•

•

Stripe and Adyen Settlement Account UK: Receive PSP Payouts in GBP

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

UK e-commerce businesses often assume their payment processing is working correctly — until month-end reconciliation reveals that EUR settlements from Stripe or Adyen have arrived as GBP, with no FX charge on the invoice and no warning from the bank. The account receiving those payouts converted the currency on arrival. The business had no recourse.

The PSP settlement account is the account registered in the payment processor's dashboard as the destination for net settlement funds. The type of account used determines whether GBP and EUR payouts arrive in their original currency or get converted at the bank's internal rate before the finance team sees them.

For UK businesses processing multi-currency payments through Stripe, Adyen, or PayPal, an FCA-authorised UK EMI account with separate GBP and EUR balances is the most appropriate structure. It eliminates forced conversion on credit, preserves settlement currencies for accurate reconciliation, and supports both Faster Payments (GBP) and SEPA Credit Transfer (EUR) — the two rails PSPs use to deliver UK payouts.

[aa key-takeaways]

Key Takeaways

A PSP settlement account receives net funds from Stripe or Adyen after fees are deducted and the standard settlement period (T+1 to T+3) clears

Stripe routes GBP payouts via Faster Payments; Adyen routes GBP via Faster Payments and EUR via SEPA Credit Transfer

Traditional UK banks auto-convert incoming EUR settlements to GBP at an internal spread — typically 1.5–2.5% — with no separate line item visible

FCA-authorised EMI accounts issue named UK sort codes and IBANs accepted by all major PSPs, and hold each currency in a separate balance without forced conversion

Both Stripe and Adyen allow businesses to register separate bank details per currency, routing GBP and EUR to different sub-balances within the same account

[aa btn]Open Your Settlement Account[/aa]

[/aa]

What Is a PSP Settlement Account and How Does Settlement Work

A PSP settlement account is the bank or EMI account registered in a payment processor's dashboard as the destination for settlement funds. PSPs batch daily transactions, deduct processing fees, and push the net amount to this account on the settlement schedule. It is not the account used for day-to-day business operations — it is the account that receives the proceeds of card processing after clearing.

Understanding how PSP settlement flows into a multi-currency EMI account begins with the settlement cycle and how payout rails work in the UK context.

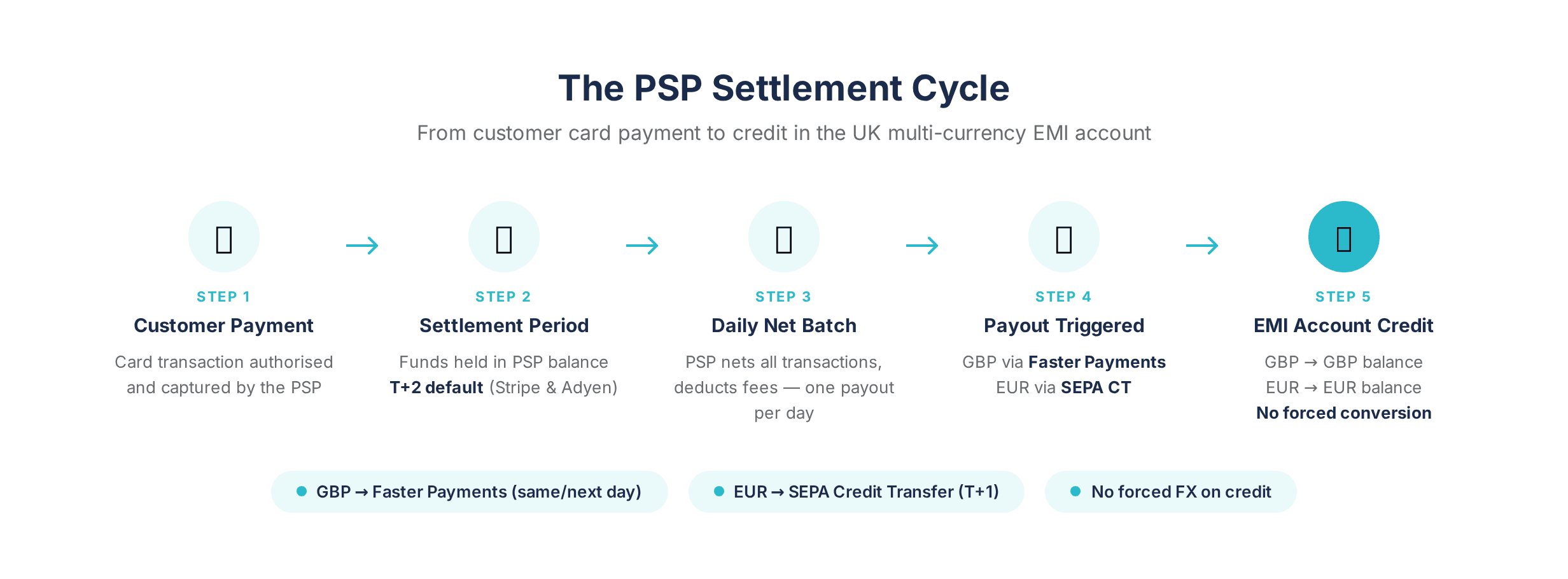

The Settlement Cycle — From Customer Payment to Bank Credit

When a customer completes a card transaction, the PSP authorises and captures the payment. The funds are held in the PSP's internal balance — not released to the merchant immediately. The settlement period then runs: typically T+2 for Stripe on new accounts, T+2 for Adyen (configurable by merchant agreement), during which the PSP nets all daily transactions, deducts processing fees, and sends the remaining amount to the registered account as a single payout.

This netting matters. The business receives one daily settlement figure, not individual per-transaction credits. If that figure is in EUR and the receiving account is GBP-only, the bank converts on arrival. No notification is sent. No separate charge appears. The FX spread is embedded in the rate applied, and the converted GBP credit appears as though that was simply what the settlement was worth.

The only point of control is the account the PSP is configured to send to. Once the payout is triggered, the conversion is irreversible.

How Stripe and Adyen Route GBP and EUR Payouts to a UK Account

Stripe uses Faster Payments for GBP payouts, which typically credit within hours of the payout being triggered on business days. For EUR, Stripe supports SEPA Credit Transfer when a valid IBAN is registered as the EUR payout destination. The Stripe settlement account UK GBP EMI configuration requires a sort code and account number for GBP, and an IBAN for EUR — both provided by an FCA-authorised EMI account.

Adyen follows a similar structure. GBP settlements route via Faster Payments; EUR settlements route via SEPA Credit Transfer to the IBAN registered in the Adyen Customer Area. The European Central Bank oversees SEPA scheme governance, with standard SEPA Credit Transfer settlement at T+1 from the sending bank.

Both PSPs allow businesses to register separate bank details per currency. GBP and EUR payouts can be directed to different sub-balances within a single multi-currency EMI account. The configuration is set in the PSP dashboard — not managed by the receiving account.

[aa fast-fact]

Fast Fact: Stripe's default payout schedule is T+2 for new accounts, moving toward T+1 as account history builds. Adyen's default is T+2, adjustable based on merchant agreement. Settlement timing is governed by the PSP — not the receiving EMI account.

[/aa]

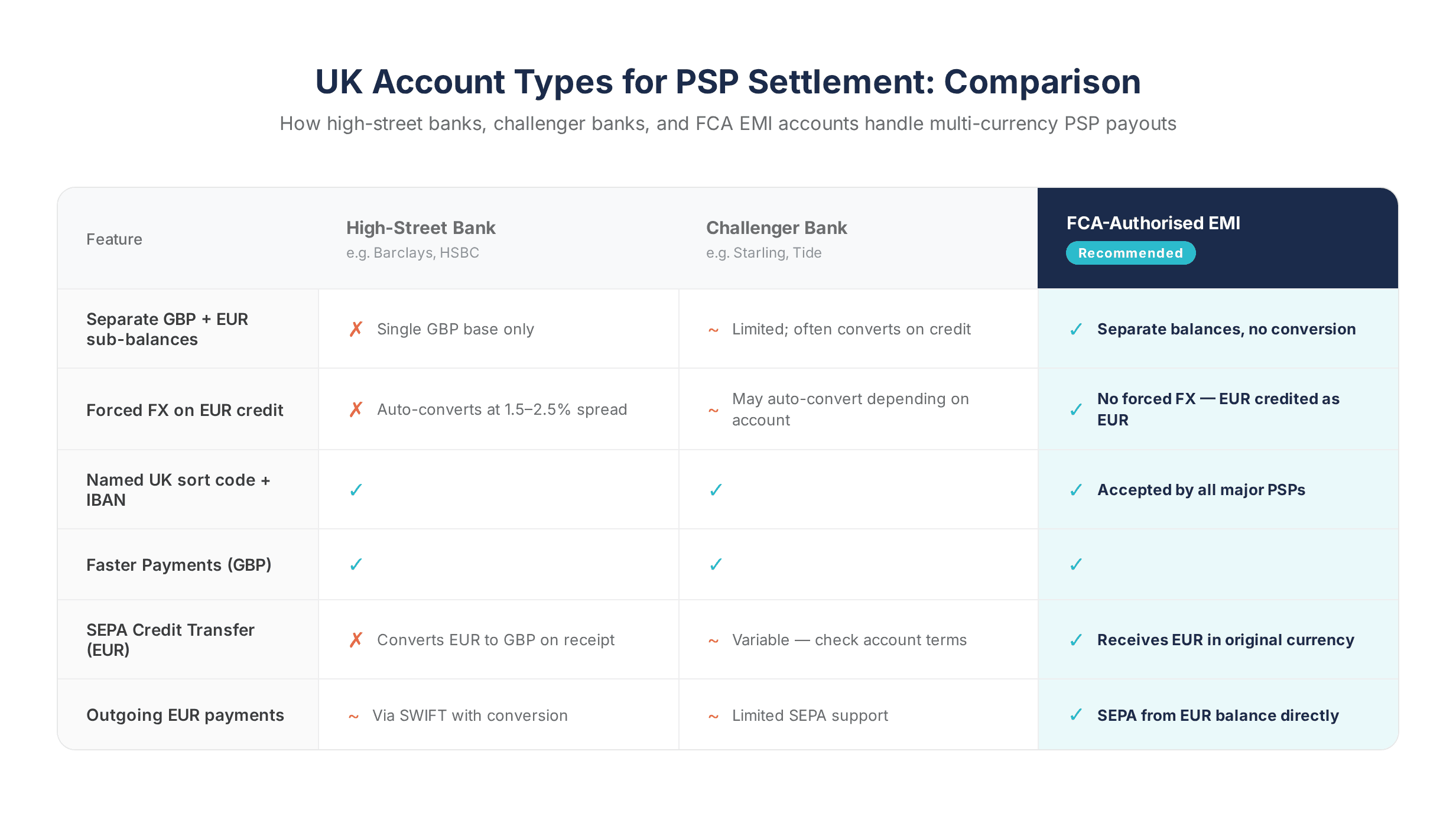

Why the Type of UK Account You Use for PSP Settlements Matters

Standard UK business accounts operate in GBP as their base currency. When Stripe or Adyen sends a EUR settlement, the bank auto-converts at its internal rate. The PSP settlement account UK EMI GBP EUR distinction becomes financially material at scale — and the problem remains invisible until reconciliation flags it.

Forced FX Conversion — How Traditional Banks Silently Erode Settlement Margins

A UK business bank account receiving a EUR settlement will convert it automatically. The bank applies its internal FX spread — typically 1.5–2.5% above the mid-market rate — without a separate transaction charge. The conversion does not appear as a fee in the bank statement. It appears as a lower-than-expected GBP credit.

On €100,000 of annual EUR settlement volume, a 2% bank FX spread represents €2,000 in annual margin erosion that never appears on any invoice. At €500,000 annual volume, that figure reaches €10,000. The businesses most exposed are those using an Adyen settlement account UK GBP EUR configuration without realising the receiving bank is converting on credit.

The issue compounds during reconciliation: the GBP amount credited does not match the EUR figure shown in the PSP dashboard, and the difference cannot be attributed to a specific fee.

Named Sort Code and IBAN — What UK EMI Accounts Provide for PSP Payout Routing

FCA-authorised EMIs issue unique, named sort codes and IBANs tied to the business entity. From Stripe's or Adyen's perspective, an EMI account is operationally identical to a bank account. The setup process is the same: sort code plus account number for GBP, IBAN for EUR.

This matters for businesses needing to receive Stripe Adyen PayPal settlements UK in multiple currencies. All three PSPs accept FCA-regulated EMI-issued account details for payout routing with no secondary verification or PSP-side restriction.

What changes after the credit arrives: the EMI holds it in the originating currency. The business then decides whether to convert, hold, or deploy those funds — paying EUR-denominated supplier invoices directly from the EUR balance without triggering an FX conversion.

The key differences between FCA-authorised EMI accounts and traditional UK banks are operational rather than regulatory — both hold funds securely and legally, but their currency handling on credit is fundamentally different.

FCA-Regulated EMI Accounts vs Traditional Banks for PSP Settlement

The right PSP settlement account provides four things: multi-currency balance support without forced conversion, named UK sort code and IBAN accepted by PSPs, Faster Payments for GBP and SEPA for EUR, and outgoing payment capability from the same account.

How EMI Accounts Hold GBP and EUR in Separate Balances

Multi-currency EMI accounts maintain GBP and EUR as distinct sub-balances. A Stripe GBP payout credits to the GBP balance via Faster Payments. An Adyen EUR payout credits to the EUR balance via SEPA — without triggering conversion at any point.

This design addresses the PSP settlement account UK EMI multi-currency without forced FX requirement that most standard UK business accounts cannot meet. The EUR balance can be used directly: to pay EUR-denominated supplier invoices, to hold as a natural FX hedge, or to convert to GBP at a chosen rate and timing rather than at the bank's discretion on arrival.

For businesses holding multi-currency balances without triggering forced FX conversion, the mechanism is consistent: each currency credits to its own sub-balance, with no automatic conversion on receipt. To receive Stripe Adyen PayPal settlements in original currency UK FCA EMI no forced FX, the account must be issued by an FCA-authorised EMI with distinct currency balances — not a display account that converts on settlement.

Regulatory Framework — Electronic Money Regulations 2011 and the FCA Register

EMIs operating in the UK are authorised under the Electronic Money Regulations 2011 and listed on the FCA Register. They do not hold deposit-taking licences, but they are fully recognised for payment and settlement purposes under UK financial services law.

For a CFO or finance manager evaluating whether an EMI is a credible settlement account: the FCA Register confirms authorisation status, the EMI's named sort code and IBAN are accepted by Stripe, Adyen, and PayPal, and the account structure is legally equivalent for receiving and sending settlement funds. The regulations also require EMIs to safeguard client funds separately from their own capital — a defined regulatory protection.

[aa cta]

Connect Stripe and Adyen Payouts to a UK Multi-Currency Account

EQWIRE is an FCA-authorised EMI account with separate GBP and EUR balances — accepted by all major PSPs and set up in minutes.

[aa btn]Open Your Settlement Account[/aa]

[/aa]

How to Connect Stripe and Adyen Payouts to a UK Multi-Currency EMI Account

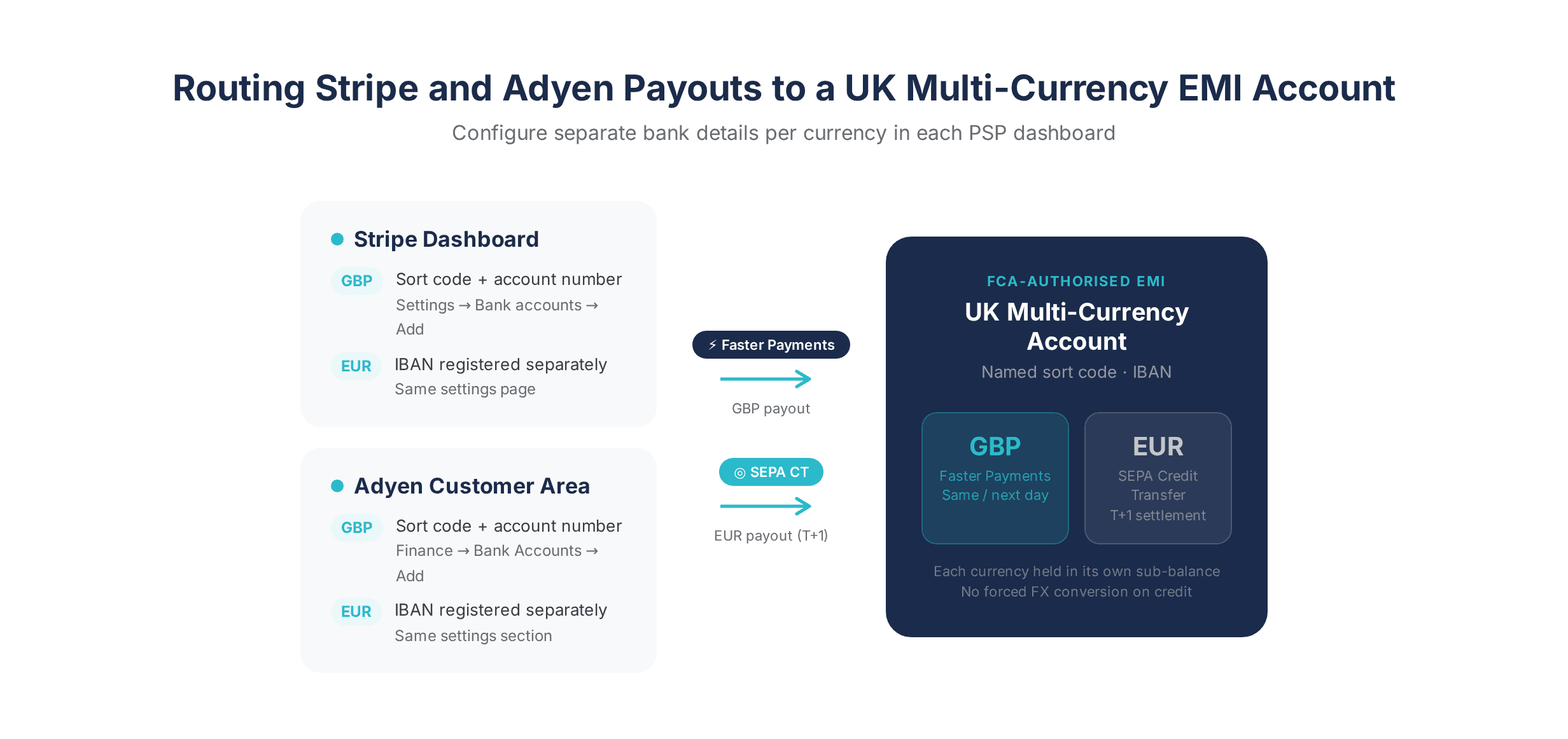

Step-by-step: route Stripe and Adyen GBP settlements into a UK multi-currency EMI account by updating the payout bank details in each PSP dashboard. Both platforms support per-currency configuration. The process takes under ten minutes per PSP once the EMI account details are available.

Configuring Payout Bank Details in Stripe

In Stripe Dashboard: Settings → Bank accounts and scheduling → Add bank account. This is the standard process for how to set up a PSP settlement account for Stripe and Adyen UK.

GBP: enter the EMI-issued sort code and account number

EUR: enter the EMI-issued IBAN

Set payout schedule to automatic daily — recommended for cash flow visibility

Stripe validates account details before activating; allow one business day for verification

Once active, Stripe routes GBP payouts via Faster Payments and EUR payouts via SEPA to the corresponding sub-balance.

Configuring Payout Bank Details in Adyen

In Adyen Customer Area: Finance → Bank Accounts → Add bank account. Adyen supports separate account registration per settlement currency.

GBP: sort code + account number

EUR: IBAN

Payout schedule is configurable per currency — daily for GBP is standard; EUR follows T+2 by default

How ecommerce businesses receive PSP payouts and pay suppliers from the same UK account: after configuring both PSPs to send payouts to the EMI account, the EUR sub-balance credited from settlements can be used directly for EUR-denominated outgoing payments. No conversion required — EUR payments draw from the EUR balance.

Key Considerations When Choosing a PSP Settlement Account in the UK

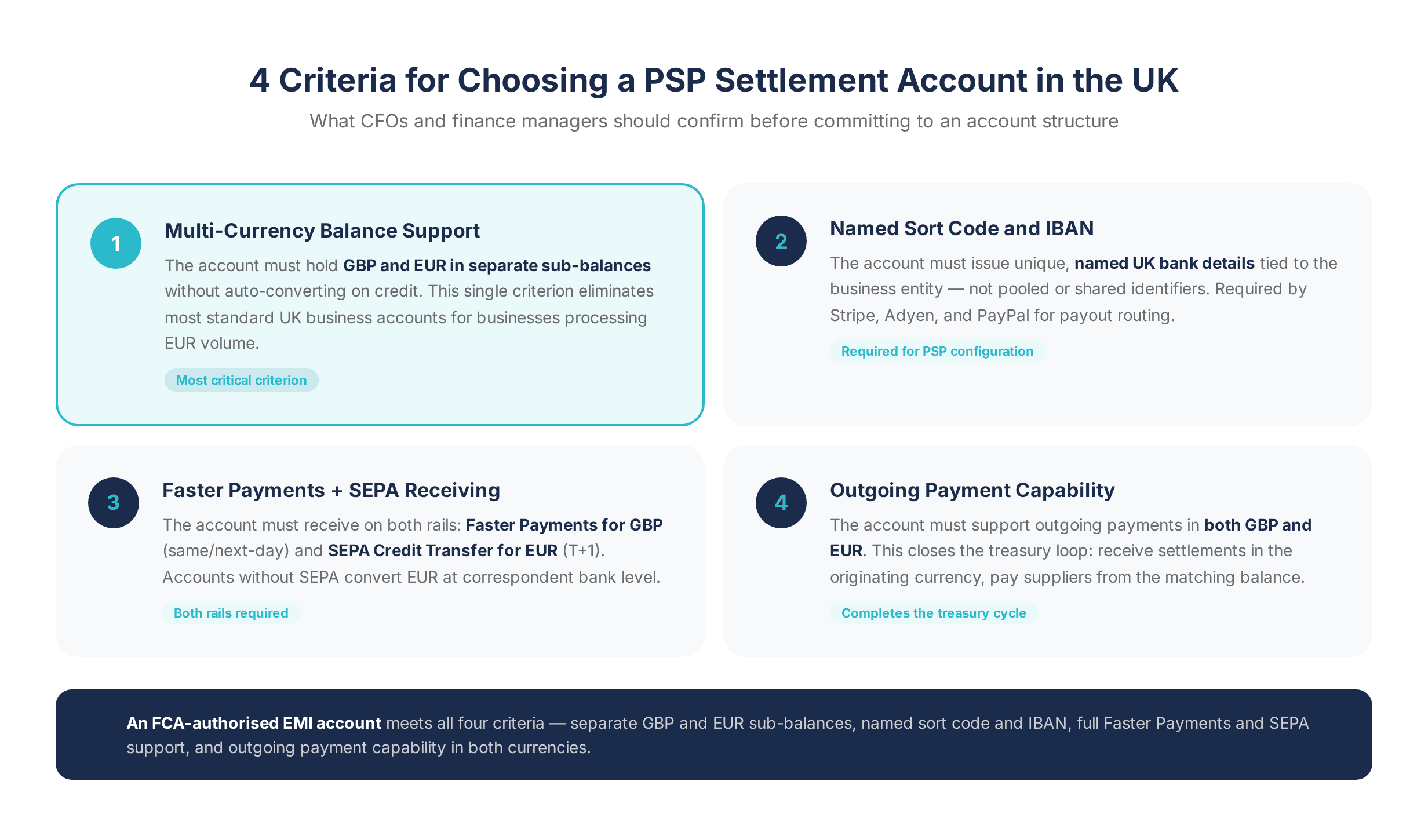

Four criteria determine whether an account is operationally suitable for multi-currency PSP settlement. Finance managers evaluating a PSP settlement account should confirm each before committing.

Multi-currency balance support. The account must hold GBP and EUR in separate sub-balances without auto-converting on credit. This single criterion eliminates most standard UK business accounts for businesses processing EUR volume.

Named sort code and IBAN. The best UK account to receive Stripe Adyen PayPal payouts GBP EUR issues sort codes and IBANs individually tied to the business entity, accepted directly in each PSP's payout configuration — not pooled or shared identifiers.

Faster Payments and SEPA receiving capability. The account must receive on both rails: Faster Payments for GBP and SEPA Credit Transfer for EUR. Accounts without SEPA receiving capability cannot accept EUR payouts from Adyen or Stripe without triggering a conversion at the correspondent bank level.

Outgoing payment capability. To receive GBP payouts from multiple PSPs into one UK account and use those funds efficiently, the account must support outgoing payments in both GBP and EUR. This closes the treasury loop: receive settlements in the originating currency, pay suppliers from the matching currency balance.

EQWIRE is an FCA-authorised EMI account that meets all four criteria — named UK sort code and IBAN, separate GBP and EUR sub-balances, full Faster Payments and SEPA support, and outgoing payment capability in both currencies. For businesses evaluating Stripe settlement account options available to UK businesses, it provides a structure built specifically for multi-currency PSP settlement.

[aa cta]

One UK Account for All Your PSP Settlements

Hold GBP and EUR separately, receive Stripe, Adyen and PayPal payouts without conversion, and pay suppliers — all from one FCA-regulated account.

[aa btn]Get Started with EQWIRE[/aa]

[/aa]

FAQ

What is a PSP settlement account and how does it differ from a regular business account?

A PSP settlement account is the bank or EMI account registered in a payment processor's dashboard to receive settlement funds after the standard clearing period. Unlike a standard UK business account — which auto-converts incoming foreign currency receipts to GBP — a dedicated PSP settlement account at an FCA-authorised EMI holds GBP and EUR in separate balances without triggering conversion on credit. The distinction is financially material for any business processing multi-currency volumes through Stripe, Adyen, or PayPal.

How do I set up a PSP settlement account for Stripe and Adyen in the UK?

In Stripe, bank details are added under Dashboard → Settings → Bank accounts and scheduling. In Adyen, accounts are configured under Finance → Bank Accounts in the Customer Area. Both PSPs require a UK sort code and account number for GBP payouts, and an IBAN for EUR payouts. An FCA-authorised EMI account provides both, and the setup process for how to set up a PSP settlement account for Stripe and Adyen UK is identical to adding a standard bank account.

Can I receive both GBP and EUR settlements into one UK account without forced FX?

Yes. Stripe and Adyen both support per-currency bank account registration within the same payout configuration. A PSP settlement account UK EMI multi-currency without forced FX setup requires an FCA-authorised account with distinct currency sub-balances — GBP credits via Faster Payments, EUR credits via SEPA, each held in the originating currency without auto-conversion.

What FCA-regulated account types are suitable for Stripe and Adyen settlement in the UK?

FCA-authorised EMI accounts are the most suitable account type for receiving PSP payouts in multiple currencies. Regulated under the Electronic Money Regulations 2011 and listed on the FCA Register, they issue UK sort codes and IBANs accepted by all major PSPs. As the best UK account to receive Stripe Adyen PayPal payouts GBP EUR, they hold GBP and EUR in separate balances, apply no forced FX conversion on credit, and support both Faster Payments and SEPA.

How long does it take for Stripe and Adyen to settle funds to a UK EMI account?

Stripe's default payout schedule is T+2 for new accounts, moving toward T+1 as account history builds. Adyen's default is T+2, adjustable by merchant agreement. GBP payouts via Faster Payments typically credit within hours of the payout being triggered. EUR payouts via SEPA Credit Transfer usually arrive the next business day after the PSP initiates the transfer. Settlement timing is governed by the PSP — the receiving EMI account does not introduce additional delays.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)