•

•

How to Receive HKD Payments as a UK-Based Exporter to Asia

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

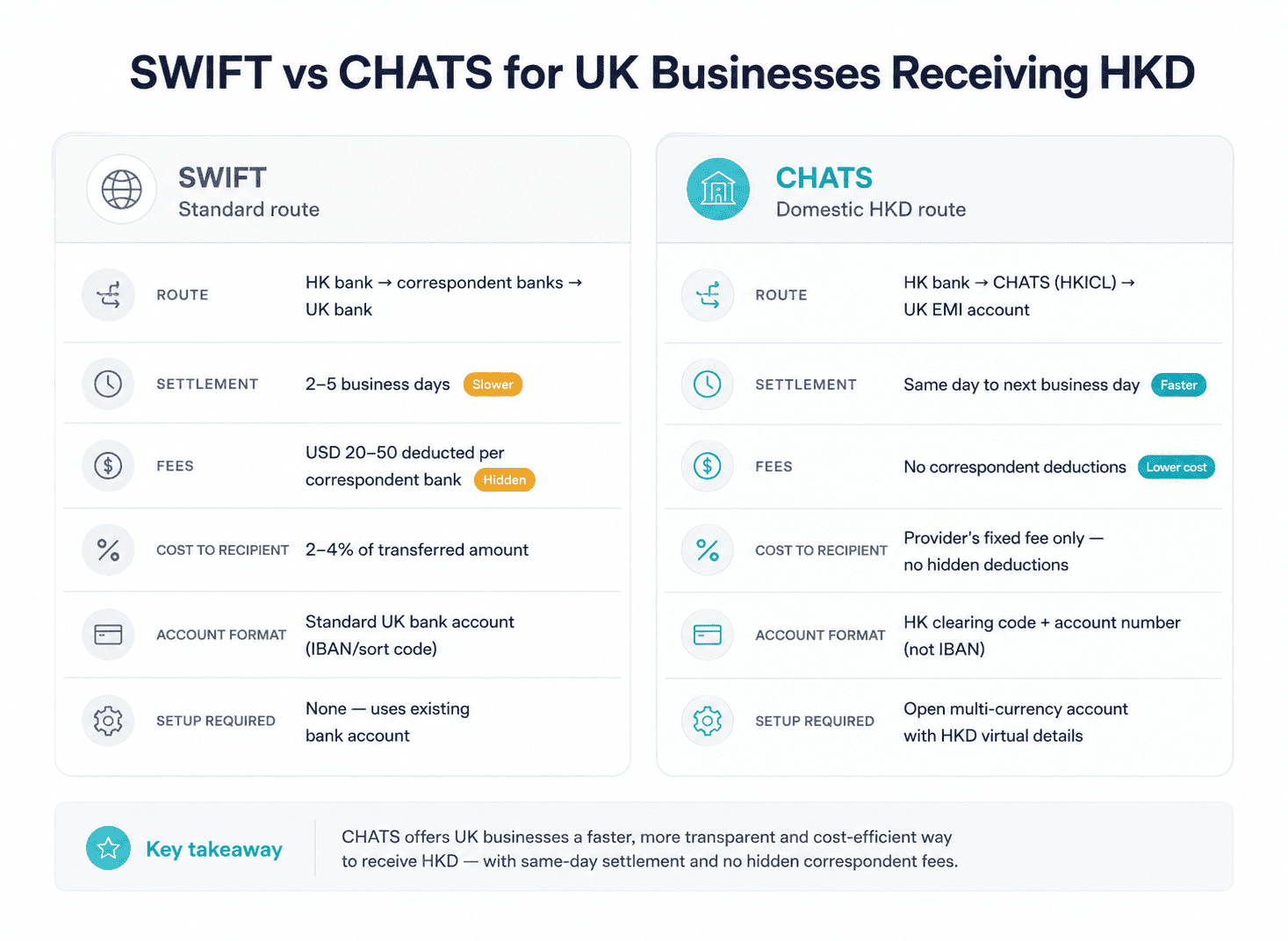

Sending a SWIFT payment from Hong Kong to a standard UK bank account costs the sending business a fixed outbound fee plus correspondent bank deductions of USD 20–50 per intermediary, with settlement taking two to five business days. For UK exporters billing Hong Kong clients regularly, those charges add up to 2–4% of the transferred amount on every invoice cycle, a cost that does not appear on any line item but arrives as a shortfall between invoiced and received amounts.

The solution is to receive HKD UK business account details issued by an FCA-authorised electronic money institution (EMI). These are virtual HKD account numbers that Hong Kong clients pay as a domestic transfer, routing funds through CHATS (Hong Kong's real-time settlement infrastructure) rather than the SWIFT correspondent chain. UK businesses can set up this structure without opening a bank account in Hong Kong. No travel or local registration is required.

[aa key-takeaways]

Key Takeaways

UK businesses can receive HKD from Hong Kong clients without a local bank account, using virtual HKD account details issued by an FCA-authorised EMI in the UK.

HKD transfers routed through CHATS (Clearing House Automated Transfer System) settle same-day to next business day, versus 2–5 days via SWIFT with correspondent deductions.

Setting up a UK multi-currency account that accepts HKD requires standard KYC documents only, with no travel to Hong Kong or local company registration required.

HKD accounts use a 3-digit Hong Kong bank clearing code, not an IBAN, as providing an IBAN to a Hong Kong client causes the payment to be rejected or returned.

Once HKD arrives in a multi-currency account, businesses can hold the balance or convert to GBP at a chosen rate, depending on supplier obligations and FX priorities.

[aa btn]Book a Call[/aa]

[/aa]

What UK Businesses Need to Know Before Setting Up HKD Receiving

UK businesses have two options for receiving HKD payments: routing them as international SWIFT transfers through a standard bank account, or opening an HKD multi-currency account with a UK-based EMI that issues a virtual local account number. The first option requires no setup but carries ongoing correspondent fees and conversion markups. The second requires a one-time onboarding process but eliminates those costs on every subsequent payment.

Why SWIFT Transfers Lose Value When Receiving HKD

When a Hong Kong client pays via SWIFT, the payment travels through the international correspondent banking network before reaching the UK recipient. Each correspondent bank in the chain deducts a handling fee (typically USD 20–50) directly from the principal. The UK business receives less than the invoiced amount, and the shortfall is not itemised anywhere.

The Bank for International Settlements has documented the structural costs of correspondent banking, noting that declining relationships in many corridors increase per-transaction costs for businesses without direct settlement access. For UK exporters receiving regular HKD income from Asia, this structure imposes a compounding cost. A business receiving ten invoiced payments per month at HKD 50,000 each can lose the equivalent of GBP 300–700 monthly in fees and FX markup, with no single charge appearing on the bank statement.

[aa fast-fact]

Fast Fact: The global average cost of sending $200 cross-border stood at 6.5% in Q1 2025 (FSB/G20 Roadmap data). For UK recipients, HKD-to-GBP SWIFT transfers typically carry a combined cost of 2–4% after correspondent deductions and conversion markup.

[/aa]

What a Virtual HKD Account Is

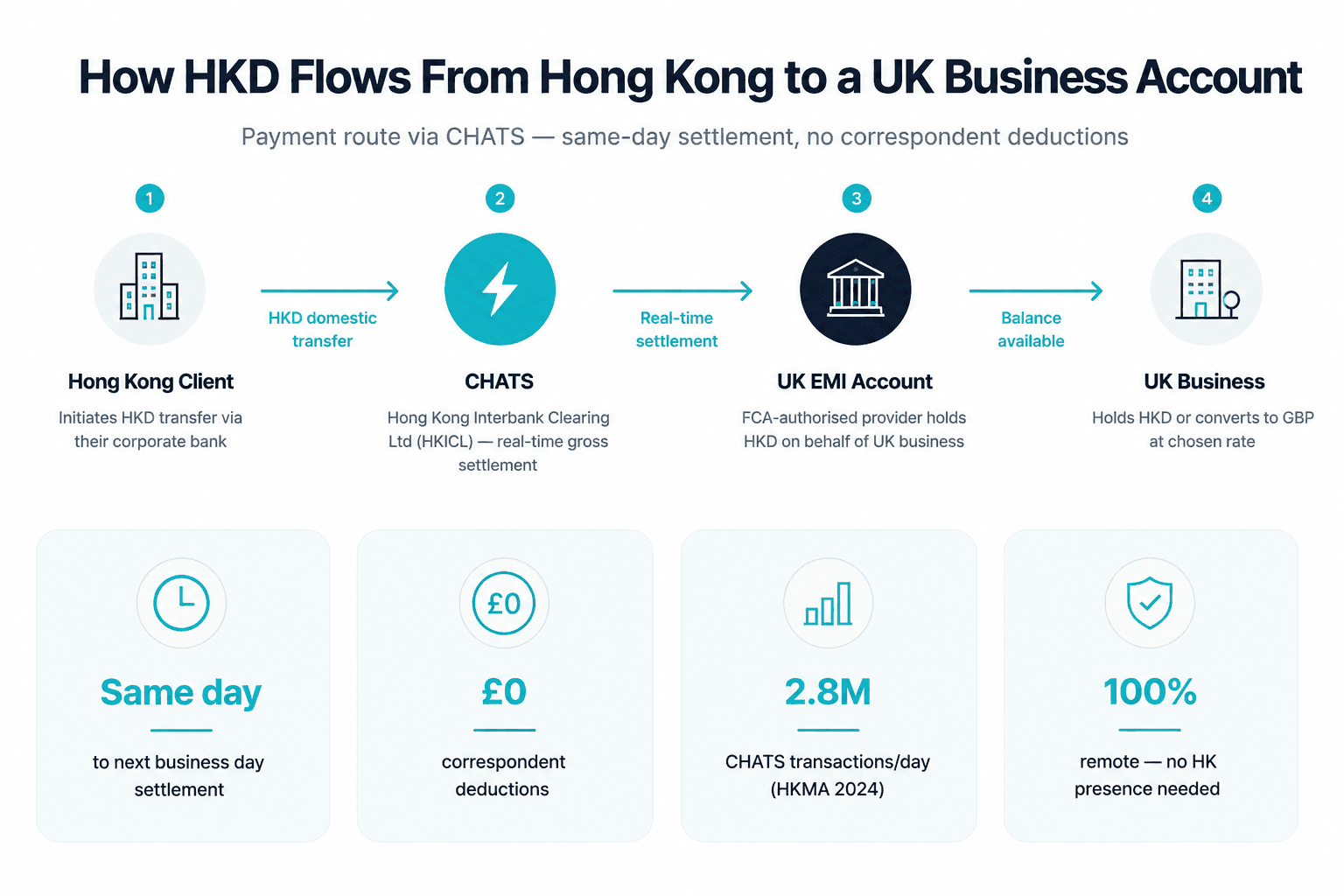

FCA-authorised electronic money institutions in the UK can issue real HKD account numbers linked to a UK-registered business. These accounts do not use an IBAN. Instead, they carry a 3-digit Hong Kong bank clearing code and an account number, identical in format to a domestic HK bank account from the sender's perspective.

When a Hong Kong client pays to these details, the payment routes through CHATS (Clearing House Automated Transfer System), operated by HKICL. CHATS is Hong Kong's real-time gross settlement system for HKD. According to the Hong Kong Monetary Authority, HKD CHATS processed an average of 2.8 million RTGS transactions per operating day in 2024, with an average daily settlement value of HK$1,156 billion. For CHATS-routed payments, settlement completes same-day to next business day, with no correspondent deductions.

What You Need Before You Start

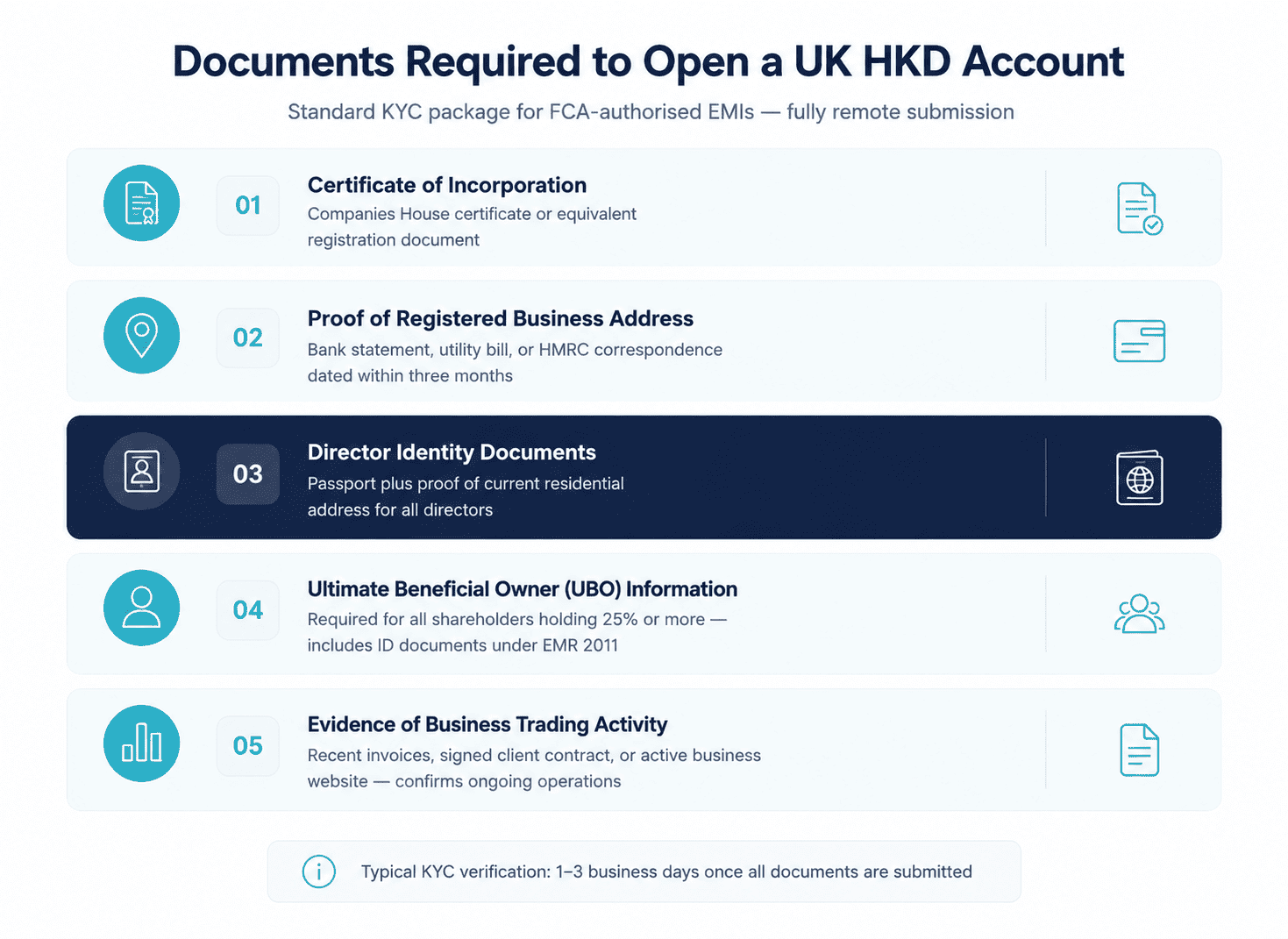

Opening a UK business account that accepts HKD requires standard KYC documentation submitted through a secure online portal. For UK-registered limited companies, the process is entirely remote, with no branch visits or in-person interviews.

Business Documents Required for a UK Multi-Currency Account

Certificate of incorporation (Companies House certificate or equivalent)

Proof of registered business address (bank statement, utility bill, or HMRC correspondence dated within three months)

Director identity documents: passport plus proof of current residential address

Ultimate Beneficial Owner (UBO) information for all shareholders holding 25% or more (including ID documents if the provider is an authorised EMI under the Electronic Money Regulations 2011)

Evidence of business trading activity: recent invoices, a signed supplier or client contract, or a business website confirming active operations

This is the standard documentation set across regulated UK EMI platforms authorised under the Electronic Money Regulations 2011. The FCA requires authorised institutions to apply appropriate due diligence to onboarded businesses, and source-of-funds checks become more detailed for accounts processing higher monthly volumes.

Eligibility and Common Reasons Applications Are Delayed

UK-registered limited companies actively trading with Asian markets qualify for HKD-capable accounts with most FCA-authorised providers. Applications are most frequently delayed by three issues:

Incomplete UBO documentation when the company has a layered holding structure

A registered address that does not match any submitted proof of address

No evidence of active trading

Businesses that prepare all five document categories before starting the onboarding process typically complete KYC verification within 1–3 business days.

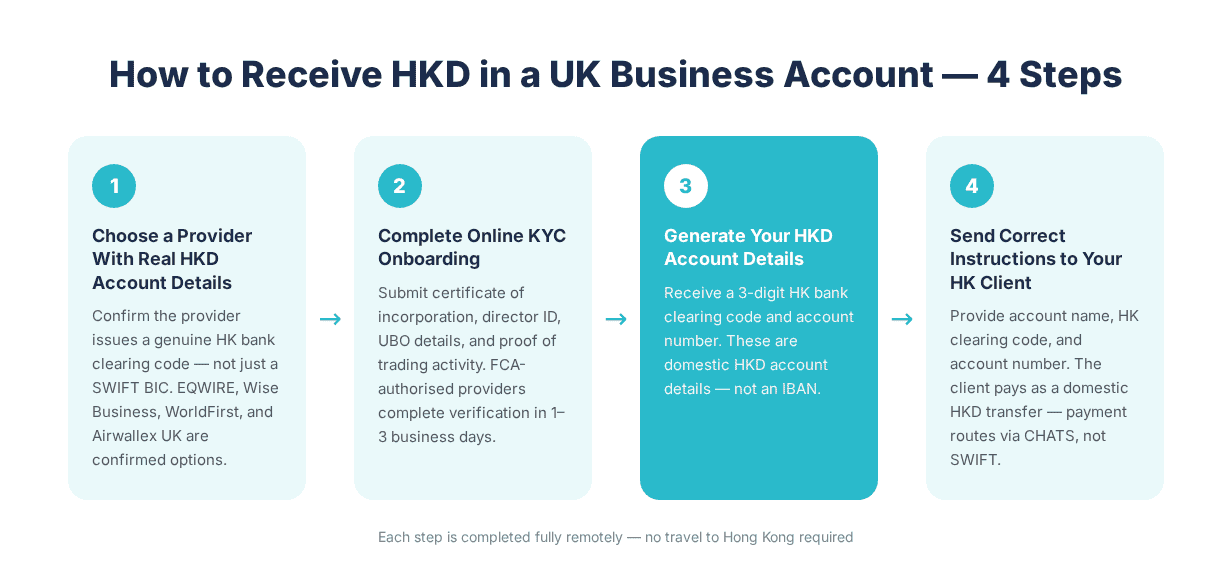

Step-by-Step: How to Receive HKD in a UK Business Account

UK SMEs receiving HKD from Hong Kong clients without opening a local account follow four steps, each entirely remote: choosing a provider that issues genuine virtual HKD account numbers, completing digital KYC onboarding, generating account details, and sending accurate payment instructions to the Hong Kong client.

Step 1 — Choose a Provider That Issues Real HKD Account Details

Not all UK multi-currency accounts issue genuine HKD account numbers. Some accept inbound SWIFT transfers denominated in HKD but convert the funds on arrival. The payment still routes through the SWIFT correspondent chain, and the UK business absorbs the associated fees. A genuine virtual HKD account carries a real Hong Kong bank clearing code and account number that Hong Kong clients pay as a domestic transfer.

Providers with confirmed HKD virtual account issuance include EQWIRE (FCA-authorised, UK-based with fully remote onboarding), Wise Business, WorldFirst, and Airwallex UK. The qualifying test is whether the account details include a domestic HK bank clearing code, not merely a SWIFT BIC. Providers set up similarly to how offshore companies access GBP sort codes through UK EMIs apply the same regulated structure to HKD virtual accounts.

Step 2 — Complete Online Onboarding and KYC Verification

All regulated UK providers conduct digital onboarding. The process involves submitting the document set through a secure portal, completing a director identity check (typically a short video verification or selfie alongside a passport scan) and confirming the intended business purpose of the account.

Providers under the Electronic Money Regulations 2011 (EMR 2011) must apply proportionate due diligence. Accounts with straightforward ownership structures and full documentation packages typically receive approval within 1–3 business days. UK businesses already using FCA-authorised EMI accounts for PSP payouts go through the same onboarding process for HKD capability.

Step 3 — Generate Your HKD Account Number and Routing Details

Once verified, the provider issues HKD account details:

Beneficiary name: the registered business name, exactly as it appears on the certificate of incorporation

HK bank clearing code: a 3-digit number identifying the provider's banking partner in Hong Kong

HKD account number: typically 9–12 digits, specific to the business's account

HKD accounts use Hong Kong's domestic banking format, not the IBAN structure used in Europe. The clearing code and account number are the two fields Hong Kong bank systems use to route a domestic HKD transfer. This is how to set up a UK business account to receive HKD from Hong Kong clients without opening an account in Hong Kong.

[aa cta]

Open a UK Business Account That Receives HKD

EQWIRE is FCA-authorised and issues virtual HKD account details for UK-registered businesses. Onboarding is fully remote and typically completes within 1–3 business days.

[aa btn]Create Account[/aa]

[/aa]

Step 4 — Send the Correct Payment Instructions to Your Hong Kong Client

A correct payment instruction includes the account name exactly as registered, the HK bank clearing code (3 digits), and the HKD account number. Optionally include the provider's SWIFT BIC for international routing fallback.

The client should not provide an IBAN. IBAN is a European account number format, and Hong Kong's banking system does not use it for domestic HKD transfers. A payment sent using an IBAN in place of HK account details will be rejected or returned.

What Happens When Your Hong Kong Client Pays

When a Hong Kong client transfers HKD to a virtual account number, the payment routes through CHATS (Hong Kong's real-time gross settlement system, operated by HKICL). The receiving UK EMI's account receives the funds in real time, and the balance appears in the business's multi-currency account typically within the same business day.

Settlement Times for HKD Received by a UK Business Account

CHATS-routed payments settle same-day to next business day. For UK exporters, this is a material improvement over SWIFT, which takes 2–5 business days and routes through correspondent intermediaries that each deduct a fee from the principal.

The Bank of England's cross-border payments oversight recognises that multi-leg SWIFT transfers remain the primary source of delay in international payment corridors. CHATS access via a UK EMI addresses this problem for HKD receipts specifically. Most major Hong Kong corporate banks process outbound CHATS transfers to virtual account numbers — HSBC HK and DBS HK are common examples. Where CHATS is unavailable, the payment reverts to SWIFT.

[aa fast-fact]

Fast Fact: HKD CHATS processed an average of 2.8 million RTGS transactions per operating day in 2024, with a daily settlement value of HK$1,156 billion (HKMA, 2024).

[/aa]

Managing HKD After It Arrives

For UK exporters who receive HKD Asia payments on a recurring basis, the decision of when and whether to convert to GBP depends on the business's supplier obligations and approach to FX exposure.

Holding HKD vs Converting to GBP Immediately

Holding HKD allows businesses to pay Hong Kong or mainland China suppliers directly, avoiding a round-trip HKD-to-GBP-to-HKD conversion. The HKMA maintains the Hong Kong dollar within a tight USD 7.75–7.85 currency peg, providing meaningful rate stability for planning purposes.

Converting immediately offers simplicity: the GBP value of each received invoice is fixed at the point of receipt. Most UK multi-currency accounts supporting HKD allow both approaches — the balance is held by default until a manual conversion is triggered.

FX Timing for Exporters With Regular HKD Income

Businesses receiving HKD on a predictable monthly cycle can reduce total conversion costs by batching conversions. Each conversion carries a spread, so fewer, larger conversion events at chosen rate points reduce the cumulative cost. Some providers offer rate alerts, allowing the finance team to set a target rate and convert automatically.

Common Mistakes UK Businesses Make When Receiving HKD

Providing an IBAN instead of HK account details is the most frequent error. An IBAN is not a valid format for the HK client's domestic banking system. The payment is typically returned or held pending correction.

Choosing a provider that converts HKD on arrival rather than issuing a genuine virtual account means the payment still travels via SWIFT, and correspondent deductions apply.

Not verifying the provider's FCA authorisation before opening an account. UK businesses can check the FCA register of electronic money and payment institutions before proceeding. Similar logic applies to related structures: businesses obtaining UK bank details through an EMI without a local office and those accessing EUR IBAN accounts through UK-based providers follow the same verification principle.

Converting every HKD receipt to GBP immediately without assessing whether Asian supplier payments can be made in HKD directly creates unnecessary round-trip conversion costs.

Providing a beneficiary name that differs from the registered business name on the account causes reconciliation failures and delays settlement.

FAQ

Can a UK SME receive HKD from Hong Kong clients without opening a local account?

Yes. FCA-authorised electronic money institutions in the UK issue virtual HKD account numbers linked to a UK-registered business. The Hong Kong client pays to these details as a standard domestic HKD transfer, and the funds arrive in the UK business's multi-currency account without SWIFT correspondent fees or deductions. No Hong Kong registration, local office, or in-person bank visit is required.

How do I send the correct payment instructions to my Hong Kong client?

Provide the beneficiary account name as registered with the provider, the HK bank clearing code (a 3-digit number), and the HKD account number issued after onboarding. Do not send an IBAN. HKD accounts use Hong Kong's domestic banking format, not the European IBAN structure. An IBAN sent for an HKD domestic transfer will typically be rejected or returned by the sender's bank.

What happens if my Hong Kong client sends HKD via SWIFT instead of through CHATS?

The payment will arrive, but it will route through correspondent banks rather than CHATS. Each correspondent intermediary may deduct USD 20–50 from the principal, and settlement can take 2–5 business days. Confirming with the client that their bank can process the payment as a CHATS domestic transfer avoids this outcome in most cases.

How long does KYC verification take to open a multi-currency account in the UK?

Most FCA-authorised providers complete KYC within 1–3 business days once all documents are submitted in full. Required documents typically include a certificate of incorporation, proof of registered address, director identity documentation, and evidence of active business trading.

Is there a minimum transaction size for receiving HKD into a UK business account?

Most multi-currency accounts have no minimum for incoming HKD transfers, but some providers charge a small fixed fee per received payment. Reviewing the provider's fee schedule before account opening avoids unexpected per-transaction charges.

UK exporters with Hong Kong clients no longer need a local banking presence to receive HKD UK business account payments efficiently. FCA-authorised EMIs issue virtual HKD account details that route through CHATS for same-day settlement without correspondent deductions. The key operational requirement is accuracy: providing the HK clearing code and account number rather than an IBAN, and ensuring the beneficiary name matches the registered account exactly.

EQWIRE provides a multi-currency account with HKD capability for UK-registered businesses, with fully remote onboarding. Finance teams can open an account and receive virtual HKD account details without travel or local registration.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)