•

•

HKD to GBP Conversion: How to Convert Hong Kong Dollars for UK Businesses

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

UK businesses that trade with Hong Kong suppliers and marketplaces regularly receive payments in Hong Kong dollars that need converting into pounds sterling. HKD to GBP conversion business activity has grown alongside UK-Hong Kong trade, yet many companies still let their bank or payment provider convert receipts automatically, at a rate the provider sets. This guide explains how the conversion actually works and which methods UK businesses can use. It also covers settlement times and the mistakes that quietly cost money on every transfer. Finance teams that understand these mechanics can decide when to convert Hong Kong dollars, rather than have the decision made for them.

[aa key-takeaways]

Key Takeaways

HKD is pegged to the US dollar within a 7.75–7.85 band, so the HKD-GBP rate largely tracks GBP-USD movements rather than trading as an independent pair.

Banks, specialist FX brokers, and EMI multi-currency accounts all convert HKD to GBP, but their fees and spreads differ significantly.

Many banks and payment service providers automatically convert HKD receipts into GBP on arrival, often at an uncompetitive rate.

EMI accounts with a Hong Kong dollar wallet let a business hold HKD and convert only when the rate suits it.

SWIFT transfers typically settle within one to five business days, though SWIFT gpi payments can arrive within hours.

[aa btn]Book a Call[/aa]

[/aa]

What HKD to GBP Conversion Means for UK Businesses

HKD to GBP conversion business needs typically arise when a UK company receives Hong Kong dollars from a supplier refund or a marketplace payout, then needs pounds sterling to pay suppliers or cover a tax bill. Converting between the two currencies looks like any other foreign exchange transaction, but the mechanics behind the Hong Kong dollar make it different from converting euros or US dollars.

The Hong Kong dollar is pegged to the US dollar, not freely floating against sterling. Under the Hong Kong Monetary Authority's Linked Exchange Rate System, the HKMA commits to keep the HKD trading between 7.75 and 7.85 per US dollar. The HKD-GBP rate effectively follows the GBP-USD rate rather than moving independently. A business watching GBP-USD movements gets a reasonable proxy for how HKD-GBP will behave over the same period.

Consider a UK homeware importer that receives a Hong Kong dollar refund from a supplier after a returned shipment. If GBP-USD strengthens in the days before the refund lands, the HKD-GBP rate typically improves in parallel, even though nothing in the Hong Kong dollar itself has changed. Waiting a day or converting immediately can produce a meaningfully different GBP amount, purely because of dollar movements the business may never have looked at.

This detail matters for timing. A UK business assuming HKD-GBP moves on its own logic may misread a shift that is really a US dollar story. In practice, a finance manager comparing quotes across providers should check the mid-market GBP-USD rate first, then confirm the quoted HKD-GBP rate isn't unusually wide of what that implies.

[aa fast-fact]

Fast Fact: Under the HKMA's Linked Exchange Rate System, the Hong Kong Monetary Authority commits to trade HKD within a 7.75–7.85 per US dollar band, a peg that has been in place since 1983.

[/aa]

Methods to Convert HKD to GBP

UK businesses converting HKD to GBP typically choose from a small set of provider types, each with a different cost and control trade-off. The right choice depends less on which provider name is best overall and more on how often Hong Kong dollars arrive and how much control over timing matters to the business.

High-Street Banks

High-street banks offer the most familiar route: a business already holding a GBP account can request a conversion through online or telephone banking. The convenience comes at a cost. Banks typically apply the widest spread of the three options, sometimes several percentage points above the mid-market rate, because most business customers don't shop around before accepting the quoted rate.

Settlement is usually straightforward once funds arrive, since the bank credits the GBP account directly. The trade-off is transparency: many banks don't display the spread separately from the transfer fee, so the true cost is easy to miss on a statement. Business customers rarely see the mid-market rate quoted alongside the bank's offer, which makes the spread difficult to benchmark without checking an independent rate source before accepting the conversion.

Specialist FX Brokers

Specialist FX brokers focus on international payments rather than day-to-day banking, operating under FCA authorisation like other regulated payment firms. Because currency conversion is their core business, they generally quote tighter spreads than high-street banks, and larger or recurring transfers can often secure further discounts.

The trade-off is setup time. A business needs a separate account with the broker, and larger transfers may require extra verification before the first payment clears. Once onboarded, brokers are usually faster to quote and settle than a bank for the same transfer. Many brokers also offer forward contracts, letting a business lock today's rate for a transfer expected in a few weeks, which can help when a large Hong Kong dollar payment is expected on a known date.

EMI Multi-Currency Accounts

An FCA-authorised EMI issues a multi-currency account that can receive, hold, and convert several currencies from a single dashboard, often through a dedicated virtual IBAN for each currency. A UK business receiving HKD can hold the balance in Hong Kong dollars rather than accepting an automatic conversion the moment funds land.

That control is the main advantage over a bank or broker: the business decides when to convert, based on its own read of the rate, not the provider's default timing. FCA-authorised EMIs safeguard client funds separately from the firm's own balance sheet, which gives businesses a regulatory framework similar in spirit to banking, without the account being a deposit account itself.

For a UK company with recurring Hong Kong dollar income, a multi-currency account removes the need to convert every receipt immediately and instead lets conversions happen on a schedule the finance team controls.

A Hong Kong dollar-denominated virtual IBAN also gives suppliers and marketplaces a local-feeling account number to pay into, which can reduce the friction some overseas partners experience when sending funds to an unfamiliar UK account structure. The receiving business still sees the balance in its single dashboard alongside its other currencies.

[aa cta]

Hold HKD Instead of Converting on Arrival

A multi-currency account lets a business receive Hong Kong dollars and convert to GBP only when the rate works in its favour, instead of accepting whatever a bank applies automatically.

[aa btn]Create Account[/aa]

[/aa]

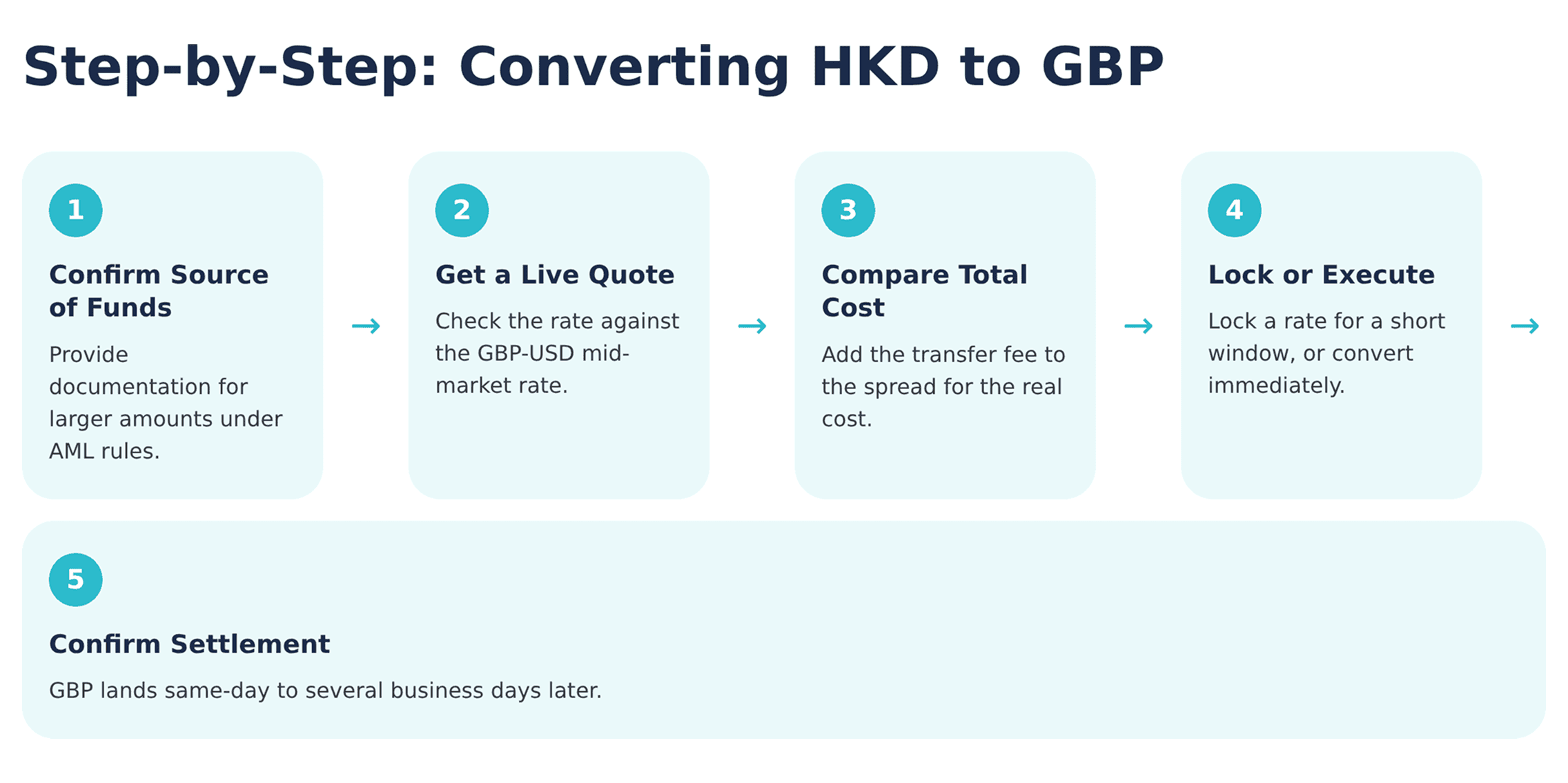

Step-by-Step Guide to Converting HKD to GBP

Converting HKD to GBP for a business follows a similar sequence regardless of provider, with the details changing at each step.

Confirm the source of funds. Most providers ask where the Hong Kong dollars came from before processing a first transfer, especially for larger amounts, under UK money-laundering regulations.

Get a live quote. Request a quote from the bank, broker, or EMI account and check the exchange rate against the current GBP-USD mid-market rate as a sanity check.

Compare the total cost. Add any transfer fee to the spread between the quoted rate and the mid-market rate to see the real cost, not just the headline fee.

Lock or execute the conversion. Some providers let a business lock a rate for a short window before funds arrive; others convert immediately at the live rate.

Confirm settlement. GBP typically lands in the business account within the timeframe the provider quoted, ranging from same-day to several business days depending on the route.

Fees and Exchange Rate Spreads Compared

The headline fee is rarely the biggest cost when a business converts HKD to GBP. The spread — the gap between the mid-market rate and the rate a provider actually offers — is where most of the cost sits, and it rarely appears as a separate line item.

High-street banks tend to apply the widest spreads, sometimes reported at up to several percentage points versus the mid-market rate. FCA-regulated specialist brokers typically narrow that gap and can save businesses several percentage points compared with a bank on the same transfer, though results vary by amount and route. An EMI account converting HKD GBP UK balances usually prices closer to the specialist broker end of the range, with the spread disclosed at the point of conversion rather than buried in a statement.

Recurring or high-value transfers change the calculation. A business converting the same corridor every month has more room to negotiate a tighter spread than one making a one-off transfer, regardless of which type of provider it uses.

A business converting a six-figure Hong Kong dollar balance rarely notices a fee of a few pounds, but a spread of even half a percentage point applied to that balance produces a meaningful difference in the GBP received. Comparing quotes across two or three providers before a large transfer is one of the simplest ways to test whether a quoted spread is competitive. Research on next-generation correspondent banking consistently points to the FX margin built into the spread, rather than the headline transfer fee, as the largest hidden cost in a cross-border transfer.

[aa fast-fact]

Fast Fact: According to the Bank for International Settlements, the global average cost of sending $200 cross-border stood at 6.5% in Q1 2025, with correspondent banking fees and FX spread among the largest components.

[/aa]

Why Some Providers Force-Convert HKD to GBP Automatically

Some banks and payment service providers convert HKD receipts into GBP automatically, without waiting for the account holder's instruction. This happens most often when the receiving account doesn't support holding Hong Kong dollars natively, so the provider's system defaults to converting into the account's base currency on arrival.

Automatic conversion is convenient for the provider and removes an operational step, but it hands the provider full control over both the timing and the rate. A business with no HKD-holding option has no opportunity to wait for a better GBP-USD movement or negotiate a rate on a larger balance.

A UK e-commerce seller receiving marketplace payouts in Hong Kong dollars, for example, may find the funds converted to GBP the same day they land, with no option to delay. Switching the payout destination to an account that can hold HKD natively is usually the only way to change that default.

Avoiding forced conversion generally means choosing a provider that can hold Hong Kong dollars as a native currency rather than converting on receipt. That account-level difference, not just pricing, is why EMI multi-currency accounts have become popular with businesses receiving recurring HKD income.

Settlement Times for HKD to GBP Transfers

Settlement speed for HKD to GBP conversion business transfers depends heavily on the payment rail. A standard SWIFT transfer typically settles within one to five business days, depending on how many correspondent banks the payment passes through before reaching the UK.

SWIFT gpi, the tracked version of the standard SWIFT network, moves faster in practice: around half of gpi payments credit within 30 minutes, and the large majority complete within 24 hours. Not every bank or corridor supports gpi tracking, so the improvement isn't guaranteed on every route.

EMI accounts and specialist brokers often quote same-day or next-day settlement once a conversion is executed, because the GBP leg of the transaction happens within their own payment network rather than a full correspondent banking chain. A business with a time-sensitive payment, such as a supplier deadline, should confirm the provider's typical settlement window before committing to a transfer date.

Public holidays in Hong Kong and the UK can add a day or more to a SWIFT-based transfer, since the payment can only move between banks that are open for business. A transfer initiated late in the Hong Kong business day, close to a UK bank holiday, is more likely to miss a same-day cut-off than one sent earlier in the week.

Common Mistakes UK Businesses Make When Converting HKD

A few recurring mistakes cost UK businesses money on HKD to GBP conversions.

Accepting the First Quoted Rate

A quote that looks reasonable in isolation can still carry a wide spread once compared with the GBP-USD-implied HKD-GBP rate. Checking the mid-market rate before accepting a quote takes a few minutes and often reveals room to negotiate.

Letting Every Receipt Auto-Convert

Automatic conversion on every incoming payment removes the option to wait for a better moment or negotiate on a larger, consolidated amount. Businesses that batch smaller receipts into fewer, larger conversions typically get quoted tighter spreads.

Ignoring Source-of-Funds Requirements

Providers can hold a transfer pending verification under UK money-laundering rules, and gathering invoices or contracts after the transfer has already stalled adds delay. Preparing this documentation before a large transfer avoids the hold-up entirely.

Waiting Until a Deadline Forces the Decision

Converting HKD to GBP only when a payment deadline is imminent removes any flexibility to wait for a better GBP-USD movement or to shop the transfer around. Businesses that track upcoming Hong Kong dollar receipts and plan the conversion a few days ahead of a deadline generally have more room to negotiate than those converting under time pressure.

[aa cta]

Move HKD to GBP on a Schedule That Suits the Business

Businesses with recurring Hong Kong dollar income can open a cross-border business account that settles conversions to GBP on their own timeline, not the bank's.

[aa btn]Create Account[/aa]

[/aa]

FAQ

What is the best way to convert HKD to GBP for a business?

The best way to convert HKD to GBP for a business depends on transfer size and frequency. A one-off, smaller transfer may be simplest through an existing bank account, despite the wider spread. A business converting Hong Kong dollars regularly, or in larger amounts, typically gets a better rate and more control through an FCA-regulated specialist broker or an EMI multi-currency account that can hold HKD until the business chooses to convert.

How long does an HKD to GBP transfer take?

A standard SWIFT-based HKD to GBP transfer typically settles within one to five business days, depending on how many correspondent banks the payment passes through. SWIFT gpi payments move faster, with roughly half crediting within 30 minutes and most completing within 24 hours, though not every bank supports gpi tracking. EMI accounts and specialist brokers often settle same-day or next-day once a conversion is executed.

Why is the HKD to GBP rate linked to the US dollar?

The HKD to GBP rate is linked to the US dollar because the Hong Kong dollar itself is pegged to the US dollar under the Hong Kong Monetary Authority's Linked Exchange Rate System, which keeps HKD trading within a 7.75–7.85 band per US dollar. HKD-GBP movements largely reflect changes in the GBP-USD rate rather than an independent HKD-GBP market.

Is there a way to get a better rate on HKD to GBP without automatic conversion?

There is no single fixed rate that is always best, since the mid-market HKD-GBP rate moves constantly with GBP-USD. The best FX rate for HKD to GBP conversion without forced conversion for UK businesses typically comes from comparing a live quote against the current mid-market rate and using a provider, such as an authorised electronic money institution, that lets the business hold Hong Kong dollars rather than converting them automatically on arrival.

Can a UK business hold Hong Kong dollars instead of converting to GBP immediately?

Yes. An EMI multi-currency account with a Hong Kong dollar wallet lets a UK business receive and hold HKD without an automatic conversion. The business can then convert to GBP whenever the rate or its cash flow needs make sense, rather than accepting whatever rate applies the moment funds arrive.

HKD to GBP conversion business decisions come down to two things: understanding what actually drives the rate, and choosing a provider structure that matches how often Hong Kong dollars arrive. The peg to the US dollar means HKD-GBP tracks GBP-USD rather than moving on its own, which is useful context when comparing quotes. Banks offer convenience at a wider spread. Specialist brokers narrow that spread for regulated international transfers, and EMI multi-currency accounts add the option to hold HKD and convert on a schedule the business sets. For companies with recurring Hong Kong dollar income, that control over timing is often worth more than a marginally better one-off rate. A multi-currency account built for this purpose is available at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)