•

•

FX-Neutral Settlement: How to Receive Multi-Currency PSP Payouts Without Forced Conversion

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A merchant sells across the UK, the EU, the US, the UAE and Hong Kong, yet every Stripe or Adyen payout lands in one currency: GBP, minus a spread that was never quoted as a fee. That spread is the cost of forced conversion, and at scale it quietly removes a slice of every non-sterling sale. FX-neutral settlement for multi-currency PSP payouts is the alternative: each payout arrives in the currency the sale was made in, so the business decides if and when to convert. This guide explains why payment service providers convert by default, the account structure that stops it, and how to configure Stripe, Adyen and PayPal to receive each settlement untouched.

[aa key-takeaways]

Key Takeaways

FX-neutral settlement means receiving each PSP payout in its original currency instead of having it auto-converted to a single base currency.

PSPs convert by default because most merchants register only one base-currency payout account, so the acquirer settles everything into it.

A multi-currency account with a per-currency IBAN and UK sort code lets you receive PSP payouts in multiple currencies without forced FX.

The hidden cost is an FX spread of roughly 0.5–1.5% above the mid-market rate on every non-base-currency transaction.

Stripe, Adyen and PayPal all support like-for-like settlement, but each needs a separate account registered per settlement currency.

[aa btn]Open a multi-currency account[/aa]

[/aa]

What FX-Neutral Settlement Actually Means

FX-neutral settlement is the practice of receiving each payment in the currency it was charged in, with no conversion applied between the sale and the payout. The acquirer holds the proceeds in the transaction currency and pays them to a receiving account that can hold that same currency. Nothing is converted unless the business chooses to convert it later.

This matters because the alternative, single-currency settlement, bakes a cost into money the business has not yet decided how to use. Receiving payouts in multiple currencies keeps that decision where it belongs: with the merchant's treasury, not the payment processor.

FX-Neutral vs Forced Conversion at Payout

The difference sits in one step. Under forced conversion, a EUR sale is changed into GBP before it reaches the account, at a rate the acquirer sets. Under FX-neutral settlement, the same EUR sale arrives as euros.

Forced conversion: EUR sale → acquirer converts to GBP → GBP lands in the account (spread already taken).

FX-neutral settlement: EUR sale → acquirer settles in EUR → EUR lands in a euro balance (no spread; convert later if needed).

What this means in practice: with like-for-like settlement, a business funding euro supplier invoices can pay them straight from the euro balance, avoiding two conversions on the same money.

The Settlement Chain: Acquirer, PSP and Receiving Account

Every card payment passes through a chain before it becomes usable cash. The cardholder pays, the acquirer (the bank or processor that accepts the card transaction) collects the funds, the payment service provider routes them, and a receiving account takes the payout. The conversion decision is made near the end of that chain, based on which currencies the receiving account can accept.

If the account holds only GBP, the settlement currency must be GBP, and every other currency is converted to reach it. If the account holds EUR, USD, AED and HKD as well, each currency can settle into its own balance.

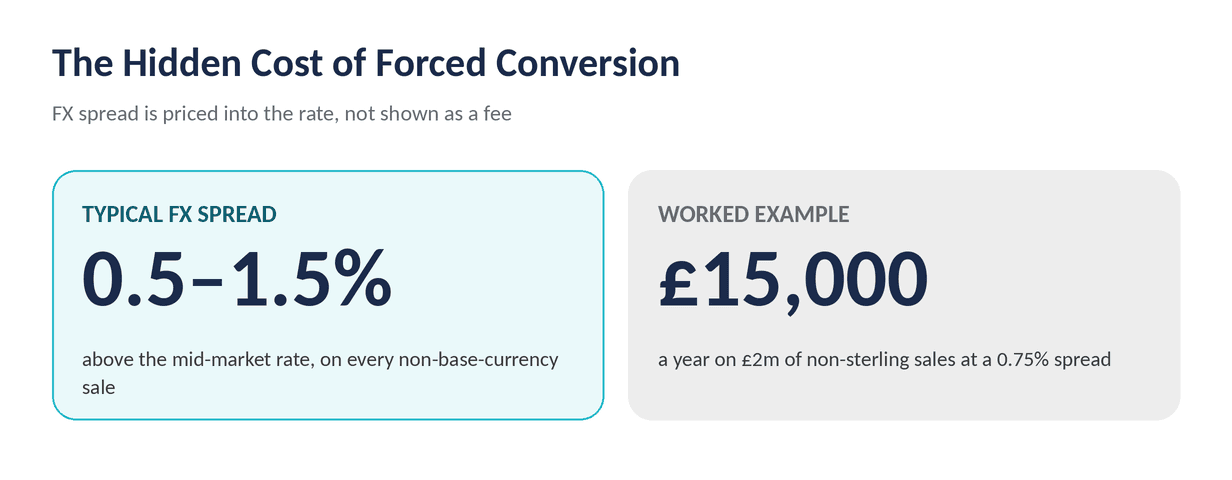

[aa fast-fact]

Fast Fact: An acquirer's FX spread is typically 0.5–1.5% above the mid-market rate, applied to the full settled amount. On £2m of non-sterling sales, a 0.75% spread is £15,000 a year in conversion cost that was never invoiced.

[/aa]

Why PSPs Force Conversion to a Base Currency

PSPs convert payouts to a base currency by default because most accounts are set up to receive only one. When a merchant registers a single GBP bank account for payouts, the acquirer has nowhere to send euros or dollars, so it converts everything to sterling first. The behaviour is a consequence of the account structure, not a deliberate penalty.

The economics, though, favour the provider. Conversion is priced as a spread rather than a line-item fee, which is why it rarely appears on a finance team's radar.

The Single Payout Account Limitation

A standard high-street business account holds one currency. Connect it to Stripe or Adyen and it can only receive that currency, so the PSP consolidates all sales into it. This is the root cause of forced FX: the receiving side cannot hold anything else.

Adding currencies to the receiving account removes the limitation. A multi-currency PSP settlement account holds several balances at once, giving the acquirer a destination for each settlement currency rather than one funnel into sterling.

Where the FX Spread Is Hidden

The spread sits inside the exchange rate, not next to it. A payout statement shows the converted GBP figure, not the mid-market rate that applied at the moment of conversion, so the difference is invisible without a side-by-side comparison. The foreign exchange spread is the gap between the rate the provider uses and the true market rate.

There is often a second, less obvious cost: the round trip. If a business converts EUR sales into GBP on the way in, then later buys euros again to pay an EU supplier, it pays a spread twice on the same value. Reconciling these flows is easier when each settlement arrives in its own currency, which is why finance teams pair multi-currency balances with automated reconciliation of multi-currency settlements.

What this means: forced conversion is not one cost but potentially two, and neither is quoted upfront.

[aa cta]

Stop losing margin to forced conversion

Receive each PSP settlement in its own currency and convert only when it suits the business, not the processor.

[aa btn]Open a multi-currency account[/aa]

[/aa]

How a Multi-Currency Account Enables FX-Neutral Settlement

A multi-currency account holds each currency in its own balance, so a payout in euros stays in euros and a payout in dirhams stays in dirhams. This is the account structure that makes FX-neutral settlement possible: it gives every settlement currency somewhere to land without conversion. The mechanism that competitors' guides tend to skip is the receiving side, because like-for-like settlement only works if the destination account can actually hold the currency.

At EQWIRE, multi-currency accounts are provided by a UK Electronic Money Institution (EMI) authorised and regulated by the Financial Conduct Authority (FCA), with funds held in safeguarded accounts under the Electronic Money Regulations 2011. Authorisation can be checked on the FCA Financial Services Register.

Per-Currency Sub-Balances and Dedicated IBANs

Each balance comes with the account details a PSP needs to pay into it. A euro balance carries an IBAN (International Bank Account Number) that clears over SEPA, while a sterling balance carries a named UK sort code and account number that clear over Faster Payments. Because these are real, named account details, Stripe and Adyen accept them as standard payout destinations.

This is exactly what a UK business needs to receive Stripe and Adyen payouts in GBP alongside foreign-currency settlements, rather than choosing one or the other.

GBP, EUR, USD, AED and HKD Held in Originating Currency

The practical question finance teams ask is direct: how do businesses receive GBP, EUR, USD, AED and HKD PSP settlements without auto-conversion to base currency? The answer is to hold a dedicated balance for each currency, each with its own receiving details, so the acquirer settles every transaction currency into its matching balance.

GBP clears via Faster Payments or CHAPS into a sterling balance.

EUR clears via SEPA into a euro balance.

USD and other major currencies settle via SWIFT or local rails where supported.

AED can be received directly, the same approach used to receive PSP payouts in AED from Adyen, Stripe and PayPal.

HKD lands in a dedicated balance, the structure UK exporters use to hold Hong Kong dollar revenue.

In practice: a merchant selling into five markets receives five settlements in five currencies, then converts only the surplus it genuinely needs in sterling.

![Diagram of a multi-currency account holding GBP, EUR, USD, AED and HKD in separate balances, each with its own IBAN or sort code]](https://framerusercontent.com/images/v84XvvEdRfq3V0IeBp8lcb3TmA.png)

Setting Up FX-Neutral PSP Payouts (Stripe, Adyen, PayPal)

To receive Stripe or Adyen payouts in the original currency, register a separate receiving account for each settlement currency, then set the payout currency to match the sale currency. The pattern is the same across providers: give the PSP a per-currency payout account, and it stops converting into a single base currency.

The four steps below apply to most setups, though exact options vary by provider and country.

Step 1: Open Per-Currency Receiving Accounts

Open a multi-currency account and note the receiving details for each currency you sell in, such as a euro IBAN and a sterling sort code. Each set of details is the destination for that currency's payouts.

Step 2: Register Each Payout Currency in Your PSP

In the PSP dashboard, add a payout account for each currency rather than a single default. Adyen calls this configuring a payout account per payout currency; Stripe calls it adding a bank account per settlement currency.

Step 3: Match the Payout Currency to the Settlement Currency

Set each currency to pay out in its own form. The goal is like-for-like settlement, where the scheme and the PSP apply no conversion because the destination currency matches the transaction currency.

Step 4: Verify the First Payout Lands Unconverted

Check the first settlement in each currency. The amount received should match the settlement report in the same currency, with no exchange rate applied between them.

Per-PSP Notes

The mechanics differ slightly between providers, and one default catches teams out.

Stripe: supports settlement in additional currencies when you add one bank account per supported settlement currency. A default settlement currency is still required, and any currency without its own configured account auto-converts into that default.

Adyen: offers like-for-like settlement when a payout account is set up per payout currency; currencies without one are paid into the primary settlement currency.

PayPal: holds balances in multiple currencies and lets you withdraw each to a matching account, but watch the account-level setting that auto-converts incoming funds to a primary currency. The same per-currency principle applies when you configure payout currencies to avoid conversion.

Which Rails Clear Each Currency

Different currencies settle over different payment rails, and the rail affects speed and cost. For wider context on cross-border settlement and correspondent banking, the Bank for International Settlements publishes ongoing analysis.

Currency | Typical rail | Indicative speed |

|---|---|---|

GBP | Faster Payments / CHAPS | Same day |

EUR | SEPA Credit Transfer | Same day or next day |

USD | SWIFT / local rails | 1–3 business days |

AED, HKD | SWIFT / local rails | 1–3 business days |

When You Should, and Shouldn't, Convert

FX-neutral settlement is most valuable when a business has real costs in the currencies it earns. A company that pays EU suppliers, US contractors or UAE staff can fund those costs straight from the matching balance, avoiding conversion entirely on that portion of revenue.

It adds less value when a business ultimately needs everything in one currency. If a UK company sells abroad but spends only in sterling, holding foreign balances delays an unavoidable conversion rather than removing it, and it adds a little operational overhead. The honest test is whether the foreign-currency balance will be spent in that currency or simply converted later anyway.

Decision trigger: if foreign-currency costs are a regular part of the business, FX-neutral settlement protects margin; if not, the saving is mostly timing.

Conclusion

Forced conversion is a default, not a rule, and it persists mainly because the receiving account can hold only one currency. Building FX-neutral settlement for multi-currency PSP payouts is a structural fix: open per-currency balances, register each currency with the PSP, and let every settlement land in the currency it was earned in. The result is the ability to receive PSP payouts in multiple currencies and convert on the business's own terms, with the spread paid only when conversion is genuinely needed.

FAQ

How do businesses receive GBP, EUR, USD, AED and HKD PSP settlements without auto-conversion to base currency?

Businesses receive GBP, EUR, USD, AED and HKD PSP settlements without auto-conversion to base currency by holding a dedicated balance for each currency in a multi-currency account, then registering each balance as a separate payout destination in the PSP. Stripe and Adyen settle each transaction currency into its matching account, so euros stay as euros and dirhams stay as dirhams. Conversion happens only when the business chooses to move funds between currencies.

Can you receive Stripe payouts without forced conversion?

Yes. Stripe supports settlement in additional currencies when you add one bank account per supported settlement currency, and charges in those currencies then settle without conversion. The important detail is that Stripe still requires a default settlement currency, so any currency without its own configured payout account is converted into that default. To get PSP payouts without forced conversion across every market, register a receiving account for each currency you sell in.

What is the difference between multi-currency settlement and FX-neutral settlement?

Multi-currency settlement describes the acquirer holding and paying out each transaction currency separately rather than consolidating into one. FX-neutral settlement is the outcome for the merchant: receiving each payout in its original currency with no exchange rate applied. In practice they go together, because settling each currency separately is what allows the payout to stay FX-neutral.

Do I need a separate IBAN for each settlement currency?

You need separate receiving details for each currency, which usually means a dedicated IBAN for euros and a named sort code and account number for sterling. Most PSPs allow only one bank account per settlement currency, so each currency must point to its own balance. A multi-currency account provides these details for several currencies at once, which is why it supports PSP payouts without forced FX.

Is FX-neutral settlement worth it for a smaller business?

It depends on whether the business spends in the currencies it earns. A smaller company that pays foreign suppliers or contractors can save the full FX spread, often 0.5–1.5% per conversion, by funding those costs directly from matching balances. A business that converts everything to sterling regardless gains mainly timing flexibility rather than a hard cost saving, so the benefit scales with the share of revenue spent in foreign currencies.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)