•

•

Personal Account for Non-Residents Receiving HKD: Hold Hong Kong Dollars Abroad

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A growing number of professionals earn Hong Kong dollars while living somewhere else. A remote employee on a Hong Kong payroll, a freelancer billing a Hong Kong studio, a founder drawing dividends from a Hong Kong company: all of them need a way to receive HKD without setting foot in a local branch. The problem is that a personal account that lets non-residents receive HKD and hold Hong Kong dollars abroad rarely comes from a Hong Kong bank. Most local banks expect residency or an in-person visit, so the practical answer is a multi-currency account from a regulated payment provider. This guide explains how non-residents can receive Hong Kong dollars without a Hong Kong bank account, how the money actually arrives, what protects it, and who qualifies to open one.

[aa key-takeaways]

Key Takeaways

Non-residents generally cannot open a personal Hong Kong bank account, because local banks require residency or an in-person visit.

A non-resident HKD account is usually a multi-currency account from a regulated electronic money institution (EMI), not a high-street bank.

Inbound HKD typically arrives through SWIFT or local payment details, then sits in the account until the holder decides to convert.

Because the Hong Kong dollar is pegged to the US dollar, the main cost is the FX spread on conversion, not exchange-rate swings.

Regulation matters: an FCA-authorised EMI safeguards client funds in segregated accounts, though e-money is not covered by the FSCS.

[aa btn]Book a Call[/aa]

[/aa]

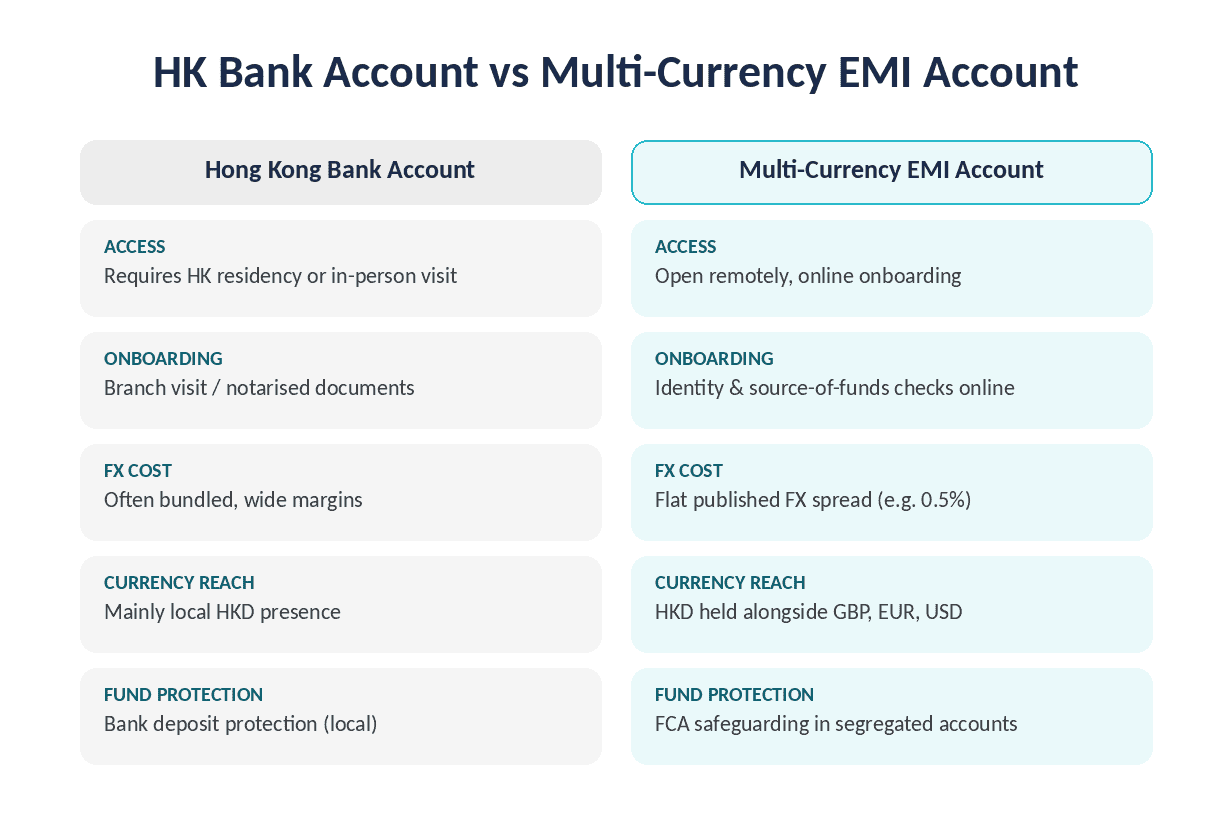

Why non-residents struggle to receive HKD without a Hong Kong bank account

Hong Kong banks generally require residency, a local address, or an in-person visit, so non-residents rarely qualify for a personal HKD account. The city remains one of the world's largest financial centres, yet its retail banks apply strict onboarding rules shaped by anti-money-laundering supervision from the Hong Kong Monetary Authority (HKMA). For someone living in London, Lisbon, or Dubai, a trip to a Hong Kong branch is not a realistic step before the first salary lands.

Several barriers stand between a non-resident and a local account:

Residency proof: most Hong Kong banks ask for a local address and, often, a Hong Kong ID.

In-person onboarding: branch visits or notarised documents are common for non-residents.

High minimums and reviews: personal accounts may carry balance requirements and periodic activity checks.

The currency itself adds a useful nuance. The Hong Kong dollar trades inside a narrow band against the US dollar under the HKMA's Linked Exchange Rate System, held between 7.75 and 7.85 HKD per USD since 2005. Day-to-day volatility is therefore small. For a non-resident, that changes the maths: the real cost of receiving Hong Kong dollars is rarely the exchange rate moving against them, but the fees and FX margin charged when the money is forced through conversion.

What a non-resident personal account for HKD actually is

A non-resident HKD account is a multi-currency account, usually provided by a regulated electronic money institution (EMI), that can receive and hold Hong Kong dollars without a local bank. It is not a Hong Kong bank account, and it does not pretend to be one. Instead, it gives the holder currency balances and payment details that let HKD arrive from abroad, sit in the account, and convert on the holder's timing.

This category sits between two familiar things. It offers the everyday function people expect from a bank, receiving income and holding a balance, while running on the regulated payment infrastructure that fintech providers such as Wise, Airwallex, and Currenxie also use. EQWIRE operates the same way for professionally active individuals, with the Hong Kong dollar sitting inside a 66-currency network. A non-resident treats it as a place to gather HKD income alongside GBP, EUR, and USD in one view.

Multi-currency EMI accounts vs traditional Hong Kong bank accounts

The clearest difference is access. A Hong Kong bank account demands a local footprint; a multi-currency account HKD setup from an EMI can be opened remotely, with identity and source-of-funds checks done online. A bank account gives a domestic Hong Kong presence, which suits residents and local businesses. An EMI account gives reach across currencies and borders, which suits someone whose life or work spans more than one country.

Cost structure differs too. Traditional accounts can bundle charges into maintenance fees and wide FX margins, while regulated EMIs tend to publish a flat FX spread and per-transfer pricing. For a non-resident who mainly needs to collect HKD and convert it cleanly, the second model is easier to predict. Those weighing the two routes can read EQWIRE's comparison of a FCA-authorised EMI against a popular fintech alternative.

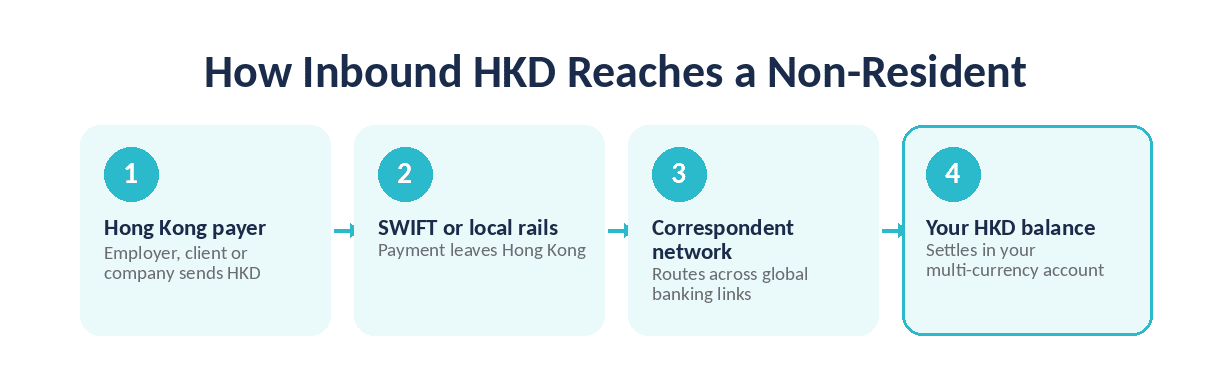

How inbound HKD payments reach a non-resident abroad

Inbound HKD typically arrives through SWIFT or through local payment details provided by the account. When a Hong Kong employer or client sends Hong Kong dollars, the payment routes across the correspondent banking network that the Bank for International Settlements describes in its payment systems data. The funds then settle into the holder's multi-currency account and appear as an HKD balance.

The holder shares account details once, and the payer treats each transfer as a standard international payment. EQWIRE's currency network settles Hong Kong dollar payments on a T+1 value date, with a 14:30 UK cut-off, so a payment submitted before the cut-off clears the next business day. The mechanics mirror how UK exporters already handle the currency, covered in EQWIRE's guide to receiving HKD payments in a business account.

[aa fast-fact]

Fast Fact: The Hong Kong dollar has been pegged to the US dollar within a 7.75–7.85 band since 2005, one of the longest-running currency pegs in the world.

[/aa]

How to receive and hold Hong Kong dollars abroad, step by step

Setting up a personal account for non-residents to receive HKD and hold Hong Kong dollars abroad follows a short, repeatable sequence. The process is built around remote onboarding, so no Hong Kong visit is required.

Open a multi-currency account with a regulated provider that supports HKD and accepts non-residents.

Complete identity and source-of-funds checks online, including proof of where the Hong Kong dollar income comes from.

Collect the account's payment details for receiving HKD from abroad.

Share those details with the Hong Kong payer (an employer, client, or company paying dividends).

Receive the HKD balance once each transfer settles.

Hold or convert the funds, choosing the moment and the target currency.

Setting up the account and currency details

The first balance is the foundation. Once the multi-currency account HKD profile is active, the provider issues the details a payer needs to send Hong Kong dollars. A holder receiving other currencies as well, say GBP from a UK client or EUR from a European one, manages them from the same dashboard. This single-view approach is the same one EQWIRE describes for people who hold multiple currencies in one account rather than juggling separate logins.

Accuracy at this stage prevents delays. A payer who keys in the wrong reference or routing detail can trigger a returned payment, so most providers display the exact fields to copy. For recurring HKD salary, the holder enters the details once with the employer's payroll team and leaves them in place.

Receiving HKD and choosing when to convert

The advantage of holding HKD is timing. Money received from abroad does not have to convert the moment it lands; it can stay as a Hong Kong dollar balance until the holder needs another currency. Because the peg keeps HKD stable against the US dollar, the decision is less about catching a rate and more about avoiding repeated conversion costs.

When conversion does happen, the FX spread is the number that matters. EQWIRE applies a 0.5% spread, so a holder can estimate the cost of moving HKD into GBP, EUR, or USD before confirming. Someone receiving a regular foreign-currency income will recognise the pattern from EQWIRE's walkthrough on receiving a foreign-currency salary into a UK account.

[aa cta]

Receive and Hold HKD Without a Hong Kong Bank Account

Open a multi-currency personal account, share your details with a Hong Kong payer, and hold Hong Kong dollars until conversion suits you.

[aa btn]Create Account[/aa]

[/aa]

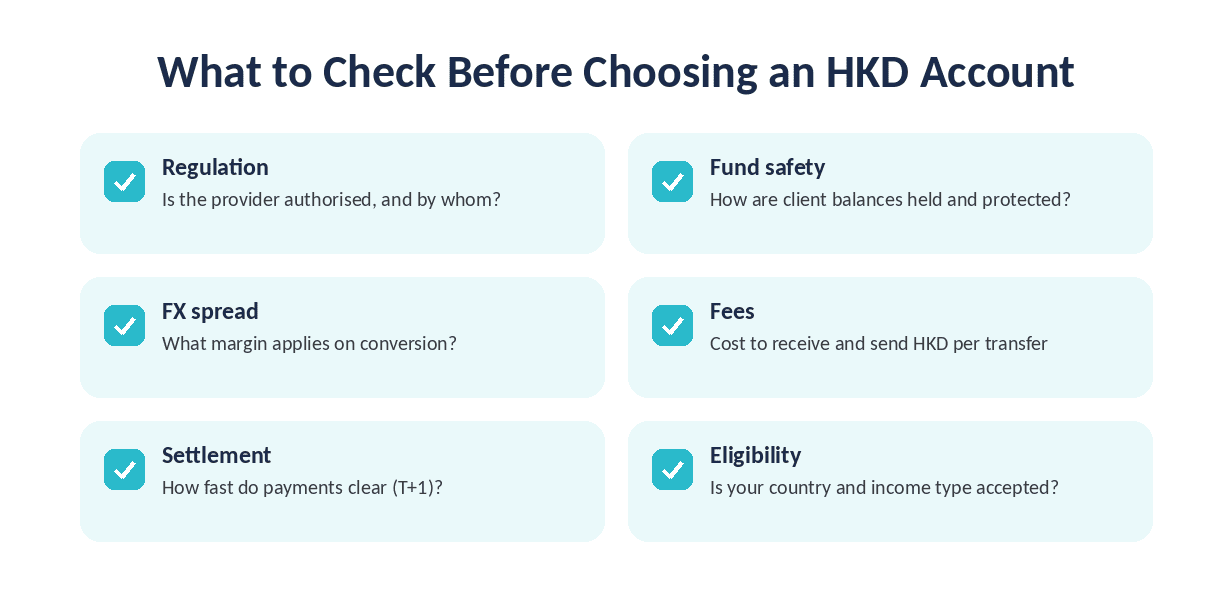

What to check before choosing an HKD-capable account

Not every provider that lists HKD treats it the same way, so a non-resident should compare on a few concrete points rather than on marketing claims. The aim is a setup that meets the standards expected of a regulated provider, receives reliably, and converts at a clear price.

A short checklist covers most of the decision:

Regulation: is the provider authorised, and by whom?

Fund safety: how are client balances held and protected?

FX spread: what margin applies on conversion, and is it published?

Fees: what does receiving and sending HKD cost per transfer?

Settlement: how fast do inbound and outbound payments clear?

Eligibility: does the provider accept the holder's country and income type?

Regulation and fund safeguarding (FCA, EMI rules)

Regulation is where a held HKD balance is either protected or exposed. In the UK, an electronic money institution must be authorised by the Financial Conduct Authority, and its status can be confirmed on the FCA Financial Services Register. EQWIRE is an FCA-authorised EMI (firm reference number 901100), which a holder can verify directly rather than take on trust.

Authorisation brings a specific duty. Under the Electronic Money Regulations 2011, an EMI must safeguard client money in segregated accounts kept separate from its own funds. One limitation is worth stating plainly: e-money is not covered by the Financial Services Compensation Scheme, so the protection comes from safeguarding rather than deposit insurance. The FCA explains what authorisation means for consumers using a payment provider, and that distinction should shape expectations.

Fees, FX spread, and settlement times

Pricing decides how much of the HKD income survives the journey. Providers such as Wise, Airwallex, Currenxie, and WorldFirst each publish their own receiving fees and FX margins, and the gap between a transparent spread and a hidden one can be significant on recurring payments. A flat, visible spread makes the cost of receiving HKD from abroad predictable month to month.

Settlement speed is the second variable. EQWIRE's Hong Kong dollar payments carry a T+1 value date with a 14:30 UK cut-off, which tells a holder exactly when a payment submitted today will clear. Predictable timing matters for anyone planning around a salary or invoice cycle.

Who can open a non-resident HKD account (eligibility)

Eligibility is the step that most often surprises applicants, because a non-resident HKD account is not open to everyone by default. Regulated providers apply customer-acceptance rules based on country of residence, the nature of the income, and risk appetite. EQWIRE, for instance, offers personal accounts to professionally active individuals rather than to the general retail public, and does not facilitate crypto transactions.

In practice, a strong applicant can show clear, lawful HKD income: a Hong Kong employment contract, client invoices, or company dividend records. An expat receiving a Hong Kong salary, a freelancer with Hong Kong clients, or a founder taking distributions usually fits the profile, which is why an HKD account for expats and remote earners is a common use case. Applicants from sanctioned jurisdictions or with unverifiable sources of funds will not pass onboarding, and providers are required to decline them.

[aa cta]

Get Paid in HKD by a Hong Kong Employer

See how remote employees receive a foreign-currency salary and hold it across currencies without losing value to forced conversion.

[aa btn]Open Remote Employee Account[/aa]

[/aa]

FAQ

How to receive HKD salary without a Hong Kong bank account?

A non-resident can receive an HKD salary by opening a multi-currency account with a regulated electronic money institution that supports the Hong Kong dollar, then sharing that account's payment details with the employer's payroll team. The salary arrives through SWIFT or local payment rails and settles as an HKD balance, which the holder can keep or convert. No Hong Kong residency or branch visit is needed, because onboarding is completed online with identity and source-of-funds checks. EQWIRE settles HKD on a T+1 value date with a 14:30 UK cut-off, so a holder knows when each payment will clear.

Can a non-resident open a Hong Kong dollar account?

A non-resident generally cannot open a personal Hong Kong dollar account at a Hong Kong bank, because local banks require residency or an in-person visit. The practical alternative is a multi-currency account from a regulated provider, which can be opened remotely and can both receive and hold Hong Kong dollars. The Hong Kong Monetary Authority supervises local banks closely on anti-money-laundering grounds, which is why their onboarding rules are strict for people based abroad. An EMI account does not replace a Hong Kong bank account, but it covers the core need: receiving and holding HKD without a local presence.

Is the money safe in a non-resident HKD account?

Funds in an FCA-authorised electronic money institution are safeguarded in segregated client accounts, kept separate from the provider's own money under the Electronic Money Regulations 2011. This is different from bank deposit protection, because e-money is not covered by the Financial Services Compensation Scheme. Safeguarding means client balances are held so they can be returned even if the provider fails, but there is no government-backed insurance payout. A holder can confirm a provider's authorisation on the FCA register before opening an account, and EQWIRE publishes its firm reference number (901100) for that purpose.

What does it cost an expat or remote worker receiving HKD salary to hold Hong Kong dollars without a HK bank?

For an expat or remote worker receiving HKD salary, the main cost of holding Hong Kong dollars without a HK bank is the FX spread applied when converting, plus any per-transfer fees. Because the Hong Kong dollar is pegged to the US dollar within a 7.75–7.85 band, exchange-rate swings are small, so the conversion margin is the figure to compare. EQWIRE applies a 0.5% FX spread and charges £0 onboarding and maintenance for individuals, which makes the running cost easy to estimate. Holding HKD rather than converting on receipt also avoids paying that spread more than once.

Can someone hold Hong Kong dollars in the UK or EU?

Someone living in the UK or EU can hold Hong Kong dollars through a multi-currency account that supports HKD, without needing any Hong Kong banking relationship. The balance sits in the account as Hong Kong dollars and converts to GBP, EUR, or USD only when the holder chooses. This suits people with recurring HKD income who want to control conversion timing and cost. Providers apply their own eligibility rules, so acceptance depends on country of residence and the source of the HKD income.

A personal account for non-residents to receive HKD and hold Hong Kong dollars abroad solves a narrow but real problem: collecting Hong Kong dollar income when a local bank account is out of reach. The route runs through regulated multi-currency accounts rather than Hong Kong branches, with HKD arriving by SWIFT or local details and resting as a balance until conversion makes sense. Because the currency is pegged, the decision turns on fund safety and the FX spread rather than on timing the market. For professionals splitting their working lives across borders, that combination of regulated safeguarding, transparent conversion, and remote access is what makes holding Hong Kong dollars abroad practical. Expats and remote earners weighing their options can start with EQWIRE's account built for people living and working across countries, then open an account at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)