•

•

Safeguarding of Client Funds in a UK EMI Account: What Businesses Need to Know

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

UK electronic money institutions held billions of pounds in customer balances during 2025, yet the money sitting in an EMI account follows a different rulebook from the one that covers a high-street bank deposit. Safeguarding of client funds in a UK EMI account is the legal mechanism that keeps customer money ring-fenced from the institution's own finances, so balances can be returned if the firm fails. It is not the Financial Services Compensation Scheme (FSCS), and that distinction shapes how protected company cash really is. This guide compares EMI safeguarding with FSCS bank cover and explains what happens to client funds if a provider becomes insolvent. It also sets out the new FCA safeguarding rules that take effect on 7 May 2026, and shows how a business can confirm its provider safeguards correctly before moving any money.

[aa key-takeaways]

Key Takeaways

Safeguarding ring-fences client funds from an EMI's own money, so balances are returned to customers if the institution fails.

EMI balances are not covered by FSCS when the institution itself fails; protection comes from safeguarding under the Electronic Money Regulations 2011.

UK EMIs safeguard money in one of two ways: segregation in a designated safeguarding account, or an insurance policy or comparable guarantee.

FSCS caps bank deposit compensation at £120,000 per eligible person, while safeguarding has no cap but offers no instant payout scheme.

From 7 May 2026, the FCA's PS25/12 rules add daily reconciliations, monthly reporting, annual audits, and resolution packs.

Businesses can verify protection through the FCA Register, the firm reference number, and the provider's stated safeguarding method.

[aa btn]Book a Call[/aa]

[/aa]

Safeguarding of Client Funds in a UK EMI Account: What Businesses Are Really Comparing

Safeguarding is the regulatory mechanism that protects customer money held by a UK electronic money institution. Under the Electronic Money Regulations 2011, an EMI must keep client funds separate from its own working capital and hold them so they can be returned if the firm collapses. The comparison most businesses are actually making is not "is an EMI risky?" but "how does this protection differ from a bank?"

What an EMI Account Is and How It Differs From a Bank Account

An electronic money institution issues e-money and runs payment accounts, but it does not lend customer deposits the way a bank does. A bank takes deposits onto its own balance sheet and lends them out. An EMI cannot. It must hold the equivalent of every customer balance in safeguarded form at all times.

That structural difference explains the different protection regime. EQWIRE has set out the deeper differences between an FCA-authorised EMI and a bank in a separate guide. The short version: a bank balance is a claim against the bank, while an EMI balance is customer money the firm is holding on trust.

Here is why the distinction matters in practice. A bank can put deposits to work, so a depositor becomes one creditor among many if the lender collapses. An EMI never owns the money it holds. Customer balances stay reserved for customers at all times, which is the foundation of every protection that follows.

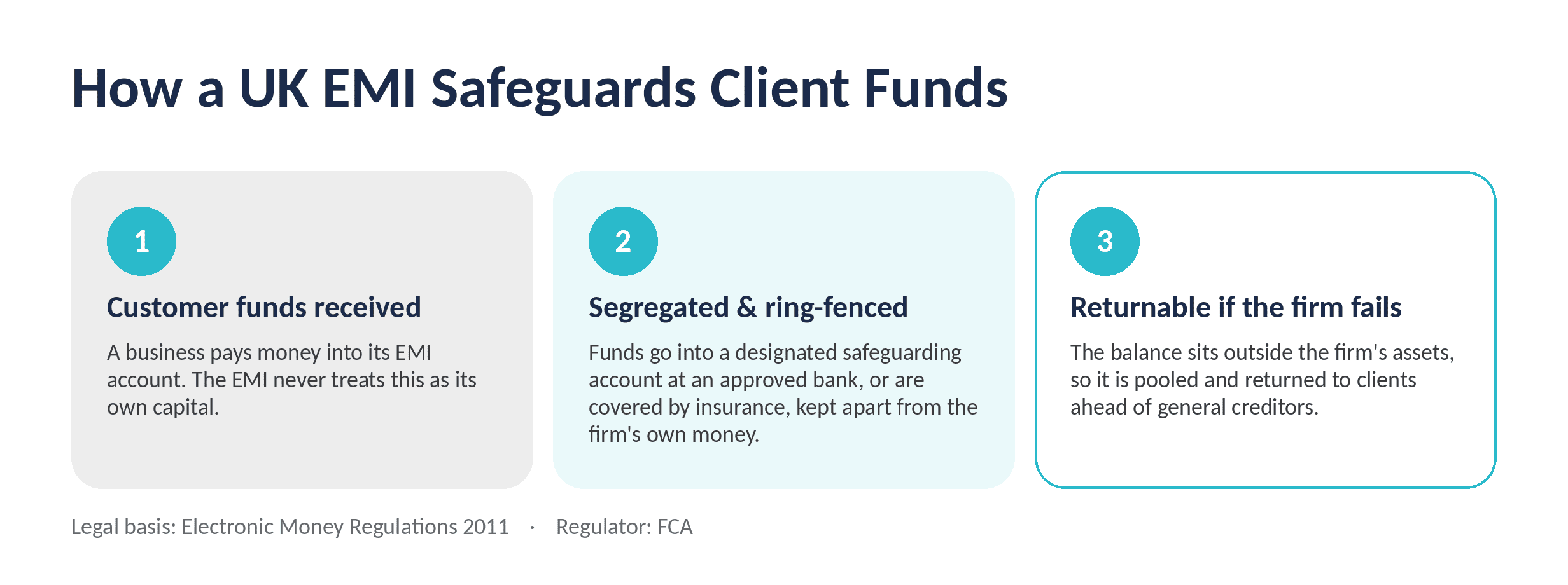

How Safeguarding Protects Business Funds

UK EMIs safeguard electronic money institution client funds using one of two methods set by the FCA:

Segregation: relevant funds are placed in a designated safeguarding account at an authorised credit institution, kept apart from the EMI's own money.

Insurance or comparable guarantee: an authorised insurer covers the relevant funds, paying out if the firm cannot return them.

Most EMIs use segregation. The ring-fenced funds do not belong to the institution, so they sit outside the pool available to general creditors in an insolvency.

In practice, the safeguarding account sits at an approved credit institution, and the EMI must reconcile its own records against that account on a regular basis. The aim is straightforward: at any given moment, the ring-fenced balance should match what customers are collectively owed. A firm that lets those records drift is the kind of provider regulators worry about, which is exactly what the 2026 reforms set out to fix.

Safeguarding vs FSCS: A Side-by-Side Comparison

The key difference between safeguarding and FSCS is the form of protection. FSCS is a compensation scheme that pays eligible bank depositors up to a fixed limit. Safeguarding is not a compensation scheme at all. It ring-fences the actual client money so it can be returned, with no upper cap on the amount protected.

Feature | EMI safeguarding | Bank FSCS protection |

|---|---|---|

Protection mechanism | Client funds ring-fenced (segregation or insurance) | Statutory compensation scheme |

Coverage limit | No cap — full client balance is ring-fenced | £120,000 per eligible person, per institution |

What happens on failure | Safeguarded funds pooled and returned to clients | FSCS compensates up to the cap |

Speed of return | Via an insolvency practitioner; can take weeks or months | Typically within days for covered deposits |

Legal basis | Electronic Money Regulations 2011 | FSCS deposit protection rules |

Coverage Limits: Full Ring-Fencing vs the £120,000 Cap

FSCS protects eligible deposits up to £120,000 per person, per banking licence, a limit that rose from £85,000 on 1 December 2025. A company holding £500,000 at a single bank sees only £120,000 of it compensated if that bank fails. Safeguarding works differently. Because the full client balance is ring-fenced, there is no £120,000 ceiling on the amount that can be returned from an EMI. For a business that routinely parks six- or seven-figure sums between supplier runs, that absence of a cap is the single most important difference between the two regimes.

What Happens if the Provider Fails

If a bank fails, FSCS steps in and compensates covered depositors. If an EMI fails, the safeguarded funds are pooled and distributed to clients ahead of general creditors. The FCA's consumer guidance is candid about the trade-off: customers should get most of their money back, but it may take time and the administrator can deduct the costs of the distribution.

What that looks like in practice is a recovery rather than a guaranteed payout. The insolvency practitioner verifies each client claim against the safeguarding records, settles the costs of running the administration, then returns the remaining pooled balance. A clean reconciliation history shortens that timeline. Poor records lengthen it, which is one reason the quality of a provider's safeguarding operation, not just its licence, decides how a failure plays out.

[aa fast-fact]

Fast Fact: When the EMI Supercapital entered administration, the administrator deducted around 10.48% of client e-money balances to cover administration costs, and customers waited several months to receive the remaining 89.52%.

[/aa]

Speed of Fund Recovery

Speed is where FSCS holds an advantage. Compensation for covered bank deposits is usually paid within days. EMI safeguarded funds run through an insolvency practitioner, so distribution can take weeks or months while the administrator confirms balances and the costs of the process.

One nuance matters here. FSCS never compensates an EMI's own collapse. It does, however, cover the failure of the bank holding the EMI's safeguarded funds, up to £120,000 per customer. So a business holding money with an EMI carries two distinct, low-probability risks: the EMI failing, and the safeguarding bank failing. The first is handled by segregation, the second by FSCS.

[aa cta]

Hold Business Funds With an FCA-Authorised EMI

EQWIRE is a UK electronic money institution authorised by the Financial Conduct Authority, and it safeguards client funds in segregated accounts in line with the Electronic Money Regulations 2011.

[aa btn]Create Account[/aa]

[/aa]

When an EMI Account Is the Right, Safe Choice for a Business

For many companies, a UK EMI account is as safe as a bank for business funds in practical terms, because the full balance is ring-fenced rather than capped at £120,000. The right answer depends on the balance held and the currencies in play. How the provider operates matters just as much, far more than a simple bank-versus-EMI hierarchy.

Use Cases Where EMI Safeguarding Fits

EMI accounts suit businesses that move money internationally or hold balances above the FSCS cap. Typical scenarios include multi-currency operations and frequent cross-border supplier payments. Fast digital onboarding adds to the appeal for companies that cannot wait weeks for a traditional bank to open an account. EQWIRE has compared dedicated EMI accounts for international SMEs against popular alternatives, and reviewed the choice when comparing popular EMI providers for offshore companies.

For a trading company holding £400,000 across three currencies, full ring-fencing protects the entire balance. The same sum at one bank would leave most of it outside FSCS cover. An e-commerce business collecting receipts in euros and dollars sees a similar benefit, since the money stays reserved in each currency rather than sitting partly unprotected above the deposit cap.

When a Bank Account May Still Suit a Business Better

A traditional bank account fits companies that need credit facilities, overdrafts, or physical cash handling. Smaller balances that sit comfortably under the £120,000 FSCS limit also gain little extra protection from ring-fencing, and the speed of FSCS compensation can outweigh the higher cap that safeguarding offers. Many businesses end up using both: a bank for lending and day-to-day domestic cash, an EMI for multi-currency balances and international flows. The honest position is that neither model is universally safer. Each serves a different purpose.

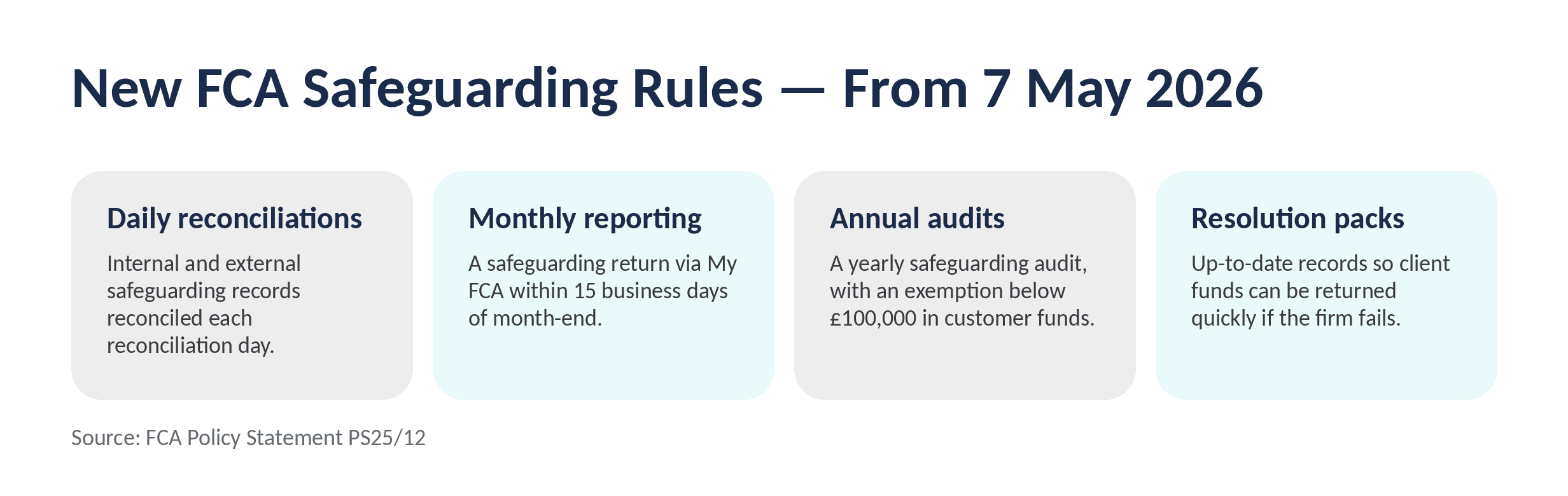

How the New FCA Safeguarding Rules Change the Comparison (From 7 May 2026)

From 7 May 2026, the FCA's PS25/12 safeguarding rules tighten how EMIs handle client money. The reforms respond to repeated safeguarding failures and narrow the practical gap between EMI protection and bank protection.

The main new obligations include:

Daily reconciliations: firms must reconcile internal and external safeguarding records at least once each reconciliation day.

Monthly reporting: authorised firms submit a safeguarding return through My FCA within 15 business days of each month-end.

Annual audits: firms commission a safeguarding audit, with an exemption for those holding less than £100,000 in customer funds.

Resolution packs: firms maintain regularly updated records so client funds can be returned quickly if the firm fails.

[Visuals - FCA 2026 Safeguarding Rules Timeline - Timeline of new FCA PS25/12 obligations effective 7 May 2026: daily reconciliation, monthly reporting, annual audit, and resolution pack]

What This Means for Businesses Choosing a Provider

These FCA safeguarding rules give companies more evidence to inspect. A provider that already reconciles daily and commissions audits is demonstrating operational discipline, not just a licence. Monthly returns mean the regulator now sees safeguarding positions in close to real time, which makes persistent shortfalls far harder to hide. The Payment Services Regulations 2017 apply the equivalent regime to payment institutions, so the same questions work across both firm types. The practical takeaway: stronger oversight makes a well-run EMI a more credible home for company cash than it was a year ago, and it gives finance teams a concrete checklist to hold providers against.

How to Choose a UK EMI to Trust With Company Funds

Understanding how UK EMIs protect client funds is only useful if a business can verify a specific provider. A short due-diligence check answers most of the question before any money moves.

Verify Authorisation and the Firm Reference Number

Every authorised firm appears on the FCA Register with a firm reference number. Checking that number confirms the provider is an Authorised Electronic Money Institution (AEMI), a Small EMI (SEMI), or an Authorised Payment Institution (API), rather than an unregulated app. EQWIRE, for example, operates under firm reference number 901100.

Confirm the Safeguarding Method and Provider Conduct

A trustworthy provider states how it safeguards funds and which method it uses. Businesses opening accounts as offshore or non-UK entities should also confirm the provider's onboarding standards, since the regulatory checks UK providers apply signal how seriously a firm treats compliance. A provider that cannot explain its safeguarding arrangement clearly is a warning sign.

Three quick questions tend to separate strong providers from weak ones. Where are client funds held, and at which credit institution? How often does the firm reconcile its safeguarding records? And can it evidence the audit and reporting it is now required to complete? A provider that answers all three without hesitation is treating client money the way the rules intend.

FAQ

Is a UK EMI account as safe as a bank account for business funds?

A UK EMI account is as safe as a bank account for business funds in practical terms, though the protection works differently. A bank deposit is covered by FSCS up to £120,000 per person, while an EMI ring-fences the full client balance through safeguarding under the Electronic Money Regulations 2011. For balances above the FSCS cap, ring-fencing can protect more money than a bank's compensation limit. The trade-off is speed: FSCS usually pays within days, whereas safeguarded funds are returned through an insolvency process that can take longer.

What is the difference between safeguarding and FSCS protection?

The difference between safeguarding and FSCS protection is the form each one takes. FSCS is a statutory compensation scheme that reimburses eligible bank depositors up to £120,000 if a bank fails. Safeguarding is not compensation. It requires an EMI to hold client funds separately from its own money, either in a segregated account or under an insurance policy, so the funds can be returned directly. Safeguarding has no upper limit on the protected amount, but it does not guarantee an instant payout.

How do UK EMIs protect client funds if the provider becomes insolvent?

UK EMIs protect client funds by ring-fencing them from the firm's own assets, so they sit outside the pool available to general creditors. If the provider becomes insolvent, an insolvency practitioner pools the safeguarded funds and distributes them to customers. According to FCA guidance, customers should receive most of their money back, although the administrator can deduct distribution costs and the process can take weeks or months. EMIs using the insurance method instead rely on a payout from an authorised insurer.

Is there a limit on how much is protected in a UK EMI account?

There is no fixed cap on the amount safeguarded in a UK EMI account, which differs from the £120,000 FSCS limit that applies to bank deposits. Because safeguarding ring-fences the actual client balance, the full sum is protected in principle. One related limit does apply: if the bank holding an EMI's safeguarded funds fails, FSCS cover for that bank is capped at £120,000 per customer.

How can a business check that its EMI safeguards client funds correctly?

A business can check safeguarding by confirming the provider on the FCA Register using its firm reference number, then asking how the firm safeguards funds and which method it uses. From 7 May 2026, FCA rules require authorised firms to reconcile daily, report monthly, and commission annual audits above the £100,000 threshold, so a provider can be asked to evidence these practices. A clear, documented answer signals a compliant provider, while vagueness about safeguarding arrangements is a red flag.

Choosing where to hold company funds comes down to matching protection to purpose. Safeguarding of client funds in a UK EMI account ring-fences the full balance under the Electronic Money Regulations 2011, while FSCS compensates bank deposits up to £120,000. The new FCA rules from May 2026 strengthen EMI oversight further, narrowing the difference between the two models. For businesses that move money across borders or hold balances above the FSCS cap, a well-regulated EMI offers protection that scales with the balance. EQWIRE operates as an FCA-authorised electronic money institution that safeguards client funds in segregated accounts, and companies can open a multi-currency business account at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)