•

•

How to Run Weekly Supplier Batch Payments Without SWIFT

This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction and change over time. Businesses should consult qualified legal counsel and compliance professionals before making corporate structuring or banking decisions. EQWIRE does not guarantee account approval with any provider mentioned or referenced in this article.

It is Monday morning. Your accounts payable team has 22 supplier invoices queued and ready to pay. Each one goes out as a SWIFT wire. Each wire carries a bank outgoing fee of £15–25, a correspondent bank charge of $10–30, and a 2–3 business day wait before the supplier sees cleared funds. Multiply that across 52 weeks, and a routine supplier run becomes a significant operating cost — often exceeding £20,000 a year in fees alone.

Businesses that want to avoid SWIFT fees on weekly supplier payments UK can route those transactions entirely on local rails. You can run weekly supplier batch payments without SWIFT by directing GBP payments over UK Faster Payments and EUR payments over SEPA Credit Transfer — both accessible through an FCA-authorised EMI account that supports batch file upload. Batch supplier payments on UK local rails for GBP and EUR settle same-day, cost pence per transaction, and carry no correspondent chain.

This guide covers which rails replace SWIFT for supplier runs, how to build and execute the weekly batch workflow, what account type you need, and what the cost difference looks like over a full year.

Key Takeaways

SWIFT is built for cross-border, multi-correspondent routing — it is the most expensive and slowest option for domestic GBP and intra-EU EUR supplier payments

UK Faster Payments settles GBP transfers in seconds, 24/7, with individual transaction limits up to £1 million per payment under the Pay.UK scheme

SEPA Credit Transfer moves EUR payments across 36 countries same-day, with no correspondent bank in the chain and no deductions from the payment amount

A batch CSV file upload lets you execute 20–500 supplier payments in a single submission, replacing manual wire-by-wire SWIFT processing

An FCA-authorised EMI account gives direct access to both local rails from a single dashboard — no SWIFT membership, no correspondent bank overhead

A business running 15 SWIFT wires per week can realistically save £20,000–£30,000 per year by switching to local payment rails

Why SWIFT Is Costing You More Than You Realise on Supplier Payments

SWIFT — the Society for Worldwide Interbank Financial Telecommunication — is not a payment rail. It is a secure messaging network that carries instructions between financial institutions through a chain of correspondent banks, each of which holds accounts for the next institution in the route. Each correspondent in the chain may deduct its own processing fee before the funds arrive at the destination.

That architecture was designed for large-value international transactions moving between countries with no direct payment infrastructure. For a UK business paying a domestic supplier in GBP, or an EU counterpart in EUR, routing through SWIFT means paying for a correspondent chain that adds no operational value to the transaction.

The Hidden Fee Stack on Every SWIFT Transfer

The outgoing wire fee shown on your bank statement — typically £9.50–£25 at major UK banks — is only the first layer. Beneath it sit correspondent bank charges ranging from $10 to $30 per transfer, deducted silently from the payment amount in transit. If two correspondent banks are involved — common when routing between UK and non-Eurozone EU accounts — the deduction may apply at each hop.

For a business sending 15 supplier payments per week, the blended cost per wire — bank fee plus correspondent charges — typically falls between £30 and £50. Over 52 weeks, that is £23,400 to £39,000 in payment costs on a single recurring routine. That figure excludes the FX spread on any cross-currency leg and the staff time spent on manual reconciliation.

Speed and Predictability Problems with SWIFT

SWIFT settlement takes 2–3 business days under normal conditions, and longer when a payment hits a cut-off time or passes through a correspondent with a processing delay. A batch submitted Monday morning at 9am may not clear until Wednesday afternoon, or Thursday if any payment needs a second correspondent leg.

There are no real-time status updates on individual SWIFT transfers. Confirmation arrives by end-of-day notification or not at all until the beneficiary reports receipt. Finance teams typically spend hours each week cross-referencing bank statements against supplier remittances, chasing missing payments by email, and re-issuing recalls for returned funds. For businesses operating on tight supplier payment terms — net 30, net 15, or COD — this settlement lag carries real commercial risk.

The Local Rails That Replace SWIFT for Weekly Supplier Payments

For UK businesses processing batch supplier payments on UK local rails in GBP and EUR, two schemes replace SWIFT entirely — no correspondent bank, no 2–3 day delays, no per-wire fee stack. Together, Faster Payments and SEPA Credit Transfer cover every GBP–EUR supplier corridor where most UK businesses concentrate their SWIFT spend.

Faster Payments for GBP Supplier Payments

UK Faster Payments is the country's real-time interbank payment scheme, operated by Pay.UK. Payments settle in seconds, around the clock, every day of the year — including weekends and bank holidays. The scheme limit per individual transaction is £1,000,000, though the effective limit may vary by sending institution.

For batch supplier payments, Faster Payments is the natural SWIFT replacement for any GBP outgoing — domestic UK suppliers, manufacturers, logistics providers, UK-based freelancers invoicing in sterling, and weekly payroll runs for UK employees or contractors. To replace SWIFT with batch Faster Payments UK, the sending account must have direct scheme access, not BACS or a sponsor bank pipeline that re-routes instructions via SWIFT. The per-transaction cost through an FCA-authorised EMI account with direct access is typically pence, compared to £30–50 per SWIFT wire. Settlement reaches the supplier's sort code and account within seconds of batch execution.

SEPA Credit Transfer for EUR Supplier Payments

SEPA Credit Transfer (SCT) is the euro payment scheme covering 36 countries in the SEPA zone, administered by the European Payments Council (EPC). It routes EUR payments using IBAN and BIC identifiers with standard next-business-day settlement (D+1) and no correspondent bank in the chain — meaning no silent fee deductions in transit.

For UK businesses with EUR-denominated supplier contracts — EU manufacturers, German software vendors, Dutch logistics partners — SEPA Credit Transfer eliminates the SWIFT markup entirely. There are no correspondent charges, the fee is a flat rate per transfer, and the beneficiary receives the exact amount instructed. SEPA Instant Credit Transfer (SCT Inst) extends the scheme to real-time settlement: 10 seconds, 24/7, for transactions up to €100,000 per payment at participating institutions.

When SWIFT Is Still the Right Choice

SWIFT remains necessary for payments outside the GBP–EUR corridor: a USD invoice from a US supplier, a JPY payment to a Japanese manufacturer, or any transfer to a country not covered by the SEPA zone. The strategic shift is to stop defaulting to SWIFT for every cross-border payment and reserve it for corridors where no local rail exists.

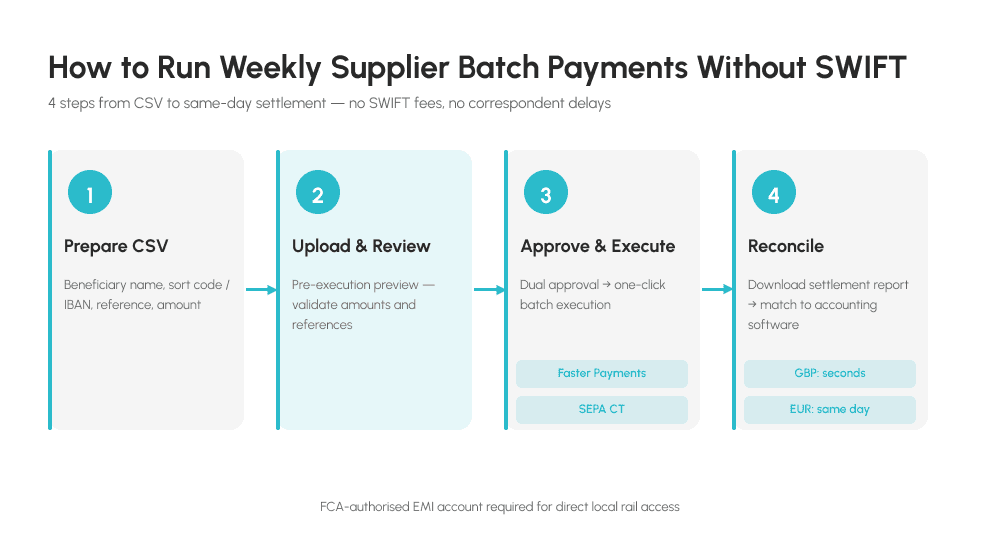

How to Run Weekly Supplier Batch Payments Without SWIFT — Step by Step

The step-by-step process to switch from SWIFT to local payment rails for supplier payments UK is straightforward: it requires no new integrations, no technical development, and most finance teams complete the migration in under a week. The critical enabler is an account with direct access to both Faster Payments and SEPA Credit Transfer and a batch file upload interface.

Step 1: Prepare Your Batch File in CSV Format

Most FCA-authorised EMI accounts accept payment batches in CSV format. Required fields for a GBP Faster Payments batch: beneficiary name, sort code (6 digits), account number (8 digits), payment reference (18 characters max), and amount in GBP to two decimal places. For EUR SEPA payments, replace sort code and account number with IBAN and BIC.

Many finance teams maintain two separate CSV templates — one for GBP runs, one for EUR — or a single file with a currency column if the platform supports multi-rail batch upload. For a detailed walkthrough of file formatting requirements, see the guide on CSV formatting for batch supplier payments. Validate the CSV before uploading: check for duplicate payment references, confirm amounts match approved invoices, and verify beneficiary names are consistent with your supplier records.

Step 2: Upload and Review in Your EMI Account

Upload the CSV through the batch payment interface. A well-designed EMI platform displays a pre-execution preview showing the number of payments, total debit amount, per-payment breakdown, and any validation errors — before a single payment is sent. Review the total value and any flagged rows carefully.

The pre-submission review step eliminates the most common errors in manual SWIFT entry: transposed digits, wrong amounts, duplicate references. Some platforms allow editing individual line items within the preview; others require you to correct the CSV and re-upload.

Step 3: Approve and Execute the Batch

For batches above a defined value threshold, a dual-approval workflow is the recommended control — one team member prepares and uploads the batch, a second reviews and authorises it. This mirrors the sign-off controls most finance teams already apply to SWIFT runs, and is natively supported by most FCA-authorised EMI platforms through role-based user access.

Once approved, the platform routes each payment to the appropriate rail: GBP lines via Faster Payments, EUR lines via SEPA Credit Transfer. GBP payments reach beneficiary accounts within seconds. EUR payments settle within the same business day. A full run of 25 supplier payments processes and settles in under a minute — compared to several hours of manual SWIFT submission.

Run your first SWIFT-free supplier batch this week

EQWIRE provides direct access to UK Faster Payments and SEPA Credit Transfer with batch CSV upload built in. No 2–3 day waits.

Step 4: Reconcile and Confirm Settlement

After execution, download the settlement report from your EMI account dashboard. A complete report includes the settled status of each individual payment, the exact settlement timestamp, the payment reference, and the beneficiary name — everything needed for line-by-line matching in your accounting software.

Because Faster Payments settles in seconds and SEPA Credit Transfer completes the same business day, the reconciliation for a Monday morning batch run can be finished by Monday afternoon. Flag returned or rejected payments immediately — most EMI platforms display rejection reasons in the settlement report. For a practical breakdown of the upload and reconciliation process, see the guide on batch payment file upload for supplier payroll.

What Type of Account Gives You Direct Access to Local Payment Rails?

Not all business accounts support batch file upload or originate payments directly over Faster Payments and SEPA Credit Transfer. The account structure matters significantly. Traditional UK high-street banks often route cross-border instructions through internal SWIFT-format pipelines, and their batch payment functionality is typically limited to BACS file submissions — suitable for 3-day payroll cycles, but not for same-day supplier runs.

For finance teams asking how to automate weekly supplier batch payments UK without SWIFT using an EMI account, the CSV upload workflow is the lowest-friction migration path available. FCA-authorised Electronic Money Institutions (EMIs) are designed specifically for this kind of operational payment efficiency at scale. Unlike EMIs that hold only FCA registration (a lighter-touch regime), FCA-authorised EMIs hold a full Electronic Money Institution licence — requiring client funds to be safeguarded in segregated accounts, legally ring-fenced from the institution's own operating capital.

For batch supplier payment use, the account should offer: CSV batch upload for both GBP and EUR in a single interface; direct Faster Payments access (not re-routed via a sponsor bank's SWIFT pipeline); SEPA Credit Transfer origination from a named EUR IBAN; multi-user access with configurable approval workflows; and real-time payment status with downloadable settlement reports.

A multi-currency account holding GBP, EUR, and USD consolidates incoming receipts and outgoing supplier batches in one place — removing the overhead of sweeping funds between separate accounts before each payment run, a common friction point for import/export businesses.

Cost Comparison: SWIFT vs Faster Payments and SEPA for a Weekly Supplier Run

The table below compares the per-payment costs and operational characteristics of SWIFT against local rails for a typical UK SMB. Businesses that avoid SWIFT fees on weekly supplier payments UK by routing through Faster Payments and SEPA CT retain the same beneficiary coverage at a fraction of the annual cost.

SWIFT Wire | Faster Payments (GBP) | SEPA Credit Transfer (EUR) | |

|---|---|---|---|

Bank / platform fee | £15–25 | £0.10–0.30 | £0.10–0.30 |

Correspondent bank fee | $10–30 | None | None |

Settlement time | 2–3 business days | Seconds | Same business day |

24/7 availability | No | Yes | No (standard) / Yes (SCT Inst) |

Batch file upload | Limited at most banks | CSV supported | CSV supported |

Real-time status | No | Yes | Yes |

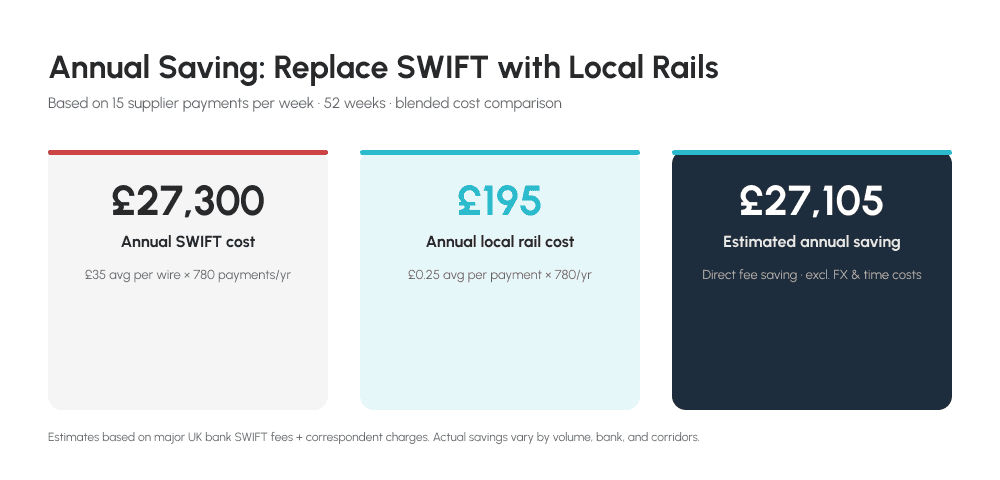

For a business sending 15 supplier payments per week, the annual saving from switching to local rails is substantial:

SWIFT: 15 payments × £35 blended average × 52 weeks = £27,300/year

Faster Payments + SEPA CT: 15 payments × £0.25 average × 52 weeks = £195/year

Estimated annual saving: £27,105

Exact figures depend on your bank's fee structure and the payment corridors involved. The relative saving — local rails versus SWIFT for domestic and intra-EU payments — remains consistent at all volume levels. For businesses already using Faster Payments to automate other recurring payment types, the same infrastructure handles supplier runs without additional setup. See how businesses automate payouts via Faster Payments.

FAQ

Can UK businesses really run weekly supplier batch payments without SWIFT?

Yes. For GBP payments to UK-based suppliers, UK Faster Payments settles in seconds, 24/7, with per-payment limits up to £1 million under the Pay.UK scheme. For EUR suppliers in the SEPA zone, SEPA Credit Transfer is available through FCA-authorised EMI accounts with no SWIFT routing required. The only transactions that still need SWIFT are those outside the GBP–EUR corridor — for example, USD to a US supplier.

How do I replace SWIFT wire with Faster Payments for weekly supplier payments?

Open an FCA-authorised EMI account that supports batch CSV upload. Prepare a file with beneficiary name, sort code, account number, reference, and amount for GBP payments — or IBAN and BIC for EUR. Upload the CSV each Monday, review the batch preview, apply dual approval if required, and execute. GBP payments reach suppliers within seconds; EUR payments settle the same business day via SEPA Credit Transfer.

How do I run weekly supplier batch payments using local rails UK without SWIFT fees?

Direct local rail access requires an FCA-authorised EMI account with built-in batch upload. GBP payments route via Faster Payments — settling in seconds with no correspondent bank charge. EUR payments route via SEPA Credit Transfer — same-day settlement at a flat per-payment fee. Per-payment cost drops from £30–50 per SWIFT wire to pence, eliminating SWIFT fees entirely for GBP and EUR supplier runs.

How much can businesses save replacing SWIFT with Faster Payments UK?

A business sending 15 wires per week typically pays £25–45 per transaction in combined bank and correspondent bank charges. Switching to local rails for the same payments reduces per-transaction cost to pence — a direct saving of £19,500–£35,000 per year at that volume, before accounting for FX spread reduction and time recovered from manual reconciliation.

What is an alternative to SWIFT for regular UK and EU supplier payments?

For GBP payments, UK Faster Payments is the primary SWIFT alternative — settling in seconds, 24/7, with no correspondent fees. For EUR payments within the SEPA zone, SEPA Credit Transfer provides the same country coverage at a flat fee with no correspondent deductions. Together, these two rails cover the GBP–EUR corridors where most UK businesses concentrate their SWIFT spend. Access both through an FCA-authorised EMI account with batch file upload.

Stop paying SWIFT fees on predictable weekly supplier runs

Switch to local rails with no minimum volume, no lock-in, and same-day settlement for both GBP and EUR suppliers.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)