (EPC) and operates on two standards: SEPA Credit Transfer (SCT), which settles in one business day, and SEPA Instant Credit Transfer (SCT Inst), which settles in under 10 seconds where supported. SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a global messaging network that facilitates cross-border transfers in any currency, including USD, AED, and non-SEPA currencies. SWIFT transfers route through a correspondent banking chain and typically settle in 1–5 business days. SEPA is faster and often cheaper for EUR payments within Europe; SWIFT is the standard for USD, AED, and any currency outside the SEPA zone.

For remote professionals managing GBP, EUR, USD and AED from a single multi-currency account digital nomad infrastructure, understanding which payment rail serves which currency reduces delays and unexpected costs. EQWIRE's individual multi-currency accounts are authorised and regulated by the Financial Conduct Authority, with client funds held in segregated safeguarding accounts. Remote professionals and expats can apply entirely online at client.eqwire.com/sign-up and receive GBP, EUR, and USD payment details upon approval.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)