•

•

Director Dividend Account: Receiving GBP, EUR and USD as a Company Director

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A UK company director receives a £60,000 EUR dividend from a German subsidiary. By the time the transfer arrives at a standard high-street bank, £1,400 has been lost to FX conversion fees — automatically applied, with no option to hold the euros. This is not an edge case. It is the default behaviour of most UK business bank accounts, and it costs directors thousands of pounds each year.

A dedicated director dividend account solves this problem. It is a multi-currency payment account — typically held at an FCA-authorised EMI — that receives GBP, EUR and USD in separate currency wallets, without triggering automatic conversion. This article explains how these accounts work, what the regulatory framework looks like, and how to set one up.

[aa key-takeaways]

Key Takeaways

A director dividend account is a multi-currency payment account used to receive and segregate GBP, EUR and USD dividend income

FCA-authorised EMI accounts hold balances in separate currency wallets — EUR stays EUR, USD stays USD, until the director decides to convert

Named IBANs are required to receive EUR via SEPA and USD via SWIFT without rejection or auto-conversion

UK Faster Payments handles same-day GBP dividend receipts without correspondent bank delays

Board fees, consulting retainers and dividend distributions can all be received into the same account

FCA-authorised EMI accounts are typically faster to open than traditional bank accounts and carry lower FX margins

[aa btn]Open an Account[/aa]

[/aa]

What Is a Director Dividend Account?

A director dividend account is not a formally regulated product category. It is a use case: a multi-currency payment account used specifically by a UK company director to receive dividend distributions, board fees, and consulting income in their original currency.

The account holder is the director personally — not the company. What distinguishes it from a standard salary account is currency handling. Directors receiving dividends from EU subsidiaries or US parent companies need an account that accepts SEPA EUR transfers and SWIFT USD payments without converting them on arrival. A standard UK current account does neither reliably.

How Directors Receive Dividends in the UK

Under UK company law, dividends are distributions of post-tax profit, declared by the board and documented via a dividend voucher. They can be paid monthly, quarterly, or annually, depending on the company's dividend policy.

For directors of UK subsidiaries with EU or US parents, the paying entity may transfer EUR or USD directly. The Companies Act 2006 governs the mechanics of UK dividend declarations, but it places no restriction on the currency in which dividends are paid. The bottleneck is the receiving account — most UK bank accounts auto-convert foreign currency inflows at the bank's own rate, typically 1.5–3% above the mid-market rate.

Why a Separate Account Improves Clarity and Tax Reporting

HMRC requires directors to report foreign dividend income in sterling on their self-assessment return. The applicable rate is the exchange rate on the date of receipt — not when the director converts the funds.

When dividend income is held in a dedicated multi-currency account for GBP, EUR and USD, the director and their accountant can identify each inbound transfer by date and currency. This makes year-end reconciliation significantly cleaner. Without currency segregation, EUR and USD dividends appear as GBP entries in a bank statement — already converted at an undocumented rate.

[aa fast-fact]

Fast Fact: A director receiving EUR 80,000 in annual dividends via a bank that applies a 2% FX margin loses approximately £1,440 compared to holding the balance and converting at the mid-market rate. Over five years, that is over £7,000.

[/aa]

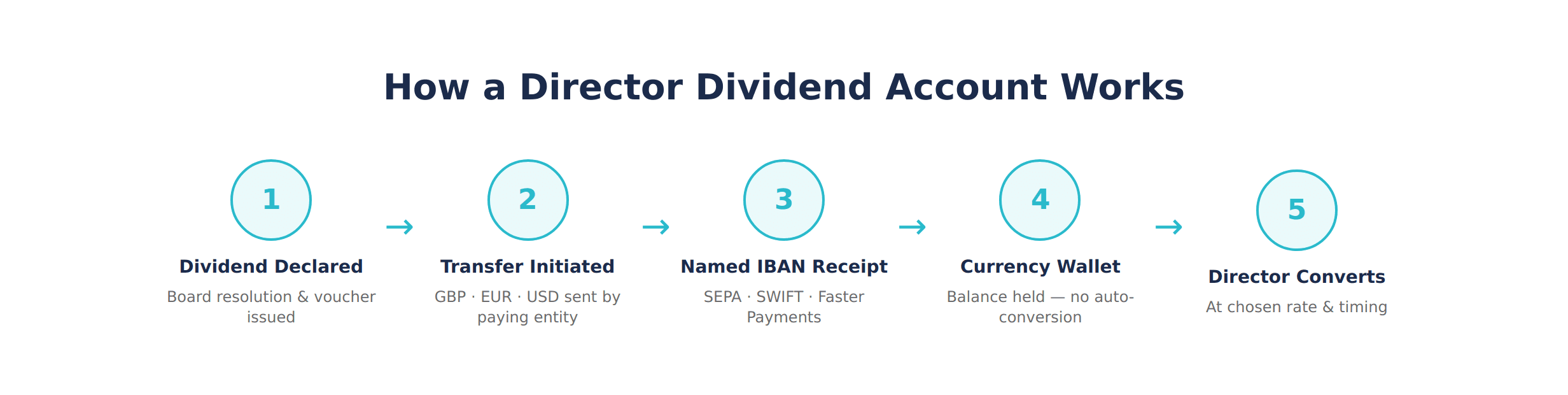

How a Multi-Currency Director Dividend Account Works

The architecture of a director dividend account built on an FCA-authorised EMI platform has three components: currency wallets, named IBANs, and payment rail access. Together, they allow a director to receive dividends in their original currency and hold them until conversion makes financial sense.

This is what distinguishes an account for director dividends GBP EUR USD at an EMI from a standard business bank account: the EMI does not convert on arrival. The balance sits in the wallet of the currency it was received in.

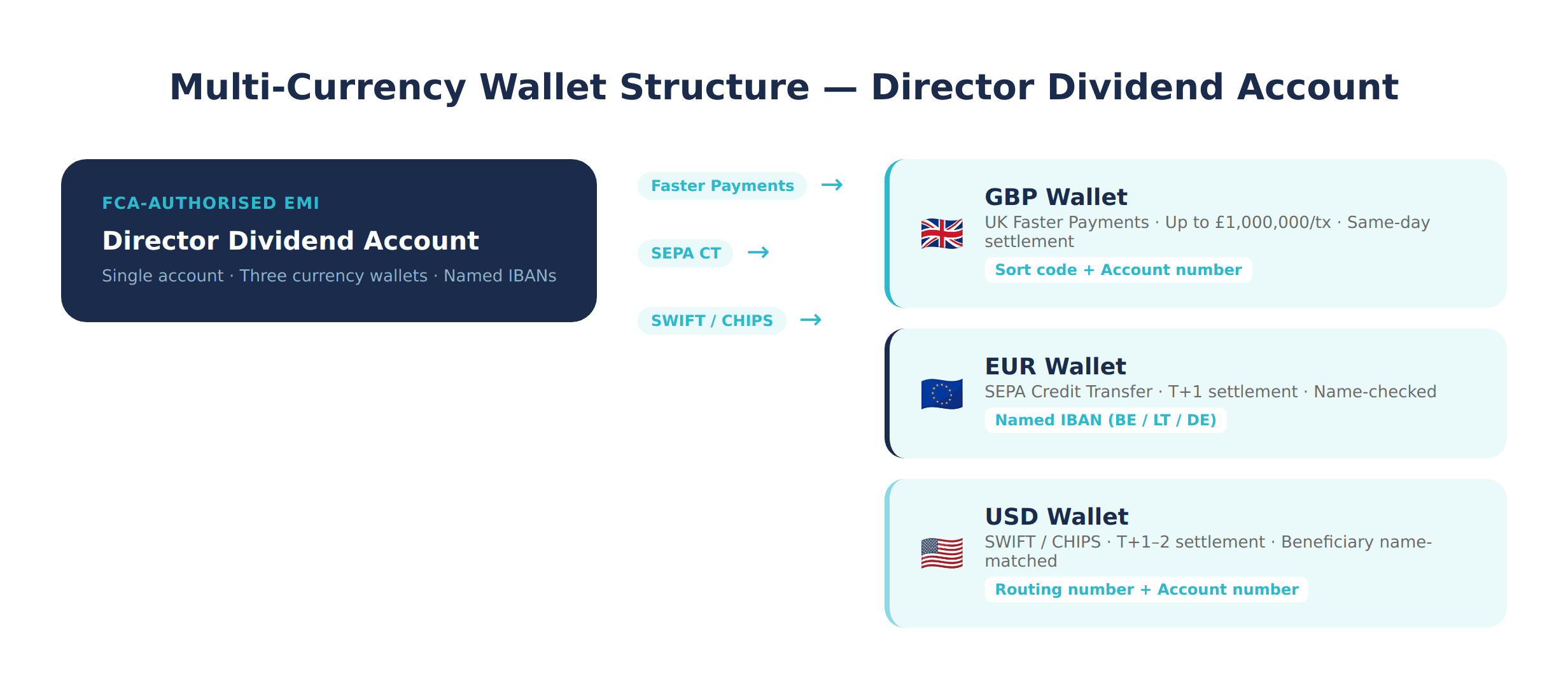

Currency Segregation — Holding Balances Without FX Conversion

Most EMI multi-currency accounts operate on a wallet model. EUR received stays in the EUR wallet. USD received stays in the USD wallet. GBP stays in the GBP wallet. The director converts only when they choose to — not when the bank decides to.

Contrast this with a standard bank: incoming EUR may be converted to GBP automatically at the bank's rate the moment the transfer settles. The director has no control, no timing choice, and often no advance notice of the rate applied.

Accounts that hold multi-currency balances without FX conversion are particularly valuable for directors whose companies also have EUR-denominated costs — the received EUR dividend can be used directly to pay EU suppliers without conversion in either direction.

Named IBANs for EUR and USD Receipts

A named IBAN is an IBAN assigned exclusively to one account holder — not shared with other clients of the same EMI. This distinction matters for two practical reasons.

First, SEPA EUR transfers require the beneficiary name to match the account holder name. Many EU-based companies — and most European payment systems — apply name-checking rules before releasing a transfer. A shared IBAN fails this check because the account name is the EMI's, not the director's. The payment is rejected or returned.

Second, SWIFT USD payments include a beneficiary field that must match exactly. A named IBAN business account in the UK satisfies both requirements: the director's name appears on both the IBAN and the SWIFT beneficiary record, so EUR and USD dividends route directly to the right wallet.

UK Faster Payments for GBP Dividends

GBP dividend payments from UK Ltd companies are typically sent via the UK Faster Payments scheme, which settles in seconds — 24 hours a day, 365 days a year. For larger distributions, CHAPS (same-day high-value settlement, typically used above £250,000) is the alternative.

The Faster Payments limit for most EMI and bank accounts is up to £1,000,000 per transaction. For quarterly or annual dividend runs, this covers most director-level distributions without needing to split the payment.

Legacy BACS transfers — still used by some older payroll and finance systems — take three business days. Directors who rely on BACS for dividend receipt may experience unnecessary delays. Switching the receiving account to an EMI with Faster Payments access resolves this.

[aa cta]

Open a Director Dividend Account with Named IBANs

Receive GBP, EUR and USD dividends without FX conversion — FCA-authorised, ready in minutes.

[aa btn]Open an Account[/aa]

[/aa]

The Regulatory Framework — FCA-Authorised EMI vs. Bank

The question finance managers ask most often: is an EMI account as safe as a bank account for receiving director dividends?

The answer depends on what "safe" means. For a payment account used to receive and hold dividend income — not a savings account — an FCA-authorised EMI provides a structurally sound solution. Understanding the regulatory distinction helps directors choose the best account for company directors receiving foreign dividends UK.

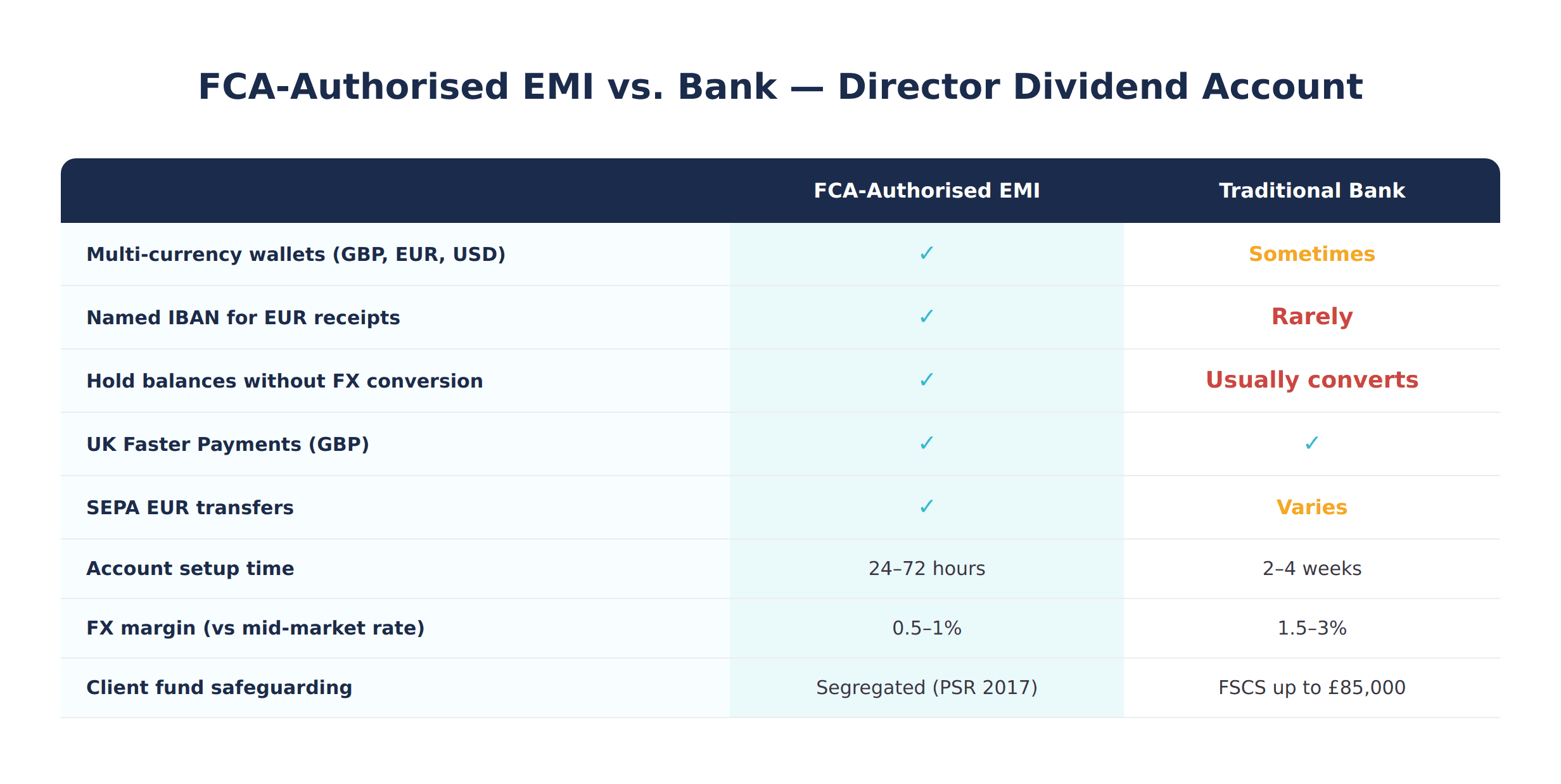

What FCA Authorisation Means for Director Accounts

An FCA-authorised EMI is licensed under the Electronic Money Regulations 2011 to issue electronic money and provide payment services. The FCA licence covers incoming and outgoing payments, currency exchange, and account management.

What it does not cover: lending, deposit-taking, or interest. For a director using the account as a pass-through for dividend receipts, these omissions are irrelevant. The account is a payment instrument, not a savings vehicle.

Safeguarding Rules and What Protects Your Funds

Under the Payment Services Regulations 2017, FCA-authorised EMIs are required to safeguard client funds. This means the EMI must hold client money in a segregated account at a credit institution — completely separate from the firm's own operating funds.

If the EMI becomes insolvent, safeguarded client funds are ring-fenced and returned to account holders in the insolvency process. This is different from FSCS protection at a bank (which covers deposits up to £85,000 automatically), but it provides meaningful structural protection for director dividend balances.

The practical implication: a director holding EUR 50,000 in dividend income at an FCA-authorised EMI has legal protection over those funds. They are not at risk if the EMI's business fails.

[aa fast-fact]

Fast Fact: As of 2024, the FCA register lists over 200 authorised EMIs operating in the UK — including providers offering named IBANs, multi-currency wallets, and real-time Faster Payments access for business and director accounts.

[/aa]

Step-by-Step: Setting Up a Director Dividend Account

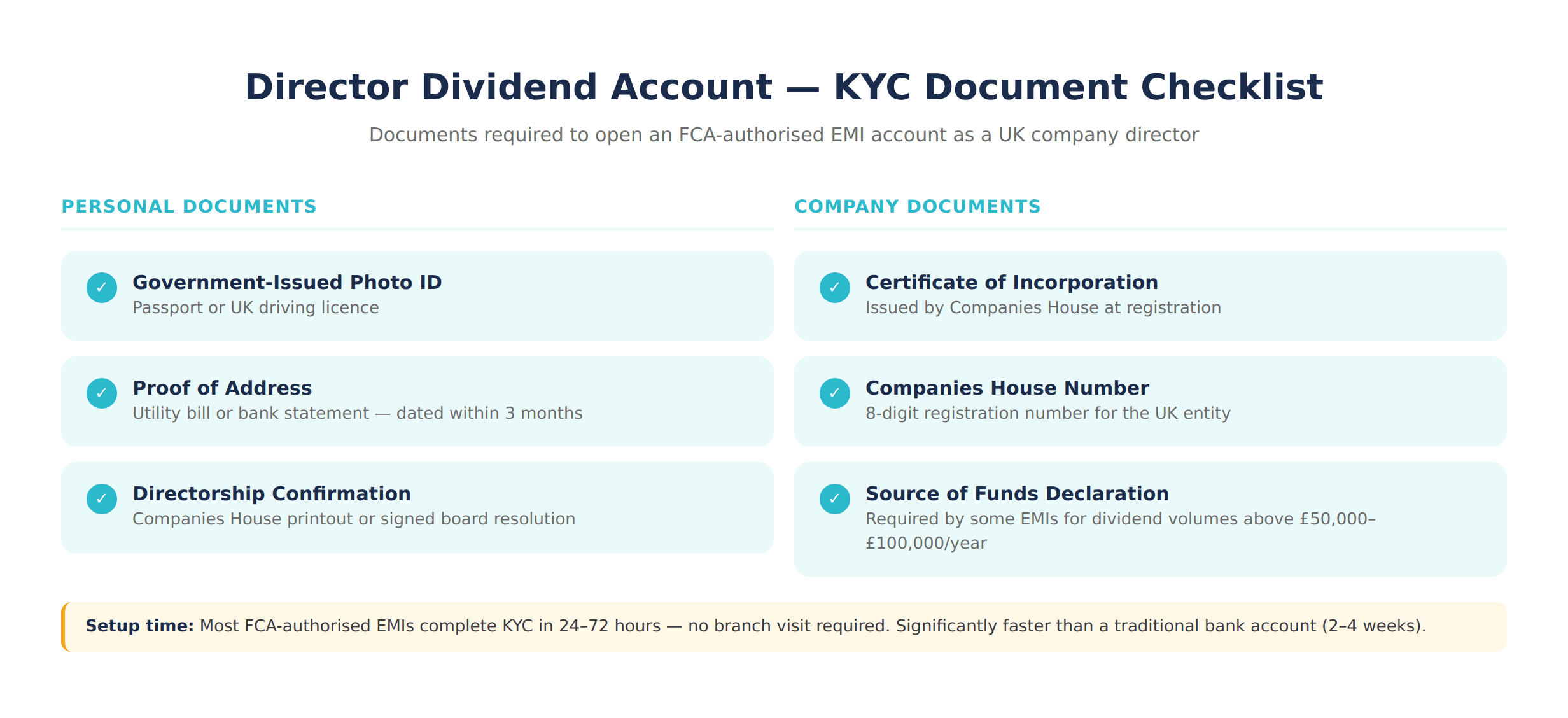

For a director and board member account for GBP EUR USD fees and dividends UK FCA EMI, the onboarding process is significantly lighter than opening a full business bank account. Most FCA-authorised EMIs complete KYC in 24–72 hours and do not require branch visits.

Here is the standard setup sequence.

Documents Typically Required (KYC)

The director applies individually — this is a personal account for receiving distributions, not a company account. Standard documentation includes:

Government-issued photo ID (passport or driving licence)

Proof of address (utility bill or bank statement, dated within 3 months)

Companies House company number

Certificate of Incorporation

Confirmation of directorship role (Companies House printout or board resolution)

Some EMIs also request a source of funds declaration for higher-volume dividend flows — typically triggered above a threshold of £50,000–£100,000 per year. This is a standard AML requirement, not a barrier.

The full process is substantially faster than a high-street bank. Traditional banks often require in-branch verification, a business relationship manager, and a 2–4 week underwriting review for new director accounts.

How to Configure Currency Wallets

After onboarding is complete, the account setup involves activating wallets and obtaining named IBANs for each currency.

How company directors receive foreign dividends in original currency UK without FX conversion comes down to this configuration step: the EUR and USD wallets must be active before the first dividend transfer. Sending EUR to an account that has not yet issued a EUR IBAN results in a rejected or returned payment.

The typical sequence:

Activate GBP wallet — Faster Payments sort code and account number issued immediately

Request EUR IBAN — typically an IBAN in BE, LT, or DE jurisdiction, assigned to the director's name

Request USD account details — routing number (ABA) + account number, or SWIFT/BIC + IBAN depending on the EMI's correspondent bank

Share the correct details with the dividend-paying company before the next distribution date

A test transfer — EUR 10 or USD 10 — before the full dividend run confirms the routing is correct and the currency holds without auto-conversion.

Currency | Payment Rail | Settlement | Key Requirement |

|---|---|---|---|

GBP | UK Faster Payments / CHAPS | Seconds / Same day | Sort code + account number |

EUR | SEPA Credit Transfer | T+1 | Named IBAN (IBAN must match beneficiary name) |

USD | SWIFT / CHIPS | T+1–2 | Routing number + account number or SWIFT BIC |

For directors with dividends from multiple entities in different currencies, the same account handles all three rails — no need for separate accounts per currency.

FAQ

Can a company director receive GBP, EUR and USD dividends into the same account?

Yes. An FCA-authorised EMI account with multi-currency wallet support holds GBP, EUR and USD in separate balances within a single account. Each currency has its own IBAN or account details. Dividends paid in EUR by EU entities route to the EUR wallet; USD distributions from US parents go to the USD wallet; GBP payments from UK subsidiaries settle via Faster Payments into the GBP wallet.

What is the best account for company directors receiving foreign dividends in the UK?

An FCA-authorised EMI account with named IBANs and currency wallet segregation is the most practical option for directors receiving foreign dividends. It avoids automatic FX conversion, supports SEPA for EUR and SWIFT for USD, and is typically faster to open than a traditional business bank account. Directors should verify the EMI is listed on the FCA register before opening an account.

How does a director account with multi-currency GBP EUR USD named IBAN work for tax reporting?

HMRC requires that foreign dividend income is declared in GBP at the exchange rate on the date of receipt. A director account with named IBAN for multi-currency GBP EUR USD keeps each inbound transfer dated and currency-identified, making it straightforward to calculate the sterling equivalent at the time of receipt for self-assessment purposes.

What documents does a UK company director need to open a multi-currency dividend account at an EMI?

Standard requirements are: government-issued photo ID, proof of address dated within 3 months, Companies House number, Certificate of Incorporation, and confirmation of directorship. Some providers may request a source of funds declaration for high-volume accounts. The process is typically completed in 24–72 hours with no branch visit required.

Can board fees and dividend payments be received into the same account for director receiving board fees in multiple currencies UK?

Yes. A multi-currency director account handles all types of director income — dividends, board fees, consulting retainers — regardless of the paying entity or currency. Each inbound transfer is routed to the appropriate currency wallet based on the currency of the transfer, with no manual sorting required. Directors receiving USD board fees from a US parent and EUR dividends from a European subsidiary can hold both in the same account, unconverted, until it is optimal to exchange or transfer.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)