•

•

CNY to GBP or EUR: How to Convert Chinese Yuan Without Losing on FX

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A UK exporter invoices a Chinese buyer for ¥350,000. Three days later, £38,500 lands in the business account — roughly £1,200 less than the mid-market rate would have delivered. Nothing went wrong technically. The gap simply disappeared into a retail FX margin and a correspondent bank fee that never appeared on any invoice.

This is what CNY to GBP EUR conversion business UK operations run into every month: the process works, but the pricing is opaque. This guide sets out a repeatable workflow — from account setup to reconciliation — for converting Chinese yuan into GBP or EUR without giving away margin at each step. The short answer: competitive conversion depends on the type of account receiving the CNY, the timing of the conversion relative to CNH market hours, and avoiding a handful of well-known markup traps.

[aa key-takeaways]

Key Takeaways

Onshore CNY and offshore CNH price differently against GBP and EUR — the gap can run 1-2% depending on market conditions

An FCA-regulated EMI can offer tighter FX spreads than a high-street bank for receiving and converting CNY

Converting during London trading hours, when CNH liquidity is deepest, typically produces a better rate than converting overnight

"Fee-free" transfers usually recover their cost through a wider exchange rate margin, not through an added line-item fee

A monthly reconciliation routine catches rate drift and mistimed conversions before they compound

[aa btn]Compare EQWIRE FX Rates[/aa]

[/aa]

Before You Convert: A Pre-Flight Checklist

Most of the cost in CNY currency exchange for UK business transactions is decided before the money ever moves — by which account receives it and how it is documented. Getting this stage right removes the two most common causes of delay: rejected payments and manual compliance reviews.

Documents and Account Setup You Need First

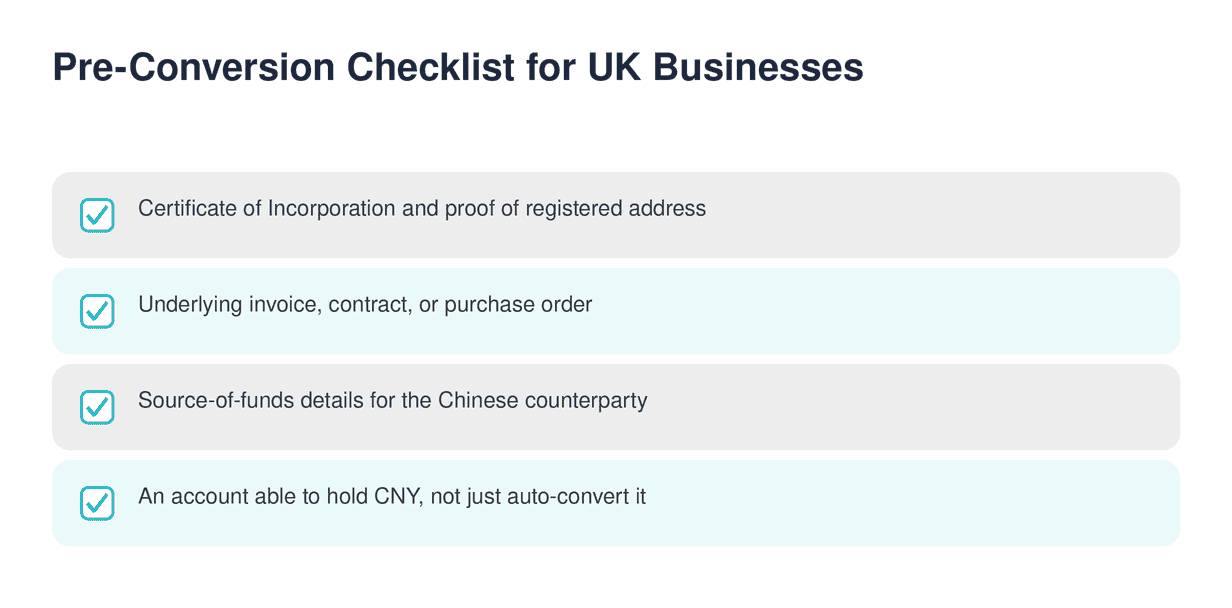

A UK business set up to receive CNY payments will typically find that banks or EMIs ask for the following before the first transfer:

Certificate of Incorporation and proof of registered address

Details of the underlying trade — invoice, contract, or purchase order

Source-of-funds information for the Chinese counterparty

A business account already capable of holding CNY or converting it on arrival

Approval timelines vary by provider. A high-street bank can take one to two weeks to add CNY receiving capability to an existing account, while an EMI built for multi-currency receivables typically confirms this within a few business days of onboarding.

What this means in practice: if the receiving account cannot hold CNY natively, the payment is auto-converted on arrival at whatever rate the provider sets that day — with no opportunity to time the conversion.

Setting Up an Account That Can Receive and Convert CNY

To convert Chinese yuan GBP EUR EMI account setups need one capability traditional current accounts often lack: the ability to hold a CNY balance rather than force an immediate conversion. That single feature determines whether a business can choose its conversion timing at all.

Choosing an EMI vs a Traditional Bank

Electronic Money Institutions authorised by the FCA operate under the same safeguarding obligations that protect client funds at banks, but with FX desks built specifically for cross-border receivables. Traditional banks route CNY through correspondent networks, adding intermediary fees that are rarely itemised.

Provider type | Typical FX margin | Settlement speed | Fund protection |

|---|---|---|---|

High-street bank | 2.5%–4% | 2–3 business days | FSCS-style deposit rules vary |

FCA-regulated EMI | 0.3%–1.5% | Same day to 1 business day | Safeguarded client funds |

[aa fast-fact]

Fast Fact: A 3% FX margin on a £50,000-equivalent CNY payment costs roughly £1,500 — enough to cover a month of SaaS tooling or a freight invoice.

[/aa]

What Chinese Clients Will Ask For Before Paying You

Chinese counterparties, particularly larger buyers, often require a formal invoice denominated in CNY, a SWIFT-capable account number, and confirmation that the receiving entity matches the contracted party. Missing any of these triggers a manual review at the paying bank, which adds days before the funds even reach the UK.

[aa cta]

Receive and Convert CNY in One EMI Account

Hold, receive, and convert Chinese yuan into GBP or EUR from a single FCA-regulated account.

[aa btn]Open an EQWIRE Account[/aa]

[/aa]

Conversion Workflow, Step by Step

Once CNY lands in an account that can hold it, the actual conversion becomes a matter of timing and execution rather than eligibility. This is where yuan to pound euro conversion rates diverge most from what a rate calculator shows on a generic currency site.

Timing Your Conversion Around CNH Market Hours

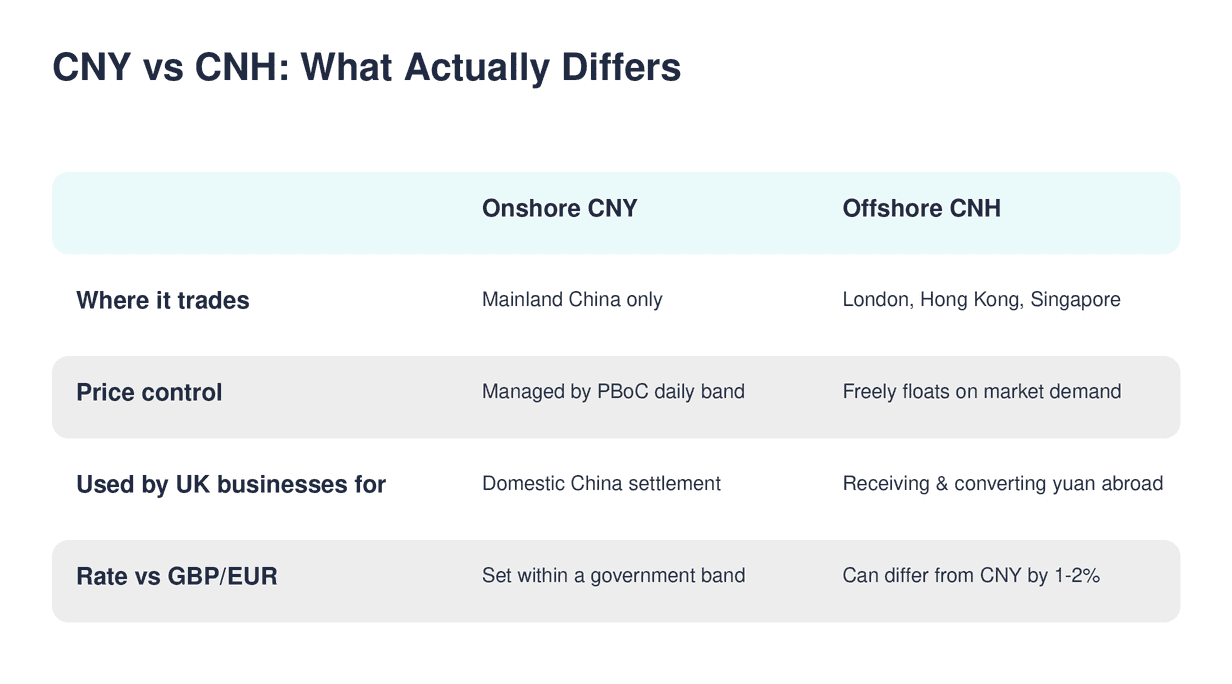

Most CNY held offshore trades as CNH — the freely traded, market-priced version of the currency, distinct from the government-managed onshore CNY. London is the largest offshore RMB trading centre outside Asia, with average daily CNH FX turnover in the hundreds of billions of pounds. Liquidity is deepest during UK trading hours, when both London and residual Asian trading overlap — spreads widen noticeably outside that window.

Here's where money is lost: converting a large CNY balance late on a Friday evening, when liquidity thins out, routinely produces a wider spread than the same trade executed on Tuesday at midday.

Batch vs Real-Time Conversion

Businesses receiving CNY from a single large buyer a few times a year benefit from converting each payment as it arrives, since holding CNY exposes the business to further rate movement. Businesses with frequent, smaller CNY receipts — recruitment payouts, marketplace settlements, recurring supplier rebates — often do better batching conversions weekly rather than paying a spread on every individual transaction.

A UK trading company receiving ten CNY payments a month from different suppliers' rebate schemes converted each one individually and paid the spread ten times over. Switching to a single weekly batch conversion cut the number of spread charges from ten to four per month, without changing the total CNY volume converted.

Common Mistakes That Cost UK Businesses Money

For a UK exporter paid in yuan, the difference between a competitive conversion and an expensive one usually comes down to three repeatable mistakes rather than bad luck with market timing.

Hidden Markups in "Fee-Free" Transfers

A transfer advertised as having no fee almost always recovers that cost through the exchange rate itself — the provider buys CNY at the wholesale rate and sells it to the business at a markup, with no separate charge to disclose. The practical fix: compare the rate actually applied against a live mid-market CNY to GBP quote before accepting a "no-fee" conversion.

Ignoring the Onshore/Offshore Rate Gap

CNY and CNH trade at a 1:1 rate against each other but price differently against GBP and EUR, because CNY remains government-managed while CNH floats freely offshore. A business assuming both quote identically against sterling can misjudge the true cost of a conversion by 1-2%, particularly during periods of currency volatility.

On a £100,000-equivalent payment, a 1.5% pricing gap between CNY and CNH quotes works out to roughly £1,500 — enough to justify asking a provider explicitly which rate feeds their pricing.

What this means: always confirm whether a quoted rate references onshore CNY or offshore CNH — the two are not interchangeable for pricing purposes.

A Monthly Reconciliation Routine for CNY Receivables

Businesses that convert CNY to GBP rates competitively tend to run the same short reconciliation process every month rather than reviewing FX costs only when a transfer looks unusually expensive.

Log the mid-market rate at the time each CNY payment was received, alongside the rate actually applied

Calculate the effective margin paid on each conversion and flag anything above 1.5%

Compare monthly totals against a comparable receivable, such as receiving HKD payments as a UK-based exporter to Asia, to spot whether CNY specifically is priced worse than other currencies on the same account

Review whether batching or same-day conversion produced the better outcome that month

How to convert CNY to GBP or EUR at competitive rates for UK exporter paid in yuan ultimately comes down to repeating this cycle: receive into an account that can hold CNY, time the conversion around CNH market hours, and check the applied margin against a public benchmark every time. Businesses that treat this as a monthly discipline — rather than a one-off setup — consistently keep more of what they invoice, similar to how FX-neutral settlement removes forced conversion from multi-currency PSP payouts.

For a more detailed look at receiving the payments themselves before conversion, see how UK businesses receive CNY payments from Chinese clients. London's position as a leading offshore RMB hub and the yuan's growing share of global payments tracked by SWIFT both mean CNY-denominated trade with the UK is only getting more common — making a disciplined conversion process a recurring line-item worth optimising, not a one-time task.

[aa cta]

Stop Losing Margin on Every CNY Conversion

Compare EQWIRE's FX rates before your next yuan payment lands.

[aa btn]Get Started[/aa]

[/aa]

FAQ

What gets a UK exporter paid in yuan the most competitive conversion rate?

Receive the payment into an account that can hold CNY rather than force an automatic conversion, convert during UK trading hours when CNH liquidity is deepest, and check the applied rate against a live mid-market benchmark quote before accepting it.

What is the difference between CNY and CNH?

CNY is the onshore, government-managed Chinese yuan used within mainland China, while CNH is the offshore version traded freely in markets including London, Hong Kong, and Singapore. They trade 1:1 against each other but can price differently against GBP or EUR.

Can a UK business hold CNY balances in an EMI account?

Many FCA-regulated EMIs support holding CNY balances alongside GBP and EUR, which allows a business to choose when to convert rather than accepting an automatic rate on arrival. Availability varies by provider, so this should be confirmed before onboarding.

What documents does a UK business need to receive CNY payments?

Typical requirements include a Certificate of Incorporation, proof of registered address, the underlying invoice or contract, and source-of-funds details for the paying Chinese counterparty. Missing documentation is one of the most common causes of delayed CNY transfers.

Is it better to convert CNY to GBP rates immediately or hold the balance?

Businesses receiving CNY infrequently and in large amounts generally benefit from converting as soon as funds arrive, since holding exposes them to further rate movement. Businesses with frequent, smaller CNY receipts often reduce costs by batching conversions weekly instead of converting each payment individually.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)