•

•

How to Receive CNY Payments from Chinese Clients as a UK Business

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

When a UK business first attempts to receive CNY from Chinese clients, the process rarely works as expected. A wire arrives from a client in Shanghai or Shenzhen, and the UK bank rejects it outright or converts it automatically at an unfavourable rate, with correspondent bank fees already deducted. The problem is structural: the Chinese renminbi operates under two parallel currency systems, and most UK businesses are unaware of which one applies to international payments.

This article explains why receiving CNY from Chinese clients as a UK business requires a specific account setup, which payment methods actually work, and how finance teams can avoid the most common sources of cost and delay.

[aa key-takeaways]

Key Takeaways

CNY (onshore renminbi) cannot be sent internationally. UK businesses receive CNH (offshore renminbi), not CNY directly, even when the invoice is denominated in CNY.

Most standard UK bank accounts do not support CNH holding, which is why incoming Chinese wires are often rejected or auto-converted to GBP.

SWIFT remains the most common transfer method but involves a correspondent bank chain that deducts fees at each hop and adds 1–5 business days to settlement.

CIPS (Cross-Border Interbank Payment System) is China's dedicated RMB settlement network, processing ¥175.49tn in 2024, but UK bank direct participation is limited.

Multi-currency accounts that support CNH holding eliminate the double FX conversion problem and give businesses control over when they convert to GBP.

UK businesses do not need FCA authorisation to receive Chinese payments. That obligation falls on the payment provider they use.

[aa btn]Book a Call[/aa]

[/aa]

Why Receiving CNY Payments from China Is Harder Than It Looks

UK banks routinely reject incoming CNY wires, not because of a compliance issue on either side, but because the renminbi operates under government-managed capital controls that prevent the onshore version of the currency from moving freely outside mainland China. Finance teams that understand this structural reality can set up the right account from the start. Those that don't spend weeks troubleshooting wire rejections that have nothing to do with their banking relationship.

PBOC Capital Controls and the Onshore Currency Lock

The People's Bank of China (PBOC) manages the yuan through a daily reference rate, with the onshore exchange rate permitted to fluctuate only within a ±2% band of that reference price. This is not a temporary restriction. It is a deliberate design feature of China's monetary system — unlike the euro or the US dollar, the renminbi does not float freely. The PBOC controls the pace and direction of currency internationalisation, and outflows of onshore CNY are restricted accordingly.

In practice, this means a Chinese business paying an overseas supplier cannot simply wire CNY across the SWIFT network the way a UK business might send GBP or EUR. The capital account is partially closed, and cross-border CNY transfers require routing through specific approved channels. For UK businesses, this is the root cause of every wire rejection: the currency arriving at the UK bank's doorstep is not the one the UK correspondent network was built to handle.

Why Most UK Banks Cannot Hold or Receive CNY Directly

Standard UK business bank accounts, including those at major clearing banks, are not set up to hold CNY. The Chinese yuan business account infrastructure in the UK is limited to a small number of specialist providers, primarily UK branches of Chinese state banks such as Bank of China UK. Even SWIFT-capable UK banks with broad currency support typically do not offer CNY accounts because the currency requires onshore settlement to receive directly, which in turn requires a mainland China banking licence or an approved correspondent relationship.

The result is that even when a Chinese client instructs their bank to send CNY, the payment is either converted to CNH before it enters the international network or returned to the sender. The currency that UK businesses can actually receive via international channels is CNH, the offshore version of the renminbi.

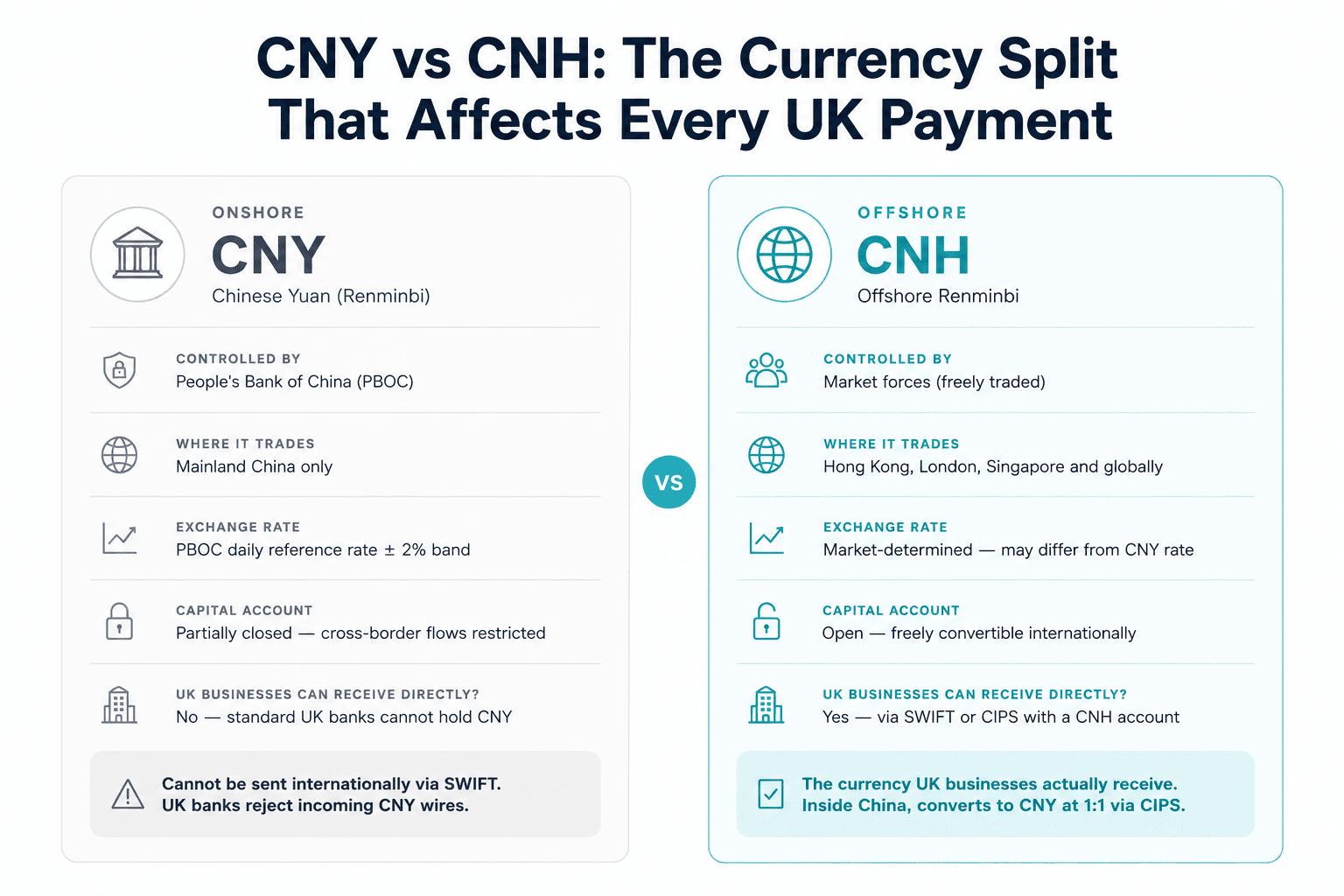

The CNY vs CNH Distinction: The Root Cause Most Businesses Miss

CNY and CNH represent the same currency unit, the renminbi, but operate under fundamentally different rules. CNY is the onshore version, managed by the PBOC and restricted to use within mainland China. CNH is the offshore version, freely traded in Hong Kong, London, Singapore, and other international financial centres. For UK businesses receiving payments from Chinese clients, the currency arriving via any international channel will be CNH, regardless of how the invoice is denominated.

The exchange rates between CNY and CNH are not always identical. Because CNH trades freely on international markets, it responds to global supply and demand, which can create a small but meaningful spread between onshore and offshore pricing. BIS triennial FX survey data shows CNH as a growing share of global FX turnover, reflecting its increasing role in cross-border trade settlement. Inside China, when an international payment arrives and needs to be settled domestically, CIPS converts CNH to CNY at a 1:1 ratio, meaning the Chinese recipient does not lose value through this process.

For UK businesses, the practical implication is direct: invoicing in CNY does not mean receiving CNY. The currency will arrive as CNH. A UK account that cannot hold CNH will either reject the payment or convert it immediately to GBP, removing any ability to time the conversion.

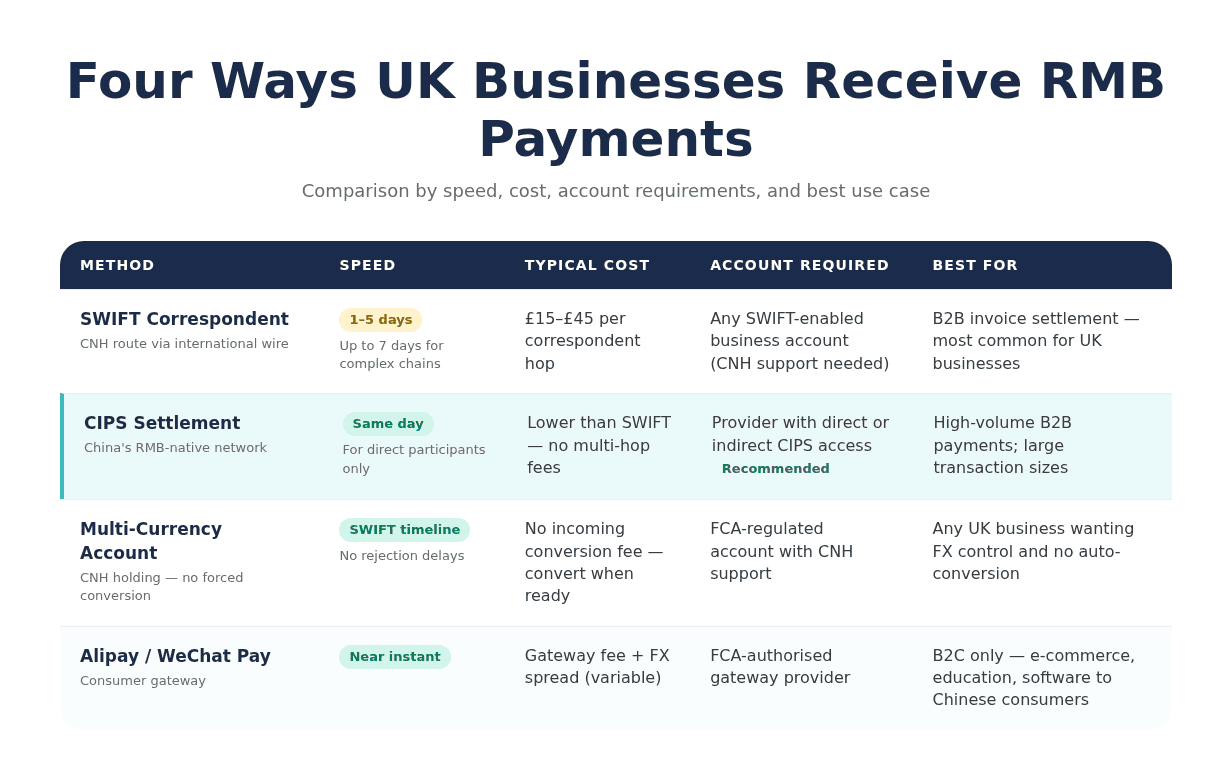

Four Methods UK Businesses Use to Receive RMB from Chinese Clients

UK businesses receive RMB payments through four main channels. Each carries different costs, timelines, and account requirements. The right choice depends on payment volume, the nature of the client relationship, and whether the business deals in B2B services or B2C consumer sales. Here is what UK companies receiving Chinese yuan payments need to know about each method.

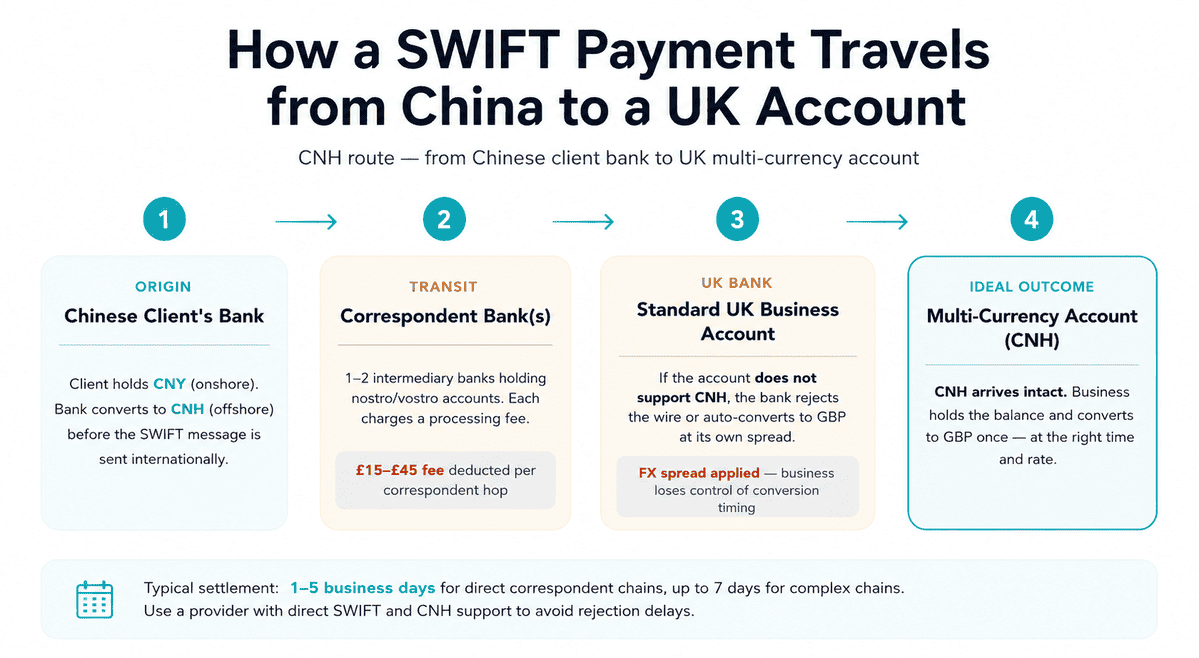

SWIFT via Correspondent Bank (the CNH Route)

SWIFT remains the most widely used channel for receiving a payment from China into a UK account. The Chinese client's bank converts CNY to CNH and transmits a payment message via SWIFT to the UK receiving bank. Because most UK banks do not have a direct banking relationship with Chinese banks, the transfer routes through one or more correspondent banks: institutions that hold accounts on behalf of both the sending and receiving bank (nostro and vostro accounts, as documented in BIS CPMI payment system oversight). Each correspondent in the chain may deduct a processing fee, typically £15–£45 per hop, which means the amount arriving can be less than the amount invoiced.

SWIFT payments from China to UK accounts typically settle within 1–5 business days, depending on the number of correspondents in the chain. Some transfers with two or more intermediaries take up to 7 business days. For businesses receiving high volumes of payments, these costs and delays compound quickly. Finance teams exploring SWIFT alternatives for UK businesses often find that local payment rails reduce per-transaction costs by 80–90%.

[aa fast-fact]

Fast Fact: For a UK business receiving 15 international payments per month via SWIFT, correspondent bank fees alone can total £4,500–£9,000 per year, before any FX conversion costs are applied.

[/aa]

CIPS: China's RMB-Native Settlement System

CIPS (Cross-Border Interbank Payment System) is China's dedicated clearing and settlement network for RMB transactions, launched in 2015 and made mandatory for cross-border CNY transfers in January 2021. Unlike SWIFT, which transmits payment messages but relies on correspondent banks for settlement, CIPS clears and settles RMB transactions directly, removing the need for multiple intermediary institutions. The BIS cross-border payments roadmap identifies correspondent banking fragmentation as a primary driver of high international payment costs.

The system has grown substantially. In 2024, CIPS processed ¥175.49 trillion across 8.2 million transactions, a 43% increase in value year-on-year. Its network now reaches 189 countries through more than 1,700 institutional participants. CIPS has adopted the ISO 20022 messaging standard, the same modern format used by SWIFT MX, which enables smoother interoperability between the two systems.

For UK businesses, the practical limitation is connectivity. Most UK-headquartered banks are indirect CIPS participants, meaning they access the system through a Chinese correspondent rather than directly. Direct participants, those with a live CIPS connection, can settle RMB transactions the same business day. Indirect participants inherit additional delays. Finance teams should ask their payment provider directly whether they have direct or indirect CIPS participation before assuming CIPS offers a speed advantage.

[aa fast-fact]

Fast Fact: CIPS processed ¥175.49 trillion in 2024, a 43% year-on-year increase, across 8.2 million transactions in 189 countries.

[/aa]

Multi-Currency Accounts With CNH Holding

Multi-currency accounts supporting CNH let UK businesses hold incoming RMB without triggering an immediate conversion to GBP. When a Chinese client sends a SWIFT payment in CNH, the funds appear in the CNH balance of the multi-currency account, visible instantly on receipt. The business then decides when and at what rate to convert, not the bank.

This approach eliminates two problems simultaneously. First, it removes the correspondent bank rejection risk: FCA-regulated multi-currency account providers have the infrastructure to accept CNH. Second, it gives the finance team control over FX timing, which matters when the CNH/GBP rate is unfavourable at the moment of receipt but may improve within days.

EQWIRE's multi-currency accounts support CNH receipt with direct SWIFT access, enabling UK businesses to consolidate incoming Chinese payments alongside EUR, USD, and GBP balances in a single account. Cross-border business banking of this kind removes the need to maintain separate accounts at specialist Chinese bank branches. The same principle applies to EUR and other currencies — EQWIRE's approach to multi-currency IBAN accounts follows a consistent multi-currency architecture.

Consumer Payment Gateways (Alipay and WeChat Pay)

For UK businesses selling directly to Chinese consumers, in e-commerce, education, or software licensing, Alipay and WeChat Pay offer a direct payment gateway that bypasses SWIFT entirely. The Chinese customer pays in CNY through their domestic wallet; the gateway provider handles the FX conversion and cross-border settlement, delivering GBP to the UK merchant account.

This method is consumer-facing by design and not suited to B2B invoice settlement. Chinese businesses do not pay supplier invoices through Alipay. For UK businesses selling services to Chinese corporates, consultancies, or distributors, the gateway route does not apply.

[aa cta]

Open a Multi-Currency Account to Accept CNH From Chinese Clients

EQWIRE multi-currency accounts support CNH receipt with direct SWIFT access and no correspondent bank markups on incoming transfers.

[aa btn]Create Account[/aa]

[/aa]

How to Avoid the Hidden FX Double Conversion

The double conversion problem arises when a UK business invoices in GBP and the Chinese client converts CNY to GBP to send the payment. At that point, two currency conversions occur: first from CNY to CNH to enter the international network, then from CNH to GBP on the UK receiving side. Each conversion carries an FX margin, often 0.5%–2.0% per leg, and neither is visible to the business at the moment of invoicing.

When the Currency Gets Converted Twice and How to Stop It

A UK consulting firm invoicing a Shanghai client for £10,000 at a CNH/GBP rate of 9.20 would expect to receive approximately CNH 92,000. If the Chinese client sends the payment in GBP, the first conversion (CNY to CNH) happens inside China at the PBOC-influenced rate. The second conversion (CNH to GBP) happens at the UK bank's spread. By the time the funds arrive, the effective rate may be 9.00 or lower, a difference of CNH 2,000, or roughly £217 on a single invoice.

The solution is to invoice in CNH. When the UK business denominates the invoice in CNH and holds a CNH account, no conversion occurs on receipt. The CNH arrives intact. The single conversion from CNH to GBP happens once, when the business chooses to convert, at a rate and timing they control.

Invoicing in CNH vs GBP: A Cost Comparison

Understanding how to invoice Chinese clients in CNH is a practical skill for any UK finance team with ongoing Chinese client relationships. The invoice states the CNH amount, the business provides CNH bank account details, and the Chinese client's bank sends a CNH SWIFT transfer. Total FX conversions: one, at the business's discretion.

Invoicing in GBP creates two conversions, neither visible on the invoice. Invoicing in USD creates the same problem, as USD is not the Chinese client's domestic currency, so a conversion still occurs before the transfer is initiated. CNH is the only invoice currency that routes without a domestic conversion on the Chinese side and without a forced conversion on the UK receiving side.

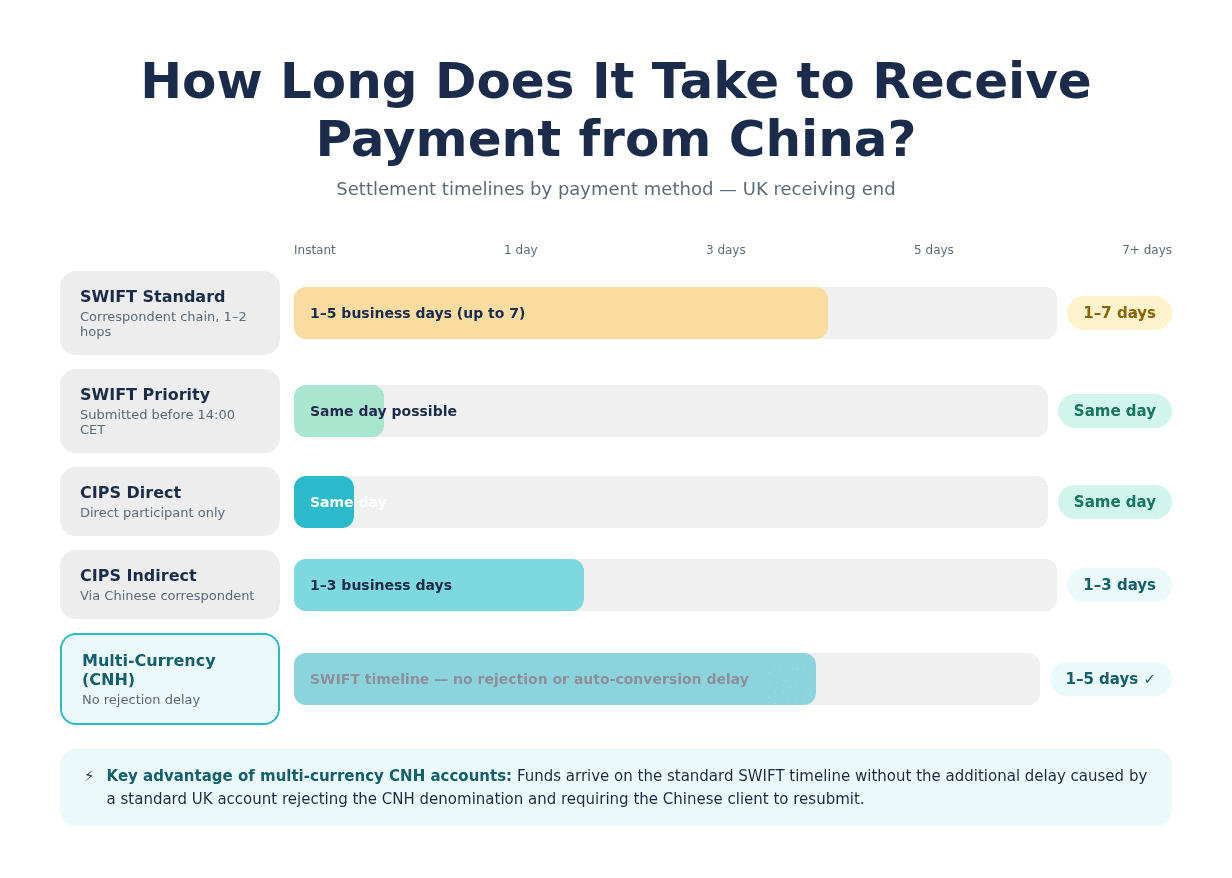

How Long Does It Take to Receive Payment from a Chinese Client?

Settlement timelines vary by method and by the specific correspondent chain involved. SWIFT transfers from China typically arrive within 1–5 business days, though some chains with two or more correspondents can extend to 7 business days, particularly if the sending bank is a smaller regional institution rather than a major clearing bank with direct UK correspondent relationships.

CIPS offers faster settlement for direct participants, with same-day settlement possible for banks with live CIPS connections. For indirect participants, which includes most UK banks, the timeline depends on their Chinese correspondent's CIPS access, and same-day settlement is not guaranteed.

Multi-currency account providers with direct SWIFT access and CNH capability typically show incoming funds as received within the standard SWIFT timeline, but without the rejection delays caused by a standard UK account refusing the CNH denomination. The Bank of England's payment and settlement infrastructure underpins the UK-side receipt of international wires, including CHAPS for high-value same-day settlement. Priority SWIFT transfers submitted before 14:00 CET can arrive same-day in some corridors.

Compliance for UK Businesses: FCA, AML, and Chinese Capital Controls

UK businesses receiving payments from China face compliance requirements on both sides of the transaction, UK-side and China-side, though the obligations are different in nature and weight.

On the UK side, the key regulatory framework is the Payment Services Regulations 2017 (PSR 2017), which requires payment service providers, not the end-recipient businesses, to hold FCA authorisation to process cross-border payments. A UK business receiving a wire from a Chinese client does not itself need FCA registration, provided it uses an FCA-authorised payment institution or bank. AML and KYC obligations do apply: UK businesses accepting large or irregular payments from overseas must conduct appropriate due diligence on their clients, maintain transaction records, and report suspicious activity to the National Crime Agency under the Proceeds of Crime Act 2002.

On the China side, PBOC capital controls impose export documentation requirements on Chinese businesses sending large international payments. Payments above a threshold (generally USD 50,000 equivalent per transaction) require supporting trade documentation (a signed contract, invoice, or proof of goods delivery) submitted to the Chinese bank before the transfer is approved. UK businesses can assist this process by ensuring invoices are detailed, consistent, and aligned with any prior contract terms on file with the Chinese client's bank.

UK businesses do not need a Chinese business licence or a mainland China bank account to receive payments from Chinese clients. An FCA-regulated multi-currency account with CNH support is sufficient on the UK side. Businesses looking to also open a GBP account for UK-side collections can do so through the same regulated provider. The compliance burden on the Chinese side rests with the client, not the recipient.

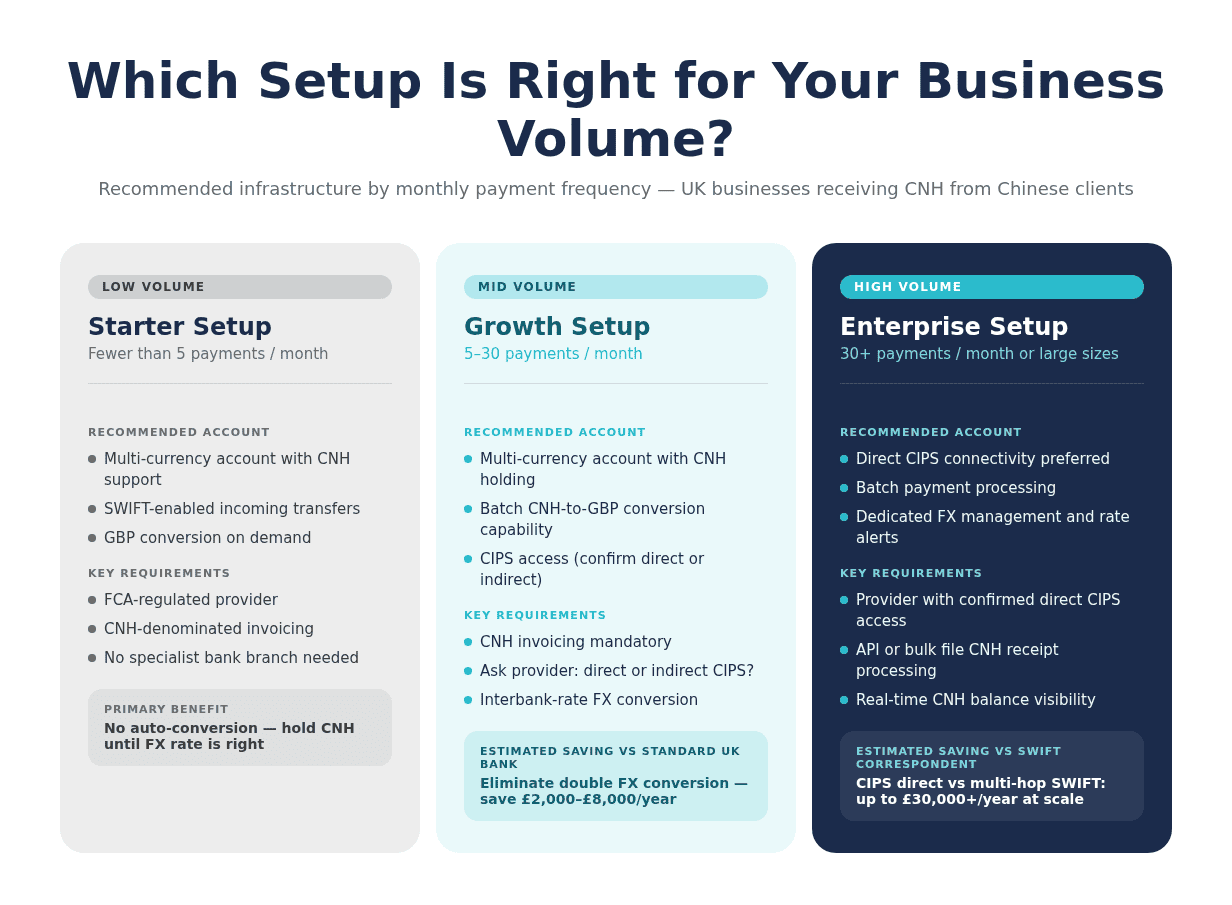

Which Setup Is Right for Your Business Volume?

Not every UK company receiving Chinese yuan payments needs the same infrastructure. A UK technology startup receiving one or two CNH invoices per quarter has different requirements from a manufacturing exporter receiving weekly payments from a Chinese distribution network.

For low-volume businesses (fewer than 5 payments per month): a multi-currency account with CNH support is the most practical setup. The account requires minimal configuration, supports CNH receipt via SWIFT, and avoids the rejection and auto-conversion problems of standard UK accounts.

For mid-volume businesses (5–30 payments per month): the double FX conversion issue becomes a material cost at this volume. Switching to CNH invoicing and holding a CNH balance before converting in batches at favourable rates reduces costs meaningfully. CIPS access through the account provider becomes relevant, and businesses should confirm whether their provider offers direct or indirect CIPS participation.

For high-volume businesses (30+ payments per month or large transaction sizes): direct CIPS connectivity, batch payment processing, and dedicated FX management tools become important. At this volume, the cost differential between SWIFT correspondent chains and CIPS direct settlement is significant. An account that consolidates CNH receipts and provides interbank-rate conversion on demand is the standard infrastructure for finance teams operating at this scale.

UK companies receiving Chinese yuan payments at any volume benefit from one consistent rule: invoice in CNH, hold CNH on receipt, and convert once. The underlying payment infrastructure, whether SWIFT or CIPS, handles the rest.

[aa cta]

Set Up Your UK Business to Receive RMB Payments in Days

Finance teams at UK SMBs use EQWIRE to consolidate incoming CNH receipts, convert to GBP at interbank rates, and eliminate the double FX conversion problem.

[aa btn]Create Account[/aa]

[/aa]

FAQ

Can a UK business receive CNY directly into a UK bank account?

No. UK businesses cannot receive onshore CNY directly into a standard UK bank account. The PBOC's capital controls prevent CNY from circulating freely outside mainland China. What UK businesses actually receive via SWIFT or CIPS is CNH, the offshore version of the renminbi, which converts to CNY at a 1:1 ratio inside China but trades freely on international markets. UK accounts that do not support CNH will reject the incoming transfer or auto-convert it to GBP immediately on receipt. To hold the received currency before converting, businesses need a multi-currency account with explicit CNH support from an FCA-regulated provider.

What is the difference between CNY and CNH for international payments?

CNY is the onshore renminbi used within mainland China and managed by the PBOC through a daily reference rate system. It cannot be used for international transfers. CNH is the offshore renminbi, freely traded in Hong Kong, London, and Singapore, and the currency used in all cross-border RMB transactions. When a Chinese business sends an international payment, the CNY in their account is converted to CNH before entering the SWIFT or CIPS network. For a UK business receiving the funds, this distinction matters because UK accounts must support CNH specifically, not generic CNY, to avoid rejection or automatic conversion.

How long does a SWIFT payment from China take to arrive in the UK?

A SWIFT payment from China typically arrives within 1–5 business days for accounts at major UK clearing banks with direct correspondent relationships to Chinese banks. Transfers routed through two or more correspondent banks, common when the sending institution is a smaller regional Chinese bank, can take up to 7 business days. Priority SWIFT transfers submitted before 14:00 CET can arrive same-day in well-connected corridors. Multi-currency account providers with direct CNH infrastructure generally process within the standard SWIFT timeline, without the additional delay of rejection and resubmission that standard UK accounts may cause.

What is CIPS and should UK businesses use it to receive Chinese yuan?

CIPS (Cross-Border Interbank Payment System) is China's dedicated clearing and settlement network for RMB transactions, mandatory for cross-border CNY since January 2021. It processed ¥175.49 trillion across 8.2 million transactions in 2024, covering 189 countries. For UK businesses, CIPS offers faster and cheaper RMB settlement than SWIFT, but only when both the Chinese sending bank and the UK receiving provider have direct CIPS participation. Most UK banks are indirect participants, meaning they access CIPS through a Chinese correspondent and do not benefit from same-day settlement. Finance teams should ask their account provider directly about their CIPS participation status before selecting it as the primary payment method.

Practical guide: UK SME receiving CNY from mainland China clients via SWIFT

For a UK SME receiving CNY from mainland China clients via SWIFT, the setup requires three elements: an FCA-regulated multi-currency account with CNH support, a CNH-denominated invoice issued to the Chinese client, and the CNH SWIFT bank details shared with the client's finance team. The Chinese client instructs their bank to send CNH via SWIFT to the UK multi-currency account. The transfer enters the SWIFT correspondent network, arrives within 1–5 business days, and appears in the CNH balance of the account. No auto-conversion occurs. The UK business then converts CNH to GBP at a time and rate of their choosing. This end-to-end process eliminates the double conversion cost, removes the rejection risk of standard UK accounts, and gives the finance team full visibility over the FX decision. For SMEs with regular Chinese client billing, the setup pays back through reduced FX costs within the first few payment cycles.

For UK businesses trading with China, the infrastructure question (which account, which method, which currency to invoice in) determines how much of each payment actually arrives. Multi-currency accounts with CNH support, CNH-denominated invoicing, and clarity on whether a provider offers direct or indirect CIPS access are the three decisions that set the baseline for cost-efficient receipt of RMB payments. Businesses ready to receive CNY from Chinese clients as a UK company can open a multi-currency account with full CNH support at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)