•

•

XCD Account for Caribbean Offshore Companies: Hold East Caribbean Dollars Offshore

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Caribbean offshore companies, whether formed in Nevis or Antigua, regularly encounter a specific banking problem: local ECCB-regulated banks decline IBC applications without detailed explanation, citing risk policy. The result is that an IBC with legitimate East Caribbean dollar revenues has no clear banking path.

Opening an XCD account Caribbean offshore company UK EMI is the practical solution that offshore structures across both jurisdictions have taken: accessing FCA-regulated payment infrastructure from a UK electronic money institution, without requiring a local Caribbean bank relationship. This guide covers the four-step process for Nevis and Antigua IBCs: selecting a compliant EMI, preparing the document package, passing KYB review, and activating the XCD account. For a complete application, the process typically takes 5–10 business days.

[aa key-takeaways]

Key Takeaways

Opening an XCD account for a Caribbean offshore company at a UK EMI requires four sequential steps: EMI selection, document preparation, KYB review, and account activation.

The document package must include a certificate of good standing issued within the past 6 months — expired certificates are the single most common rejection cause.

UK EMIs must identify every beneficial owner holding more than 25% of the IBC under the Money Laundering Regulations 2017 — nominee director structures require a separate UBO disclosure letter.

The XCD–USD exchange rate is fixed at 2.70 XCD per USD by the Eastern Caribbean Central Bank — accounts are funded via SWIFT wire, not SEPA or Faster Payments.

Onboarding at an FCA-authorised EMI typically takes 5–10 business days for a complete, well-documented application.

[aa btn]Book a Call[/aa]

[/aa]

Step 1 — Choose a UK FCA-Authorised EMI That Accepts Caribbean IBCs

Selecting the right provider for an XCD account Caribbean offshore company UK EMI application is the first decision — and the one that eliminates the most wasted compliance effort. Not all UK electronic money institutions accept offshore company structures.

The first requirement is confirming FCA authorisation under the Electronic Money Regulations 2011 — and verifying that the EMI's terms of service do not exclude Caribbean jurisdictions or IBC structures. EMIs that quietly exclude offshore entities through acceptable use policy language will reject the application immediately, with no credit applied to the compliance work already invested.

Similar structures — such as Bermuda-registered companies — have accessed UK payment accounts through FCA-authorised EMIs under the same regulatory framework.

What to Look For: FCA Registration, Multi-Currency Wallet, SWIFT Support

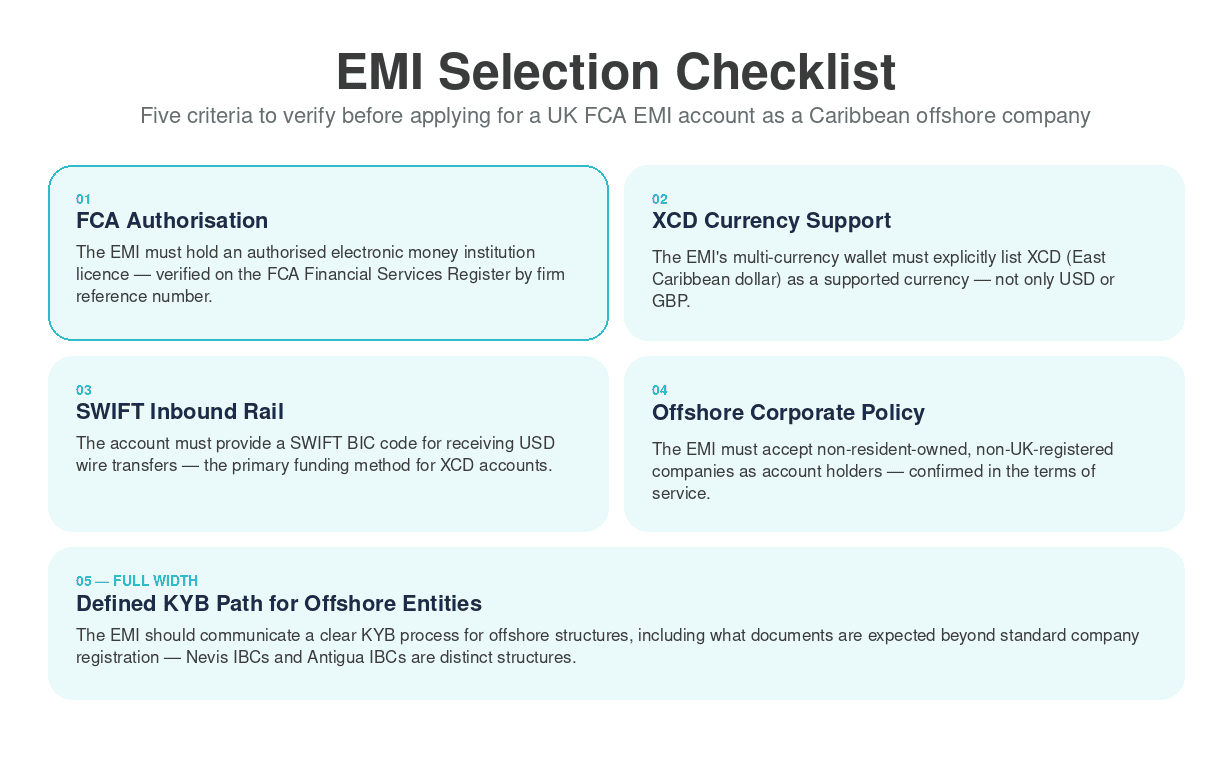

Before submitting an application, finance teams should verify five criteria:

FCA authorisation: The EMI must hold an authorised electronic money institution licence — confirmed on the FCA Financial Services Register by firm reference number.

XCD support: The EMI's multi-currency wallet must explicitly list XCD (East Caribbean dollar) as a supported currency, not only USD or GBP.

SWIFT inbound: The account must provide a SWIFT BIC code for receiving USD wire transfers — the primary funding rail for XCD accounts.

Offshore corporate policy: The EMI must accept non-resident-owned, non-UK-registered companies as account holders.

KYB process for offshore entities: The EMI should communicate a defined KYB path for offshore structures, including what documents are expected beyond standard company registration.

Red Flags — EMIs That Don't Support Offshore Entities or XCD Pairs

Some UK EMIs exclude offshore structures through policy language that is not prominently displayed:

"UK-incorporated entities only" in the eligibility section

"No high-risk jurisdictions" — with Caribbean territories on an internal blocklist

"Directors must hold UK residency" — which disqualifies most IBC directors

XCD absent from the supported currency list

The practical check: reviewing the acceptable use policy in full before starting an application is a five-minute step that eliminates the most common source of wasted compliance effort. Contacting the compliance team directly with the question "Do you accept Nevis IBCs or Antigua IBCs with non-resident beneficial owners?" resolves eligibility before any documentation effort begins.

Step 2 — Prepare the Document Package for Your IBC

Document preparation determines whether an application succeeds or fails. The majority of offshore IBC UK electronic money institution rejections stem from incomplete or outdated documentation, not from jurisdiction risk.

[aa fast-fact]

Fast Fact: An expired certificate of good standing is the most frequently cited document failure in offshore company EMI applications. EMIs require this certificate to have been issued within the previous 6 months.

[/aa]

Required Corporate Documents

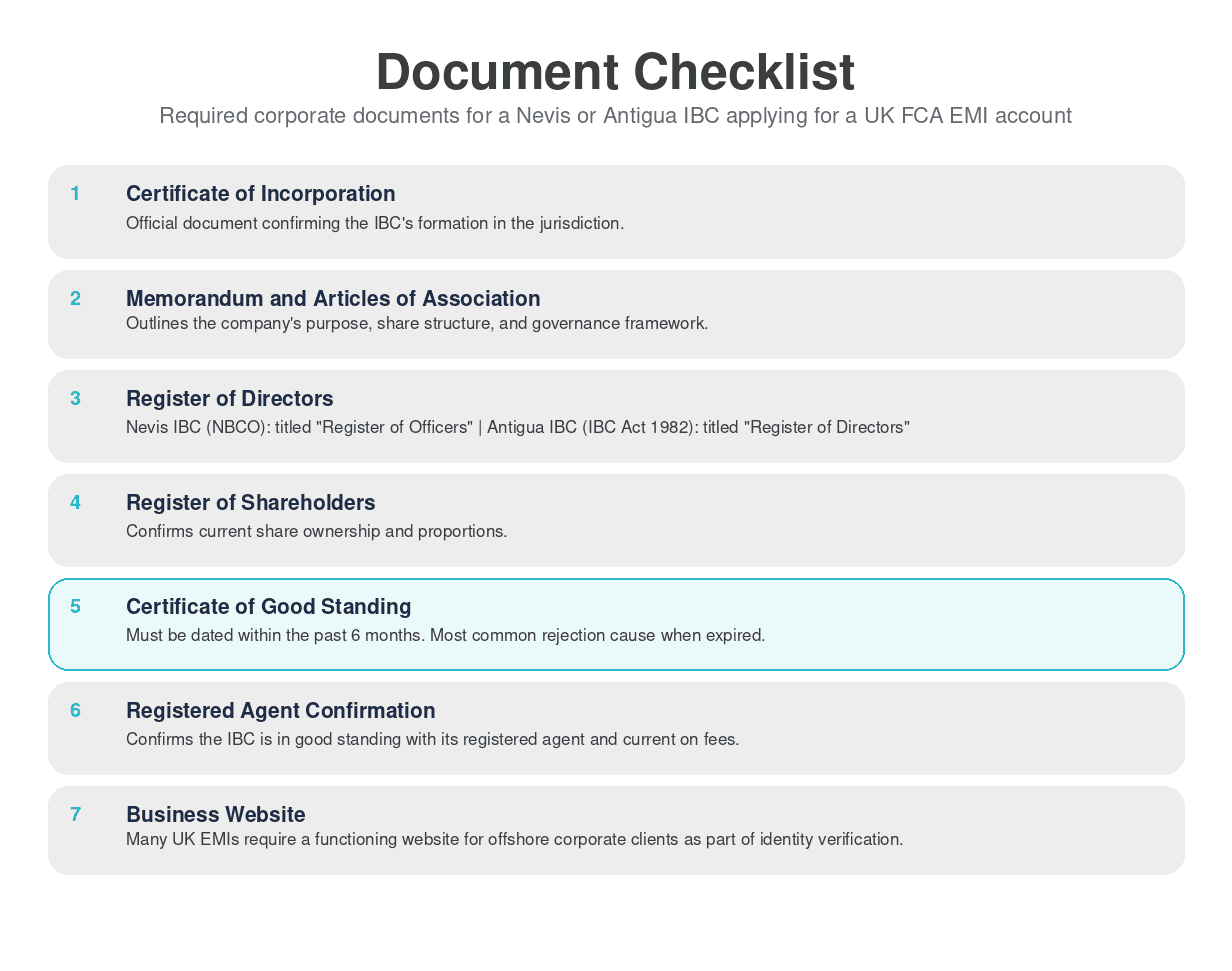

A Nevis or Antigua IBC opening a UK EMI account must submit:

Certificate of incorporation — the official document confirming the IBC's formation in the jurisdiction.

Memorandum and articles of association — outlines the company's purpose, share structure, and governance framework.

Register of directors — lists all current directors. For Nevis IBCs formed under the Nevis Business Corporation Ordinance, this is titled "Register of Officers." For Antigua IBCs under the International Business Corporations Act 1982, the equivalent document is the "Register of Directors."

Register of shareholders — confirms current share ownership and proportions.

Certificate of good standing — issued by the registered agent or local authority, dated within the past 6 months.

Registered agent confirmation — confirms the IBC is in good standing with its registered agent and current on fees.

Business website — many UK EMIs now require a functioning website for offshore corporate clients as part of identity verification for business activity.

Nevis and Antigua IBCs should confirm exact document names with their registered agent before compiling the package. Document naming conventions differ between the two jurisdictions, and mislabelled files are a common cause of unnecessary delays.

Beneficial Ownership Disclosure — What EMIs Need for Offshore Structures

Under the UK Money Laundering Regulations 2017, EMIs must identify every person who holds or controls more than 25% of a company — including offshore structures. For an Antigua IBC UK payment account application, this means full UBO documentation for every qualifying beneficial owner.

For a straightforward structure where the beneficial owners also serve as directors, the standard documents apply: a certified copy of a valid passport and recent proof of address (utility bill or bank statement, no older than 3 months) for each UBO.

The complication arises with nominee director structures — common in Caribbean IBCs where a professional nominee holds the directorship on paper. In this case, the EMI requires:

A signed UBO declaration letter naming the actual beneficial owner

Full identity documents for the actual beneficial owner (not the nominee)

A letter from the nominee service provider confirming the nominee relationship

Failing to disclose the actual beneficial owner — or submitting only the nominee's documents — is the second most common reason for rejection at a UK FCA-regulated EMI.

Common Errors That Cause Application Rejections

Expired certificate of good standing — Fix: request a fresh certificate from the registered agent before submitting (typically 1–5 business days).

Missing UBO declaration — Fix: include a signed declaration letter for every beneficial owner above the 25% threshold.

Nominee director with no UBO letter — Fix: prepare a nominee relationship letter from the registered agent plus full identity documents for the actual beneficial owner.

No source of funds explanation — Fix: include a written description of the IBC's business activity and the expected origin of the initial deposit.

Registered agent address used as business address — Fix: provide the actual operating address or principal place of business.

[aa cta]

Open an XCD Account for Your Caribbean IBC

EQWIRE accepts Nevis and Antigua IBCs — accounts live in as little as 5 business days.

[aa btn]Start Your Application[/aa]

[/aa]

Step 3 — Submit the Application and Pass KYB

KYB — Know Your Business — is the verification process a UK EMI uses to assess a corporate applicant. For a Caribbean offshore company, KYB is distinct from KYC (Know Your Customer), which verifies individual identity. KYB verifies the entity itself: its legal existence, ownership structure, business activity, and source of funds.

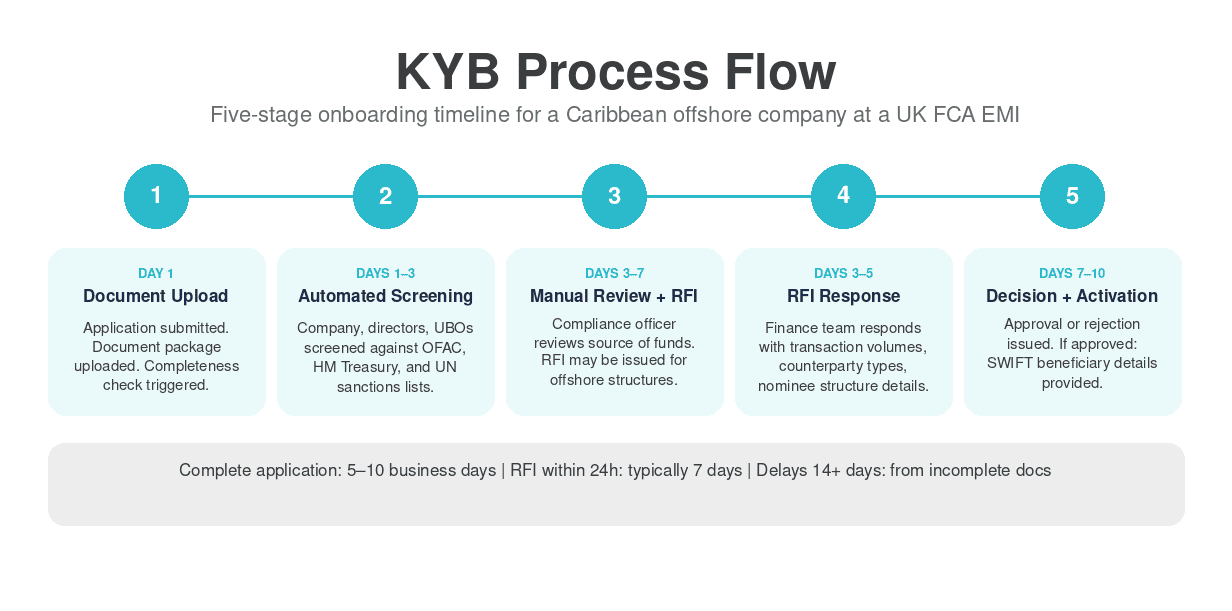

For a complete XCD business account Nevis IBC or Antigua IBC application, the KYB process moves through five stages.

What Happens During KYB Review for a Caribbean Offshore Company

Document upload and initial completeness check — The onboarding system reviews the document package. Missing items trigger an immediate request for additional information (RFI) before the file proceeds.

Automated compliance screening — The company name, directors, and UBOs are screened against sanctions lists: OFAC, HM Treasury, UN.

Compliance team manual review — A compliance officer reviews the full file. This is where the source of funds explanation and business activity description are assessed in detail.

RFI (Request for Information) — Offshore structures commonly receive an RFI during days 3–5, requesting context: expected monthly transaction volumes, types of counterparties, or clarification on the nominee structure.

Decision and account activation — Approval or rejection, with a stated reason in the case of rejection.

During the RFI stage, specific and complete responses reduce processing time significantly. Finance teams should be prepared to state: the industries the IBC operates in, the countries it transacts with, the approximate monthly inflow, and the purpose of holding XCD balances.

BVI companies accessing UK bank details through UK EMIs follow the same KYB timeline structure — the process is consistent across most offshore company jurisdictions.

Typical Onboarding Timeline and What to Expect at Each Stage

[aa fast-fact]

Fast Fact: For a Caribbean offshore company with a complete and well-prepared document package, onboarding at a UK FCA-authorised EMI typically takes 5–10 business days — a timeline that compares favourably with locally-incorporated UK company applications that involve complex group structures.

[/aa]

Day 1: Application submitted; document package uploaded to the EMI's onboarding portal.

Days 1–3: Automated compliance checks complete; account manager assigned.

Days 3–7: Compliance manual review; potential RFI issued and responded to.

Days 7–10: Decision issued; if approved, account activated and SWIFT beneficiary details provided.

An XCD account for Nevis IBC UK FCA applications that receive an RFI early — and respond within 24 hours — typically complete within 7 business days. Delays of 14+ days are almost always attributable to delayed RFI responses or incomplete initial documentation.

Step 4 — Activate the XCD Account and Make Your First Transfer

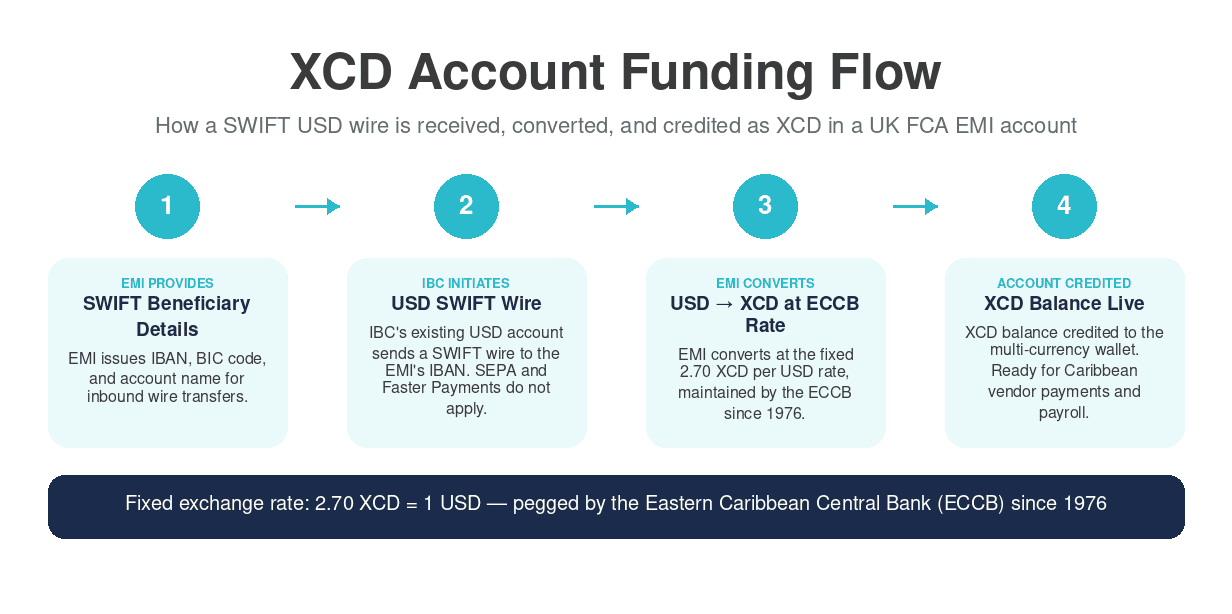

Once KYB approval is confirmed, the EMI activates the account and provides SWIFT beneficiary details — IBAN, BIC code, and account name — for inbound wire transfers. The XCD account is live. The first step is funding it.

Funding the Account — SWIFT Inflow From USD or GBP

The East Caribbean dollar (XCD) is pegged to the US dollar at a fixed rate of 2.70 XCD per USD, a rate maintained by the Eastern Caribbean Central Bank (ECCB) since 1976. The ECCB governs the currency union across eight member states, including Antigua and Barbuda and Saint Kitts and Nevis.

Funding an XCD account requires a SWIFT wire — not SEPA, which covers EUR-denominated payments only within the SEPA zone, and not Faster Payments, which is limited to GBP transactions within the UK. A Caribbean offshore company UK FCA EMI account funded from a USD source uses SWIFT as the only available inbound rail.

The practical funding sequence:

The EMI provides SWIFT beneficiary details: IBAN, BIC, and account name.

The IBC's existing USD account initiates a SWIFT wire to the provided IBAN.

The EMI converts the USD to XCD at the prevailing rate — based on the 2.70:1 ECCB peg — and credits the XCD balance.

The account is ready for outgoing XCD payments.

For Caribbean offshore companies that also require EUR access, SEPA payments as an offshore business require a separate EUR IBAN channel — distinct from the XCD wallet.

Setting Up Payment Instructions for XCD Outflows

XCD outbound SWIFT transfers from a UK EMI account are possible but less common. Most XCD spending occurs within the ECCB zone — to Caribbean vendors, local payroll, or intercompany transfers between entities in member states.

For international payables denominated in USD or GBP, the standard approach is to convert the XCD balance to USD or GBP within the multi-currency wallet, then initiate a SWIFT outflow in the target currency. This avoids double conversion costs and uses more liquid payment rails.

Common Mistakes Caribbean Offshore Companies Make With UK EMI Accounts

Understanding how a Nevis or Antigua IBC holds XCD East Caribbean dollars in a UK FCA EMI account is only part of the equation. The mistakes below account for the most common failures at each stage — from application through to ongoing account management.

Applying without checking the EMI's offshore entity policy — Terms of service vary significantly. Some EMIs that list 30+ currencies still exclude IBCs from Caribbean jurisdictions in their acceptable use policy. The check takes five minutes. The rejection wastes weeks.

Submitting an expired certificate of good standing — A certificate expired two weeks prior triggers rejection. Certificate refresh takes 1–5 business days from most registered agents — completing this before starting the application eliminates the most common single point of failure.

Failing to disclose all UBOs upfront — Compliance teams identify undisclosed beneficial owners during automated sanctions screening. Incomplete UBO disclosure extends review time and leads to rejection in a high proportion of offshore company cases.

No source of funds description for the initial deposit — EMIs are required to understand the origin of funds entering the account. A single paragraph describing the IBC's revenue model — what it does, where it earns, and what the initial deposit represents — is sufficient to prevent an RFI that adds multiple days to the review timeline.

Expecting a traditional banking relationship — UK EMI accounts do not include credit facilities, overdrafts, or physical payment cards by default. The account is a multi-currency wallet with SWIFT connectivity. Finance teams that approach it as a pure payment infrastructure tool — not a bank — manage expectations correctly from the outset.

FAQ

How do I open an XCD account for my Nevis IBC at a UK EMI?

To open an XCD account for a Nevis IBC through a UK FCA-authorised EMI, the process follows four steps: selecting an EMI that explicitly accepts Nevis IBCs and supports XCD as a currency, preparing the full corporate document package including a certificate of good standing dated within the past 6 months and UBO declarations for all beneficial owners above 25%, submitting the application and passing KYB review, and activating the account for SWIFT-funded XCD transactions. The complete process — from initial application through to how to open an XCD account for a Caribbean offshore company at a UK EMI and receive the first inbound wire — typically takes 5–10 business days for a well-prepared application.

What documents does an Antigua IBC need to open a UK FCA EMI account?

An Antigua IBC UK payment account application requires: certificate of incorporation, memorandum and articles of association (under the International Business Corporations Act 1982), register of directors and shareholders, certificate of good standing dated within the past 6 months, and UBO declarations with supporting identity documents — certified passport copy and proof of address — for all beneficial owners holding more than 25% of the company. A description of the company's business activity and source of the initial deposit is also standard. The UK Money Laundering Regulations 2017 require EMIs to carry out this level of due diligence on all corporate applicants, regardless of jurisdiction.

How long does it take to open a Caribbean offshore company account at a UK EMI?

For a Caribbean offshore company with a complete document package, onboarding at a UK FCA EMI typically takes 5–10 business days. The timeline runs: Day 1 for application submission, Days 1–3 for automated compliance checks, Days 3–7 for manual compliance review with a potential request for additional information, and Days 7–10 for approval and account activation. Structures involving nominee directors or multiple beneficial owners may take an additional 2–5 business days if an RFI is issued and requires supporting documentation.

Can I hold East Caribbean dollars in a UK EMI account as an offshore company?

Yes. A UK FCA-authorised EMI with multi-currency wallet capability can hold East Caribbean dollars (XCD) for a Caribbean offshore company, including Nevis and Antigua IBCs. The XCD is issued and regulated by the Eastern Caribbean Central Bank (ECCB) and has been pegged to the US dollar at a fixed rate of 2.70 XCD per USD since 1976. The account is funded via SWIFT wire — typically a USD transfer that the EMI converts at the ECCB-pegged rate on receipt and credits to the XCD balance.

Why was my Caribbean IBC rejected by a UK EMI — and what should I do?

Caribbean IBC applications at UK EMIs are most commonly rejected for four reasons: an expired certificate of good standing, incomplete UBO disclosure (particularly where nominee directors are involved), a missing source of funds explanation, or an absent business activity description. To address a rejection: obtain a fresh certificate of good standing from the registered agent, prepare a full UBO declaration letter for each beneficial owner above the 25% threshold, document the nominee director relationship clearly if one exists, and add a one-page business activity description covering the IBC's revenue model and expected transaction volumes. A strengthened application submitted to the same or a different FCA-authorised EMI has a materially higher approval rate than the original submission.

For a Caribbean offshore company holding East Caribbean dollars, the UK FCA-regulated EMI route delivers the payment infrastructure that local Caribbean banks routinely decline to provide: a multi-currency wallet with SWIFT connectivity, IBAN issuance, and access to international payment rails. The XCD account Caribbean offshore company UK EMI combination works best for IBCs that operate internationally, have identifiable beneficial owners, and can present a clear picture of their business activity and expected transaction volumes. EQWIRE accepts Nevis and Antigua IBC applications and provides dedicated onboarding support for offshore structures. Finance teams ready to begin can start the application here.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)