•

•

ILS Business Account for Non-Israeli Companies: Receive Israeli Shekel Without a Local Bank

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A UK-registered holding company invoicing three Israeli technology clients absorbs 2–3% in FX conversion fees and waits up to five business days for SWIFT settlement — on every payment. Over a year, that compounds into thousands of pounds in avoidable cost, simply because the company has no way to receive Israeli shekel directly.

Setting up an ILS business account as a non-Israeli company in the UK resolves this. Non-Israeli companies — including UK Ltd entities, BVI structures, UAE Free Zone companies, and Cayman or Bermuda-registered firms — can receive ILS without opening an Israeli bank account. The mechanism is an FCA-authorised Electronic Money Institution (EMI) that holds ILS on behalf of non-resident corporate clients via correspondent access to Israeli local payment rails.

This guide covers the four steps to set up ILS receipt: choosing a qualifying provider, completing the KYB process, sharing account details with Israeli clients, and managing ILS balances after receipt.

[aa key-takeaways]

Key Takeaways

Non-Israeli companies (UK Ltd, BVI, UAE Free Zone, Cayman, Bermuda) can receive ILS without opening an Israeli bank account.

Setup through an FCA-authorised EMI takes 3–7 business days with a complete KYB document pack.

Israeli clients pay via a domestic bank transfer — no SWIFT required on their end — with settlement typically completing the same business day via Israel's MASAV interbank clearing system.

Most mainstream fintech providers restrict ILS to EEA-incorporated clients; confirming non-EEA eligibility before applying is the critical first step.

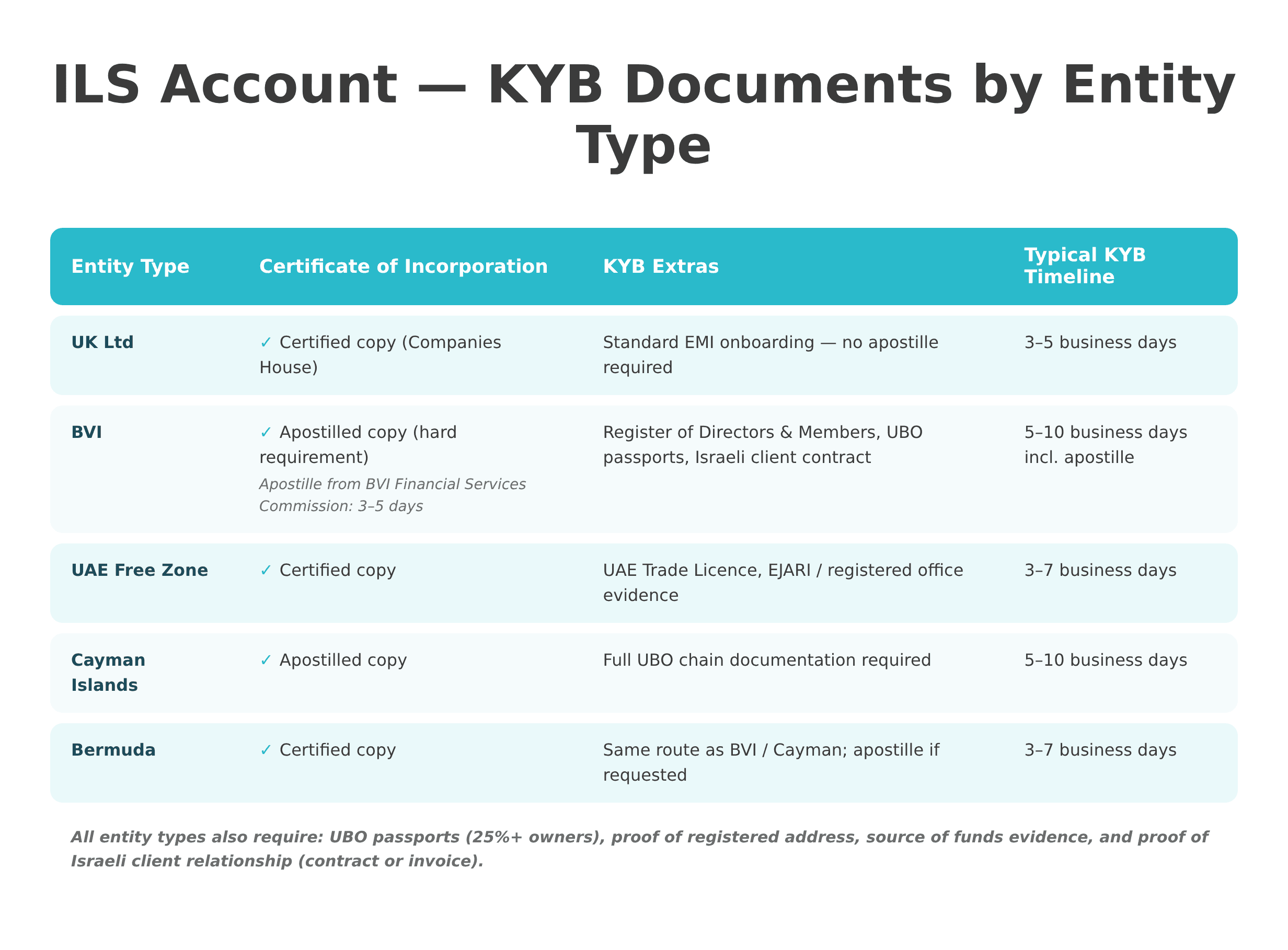

Required KYB documents differ by entity type: BVI companies need an apostilled Certificate of Incorporation; UAE Free Zone companies need a trade licence; UK Ltd companies follow standard EMI onboarding.

Holding ILS vs converting on receipt is a treasury decision — companies with ongoing ILS-denominated expenses benefit from holding; others typically convert at receipt.

[aa btn]Book a Call[/aa]

[/aa]

What You Need Before You Start — ILS Account Checklist

Opening an ILS business account as a non-Israeli company requires three things: an eligible entity type, a complete KYB document pack, and a provider authorised to offer ILS to non-resident corporates. The Bank of Israel does not prohibit non-resident entities from holding or receiving ILS — the restriction exists at the provider level, not the regulatory level.

Entity Type Eligibility

The following entity types are generally eligible to open an ILS receipt account through qualifying EMI providers:

UK Ltd — treated as a non-EEA entity post-Brexit; standard EMI onboarding applies

BVI (British Virgin Islands) — eligible; apostilled incorporation documents required

UAE Free Zone (DMCC, DIFC, RAKEZ, JAFZA, and others) — eligible; UAE trade licence required; GBP banking with a UK sort code is also available through the same FCA infrastructure

Cayman Islands — eligible with full UBO disclosure

Bermuda — eligible; onboarding follows the same route as Bermuda-registered companies accessing payment infrastructure through FCA-authorised EMIs without local presence

Sole traders, unregistered partnerships, and entities from jurisdictions on Financial Action Task Force (FATF) high-risk lists are typically excluded.

Required KYB Documents by Jurisdiction

Document requirements vary by entity type, but the core pack across all jurisdictions includes:

Certificate of Incorporation (apostilled for BVI and Cayman entities)

Register of Directors and Members (or equivalent shareholder register)

Passport copies for all Ultimate Beneficial Owners (UBOs) holding above 25%

Proof of registered address (utility bill, bank statement, or official correspondence dated within 3 months)

Proof of business activity with an Israeli counterparty — a signed contract or recent invoice demonstrating a legitimate ILS payment need

For UAE Free Zone entities, a current trade licence and registered office evidence (EJARI or equivalent) is required in addition to the core pack. For BVI entities, the apostille on the Certificate of Incorporation is the most common source of delay. Applications submitted without a properly apostilled document are routinely returned, adding 5–10 business days to the timeline.

Step 1 — Choose a Provider That Supports ILS for Non-Israeli Entities

Not every fintech provider that lists ILS as a supported currency will open an account for a non-Israeli, non-EEA company. The critical question is whether the provider has access to Israeli local payment rails for non-resident corporates — not just whether ILS appears in a supported currency list.

Key Criteria: ILS Rail Access, EEA Restriction Check, FX Fees

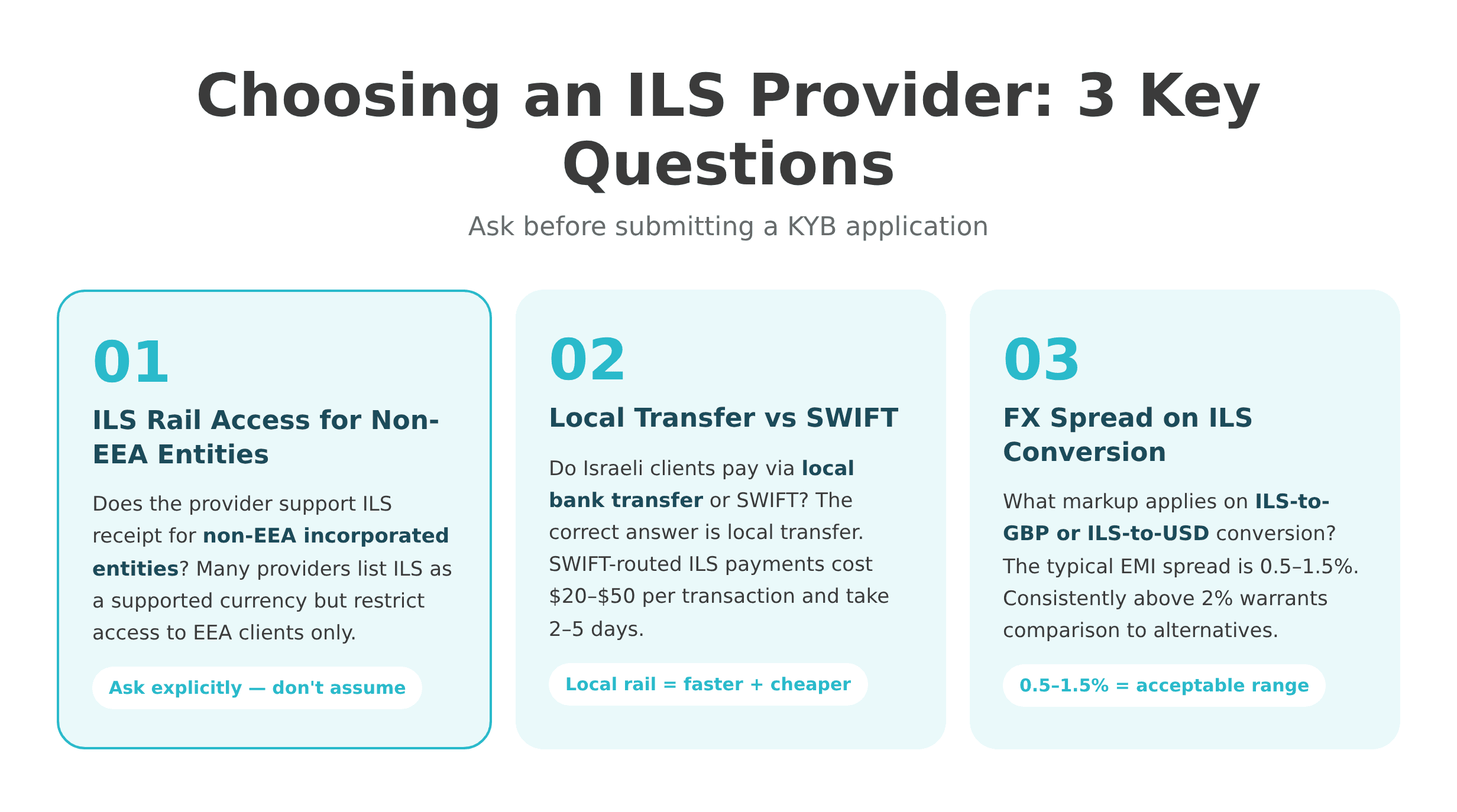

Before submitting a KYB application, finance teams should ask three specific questions:

Does the provider support ILS receipt for non-EEA incorporated entities? Not all providers that list ILS as a currency do.

Do Israeli clients send payments via local bank transfer or SWIFT? Local bank transfer is the correct answer — SWIFT-routed ILS transfers defeat the purpose of the arrangement.

What FX markup applies on ILS-to-GBP or ILS-to-USD conversion? The typical EMI spread for ILS is 0.5–1.5%; anything consistently above 2% warrants comparison.

EQWIRE is an FCA-authorised Electronic Money Institution (firm reference number 901100) that supports ILS receipt for non-Israeli entities including UK Ltd, BVI, UAE, Cayman, and Bermuda structures. The same flexibility that enables offshore companies to access payment accounts outside traditional banking through FCA-regulated infrastructure extends to ILS receipt for non-resident corporates.

Why Most Fintech Providers Block ILS for Non-EEA Clients

ILS settlement depends on correspondent banking relationships with Israeli clearing institutions. Many EMIs access ILS settlement through a correspondent that imposes its own eligibility rules — often restricting access to clients incorporated in the EEA. This is an operational constraint arising from correspondent banking dependency, not a legal prohibition on non-residents holding ILS.

Multiple providers explicitly document ILS eligibility restrictions based on client jurisdiction — demonstrating that the restriction is a provider-level decision. Post-Brexit, UK entities are classified as non-EEA by most providers, which means they may qualify under different eligibility criteria than EU-incorporated companies. The practical implication: confirming ILS eligibility with a provider before beginning a KYB application saves significant time.

Step 2 — Complete the Application and KYB Process

Once a qualifying provider is identified, the onboarding process follows a standard KYB (Know Your Business) format, typically completed remotely in 3–7 business days. No travel to Israel or to the provider's offices is required.

What to Prepare: UBO Docs, Director IDs, Proof of Business Activity

The standard document pack for an ILS multi-currency account for a foreign company includes:

Certificate of Incorporation — apostilled for BVI and Cayman; certified copy for UK Ltd and UAE Free Zone

Register of Directors and Members (or shareholder register)

Passport copies for all UBOs above 25% ownership

Source of funds evidence — bank statements or audited accounts reflecting the business's financial position

Proof of business activity with an Israeli counterparty — a contract or invoice confirms the legitimate ILS payment need and satisfies AML source of funds requirements

For UAE Free Zone entities, the trade licence and a registered address document are required in addition to the core pack. For BVI companies looking to open an ILS account without an Israeli presence, apostilles must be obtained before submission — typically from the BVI Financial Services Commission.

[aa fast-fact]

Fast Fact: BVI apostille processing typically takes 3–5 business days through the BVI Financial Services Commission. Factor this into the timeline before starting a KYB application.

[/aa]

Typical Timeline and What Causes Delays

Standard KYB processing takes 3–7 business days once a complete pack is submitted. The most common causes of delay:

Missing apostille on BVI or Cayman incorporation documents — adds 5–10 business days

Expired UBO passport — all identity documents must be current at submission

Name mismatch between the director named on incorporation documents and the passport copy provided

Incomplete UBO chain — for layered ownership structures, the full chain to natural persons must be documented

Providers authorised under the Electronic Money Regulations 2011 are required to complete KYB checks before issuing accounts. Submitting a complete, consistent document pack on the first attempt is the single most effective way to stay within the 3–7 day window.

[aa cta]

Receive ILS Without an Israeli Bank Account

EQWIRE is an FCA-authorised EMI that supports ILS receipt for non-Israeli companies, including UK Ltd, BVI, UAE, and other offshore entities.

[aa btn]Open Your ILS Account[/aa]

[/aa]

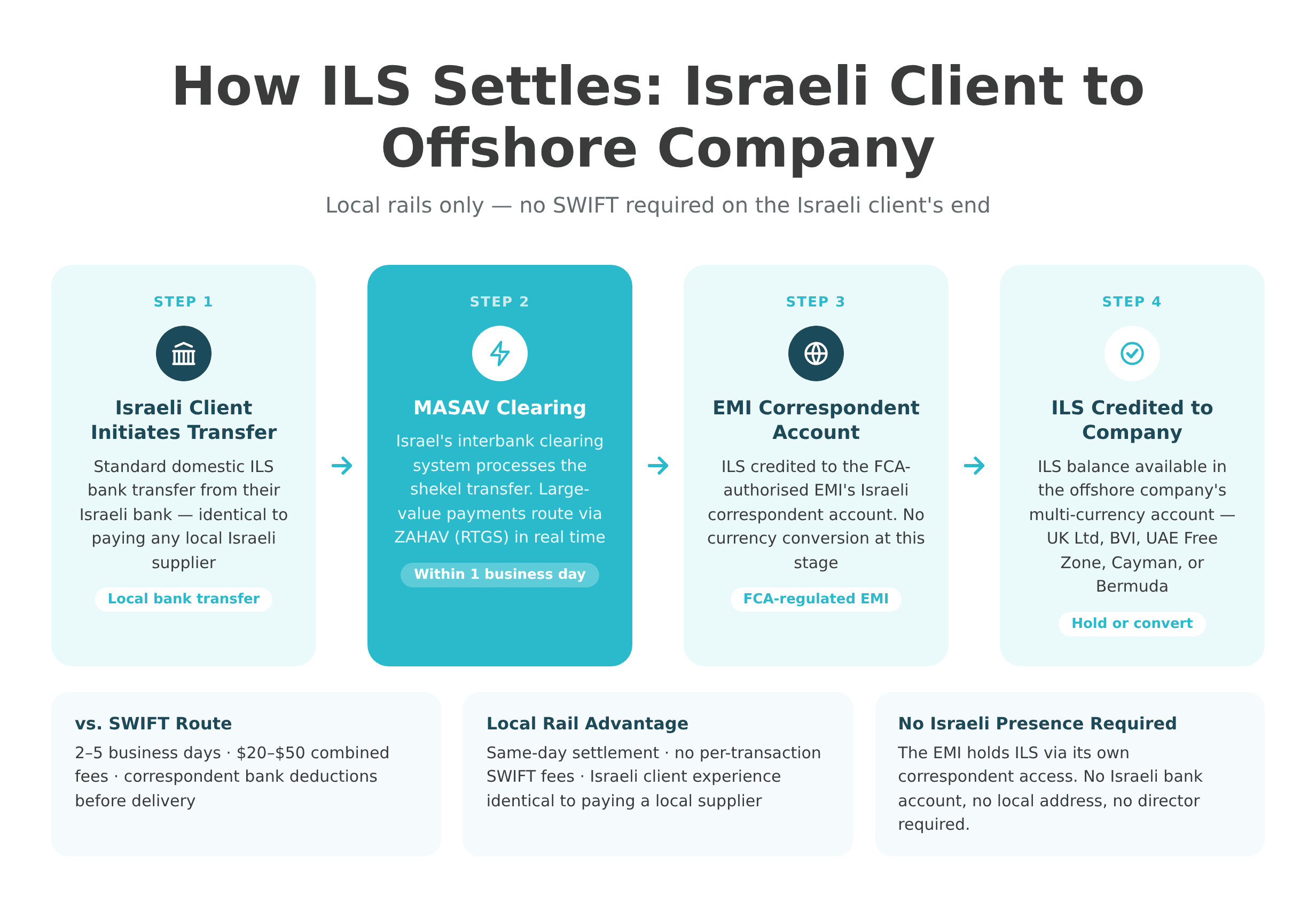

Step 3 — Share Your ILS Account Details With Israeli Clients

Once the ILS account is active, the offshore company shares local account details with its Israeli clients — the same fields used for any domestic Israeli bank transfer. For a BVI or UAE company receiving ILS from Israeli clients without opening an Israeli bank account, the process from the client's perspective is a standard local transfer, no different from paying any Israeli-based supplier.

What Information the Client Needs to Send ILS

The EMI issues dedicated account details — similar in structure to the named IBAN accounts used in multi-currency business banking — that are compatible with Israeli local payment rails. The Israeli client's bank will require:

Beneficiary name — the legal entity name as registered with the EMI

Account number — issued by the EMI, compatible with Israeli clearing systems

Bank identifier — typically a SWIFT/BIC pointing to the EMI's Israeli correspondent

IBAN — where required; Israel uses the IBAN format (IL prefix + 21 digits) for incoming international transfers

The Israeli client does not need to convert currency or use SWIFT — the payment is initiated as a local ILS bank transfer from their Israeli bank account, identical to paying any local supplier.

How the Transfer Settles: Local Israeli Rails, Not SWIFT

ILS transfers from Israeli clients settle via Israel's domestic interbank infrastructure. For retail and SMB-level transactions, settlement typically occurs through MASAV — Israel's bulk interbank clearing system. According to the Bank of Israel's MASAV clearing system documentation, MASAV clears electronic shekel transfers within seconds, with final settlement completing within one business day.

Large-value transfers may route via ZAHAV — Israel's Real-Time Gross Settlement (RTGS) system. As documented by the Bank for International Settlements, ZAHAV processes individual transactions in real time, typically completing within minutes during Israeli banking hours.

By contrast, a SWIFT-routed ILS transfer typically takes 2–5 business days and incurs combined sender, correspondent, and receiver fees of $20–$50 per transaction. For a company receiving 20 ILS payments per month, eliminating SWIFT routing saves between $400 and $1,000 in monthly fees alone.

[aa fast-fact]

Fast Fact: ILS transfers via MASAV settle within one business day. SWIFT-routed ILS transfers take 2–5 business days and carry $20–$50 in combined fees per transaction.

[/aa]

Step 4 — Manage ILS Balances and Convert to Your Base Currency

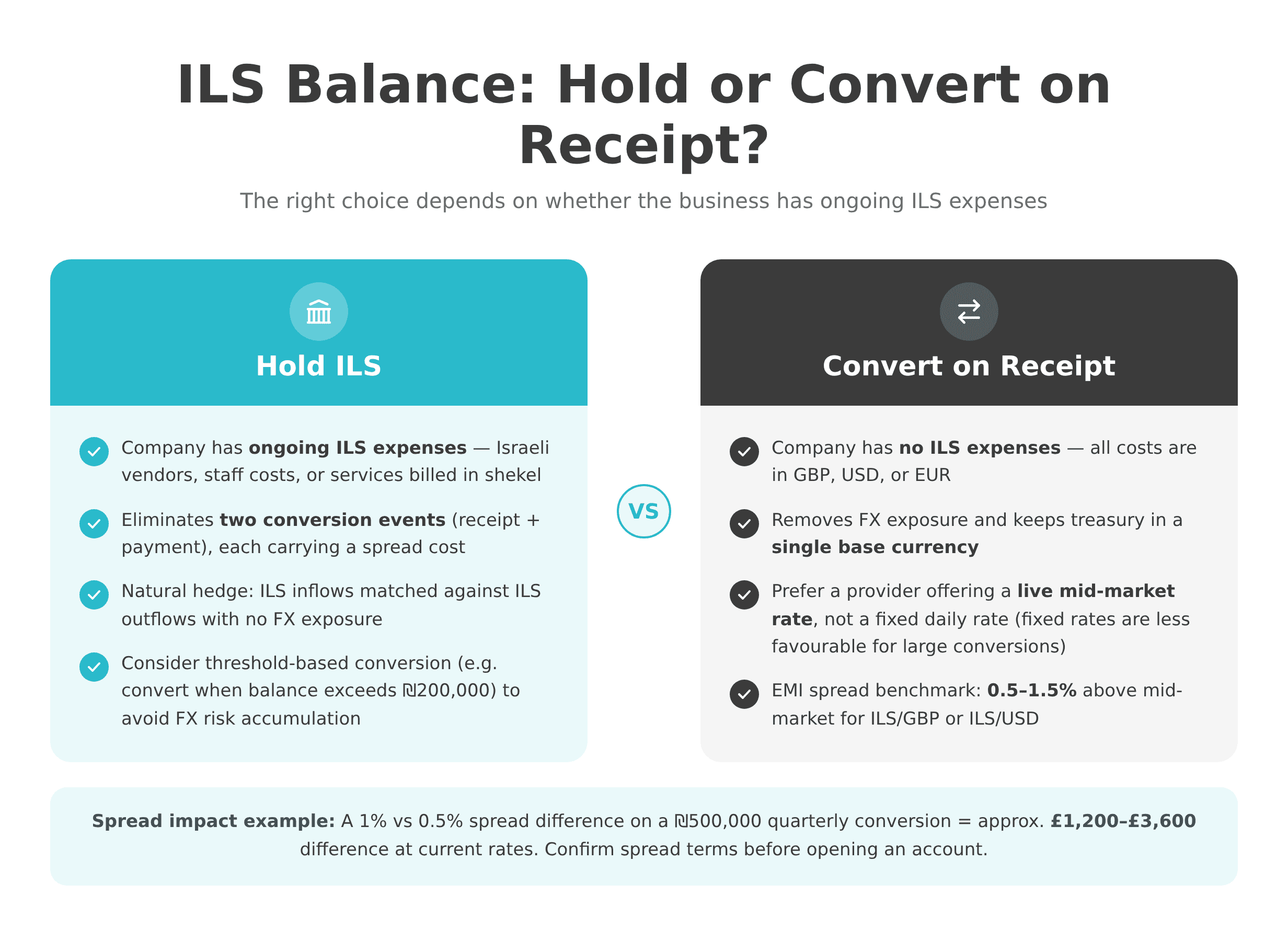

After receiving ILS, companies face a straightforward treasury decision: hold the balance in ILS or convert to a base currency on receipt. The right answer depends on the company's ILS expense profile.

Holding ILS vs Converting on Receipt

Holding ILS makes practical sense when the company has ongoing ILS-denominated outflows — Israeli vendor payments, local staff costs, or service expenses billed in shekel. In that case, receiving and holding ILS eliminates two conversion events, each carrying a spread cost.

Converting on receipt makes more sense for companies with no ILS expenses. It removes FX exposure and keeps the treasury in a single base currency. For businesses receiving ILS quarterly, a threshold-based conversion strategy — converting when the ILS balance exceeds a set amount — is a practical middle ground that avoids both FX risk accumulation and unnecessary conversion frequency.

The ILS has been traded in the CLS (Continuous Linked Settlement) system since 2008, providing final and simultaneous settlement of FX trades and reducing counterparty risk on conversion events.

FX Rate Considerations for ILS/USD and ILS/GBP

The Bank of Israel publishes a daily representative exchange rate for ILS against major currencies — this serves as the market benchmark for ILS/USD and ILS/GBP conversions. EMIs typically apply a spread of 0.5–1.5% above the mid-market rate on ILS conversion.

Finance teams should confirm whether a provider applies a live mid-market rate or a fixed daily rate. Fixed daily rates are consistently less favourable for large single conversions executed later in the trading day. For companies receiving Israeli shekel as a UK registered company or other offshore structure, the difference between a 0.5% and a 1.5% spread on a ₪500,000 quarterly conversion represents approximately £1,200–£3,600 at current exchange rates — a material difference for treasury planning.

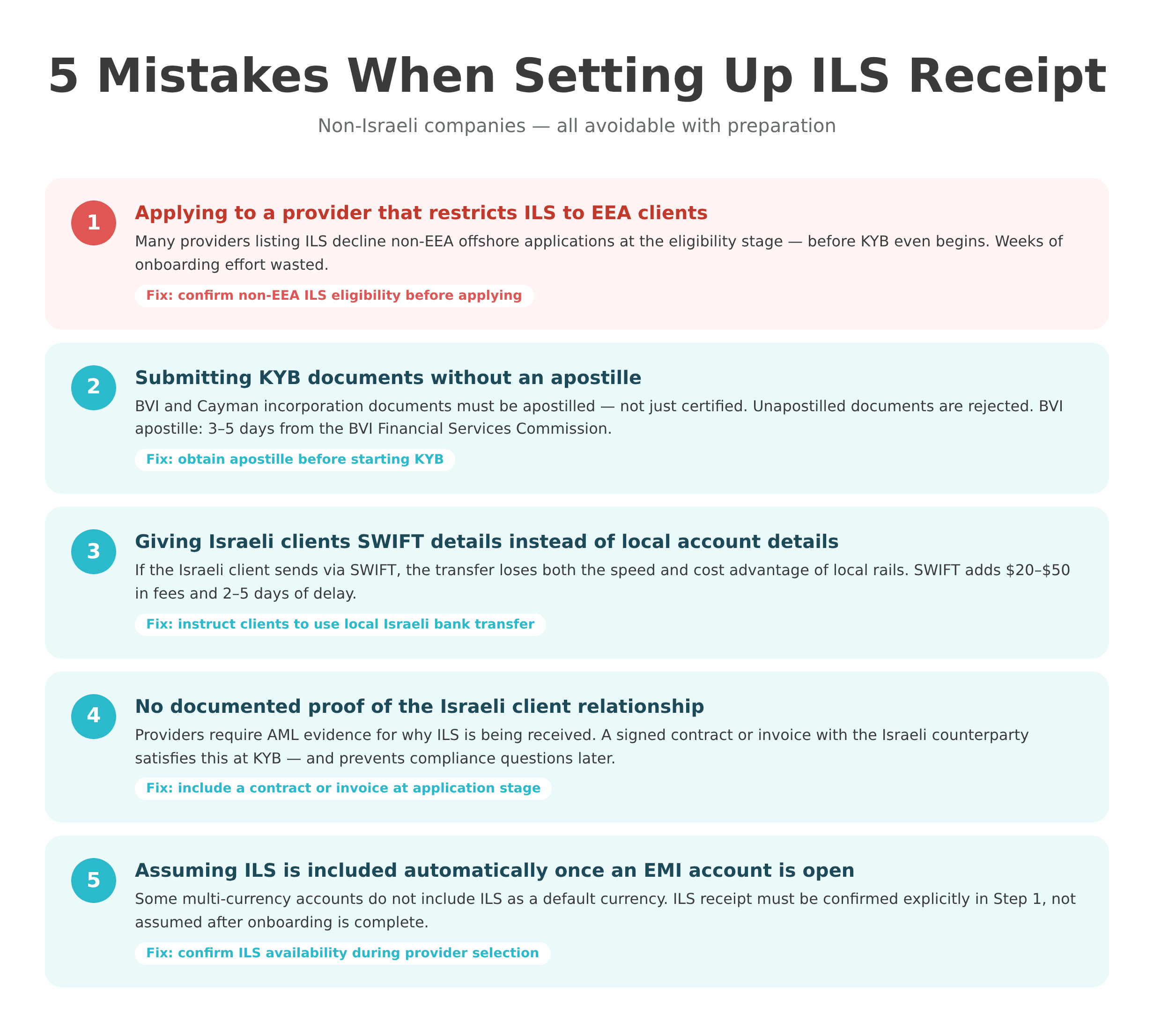

Common Mistakes Non-Israeli Companies Make When Setting Up ILS Receipt

Most problems encountered during ILS account setup fall into five categories. All are avoidable with preparation.

Applying to a provider that restricts ILS to EEA clients. Many providers listing ILS as a supported currency decline non-EEA offshore applications at the eligibility stage. Confirming ILS receipt availability for non-resident corporate entities before applying saves weeks of wasted onboarding effort.

Submitting KYB documents without an apostille where required. For BVI and Cayman entities, unapostilled or uncertified incorporation documents are rejected as a standard compliance measure. The apostille must be on the Certificate of Incorporation itself — not on a cover letter or agent confirmation.

Giving Israeli clients SWIFT details instead of local account details. If the Israeli client is directed to SWIFT, the transfer loses both the speed and cost advantage of local rails. The correct client instruction is: "Please send via local Israeli bank transfer to the following account details."

Failing to document the Israeli client relationship as the source of ILS funds. Providers operating under AML requirements expect documented evidence of why ILS payments are being received. A signed contract or purchase order with the Israeli counterparty satisfies this at the KYB stage — and prevents questions later when volumes grow.

Assuming ILS is automatically included once an EMI account is open. Some multi-currency accounts do not include ILS as a default currency. ILS receipt capability should be confirmed explicitly during provider selection in Step 1, not assumed after onboarding is complete.

[aa cta]

Set Up ILS Receipt for Your Offshore Company

Open a multi-currency account with EQWIRE and start receiving Israeli shekel from Israeli clients without local banking.

[aa btn]Get Started[/aa]

[/aa]

FAQ

Can a BVI company open an ILS business account without visiting Israel?

Yes. A BVI-incorporated company can open an ILS account through an FCA-authorised EMI without travelling to Israel or establishing a local Israeli presence. The application is completed remotely. Required documents typically include the Certificate of Incorporation with apostille, a Register of Directors and Members, UBO passport copies, and proof of business activity with an Israeli counterparty — such as a signed contract or invoice. Onboarding typically takes 3–7 business days once a complete document pack is submitted. The apostille is the most common source of delay: BVI apostilles are issued by the BVI Financial Services Commission and typically take 3–5 business days to obtain. Preparing the apostille in advance of the KYB application reduces the total setup timeline significantly.

How does a non-Israeli company receive ILS from Israeli clients without opening an Israeli bank account?

A non-Israeli company receives ILS by opening an account with an FCA-authorised Electronic Money Institution that supports ILS for non-resident corporate clients. The EMI issues account details compatible with Israeli local payment rails. The Israeli client initiates a standard domestic bank transfer in ILS from their Israeli bank — identical to paying any Israeli-based supplier. The funds settle in the non-resident company's ILS account via MASAV, Israel's interbank clearing system, typically within one business day. No SWIFT transfer is required on the Israeli client's side, and no currency conversion takes place at the point of sending.

What documents does a BVI company need to receive Israeli shekel?

A BVI company typically needs: a Certificate of Incorporation with apostille, a Register of Directors and Members, passport copies for all beneficial owners above 25%, proof of source of funds or business activity — such as a contract or invoice with an Israeli counterparty — and registered address evidence. Some providers may request a bank reference letter or financial statements for higher transaction volumes. The apostille on the Certificate of Incorporation is a hard requirement at EMI onboarding; unapostilled documents are returned without exception. Obtaining the apostille from the BVI Financial Services Commission adds approximately 3–5 business days if not already held.

Can a UAE Free Zone company receive ILS payments from Israel?

Yes. UAE Free Zone entities — including DMCC, DIFC, Jebel Ali Free Zone, and Ras Al Khaimah Free Zone companies — can open an ILS payment account with qualifying EMI providers. Required KYB documentation includes the UAE trade licence, Certificate of Incorporation, UBO passport copies, and evidence of a business relationship with Israeli clients. ILS support for non-EEA entities varies across providers, so eligibility should be confirmed directly before submitting a KYB application. Where eligible, the onboarding process is fully remote and typically completes in 3–7 business days. Israeli clients pay via domestic bank transfer in ILS — no SWIFT conversion is required on their end.

Does receiving ILS require a physical presence or address in Israel?

No. Receiving ILS through an FCA-authorised EMI does not require a physical address, local director, or any registered presence in Israel. The EMI holds ILS on behalf of the non-resident corporate client using its own correspondent access to Israeli payment infrastructure — including the MASAV interbank clearing system and, for large-value transfers, the ZAHAV real-time gross settlement system. The receiving company's registered address can be in the UK, BVI, UAE, Cayman, Bermuda, or any other eligible jurisdiction — the same structural approach that enables offshore-registered entities to access payment infrastructure through FCA-authorised channels without local banking presence.

Receiving ILS as a non-Israeli company is a solved problem, provided the right provider is selected and the KYB application is prepared correctly. The four steps covered here — choosing a qualifying EMI, completing KYB with the correct entity-specific documents, sharing local account details with Israeli clients, and making an informed decision on ILS balance management — reflect a practical and well-established process.

For UK Ltd, BVI, or UAE companies setting up an ILS business account as a non-Israeli entity, the cost case is straightforward. At $20–$50 per SWIFT transaction and 2–3% in FX conversion, a company receiving 20 ILS payments per month eliminates between $400 and $1,000 in monthly fees by switching to a local ILS receipt account. The setup cost is a one-time KYB process taking under a week.

EQWIRE provides FCA-authorised multi-currency accounts with ILS receipt capability for non-Israeli corporate clients. Applications can be submitted via the EQWIRE client portal.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)