•

•

AML Compliance for Offshore Companies Opening UK Accounts

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Offshore companies applying for UK business accounts face a compliance process that goes beyond standard identity checks. AML compliance for offshore companies seeking a UK business account is more extensive than it is for UK-incorporated entities — and understanding what that process involves helps applicants prepare correctly and avoid unnecessary delays.

The reason is regulatory, not arbitrary. Under the UK's Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017 (MLR 2017), financial institutions including FCA-authorised electronic money institutions must apply Enhanced Due Diligence (EDD) to any customer assessed as higher risk. Offshore-registered companies consistently meet that threshold. This article explains what the AML compliance process involves, which documents to prepare, which jurisdictions FCA-authorised EMIs accept, and how the onboarding timeline unfolds from application to account activation. The FCA sets out its expectations for payment firms through FCA's safeguarding requirements, which inform the compliance standards applied during offshore company onboarding.

[aa key-takeaways]

Key Takeaways

UK-regulated EMIs are legally required to apply Enhanced Due Diligence (EDD) to offshore company applications under MLR 2017 Regulation 33 — this is not a discretionary policy.

EDD requires four document categories: company formation records, UBO identification at the 25% ownership threshold, source of funds evidence, and a business activity profile.

Offshore jurisdictions such as BVI, Cayman Islands, Seychelles, and UAE/RAK are accepted by FCA-authorised EMIs — rejection typically comes from incomplete documentation, not from the jurisdiction itself.

The compliance review for offshore companies takes 5–15 business days at a UK EMI; incomplete UBO documentation is the most common source of delays.

An FCA-authorised EMI can open a UK GBP business account for an offshore company without requiring a UK physical office or a UK-resident director.

[aa btn]Book a Call[/aa]

[/aa]

Why Opening a UK Account as an Offshore Company Involves Extra Compliance Checks

UK financial regulation treats offshore-registered companies as higher-risk customers by default. That classification is built into the Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017 (MLR 2017), specifically Regulation 33, which makes Enhanced Due Diligence mandatory for any business relationship where the customer is established in a high-risk third country or where the relationship is assessed as presenting a higher risk of money laundering or terrorist financing.

Jurisdictions such as the British Virgin Islands, Cayman Islands, Seychelles, and Marshall Islands are not on the FATF Call for Action list — a designation reserved for countries like North Korea and Iran. They do, however, carry structural features — nominee shareholder arrangements, limited public beneficial ownership registers, and multi-layer corporate structures — that UK-regulated firms assess as higher risk under their internal risk-based approaches. That assessment triggers EDD as a standard procedure rather than an exceptional one.

The regulatory pressure on payment firms is real and measurable. The FCA's enforcement record reflects rising expectations: in 2024, Starling Bank was fined £28.9 million for opening over 54,000 accounts for high-risk customers without adequate AML monitoring. Cases like this explain why FCA-authorised EMIs apply thorough EDD procedures to offshore company onboarding — the regulatory and financial consequences of shortfalls are direct.

The UK's Economic Crime (Transparency and Enforcement) Act 2022, which introduced mandatory registration requirements for overseas entities holding UK property, reflects a broader legislative trend toward offshore ownership transparency — one that extends into the financial services sector and increases the due diligence expectations placed on UK-regulated payment firms.

For offshore company applicants, the practical implication is clear: more documentation, a deeper review of ownership and funds, and a longer onboarding timeline than for UK-incorporated businesses. None of this makes approval impossible — it makes preparation more important.

[aa fast-fact]

Fast Fact: In 2024, the FCA fined Starling Bank £28.9 million for opening over 54,000 accounts for high-risk customers without adequate AML screening — one of the largest payment firm fines in FCA enforcement history.

[/aa]

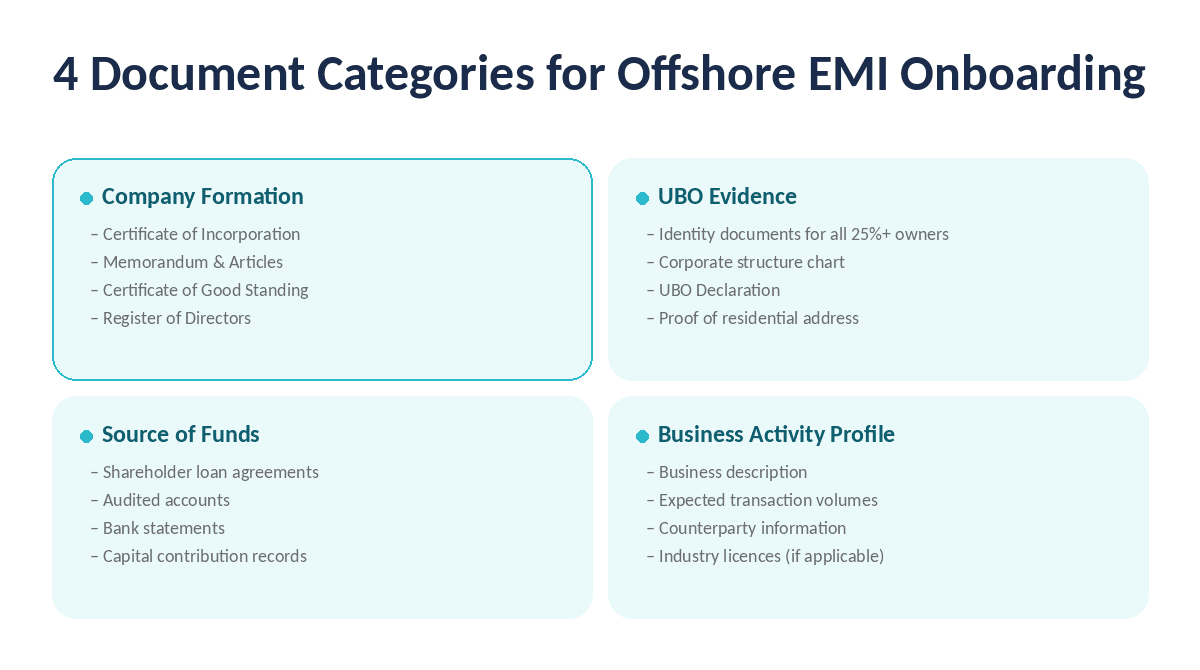

AML and KYC Documents UK EMIs Request from Offshore Companies

FCA-authorised EMIs apply a four-category document framework when onboarding offshore companies. The exact list varies by provider and by the specific risk profile of the applicant, but the categories below cover what most UK EMIs request as standard under an EDD review.

Company Formation and Registration Documents

The starting point for any offshore company onboarding is verification of the legal entity itself. EMIs require a Certificate of Incorporation issued by the registering authority in the offshore jurisdiction, along with the company's Memorandum and Articles of Association. A Certificate of Good Standing — typically no more than three to six months old at the time of submission — confirms that the company is in active status and compliant with filing obligations in its home jurisdiction.

A Register of Directors must also be provided, identifying all current directors by full legal name and nationality. In jurisdictions where nominee directors are commonplace, the EMI may request a Declaration of Nominee to confirm whether the named directors are acting on behalf of the beneficial principals. All documents must be either originals or certified copies, and any non-English materials require certified translation.

Beneficial Ownership and UBO Evidence

Identifying the Ultimate Beneficial Owner (UBO) is the core of any EDD review. Under UK AML standards, any individual who owns or controls more than 25% of the shares or voting rights in the company — directly or indirectly — qualifies as a UBO and must be identified and verified.

In multi-layer structures where an offshore company is held by one or more intermediate holding companies, the EMI traces ownership through each layer until it reaches the natural persons at the top. A corporate structure chart illustrating the full ownership hierarchy accelerates this process considerably. Each identified UBO must provide certified proof of identity (passport or national ID) and proof of residential address (utility bill or bank statement dated within three months).

Where ownership is complex or nominee arrangements exist, the EMI may request a UBO Declaration — a signed statement by the directors or legal counsel confirming the identities of the true beneficial owners. Any UBO who qualifies as a Politically Exposed Person (PEP) triggers additional scrutiny and requires enhanced source of wealth documentation.

Source of Funds Documentation

Source of funds verification answers a specific question: where did the money that capitalises this business actually come from? UK AML standards distinguish between source of funds (the origin of the money in the company's accounts) and source of wealth (how the beneficial owners accumulated their personal wealth). Both may be requested during EDD.

Common documentation includes shareholder loan agreements, investment agreements, or board resolutions authorising capital contributions. For trading companies, recent audited accounts or management accounts alongside bank statements showing business revenue provide the clearest evidence trail. Where funds originate from the sale of assets, share disposals, or inheritance, documentation demonstrating the original transaction is typically required.

The key principle is traceability: the EMI needs to follow the money from its point of origin through to the company's account in a documented, verifiable chain. Incomplete or undocumented fund flows are the most common reason EDD reviews stall.

Business Activity and Transaction Profile

Beyond the corporate and ownership layer, EMIs assess whether the company's planned activity is consistent with what is disclosed and whether the expected transaction volumes match the business profile. This section of the onboarding requires a written description of the company's business activities — what it sells or provides, to whom, and in which markets.

A projected transaction profile covers expected monthly volumes, average transaction sizes, currencies used, and the geographic reach of counterparties. Companies operating in sectors the EMI identifies as higher-risk — financial services brokerage, iGaming, digital assets, or high-value goods — may be asked to provide sample contracts, client lists (anonymised where commercially sensitive), or evidence of regulatory authorisation in their own operating jurisdiction. Offshore companies that also operate PSP settlement accounts through platforms such as Stripe or Adyen will typically be required to provide evidence of those payment processing relationships as part of their transaction profile.

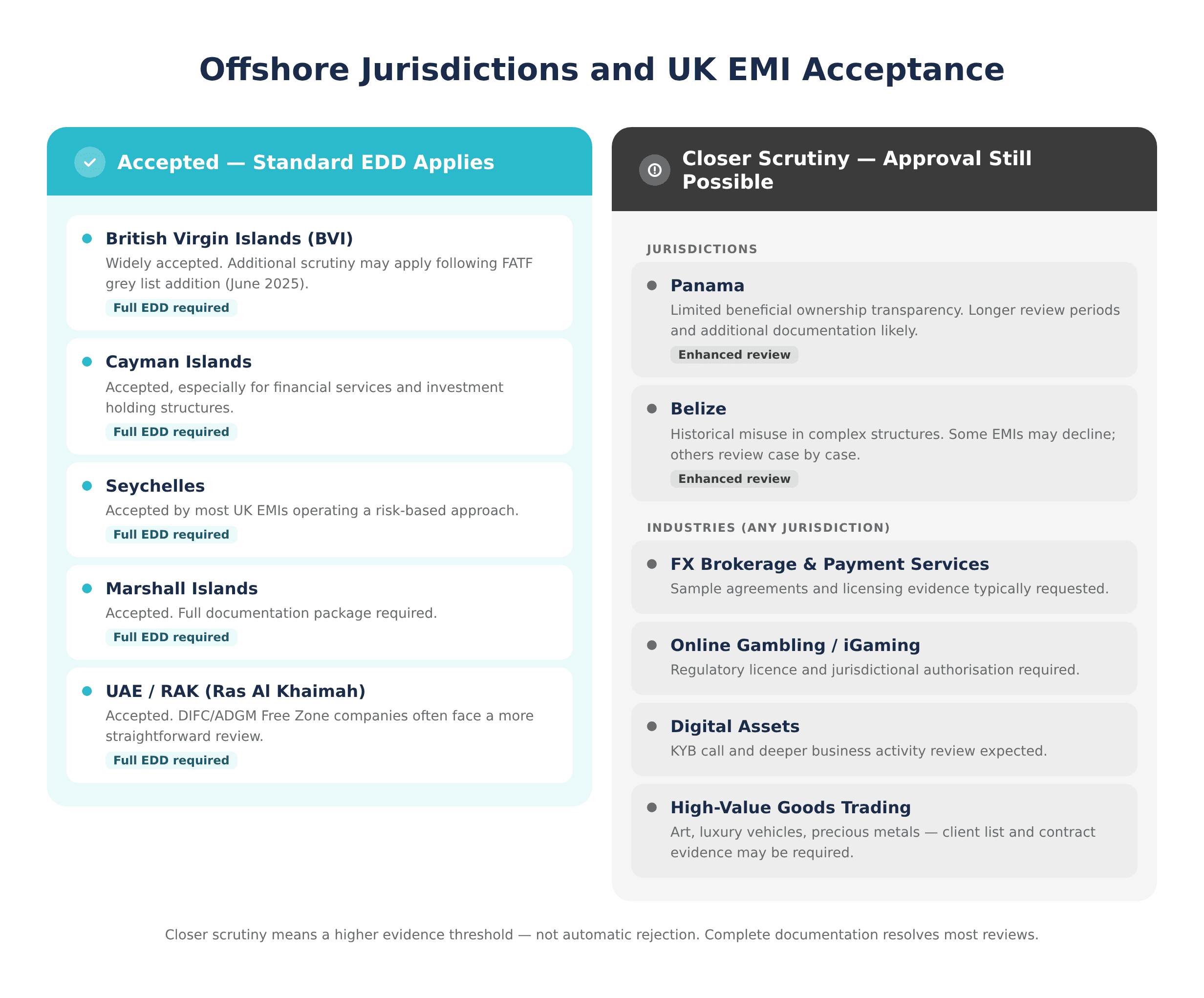

Which Offshore Jurisdictions Are Accepted by UK EMIs

Offshore incorporation does not disqualify a company from opening a UK business account at an FCA-authorised EMI. Most FCA-authorised EMIs operate a risk-based approach that distinguishes between jurisdictions that require enhanced scrutiny and those subject to FATF's formal Call for Action designations. The application process is more rigorous for offshore companies, but approval is achievable for most offshore structures operating legitimate business activities.

Jurisdictions Typically Accepted

The following offshore jurisdictions appear regularly in successful UK EMI onboarding applications. All trigger EDD as standard, but none are subject to the blanket prohibitions that apply to FATF Call for Action countries.

British Virgin Islands (BVI) is one of the most commonly accepted offshore jurisdictions for UK business accounts. BVI companies benefit from established registration infrastructure, standardised incorporation documents, and wide recognition among UK compliance teams. Following BVI's addition to the FATF grey list in June 2025, some EMIs may apply additional scrutiny — applicants should confirm current acceptance policies directly with their chosen provider and ensure beneficial ownership documentation is particularly thorough.

Cayman Islands companies are widely accepted, particularly in financial services and investment holding structures. The Cayman Islands maintains a Beneficial Ownership Register accessible to competent authorities, which supports UBO verification at FCA-regulated institutions.

Seychelles, Marshall Islands, and UAE/RAK (Ras Al Khaimah) are accepted by most UK EMIs operating a risk-based approach, though they consistently require full EDD documentation. UAE Free Zone companies — particularly those registered in DIFC or ADGM — often face a more straightforward review given the UAE's well-regarded AML infrastructure and its position on the FATF white list.

Panama and Belize structures face closer scrutiny from some UK EMIs due to limited beneficial ownership transparency and historical misuse in complex financial structures. Approval remains possible but may require additional documentation and longer review periods.

Industries That Face Additional Scrutiny

Certain industries attract deeper review regardless of jurisdiction. Companies in FX brokerage, payment services, online gambling, digital asset operations, and high-value goods trading — including art, luxury vehicles, and precious metals — can expect a longer review and additional document requests.

Additional scrutiny does not mean automatic rejection. It means the EMI's compliance team will apply a higher threshold of evidence to the business activity profile, may request sample agreements or licensing documentation, and may schedule a Know Your Business (KYB) call with the account applicant before making a decision. Companies in these sectors benefit from preparing more complete documentation upfront rather than responding reactively to individual requests.

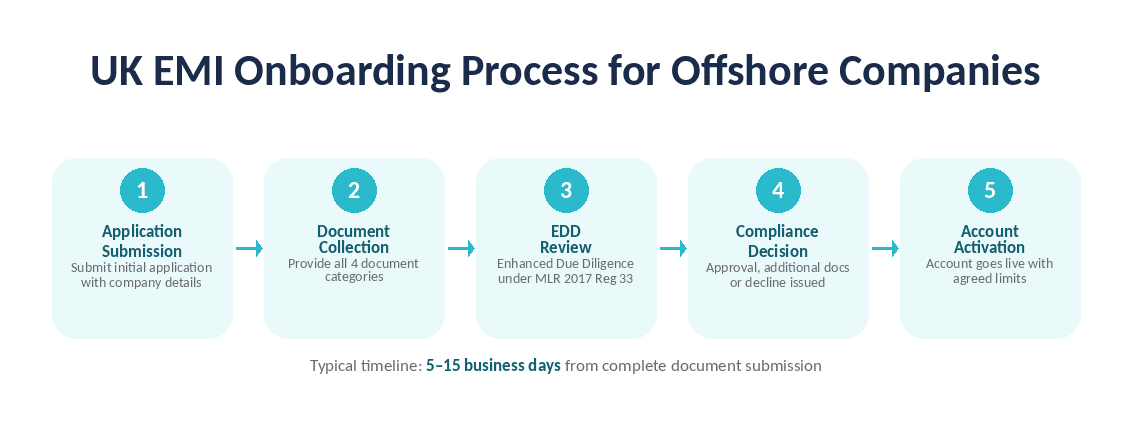

How the UK EMI Onboarding Process Works — From Application to Approval

The onboarding process at a UK FCA-authorised EMI follows a structured sequence. Understanding each stage helps applicants set accurate expectations and prepare their documentation effectively.

Stage 1 — Application submission. The applicant completes the EMI's online onboarding form, providing basic company information: registered name, jurisdiction, company number, and intended account use. At this stage, most EMIs also request a brief business description and estimated monthly transaction volumes.

Stage 2 — Initial document collection. The compliance team reviews the submitted information and issues a document request covering the four categories described above. For offshore companies, this request defaults to the EDD framework from the outset. Documents must be submitted in the required format — originals, certified copies, or notarised copies depending on the document type.

Stage 3 — EDD review. The compliance team conducts a structured review of all submitted materials. This includes verification of each document against source databases (company registers, sanctions lists, PEP databases), UBO identity verification, and assessment of the source of funds narrative. Complex ownership structures or incomplete submissions typically generate follow-up requests at this stage.

Stage 4 — Compliance decision. Following the review, the compliance team reaches an approval decision. Approved applications move to account activation. Applications with outstanding questions may enter a secondary review cycle, during which the applicant provides additional evidence. Declined applications are notified with the reason where the EMI's policy permits.

Stage 5 — Account activation. Once approved, the account is activated and the company receives its account details, including a UK sort code and account number and, where applicable, a named IBAN. The company can begin transacting immediately, subject to the transaction limits and conditions set during onboarding.

[aa cta]

Open a UK Business Account for Your Offshore Company

EQWIRE is an FCA-authorised EMI that processes offshore company applications through a structured EDD framework. GBP sort codes, multi-currency IBANs, and SWIFT and SEPA payments are available to approved applicants.

[aa btn]Create Account[/aa]

[/aa]

How Long the Compliance Review Takes and What Causes Delays

For offshore companies going through a standard EDD review, the compliance process at a UK EMI typically takes 5 to 15 business days from the point at which a complete document set has been received. That qualifier — complete document set — is material. Most delays trace back to documentation gaps rather than processing backlogs.

The most common causes of extended review times are incomplete UBO documentation (particularly where multi-layer structures involve intermediate holding companies in additional offshore jurisdictions), missing or expired source of funds evidence, and business descriptions that are vague or inconsistent with the transaction profile submitted.

Applications that include a clear corporate structure chart, certified UBO declarations for all individuals above the 25% threshold, and a traceable source of funds narrative tend to clear EDD in the lower half of that range. Applicants who wait to respond to individual document requests rather than submitting a complete package upfront typically experience timelines at the higher end.

Timing matters for businesses with active payment obligations. Starting the onboarding process before an account is urgently needed gives the compliance review room to run without pressure — and allows time to respond to follow-up requests without disrupting ongoing operations.

[aa fast-fact]

Fast Fact: Under MLR 2017 Regulation 33, Enhanced Due Diligence is a legal obligation — not a discretionary policy — for UK-regulated firms onboarding customers from high-risk third countries or relationships assessed as higher risk.

[/aa]

How EQWIRE Handles AML Compliance for Offshore Clients

EQWIRE is an FCA-authorised EMI — regulated under the Electronic Money Regulations 2011 and subject to the full scope of UK AML obligations, including the Regulation 33 EDD requirements described throughout this article. EQWIRE is listed on the FCA Register as an authorised electronic money institution, meeting the FCA financial crime guidance applied to payment firms operating in the UK. Offshore company onboarding at EQWIRE follows the four-category document framework, reviewed by an in-house compliance team.

EQWIRE accepts offshore companies from BVI, Cayman Islands, Seychelles, Marshall Islands, and UAE/RAK, subject to the standard EDD review. A UK physical office is not required. A UK-resident director is not required. The onboarding process is document-driven: the compliance team reviews the submitted materials and communicates directly with the applicant when additional evidence is needed.

Approved accounts include a UK sort code, a named IBAN account in GBP, EUR, or USD, and access to SWIFT and SEPA payment rails. As detailed in the guide to UK bank details for BVI companies, offshore companies with an EQWIRE account can receive GBP payments from UK clients and issue UK-format payment instructions without maintaining a UK presence.

The compliance process is consistent for all offshore applicants — based on documented criteria rather than opaque internal policies. Companies that have previously received rejections from high-street banks often find that EMI onboarding, while rigorous, is clearer in what it requires and why. The comparison between FCA-authorised EMIs and UK banks covers the structural differences in more detail.

[aa cta]

Ready to Apply? Start Your Account Application

EQWIRE reviews offshore company applications through a structured EDD process. Prepare company formation documents, UBO evidence, and source of funds materials before starting.

[aa btn]Create Account[/aa]

[/aa]

The regulatory framework for offshore company onboarding at UK EMIs is strict, documented, and consistent. AML compliance for offshore companies opening UK business accounts follows a defined process — four document categories, structured EDD review, and a compliance decision based on verifiable evidence. Companies that understand this process and prepare accordingly, with complete corporate documentation, clear UBO disclosure, and traceable source of funds, typically receive a faster and clearer outcome than those who approach the process without prior preparation.

For offshore companies operating in international markets, access to a UK GBP account with sort code and IBAN reduces payment friction with UK counterparties considerably. EQWIRE provides that access through an FCA-regulated framework designed for exactly this type of international business structure. Start an application at client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)