•

•

MUR Account for Offshore Companies: Receive Mauritian Rupee Without a Local Bank

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A Seychelles-registered trading company issues monthly invoices to three clients based in Mauritius. Each invoice is denominated in Mauritian rupees (MUR). The company holds a USD and EUR multi-currency account in London, but MUR is unavailable. The finance team contacts two Mauritius commercial banks. Both require local economic nexus: a resident director, a physical office, or a regulated fiduciary acting as account signatory. A third option exists: a UK electronic money institution (EMI) authorised by the Financial Conduct Authority (FCA) that supports MUR as a receivable currency.

A MUR account for an offshore company with Mauritius-based clients is achievable without opening a local bank account on the island. This guide covers the exact documents required, the four steps to activate a MUR-capable account through an FCA-regulated EMI, and the common errors that delay or kill applications, along with what happens to MUR balances once they arrive.

[aa key-takeaways]

Key Takeaways

BVI and Seychelles companies can receive Mauritian rupees (MUR) through an FCA-authorised UK electronic money institution — no Mauritius bank account required.

Onboarding at a UK EMI takes 3–5 business days with a complete KYB document pack — compared to 4–8 weeks at a Mauritius commercial bank, when applications are accepted at all.

The required documents include Certificate of Incorporation, Register of Directors and Shareholders, a UBO declaration with passport and proof of address for each 25%+ beneficial owner, and proof of business activity.

Most application delays trace to three avoidable errors: incomplete UBO documentation, a vague business purpose description, and failing to specify MUR as a required currency at the point of application.

Once credited, MUR can be held, converted to USD, EUR, or GBP within the same account, or used to send outbound payments to Mauritius-based suppliers via SWIFT.

[aa btn]Book a Call[/aa]

[/aa]

Why Offshore Companies Can't Simply Open a MUR Account in Mauritius

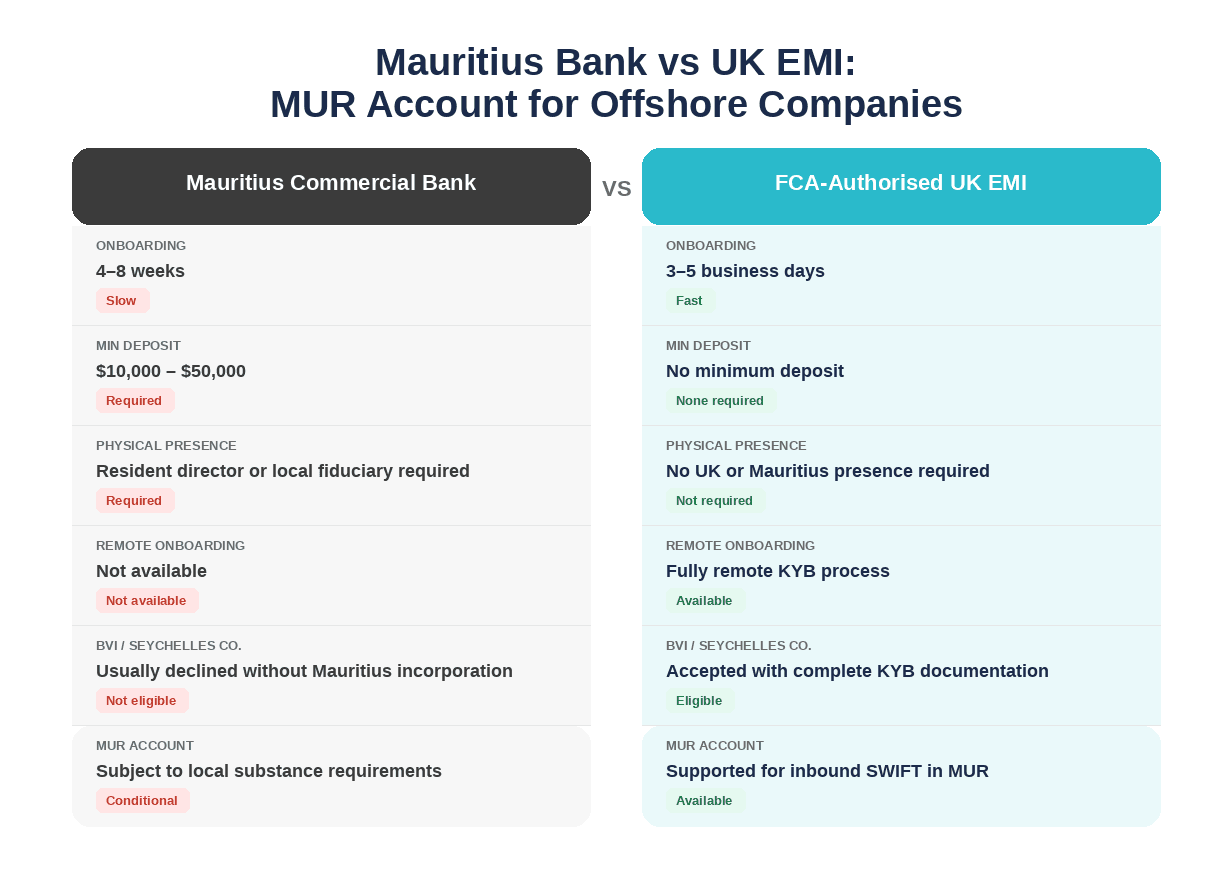

Mauritius commercial banks, including MCB, SBM, and AfrAsia, require non-resident corporate applicants to demonstrate local economic nexus. For a BVI or Seychelles company with no Mauritius presence, that requirement is almost impossible to clear without incorporating locally or engaging a licensed fiduciary.

The Bank of Mauritius, which oversees domestic banking compliance, requires non-resident corporate entities to satisfy enhanced due diligence standards. In practice, this means Mauritius banks ask for evidence of local substance: a registered office address, resident directors, or a regulated fiduciary acting as account signatory. Without at least one of these, applications typically stall before reaching a credit decision.

The Financial Services Commission Mauritius (FSC) regulates Global Business Companies (GBC) and Authorised Companies (AC): the two legal structures used for Mauritius-incorporated offshore entities. A BVI or Seychelles company operating outside this framework lacks FSC recognition, which creates an additional compliance barrier when approaching Mauritius banks for a corporate account.

[aa fast-fact]

Fast Fact: Opening a corporate bank account in Mauritius as a non-resident offshore company typically takes 4–8 weeks — and minimum deposit requirements range from $10,000 to $50,000 depending on the institution. Many applications are declined without detailed explanation.

[/aa]

The result: finance teams trying to receive MUR from Mauritius clients without a local bank account are effectively shut out of the traditional banking route. This is where FCA-regulated UK electronic money institutions fill the gap.

What Mauritius Banks Actually Require from Non-Resident Companies

To open a MUR account at a Mauritius commercial bank, a non-resident offshore company typically needs to provide:

A registered office or verifiable local address in Mauritius

At least one resident director, or a regulated fiduciary acting as account signatory

Evidence of economic substance in Mauritius: contracts, local employees, or ongoing transactions

Minimum initial deposit of $10,000–$50,000 (varies by bank and account type)

A detailed business plan satisfying both FSC and bank compliance requirements

A bank reference letter from a banking relationship of at least two years

For companies incorporated in BVI, Seychelles, Cayman Islands, or similar jurisdictions without a Mauritius presence, most of these requirements are unattainable without significant structural change. BVI companies that have already accessed UK payment infrastructure remotely. For example, obtaining a GBP sort code through a UK payment institution faces a similar dynamic when seeking Mauritius banking access.

Why a UK EMI Is a Legal and Practical Alternative

An electronic money institution (EMI) authorised by the Financial Conduct Authority (FCA) can issue multi-currency accounts, including MUR, for non-resident offshore companies. No UK incorporation is required. The UK Electronic Money Regulations 2011 establish the legal framework under which FCA-authorised EMIs can serve non-UK entities, including BVI, Seychelles, and other offshore corporate structures.

Unlike a Mauritius local bank, an FCA-authorised EMI does not require physical presence, a local signatory, or a minimum deposit. Onboarding is fully remote, and the compliance process focuses on the KYB (Know Your Business) document pack and a documented description of the company's payment flows.

EQWIRE, an FCA-authorised payment institution, supports MUR as a receivable currency for offshore companies as part of its multi-currency account structure. To verify any EMI's FCA status before applying, use the FCA Financial Services Register.

[aa cta]

Receive MUR Without a Mauritius Bank Account

EQWIRE opens multi-currency accounts for BVI and Seychelles companies, including MUR, in 3–5 business days.

[aa btn]Create Account[/aa]

[/aa]

What You Need Before Applying for a MUR Account

Before submitting an application to open a MUR account as a non-resident company, offshore entities need to prepare two things: a complete KYB document pack and a clear description of their Mauritius payment flows. Partial submissions and vague business descriptions are the two factors most responsible for delayed or failed applications.

Document Checklist for BVI and Seychelles Companies

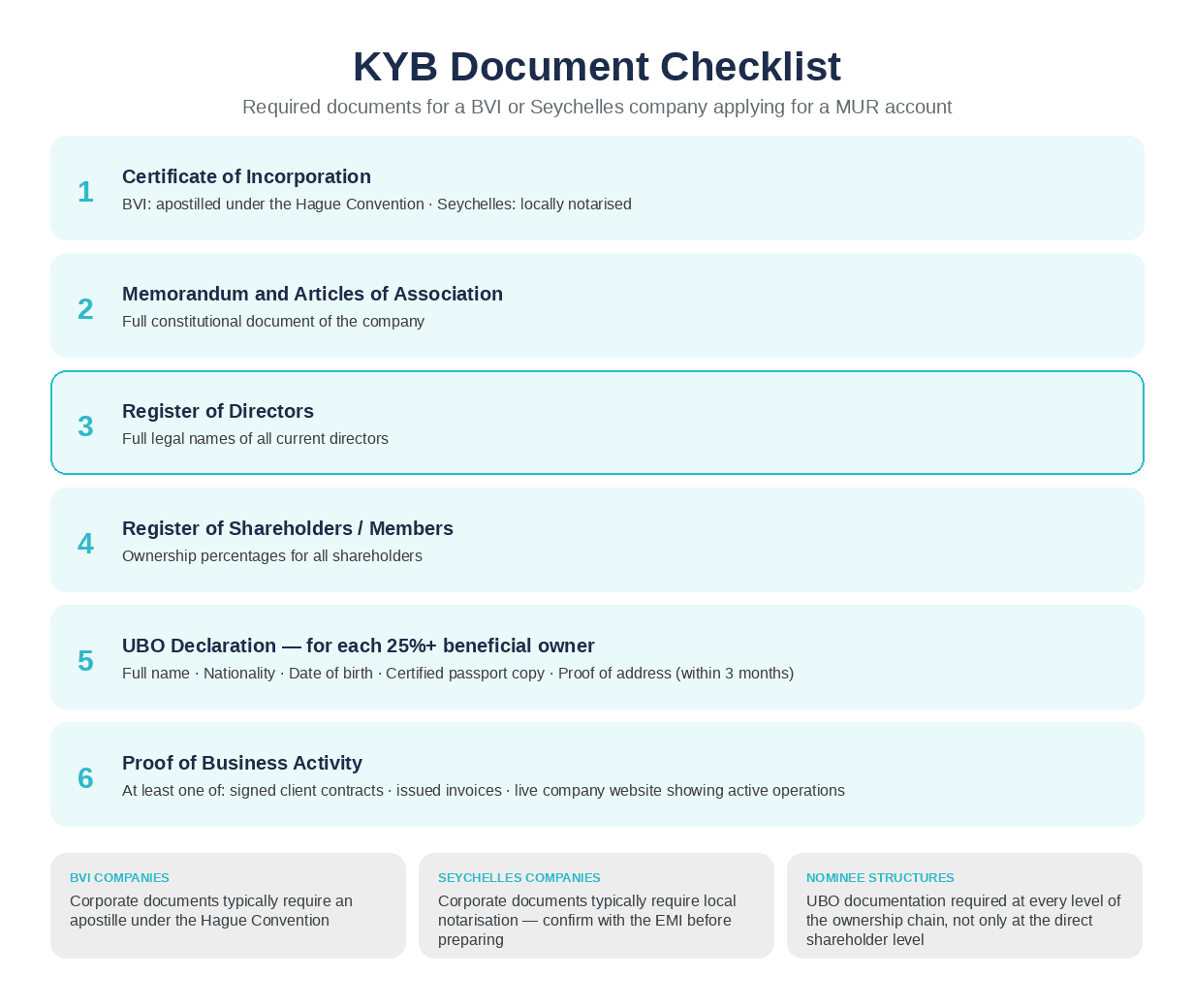

The standard KYB pack for a BVI or Seychelles company applying for a MUR multi-currency account offshore includes:

Certificate of Incorporation — apostilled for BVI companies; locally notarised for Seychelles

Memorandum and Articles of Association

Register of Directors — listing all current directors by full legal name

Register of Shareholders / Register of Members — showing ownership percentages

UBO declaration — for each ultimate beneficial owner holding 25% or more: full name, nationality, date of birth, certified passport copy, and proof of residential address (utility bill or bank statement dated within three months)

Proof of business activity — at least one of: signed client contracts, issued invoices, or a live company website demonstrating active operations

For nominee director or shareholder structures, each layer of the ownership chain requires its own documentation. The 25% UBO threshold applies at every level — not only to immediate shareholders. Submitting the nominee's information without disclosing the underlying beneficial owner is one of the most common compliance holds.

Information About Your Mauritius Clients and Payment Flows

EMI compliance teams require a payment flow description alongside the corporate documents. The description must answer: who are the Mauritius counterparties, in what currency and approximate volume are payments expected, and what is the commercial relationship?

A generic statement such as "international trade" or "consulting services" is insufficient. An effective payment flow note for an offshore company Mauritian rupee payment use case specifies: the nature of the business ("export of IT consulting services to Mauritius-based companies"), the number and approximate identity of clients ("three Mauritius-based corporate clients"), the invoice currency and frequency ("monthly invoices denominated in MUR"), and the expected transaction range ("average MUR 150,000–300,000 per invoice, MUR 500,000–900,000 per month").

Payment flows that are clearly documented reduce compliance review time significantly. Ambiguous descriptions trigger follow-up questions and add 3–5 days to the timeline, a fully avoidable delay.

How to Open a MUR Account for Your Offshore Company — Step by Step

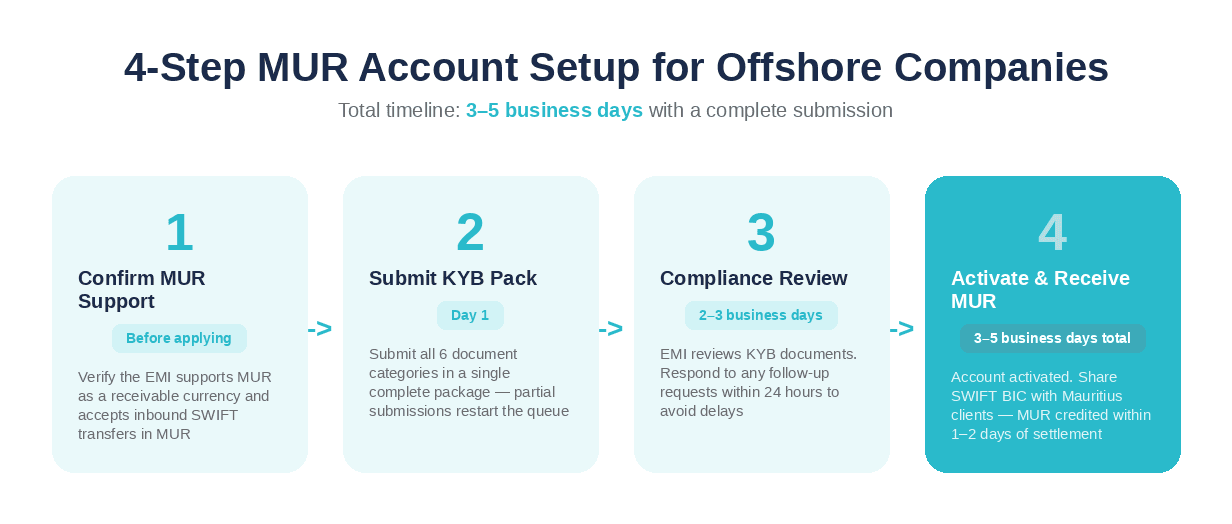

For a BVI or Seychelles company receiving MUR from Mauritius clients, the process through a UK EMI account follows four steps. Each step is discrete and sequential; beginning the next step before the prior one is confirmed is the most common source of avoidable delays.

Step 1 — Confirm MUR Is Supported by the EMI

Not all FCA-authorised EMIs hold MUR as a receivable currency. Before preparing documents, confirm with the EMI that MUR is on its supported currency list and that inbound SWIFT payments in MUR can be credited to a named account. EQWIRE supports MUR for offshore company accounts as part of its multi-currency account structure.

This is also the stage to confirm whether the EMI supports outbound MUR payments, relevant for companies that pay Mauritius-based suppliers in addition to receiving client funds. Some EMIs offer inbound MUR only; others provide bi-directional MUR capability. Clarifying this upfront avoids a second application process later.

The same approach Seychelles companies use to access European IBANs and SEPA payments through a UK-based payment institution applies here: confirm currency support first, then initiate KYB.

Step 2 — Prepare and Submit Your KYB Pack

Assemble all six document categories listed above into a single, complete submission. Partial submissions (a missing UBO passport copy, an unsigned Register of Directors, or a business purpose description that is too vague) reset the compliance queue and typically add 2–5 days to the timeline.

The KYB pack for a MUR account for a BVI company and for a Seychelles-registered entity is identical in structure. The difference lies in document certification: BVI corporate documents typically require an apostille under the Hague Convention; Seychelles documents may require local notarisation. Confirm the specific requirement with the EMI's onboarding team before submitting.

Step 3 — Compliance Review and Account Activation

Compliance review begins within one business day of a complete submission. The review itself takes 2–3 business days in standard cases. The compliance team may request additional information during this window; responding within 24 hours prevents the application from being deprioritised.

Once approved, the account is activated and the company receives its MUR account reference and SWIFT routing details. An FCA-authorised EMI safeguards 100% of client funds in segregated accounts under the FCA safeguarding requirements for EMIs, a meaningful distinction from the Mauritius Deposit Insurance Scheme, which covers up to MUR 200,000 per depositor per bank.

Step 4 — Share Your MUR Receiving Details with Mauritius Clients

Once the account is live, the company shares its MUR account reference and SWIFT BIC with each Mauritius-based client. The client initiates a standard local bank transfer in MUR from their Mauritius commercial bank. That transfer routes through correspondent banking infrastructure: from the Mauritius client's bank, via a correspondent institution, to the UK EMI, and is credited to the offshore company's MUR balance within 1–2 business days of settlement.

MUR is settled via SWIFT, not SEPA. Mauritius operates an IBAN system but is not part of the SEPA zone; MUR payments do not use SEPA payment rails. Finance teams expecting same-day SEPA-style settlement should plan for SWIFT timelines of T+1 to T+2 for MUR transactions.

Common Mistakes When Setting Up a MUR Account for an Offshore Company

Most Mauritian rupee business account applications from offshore companies are delayed, not rejected outright, because of three recurring and avoidable documentation problems.

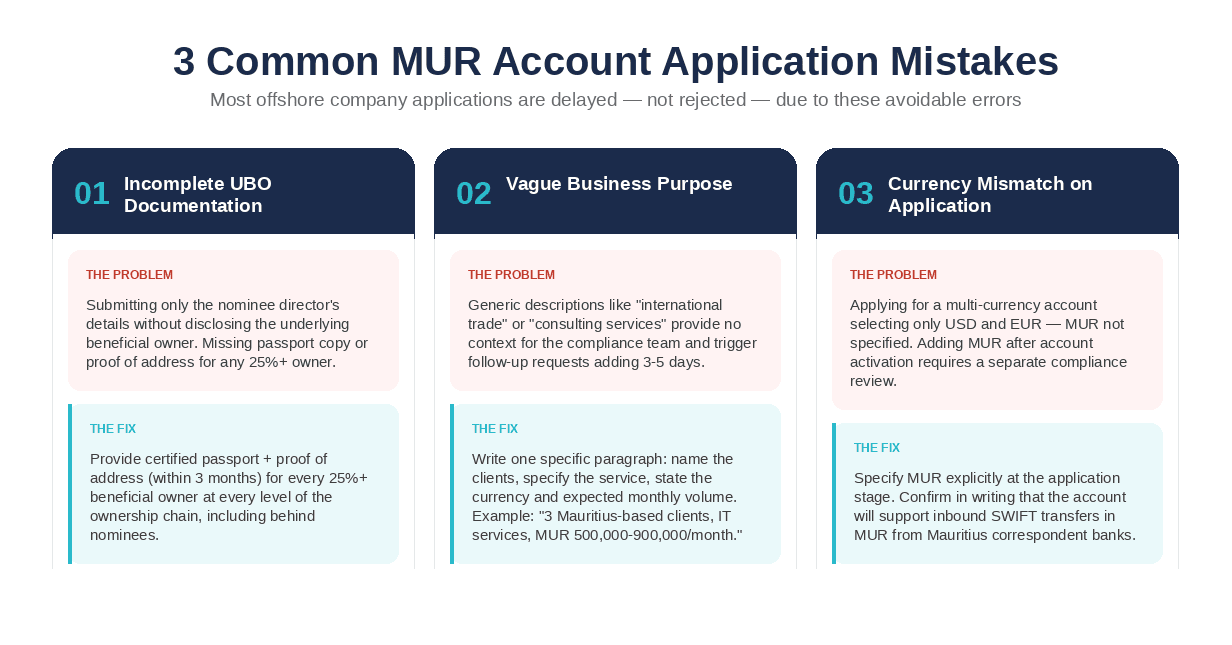

Incomplete UBO Documentation

Incomplete UBO disclosure is the most common cause of compliance holds. When a BVI or Seychelles company has layered ownership (a holding entity owning the operating entity), UBO documentation is required at every level of the structure, not only at the direct shareholder level. Each ultimate beneficial owner with 25% or more ownership must provide: a certified passport copy, proof of residential address dated within three months, and a signed UBO declaration.

Nominee structures require additional disclosure. The underlying beneficial owner's identity and documentation must still be provided, along with a copy of any nominee agreement in place. Submitting only the nominee's details without the underlying principal's identification will result in a compliance hold in every case.

Vague or Missing Business Purpose Description

A generic business purpose such as "international trade," "investment holding," or "consulting services" provides insufficient context for EMI compliance teams reviewing an offshore company Mauritian rupee payment use case. The description must specify: who the clients are, what service or product is being provided, what currency and approximate volumes are expected, and why those clients are paying in MUR rather than in USD or EUR.

Finance teams that invest ten minutes in a one-paragraph payment flow description before applying consistently move through compliance faster than those who provide a single-line business category.

Currency Mismatch on Application

Applying for a multi-currency account without explicitly requesting MUR as a required currency is a preventable friction point. If the onboarding form lists supported currencies and the applicant selects only USD and EUR, the account is configured accordingly. Adding MUR access after account activation may require a separate compliance review, adding days to what could have been resolved at the outset.

Specify MUR explicitly at application stage. Confirm in writing that the account will support inbound SWIFT transfers in MUR from Mauritius correspondent banks.

What Happens After You Receive MUR — Conversion and Management

Once MUR is credited to the account, offshore companies can hold the balance, convert it to another currency, or initiate outbound MUR payments to Mauritius-based suppliers, all within the same multi-currency account structure. For finance teams managing how to receive MUR as an offshore company, the post-receipt options are as important as the account setup itself.

Converting MUR to USD, EUR, or GBP

MUR-to-USD and MUR-to-EUR conversions are available within the account. Settlement timelines for MUR currency pairs reflect their exotic classification: T+1 to T+2 is standard. The Bank of Mauritius monetary policy framework operates a managed float system for MUR; the rupee is not freely floating, and exchange rates are managed within a band against a basket of major currencies. Finance teams should account for this when modelling FX outcomes on large MUR balances.

Companies with regular MUR receipts from Mauritius clients, a common structure for offshore company MUR conversion to USD and EUR, can schedule conversions to manage FX exposure across the managed-float band. Regular monitoring of the Bank of Mauritius rate announcements helps inform conversion timing.

Paying Mauritius-Based Suppliers from the Same Account

Outbound MUR payments via SWIFT are available from the same account that receives inbound MUR. For import-export companies, consultancies, and others operating in the Mauritius–Africa–Asia trade corridor, this means a single account structure handles both sides of MUR cash flows: receiving from Mauritius clients and paying local Mauritius suppliers.

This mirrors the model used by offshore companies accessing multiple currency corridors through a single UK-based payment account, managing cross-border currency requirements without maintaining accounts in multiple jurisdictions.

FAQ

How to receive MUR as an offshore company without a Mauritius bank account

Offshore companies can receive MUR through an FCA-authorised UK electronic money institution (EMI) without holding a Mauritius bank account. The process involves confirming that the EMI supports MUR as a receivable currency, submitting a KYB document pack, completing compliance review (typically 2–3 business days), and sharing the resulting SWIFT BIC and account reference with Mauritius-based clients. Those clients initiate standard local bank transfers in MUR; the EMI credits the balance to the offshore company's multi-currency account within 1–2 business days of SWIFT settlement. Not all UK EMIs support MUR; verify the currency list before applying.

What documents does a Seychelles company need to open a MUR account?

The KYB documentation for a Seychelles company MUR payment account includes: Certificate of Incorporation (locally notarised), Memorandum and Articles of Association, Register of Directors, Register of Shareholders, a UBO declaration with passport copy and proof of address for each beneficial owner holding 25% or more, and proof of business activity (contracts, invoices, or a company website). Seychelles documents typically require local notarisation rather than an apostille under the Hague Convention; confirm the exact standard with the EMI's onboarding team before preparing the pack. Multi-layer ownership structures require disclosure at every level of the ownership chain.

How long does it take to open a MUR account for an offshore company?

With a complete document submission, compliance review at a UK EMI takes 2–3 business days. Total onboarding time, from application to receiving SWIFT account details, is typically 3–5 business days. Incomplete submissions reset the review queue and add 3–7 days. By contrast, Mauritius commercial banks take 4–8 weeks for non-resident corporate applications, with many applications declined without detailed explanation. The UK EMI route is the most practical channel for opening a MUR account as a non-resident company on a defined timeline.

Why was my offshore company's MUR account application rejected?

The most common rejection reasons are: incomplete UBO documentation (missing a beneficial owner's passport or proof of address), a vague or generic business purpose statement, and currency mismatch (applying for a USD or EUR account without specifying MUR). Applications that fail to receive MUR in Mauritius without a local bank account through a traditional banking channel can be resubmitted through a UK EMI using a separate application process. Preparing a specific, named payment flow description, including client names, currency, approximate volumes, and commercial context, significantly reduces the risk of a second delay.

How does a BVI or Seychelles company receive MUR from Mauritius clients via UK EMI account?

Once a MUR-capable account is activated at a UK EMI, the company shares its SWIFT BIC and account reference with each Mauritius client. The client initiates a local MUR bank transfer from their Mauritius commercial bank. That payment routes through correspondent banking infrastructure: from the originating Mauritius bank, via an intermediary correspondent, to the UK EMI's correspondent institution, and is credited to the offshore company's MUR account balance within 1–2 business days of SWIFT settlement. The offshore company can then hold the MUR balance, convert it, or initiate outbound MUR payments to Mauritius-based suppliers from the same account.

Setting up a MUR account as an offshore company in Mauritius once meant navigating commercial bank requirements that effectively excluded BVI and Seychelles structures without local presence. The UK EMI route changes this calculus. An FCA-authorised EMI can hold MUR for offshore companies, credit inbound SWIFT transfers from Mauritius clients, and convert balances to USD, EUR, or GBP within the same account, without requiring physical presence, a local director, or a minimum deposit.

The setup process is direct: confirm MUR support with the EMI, submit a complete KYB document pack, clear compliance review, and share SWIFT receiving details with Mauritius counterparties. Finance teams looking to open a MUR account for an offshore company and start receiving MUR payments without a local bank account can begin the application process at client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)