•

•

Payment Account for SaaS Companies: GBP, EUR and Contractor Payouts

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

Wise works well for small teams paying occasional contractors. Revolut Business handles domestic GBP efficiently. But when you're running £50k+ monthly payout cycles across GBP and EUR — receiving subscription revenue from Stripe and settling contractor invoices within days — the question is no longer "which app should I use?" It's "what SaaS payment infrastructure do I actually need?"

Use the wrong account structure and you're paying £15–£30 per EUR contractor transfer through SWIFT, waiting 2–3 days for settlement, and reconciling two platforms every month-end. That's a structural cost, not a fintech preference.

A dedicated UK EMI account with Faster Payments for GBP and direct SEPA access for EUR is the most cost-efficient SaaS payment infrastructure for companies paying global contractors from the same multi-currency balance. This article compares the rails, account types, and providers.

[aa key-takeaways]

Key Takeaways

SaaS payment infrastructure for GBP and EUR contractor payouts requires Faster Payments and SEPA access under one account — not two separate platforms

SWIFT-based EUR payouts cost £15–£30 per transfer; SEPA Credit Transfer fees are typically under £1 — the rail choice drives total payout cost

EMI accounts regulated by the FCA ring-fence client funds via safeguarding — structurally different from a standard UK business bank account

Batch payout tools (CSV upload via Faster Payments and SEPA) are the operational differentiator for SaaS companies managing recurring contractor cycles at volume

SaaS treasury automation means collecting GBP subscription revenue and paying GBP/EUR contractors from the same multi-currency balance — eliminating forced FX conversion

[aa btn]Open an Account[/aa]

[/aa]

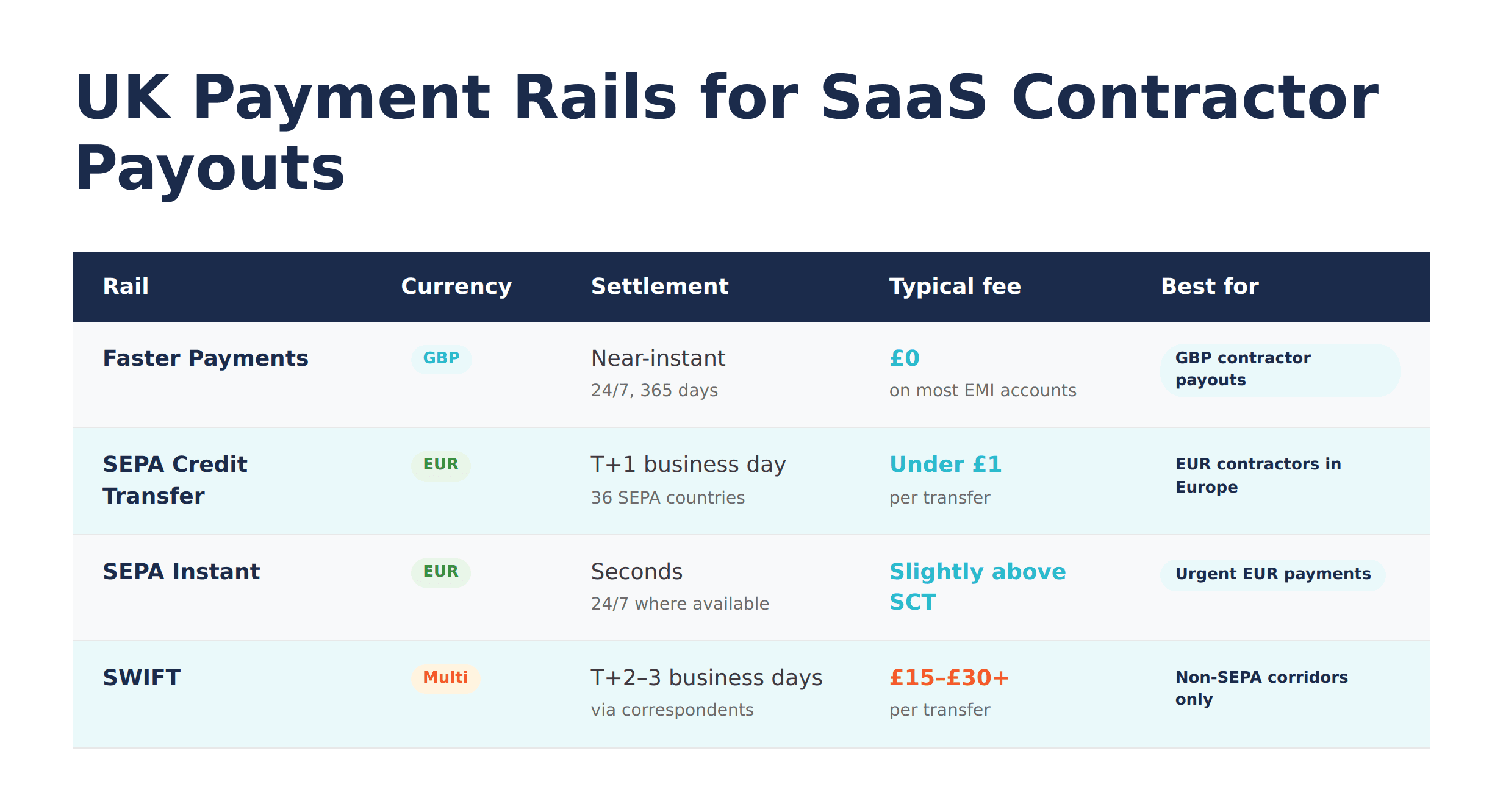

Faster Payments vs SWIFT vs SEPA: Which Rail for SaaS Contractor Payouts

The payment rail determines cost, speed, and operational complexity. Most SaaS finance teams know the names — but conflate them when it matters most. Here is what separates them for contractor payouts UK GBP EUR Faster Payments decisions.

Rail | Currency | Settlement | Typical fee | Best for |

|---|---|---|---|---|

Faster Payments | GBP | Near-instant (24/7) | £0 on most EMI accounts | Domestic GBP contractor payouts |

SEPA Credit Transfer | EUR | T+1 business day | Under £1 | EUR contractors across 36 SEPA countries |

SEPA Instant | EUR | Seconds (24/7) | Slightly above SCT | Urgent EUR payments |

SWIFT | Multi-currency | T+2–3 business days | £15–£30+ per transfer | Non-SEPA international corridors |

The cost gap between SWIFT and SEPA is not marginal. It compounds every month.

GBP Contractor Payouts: Faster Payments vs CHAPS

Faster Payments operates 24 hours a day, 365 days a year, settling domestic GBP payments near-instantly. For SaaS companies running weekly or monthly GBP contractor payout cycles, this is the correct rail — no per-transaction fee on most FCA-authorised EMI accounts, and individual payment limits typically reaching £1 million per transaction via the scheme.

CHAPS is same-day but carries a higher per-transaction fee and is designed for high-value single payments — property, corporate settlements. For recurring contractor invoices in the £500–£5,000 range, CHAPS overhead is unnecessary.

EUR Contractor Payouts: SEPA Credit Transfer vs SWIFT

SEPA Credit Transfer settles EUR payments in T+1 across 36 SEPA member countries, using IBAN as the primary identifier. SEPA Instant settles in seconds. Both carry fees well under £1 per transfer on most EMI platforms.

SWIFT routes through correspondent banks — each adding a handling fee of £15–£30 cumulative — and takes 2–3 business days. For EUR contractors based anywhere in the SEPA area, SWIFT is the wrong rail. The cost is entirely avoidable.

The critical constraint: SEPA access from a UK account requires the provider to hold direct or indirect participation in the SEPA scheme. Not all UK EMIs offer this. Without it, EUR payments default to SWIFT routing regardless of destination.

[aa fast-fact]

Fast Fact: Paying 8 EUR contractors monthly via SWIFT at £25 per transfer costs £200/month — or £2,400/year — in avoidable fees. The same 8 SEPA payments cost under £8/month. Annual saving: £2,300+, without changing the payout workflow.

[/aa]

EMI Account vs Traditional Bank: What Changes for SaaS Payment Infrastructure

Many SaaS founders assume a high-street business bank account is sufficient. For a small team paying two contractors in GBP, that assumption holds. For a growing company receiving Stripe payouts in GBP, holding EUR from EU customers, and running monthly payout cycles to contractors across Europe — it doesn't.

This is where the payment account for SaaS companies UK question becomes structural, not preferential.

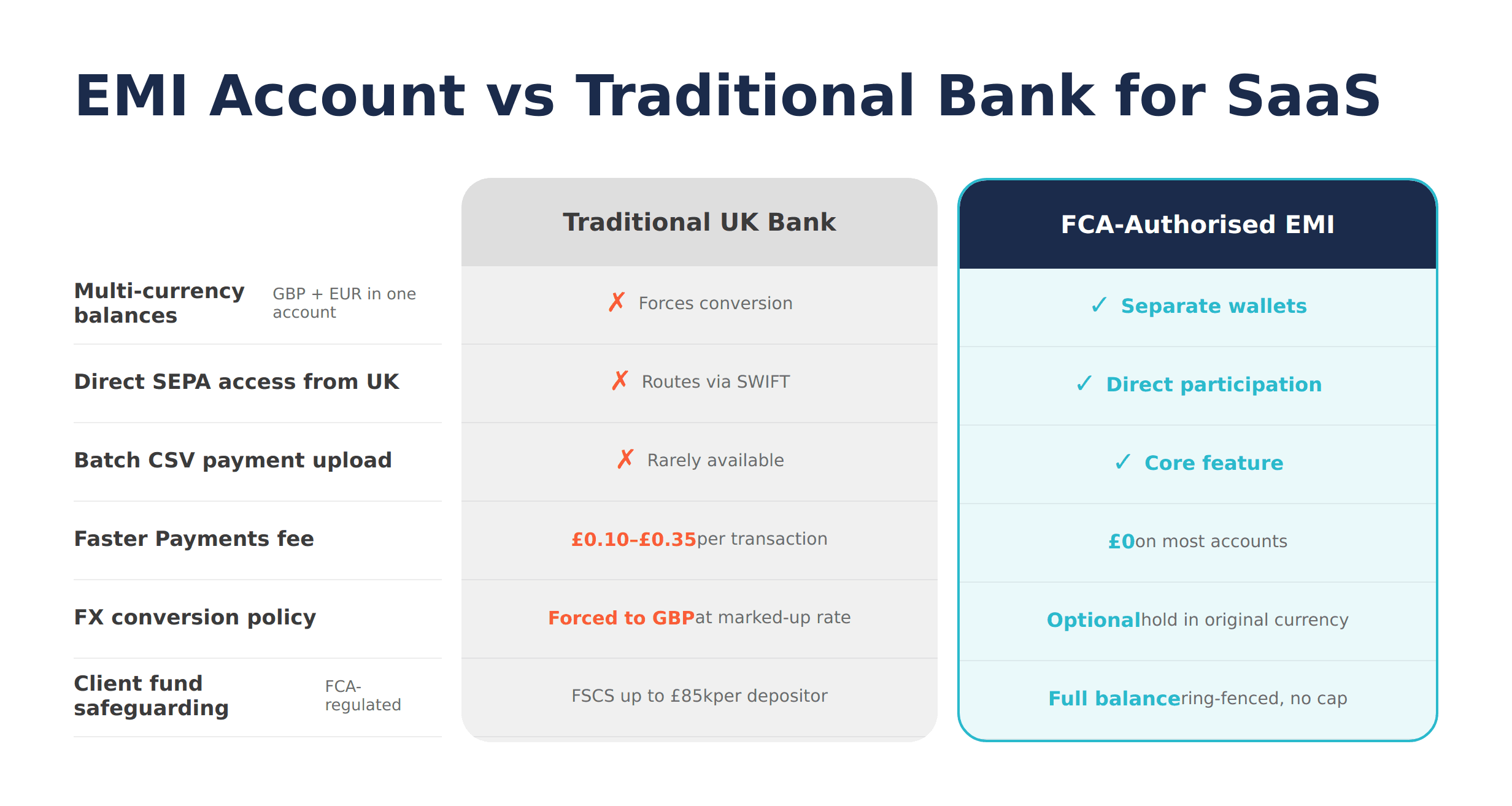

Safeguarding and FCA Regulation

Under the UK Electronic Money Regulations 2011, FCA-authorised EMIs must safeguard client funds. Client money is held separately from the EMI's own capital — in a designated safeguarding account at a credit institution, or covered by an insurance policy. If the EMI becomes insolvent, those funds are ring-fenced.

UK bank accounts carry FSCS protection up to £85,000 per depositor. EMI safeguarding protects the full balance without a cap — but within a different regulatory framework. The FCA register confirms which providers hold full authorisation versus registration. SaaS companies scaling treasury volume should confirm their provider's status before routing significant balances.

Feature Comparison: Batch Payouts, API Access, Multi-Currency Balances

Feature | Traditional UK Bank | FCA-Authorised EMI |

|---|---|---|

Multi-currency balances (GBP + EUR) | Rarely available; usually forces conversion | Standard — separate currency wallets |

Direct SEPA access from UK | Not available at most high-street banks | Available (provider-dependent) |

Batch CSV payment upload | Limited or unavailable | Core feature on most EMI platforms |

Per-transaction fee (Faster Payments) | Often £0.10–£0.35 per payment | Often £0 on EMI accounts |

FX conversion policy | Forced on incoming foreign currency | Optional — hold in original currency |

When a Bank Account Is Not Enough

Here is where the money is lost. A UK SaaS company receives £120k monthly from Stripe in GBP. Eight EUR contractors invoice monthly. The finance team uses the company's main bank for GBP and Wise for EUR payouts — two logins, two reconciliation streams.

Each EUR payment via the bank routes through SWIFT: £25 × 8 = £200/month, plus 2-day settlement delays. Wise handles EUR better but lacks a named UK IBAN for Stripe settlement and doesn't support CSV batch upload at the volume needed.

Switching to a single FCA-authorised EMI account with Faster Payments and SEPA: EUR contractor fees drop to under £8/month. GBP payouts via Faster Payments cost nothing. Stripe settles into the named UK sort code. One dashboard. One audit trail. £2,300+ saved annually.

[aa cta]

Pay GBP and EUR contractors from one account — without SWIFT fees

EQWIRE gives SaaS companies direct Faster Payments and SEPA access from a single UK multi-currency account. No SWIFT routing. No forced FX conversion.

[aa btn]Open an Account[/aa]

[/aa]

Wise vs Airwallex vs Dedicated EMI: Which Works for SaaS Contractor Payouts at Scale

The real question most SaaS CFOs arrive with is not "EMI or bank?" — it's "Wise, Airwallex, or something else?" Here is a direct assessment, based on how SaaS companies manage GBP EUR payouts UK EMI account requirements at volume.

Wise Business: Strengths and Limits for SaaS

Wise Business is well-suited for teams paying 1–5 contractors occasionally. FX rates track close to the mid-market rate. Batch upload handles up to 1,000 transfers per file on eligible plans.

The limits show at scale. Wise is not designed as a primary settlement account for companies receiving PSP payouts — not all account tiers provide a named UK sort code and account number for GBP balance receipt. SEPA access is available but routing depends on the recipient corridor. For a SaaS company needing Stripe settlement, EUR balance retention, and monthly batch payouts — Wise is workable but not purpose-built for that combined flow.

Airwallex: API-First but Checkout-Oriented

Airwallex offers strong multi-currency wallet infrastructure and a developer-first API. For SaaS companies embedding payment capabilities into their own product — accepting subscriptions, processing global billing — Airwallex is a strong fit.

As a standalone operational treasury account for a finance team running monthly contractor payout cycles, it is less natural. Airwallex is positioned as payments infrastructure for platforms, not treasury management for internal payroll and contractor payments. Capable platform — optimised for a different use case.

Dedicated UK EMI Account: The Right Infrastructure for SaaS Treasury

For SaaS companies that need (a) a named UK IBAN and sort code for Stripe and Adyen PSP settlement, (b) a EUR wallet for SEPA payouts without forced conversion, (c) CSV batch upload for monthly payout cycles, and (d) FCA-authorised safeguarding — a dedicated EMI account built for business treasury is the structurally correct choice.

This is the use case for which accounts like EQWIRE are designed. The feature set maps directly to the SaaS treasury workflow: receive subscription revenue, hold multi-currency balances, run contractor payouts via Faster Payments and SEPA from the same dashboard.

SaaS Subscription Revenue and Contractor Payout Account UK Multi-Currency

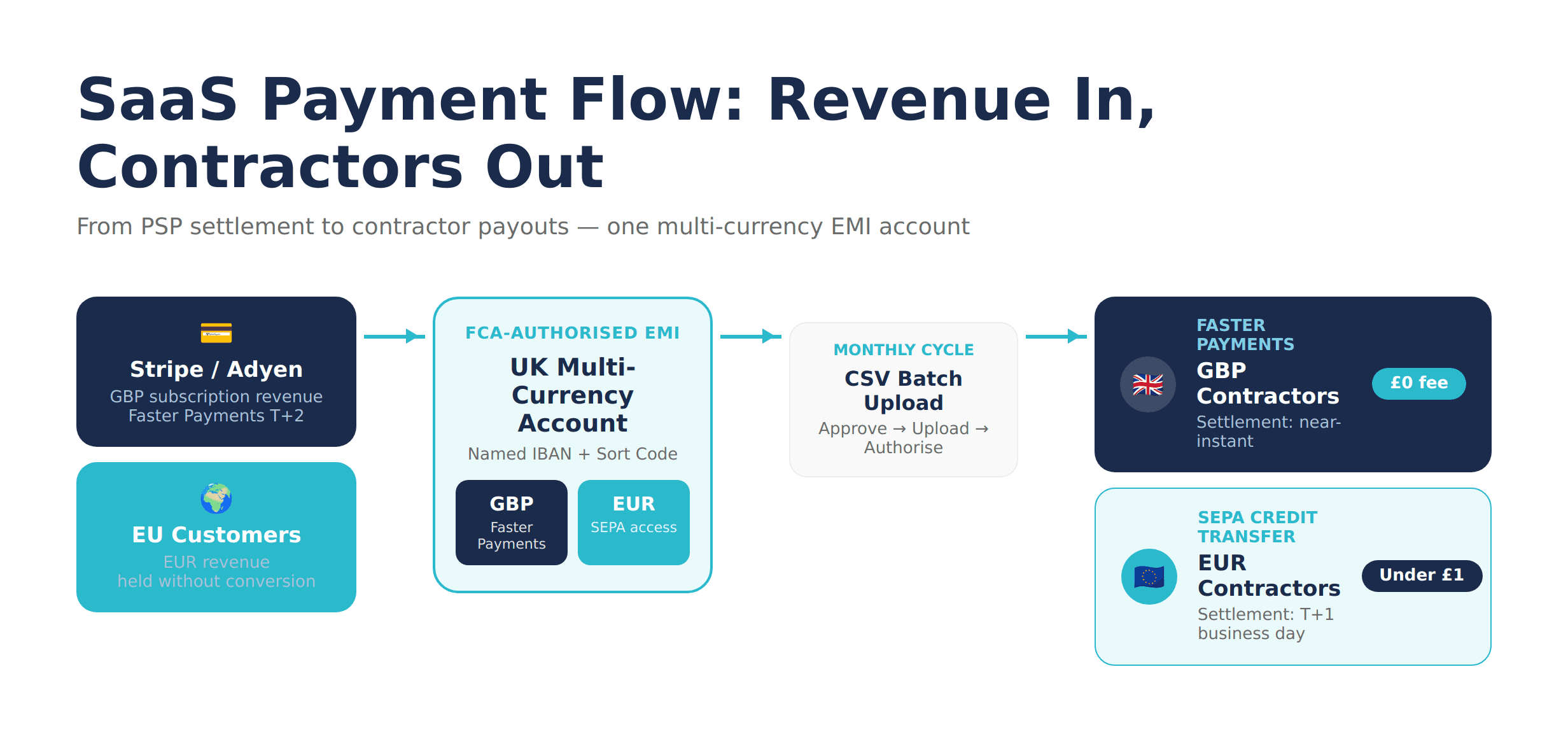

The full treasury flow — from PSP settlement to contractor payment — works as follows when the account structure is correct.

Receiving PSP Payouts (Stripe, Adyen) in GBP

Stripe and Adyen settle GBP merchant revenue via Faster Payments into the merchant's nominated UK account. The account requires a valid UK sort code and account number. Stripe's standard settlement cycle is T+2; daily payouts are available on eligible accounts.

An FCA-authorised EMI account with a named UK IBAN provides those credentials. For how PSP settlement into a UK EMI account works in practice, see receiving Stripe or Adyen payouts directly into a UK settlement account — setup requires updating the payout destination in the PSP dashboard.

Holding EUR Balances Without Forced FX Conversion

Most standard UK business accounts convert incoming EUR to GBP automatically at a marked-up rate. An EMI account with separate GBP and EUR wallets holds EUR as received — and uses it directly for EUR contractor payouts, with no conversion step and no FX margin applied.

For SaaS companies billing in both currencies, holding EUR and GBP balances without triggering automatic conversion reduces the effective cost of every EUR payout cycle. Over 12 months, that margin adds up.

Paying Contractors from the Same Multi-Currency Balance

The end-to-end payout workflow: invoice approval → CSV batch file → upload to the EMI portal → validation and maker-checker authorisation → payment release. GBP contractors receive payment near-instantly via Faster Payments. EUR contractors receive payment by T+1 via SEPA Credit Transfer.

This is the payment infrastructure for SaaS: collect GBP EUR and pay contractors from same UK account — one system, one dashboard, one reconciliation stream. For the full setup on batch payment CSV uploads for recurring contractor payout cycles, see batch payments for UK businesses.

Conclusion

The SaaS payment infrastructure decision is structural: does the account support Faster Payments for GBP, direct SEPA for EUR, multi-currency balances, and batch CSV payouts — all from the same dashboard?

The rail choice alone — SEPA versus SWIFT for EUR — can save £2,300+ annually. For same-day GBP settlement via Faster Payments for domestic contractor payouts, the account type is the decision that governs everything downstream.

[aa cta]

Ready to consolidate your GBP and EUR payment operations?

Stop running two platforms for GBP and EUR payouts. One account, one dashboard, same-day GBP settlement and T+1 EUR via SEPA.

[aa btn]Create Account[/aa]

[/aa]

FAQ

What is the best payment account for SaaS companies paying global contractors in the UK?

The best payment account for SaaS companies paying global contractors UK combines Faster Payments for GBP, direct SEPA access for EUR, and multi-currency balance wallets under one FCA-authorised account. This eliminates the need for a separate platform per currency and removes SWIFT routing fees from EUR contractor payments entirely. An FCA-authorised EMI with these capabilities is purpose-built for this use case.

How do SaaS companies manage GBP and EUR payouts from a UK EMI account?

SaaS companies manage GBP EUR payouts UK EMI account operations by maintaining separate GBP and EUR balance wallets, uploading monthly CSV batch files per currency, and releasing payments via Faster Payments (GBP, near-instant) and SEPA Credit Transfer (EUR, T+1). The account receives Stripe or Adyen settlement in GBP and holds EUR from European revenue sources separately — both flows authorised and reconciled from the same portal.

What should I look for in a SaaS subscription revenue and contractor payout account UK multi-currency?

A SaaS subscription revenue and contractor payout account UK multi-currency setup requires: a named UK sort code and IBAN for PSP settlement, separate GBP and EUR wallets with no forced conversion, direct SEPA participation for EUR payouts, Faster Payments for GBP, and CSV batch upload for recurring cycles. FCA authorisation with client fund safeguarding is the regulatory baseline. Confirm direct SEPA participation before opening — not all UK EMIs offer it.

How do SaaS platforms automate contractor payments via Faster Payments and SEPA UK EMI?

The process for how SaaS platforms automate contractor payments via Faster Payments and SEPA UK EMI runs as follows: PSP revenue settles into the GBP wallet; approved invoices are exported to a CSV file; the file uploads to the EMI portal; a maker-checker step validates the batch; payment releases via Faster Payments (GBP, near-instant) or SEPA Credit Transfer (EUR, T+1). No manual entry per contractor is required once the batch file is prepared and the approval workflow is configured.

Can I collect GBP and EUR and pay contractors from the same UK account?

Yes. A UK FCA-authorised EMI account with multi-currency wallets allows a SaaS company to receive GBP via Faster Payments, hold EUR without forced conversion, and pay contractors in both currencies from the same account. This is the core design of a purpose-built SaaS treasury account — and the step-by-step setup for a SaaS company payment account for subscription revenue and contractor payouts UK involves updating the PSP settlement destination and configuring currency-specific batch upload templates.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)