•

•

REST API Payments UK: Integrate Faster Payments and SEPA Into Your Platform

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A fintech engineering team spends eight weeks integrating with their UK bank's corporate API. They expect real-time GBP transfers and webhook status events. What they get: batch settlement with a 3 p.m. cut-off, no SEPA support, and a polling endpoint that requires them to check payment status every 30 seconds.

Meanwhile, their EUR payouts are routed through a second provider — a separate contract, a second set of credentials, and a second codebase to maintain. Two integrations. Two failure points. Double the operational overhead.

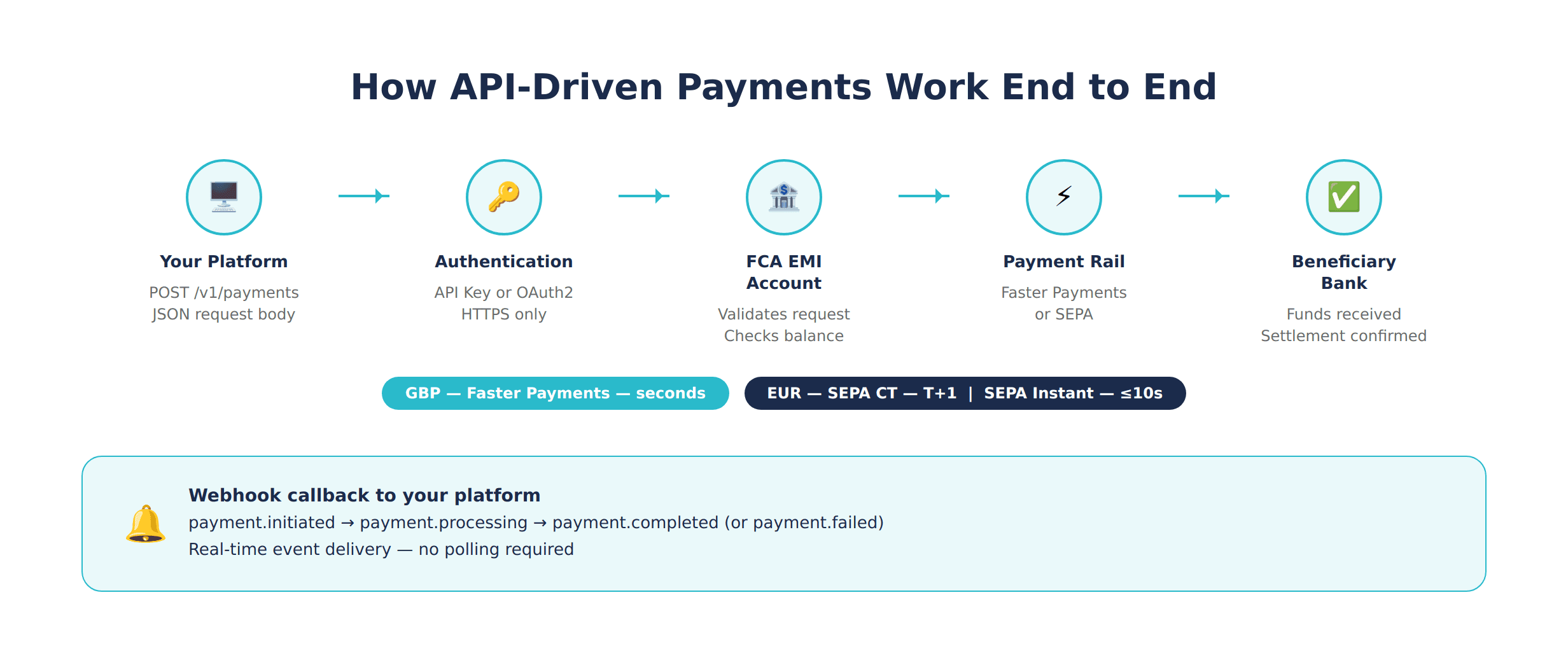

This is the reality of building payment infrastructure on top of a legacy bank API. API-driven payments built on a modern, FCA-regulated EMI account work differently: one REST integration covers UK Faster Payments (GBP) and SEPA (EUR), with real-time webhook events, sandbox testing, and a single set of credentials.

This guide covers how to integrate Faster Payments and SEPA via REST API from a UK EMI account — step by step, from account setup through production go-live.

[aa key-takeaways]

Key Takeaways

A modern API-driven payments setup exposes Faster Payments (GBP) and SEPA (EUR) through a single REST interface — no second provider needed

Authentication uses API key or OAuth2; all calls are HTTPS with JSON request and response bodies

Sandbox environments replicate production flows — test payment creation, webhook delivery, and error handling before any live funds are involved

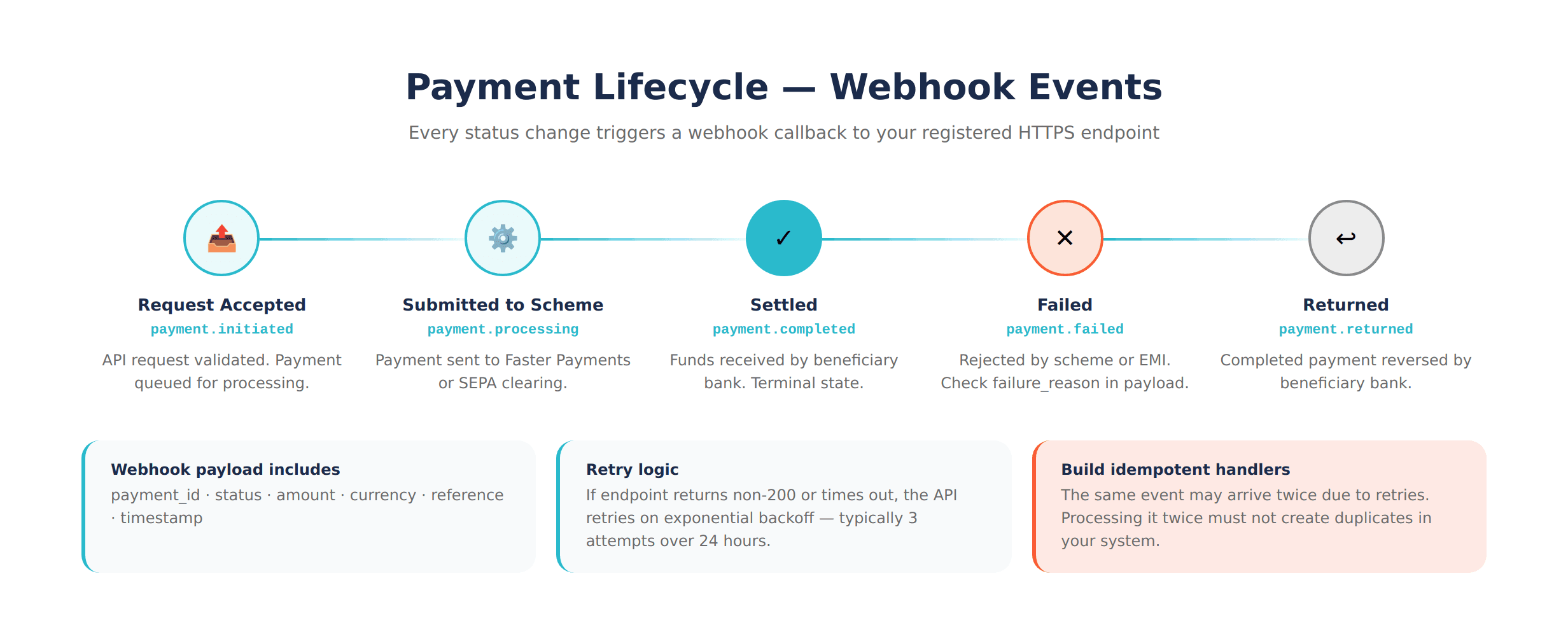

Webhook events track the full payment lifecycle: initiated → processing → completed / failed / returned

Idempotency keys prevent duplicate payments when network errors cause retry loops

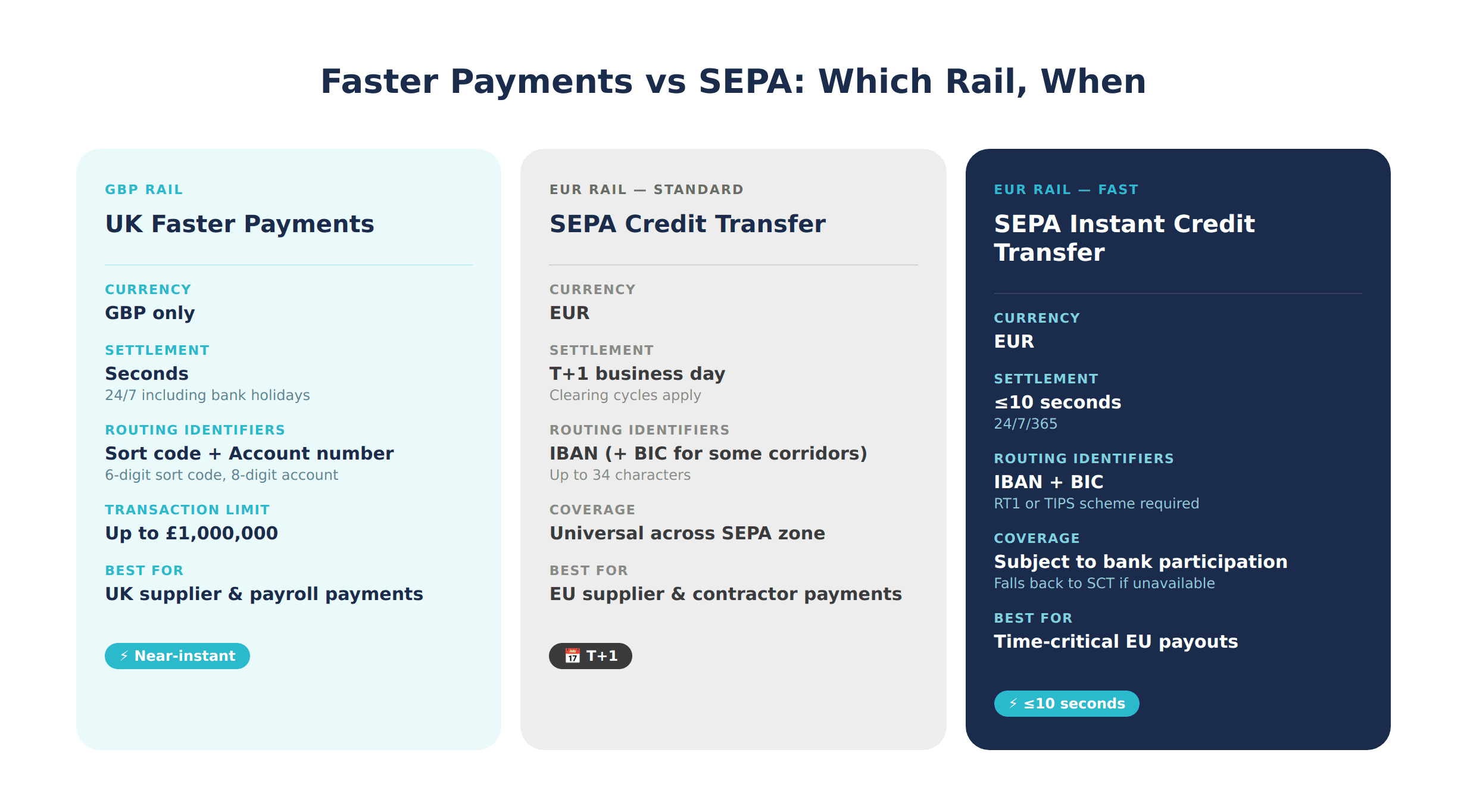

Faster Payments settles near-instantly 24/7; SEPA Credit Transfer is T+1; SEPA Instant completes in ≤10 seconds

[aa btn]Open an EQWIRE Account[/aa]

[/aa]

Step 1 — Open a UK EMI Account with API Access

Not every UK business account offers a usable REST API. Traditional high-street banks may expose API endpoints in documentation, but in practice those APIs are often limited to read-only account data or require proprietary formats that do not support real-time payment initiation, webhooks, or SEPA.

The practical route to a developer-friendly banking API UK payments setup is an FCA-authorised Electronic Money Institution (EMI). EMIs operate under the Electronic Money Regulations 2011 and are regulated by the Financial Conduct Authority, which authorises them to issue electronic money and provide payment services — including direct access to UK payment schemes and SEPA.

EQWIRE is an FCA-regulated EMI that provides REST API access covering both Faster Payments and SEPA from a single account. As noted in a deeper comparison of FCA-authorised EMIs vs traditional bank accounts, the key difference for API-integrating businesses is scheme connectivity — EMIs are built for it, most banks are not.

[aa fast-fact]

Fast Fact: The FCA Electronic Money Institution register lists over 180 authorised EMIs in the UK as of 2026. Not all offer REST API access for payment initiation — check API documentation and sandbox availability before onboarding.

[/aa]

Step 2 — Authenticate and Connect to the Sandbox

Two authentication patterns are standard across modern payment APIs:

API Key Authentication

API key authentication is the simpler option. A secret key is generated in the account dashboard and passed as a header on every request. This pattern suits server-to-server integrations where a single account initiates all payments — payroll systems, supplier payment runs, or internal payout automation.

OAuth2 Authentication

OAuth2 is used when a platform needs to act on behalf of multiple connected accounts. This is the correct pattern for embedding Faster Payments into a SaaS platform via UK payment API — where the platform triggers payments from its clients' accounts, not its own.

Connecting to the Sandbox

Before touching production credentials, connect to the sandbox base URL. The sandbox environment mirrors production: it accepts the same request structure, returns realistic response payloads, and delivers webhook events to a registered endpoint. A successful response returns account details including the GBP account number, sort code, and IBAN.

Step 3 — Initiate a UK Faster Payment via REST API

UK Faster Payments is a real-time GBP payment scheme that operates 24 hours a day, 365 days a year, including bank holidays. According to Pay.UK, the scheme processes individual transfers up to £1,000,000 per transaction, with the vast majority settling within seconds of initiation.

Required Fields — Account Number, Sort Code, Amount, Reference

A GBP Faster Payment requires: beneficiary account number (8 digits), sort code (6 digits, no dashes), amount in pence as an integer, and a payment reference of up to 18 characters visible to the beneficiary.

Request Structure and Response Fields

A successful response returns a payment_id, an initial status of initiated, and a timestamp. The payment then transitions through the lifecycle asynchronously — status updates arrive via webhook, not in the initial response.

Common Errors and Resolution

Three errors account for the majority of Faster Payment failures at integration: INVALID_SORT_CODE (must be exactly 6 digits, no hyphens), AMOUNT_EXCEEDS_LIMIT (check the configured per-transaction limit), and INSUFFICIENT_BALANCE (fund the GBP balance before payment initiation).

Step 4 — Initiate a SEPA Payment via the Same API

The same REST API base URL handles SEPA transfers. The payment_type parameter switches the rail from Faster Payments to SEPA Credit Transfer or SEPA Instant — no second provider, no separate authentication.

The ECB SEPA framework governs two distinct transfer schemes available via the payment API UK Faster Payments SEPA setup.

Required Fields — IBAN, BIC, EUR Amount, Creditor Reference

A SEPA Credit Transfer requires: beneficiary IBAN (up to 34 chars), BIC (8 or 11 chars, required for some non-Eurozone corridors), EUR amount in eurocents as an integer, creditor name, and a payment reference of up to 35 characters.

SCT vs SEPA Instant — How to Specify the Rail

To specify SEPA Instant, set payment_type to sepa_instant. The API will attempt the Instant rail first and confirm whether the beneficiary bank participates in RT1 or TIPS.

SEPA Instant Coverage and Fallback Logic

SEPA Instant settles in ≤10 seconds, 24/7. If the beneficiary bank is not reachable via SEPA Instant, the API falls back to SEPA Credit Transfer at T+1. Build your platform logic to handle both settlement timings.

[aa cta]

Add Faster Payments and SEPA to Your Platform Without a Second Provider

EQWIRE's API gives you GBP and EUR payment rails, webhooks, and a sandbox environment — all from one FCA-regulated account.

[aa btn]Get API Access[/aa]

[/aa]

Step 5 — Configure Webhooks for Payment Status Tracking

Polling for payment status is inefficient. Payment webhooks UK business account integrations use an event-driven model: the API calls your endpoint when something changes, not the other way around.

Registering Your Webhook Endpoint

Register a webhook URL in the account dashboard or via the API. The endpoint must be publicly reachable over HTTPS, capable of returning HTTP 200 within 5 seconds, and protected by signature verification.

Payment Lifecycle Events and Payload Structure

Five events cover the full payment lifecycle: payment.initiated, payment.processing, payment.completed, payment.failed, and payment.returned. The webhook payload includes payment_id, status, amount, currency, reference, and timestamp.

Retry Logic and Failure Handling

If the webhook endpoint returns a non-200 status or times out, the API retries delivery on an exponential backoff schedule — typically 3 retries over 24 hours. Build webhook handlers to be idempotent: processing the same event twice must not create duplicate records.

[aa fast-fact]

Fast Fact: A developer API for UK GBP EUR payments with webhooks and sandbox eliminates the need for status-polling loops. For a platform processing 500 payments per week, removing polling can reduce API calls by 90% or more compared to a 30-second poll interval.

[/aa]

Step 6 — Sandbox Testing Before Go-Live

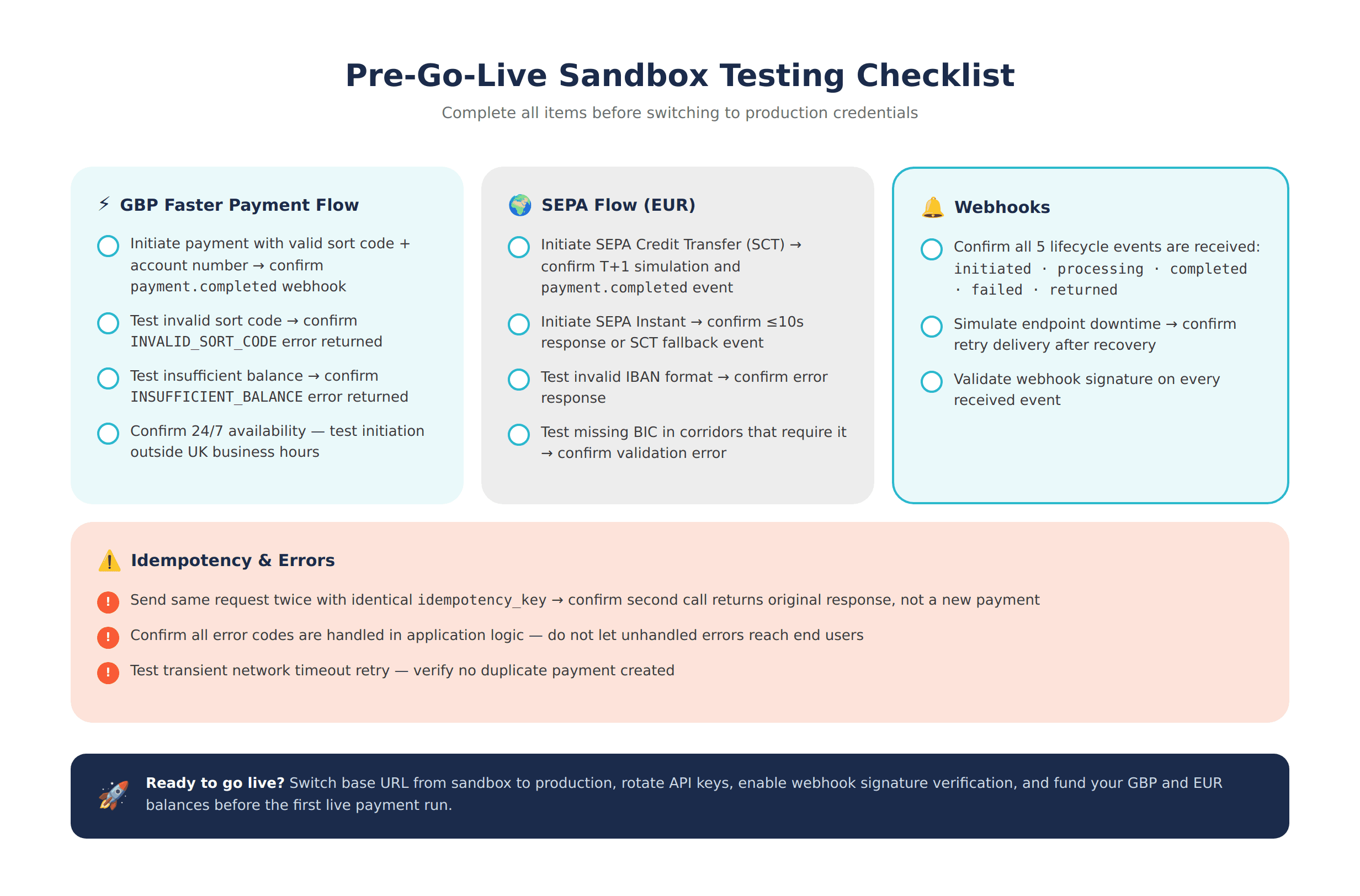

Sandbox API testing for UK Faster Payments integration is not optional — it is the only way to validate payment initiation, webhook delivery, error handling, and idempotency before real funds are involved.

What the Sandbox Environment Replicates

The sandbox mirrors production: payment initiation endpoints accept the same request structure, response payloads match production schemas exactly, webhook events are delivered to the registered endpoint, and balance simulation allows testing of insufficient-funds scenarios.

Pre-Go-Live Testing Checklist

Work through each category before switching to production credentials: GBP Faster Payment flow (valid and error paths), SEPA flows (SCT and Instant), webhook delivery and retry, idempotency key behaviour on duplicate requests, and all documented error codes.

For a practical overview of how batch and single-payment flows complement each other, see batch payment automation for UK businesses.

Step 7 — Going Live — Production Checklist and Operational Setup

Switching from sandbox to production requires more than swapping a base URL. The step-by-step process to integrate UK Faster Payments and SEPA via REST API into a SaaS platform ends here — at a production environment that is hardened, monitored, and operationally ready.

Key production readiness items: API keys stored in environment variables (never hardcoded); webhook endpoint validates the signature on every inbound event; idempotency keys implemented on every payment initiation call; error handling and alerting configured on payment.failed and payment.returned events; payment reference field maps directly to internal invoice or order ID; GBP and EUR balances funded before the first production payment run.

API-driven payments infrastructure built on a single FCA-regulated EMI account — covering UK Faster Payments and SEPA from one integration — removes the two-provider problem that slows most fintech and SaaS payment builds. Maintain one codebase, one set of credentials, and one reconciliation process.

[aa cta]

Your Payment Integration Is Ready — Your Account Should Be Too

Open an EQWIRE multi-currency account with API access and start sending GBP and EUR payments from a single integration.

[aa btn]Open an Account[/aa]

[/aa]

FAQ

How do I integrate Faster Payments and SEPA via REST API UK step by step?

Open an account with an FCA-regulated EMI that provides REST API access. Authenticate via API key or OAuth2 and connect to the sandbox. Initiate a GBP payment using sort code and account number, and a EUR payment using IBAN and BIC. Configure webhook callbacks to receive status events across the payment lifecycle. Test both payment flows in the sandbox environment before switching to production credentials. The full process from account setup to go-live typically takes between three and ten working days.

What does sandbox API testing for UK Faster Payments integration look like?

A sandbox environment accepts the same API requests as production, returns realistic response payloads, and delivers webhook events to a registered HTTPS endpoint. Testing covers happy-path flows as well as failure scenarios: invalid sort code, insufficient balance, invalid IBAN, and endpoint unavailability triggering webhook retries. Both GBP and EUR flows should be tested end to end, including idempotency key behaviour on duplicate requests.

How do I embed Faster Payments into a SaaS platform via UK payment API?

Use the payment initiation endpoint to trigger GBP payouts programmatically from platform logic. With OAuth2 authentication, the platform can initiate payments on behalf of connected accounts. Webhooks deliver real-time status updates back to the platform without polling. This architecture is standard for payroll platforms, marketplace payout flows, and subscription billing systems.

What fields are required for a SEPA payment via REST API from a UK account?

A SEPA Credit Transfer requires the beneficiary IBAN, BIC (required for some non-Eurozone corridors), EUR amount in eurocents, creditor name, and a payment reference of up to 35 characters. For SEPA Instant, the payment_type is set to sepa_instant — the API falls back to standard SCT if the beneficiary bank does not participate in RT1 or TIPS.

How do idempotency keys prevent duplicate payments in a REST API integration?

An idempotency key is a unique string included in the request header. If a network timeout causes a payment request to fail before a response is received, retrying the request with the same key returns the original response — not a second payment. Construct idempotency keys from a deterministic combination of internal references such as the invoice ID plus a date suffix.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)