•

•

ILS to EUR or GBP: Converting Israeli Shekel for International Businesses

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Cross-border payments between Israel and the UK or EU move through SWIFT rather than SEPA, since Israel sits outside the SEPA zone entirely. For a company holding Israeli shekels, that single fact shapes both the timeline and the cost of an ILS to EUR GBP conversion business account decision.

A client receipt or supplier payment in ILS forces a choice: convert into EUR, convert into GBP, or hold the balance until the rate improves. No single answer fits every business.

The right currency and route depend on where a company invoices, how concentrated its supplier base is, and how much rate risk it can absorb. This article compares the main conversion routes on rate, speed, and compliance, then walks through scenarios for exporters, SaaS businesses, and import-export operators who face this decision regularly.

[aa key-takeaways]

Key Takeaways

Israel is not part of SEPA, so ILS cross-border payments settle through SWIFT and correspondent banking rather than same-day SEPA rails.

Choosing EUR or GBP depends on invoicing currency, supplier concentration, and VAT jurisdiction, not on which rate looks marginally better today.

Banks, fintechs, and UK EMIs handle rate, speed, and compliance differently. No single route wins on all three at once.

Exporters, SaaS companies, and import-export operators each face a distinct version of the EUR-vs-GBP decision.

A multi-currency account lets a business hold ILS EUR GBP balances and choose the conversion moment instead of accepting a forced bank rate.

[aa btn]Book a Call[/aa]

[/aa]

ILS to EUR or GBP: Which Should You Convert To?

An ILS to EUR GBP conversion business account decision starts with three questions, not with today's exchange rate. The first is where the business invoices its own customers. The second is where most of its suppliers sit. The third is which currency its VAT or tax reporting runs in.

A company invoicing EU clients in euros gains little by converting Israeli shekel receipts into pounds first, since that adds a second conversion later. An import-export business paying mostly UK-based suppliers faces the opposite logic and should route toward GBP directly.

Treasury strategy carries similar weight. A business planning to reinvest ILS proceeds into euro-denominated stock should convert to EUR directly, skipping the unnecessary EUR-to-GBP leg that would otherwise add a second spread on the same funds.

A business that pays UK payroll or UK rent converts to GBP instead. Neither route is inherently cheaper. The saving comes from avoiding a second conversion, not from picking a currency that looks stronger on a given day.

The shekel itself is a free-floating currency, with representative rates published daily by the Bank of Israel rather than pegged to a single foreign benchmark. That means the ILS/EUR and ILS/GBP rates can move independently of each other on any given day, sometimes by a meaningful margin.

A business that assumes the two rates move in lockstep can misjudge which currency actually offers the better outcome on a specific date. Checking both rates separately before converting is worth the extra minute.

What Determines the Right Target Currency

Three signals point most reliably to the correct target currency for an Israeli shekel to GBP business transfer:

Invoicing currency: the currency a company already bills its own customers in

Supplier concentration: whether most payables sit in the eurozone, the UK, or both

VAT and tax jurisdiction: which currency tax and reporting obligations are denominated in

A fourth, smaller factor is banking geography. A UK-registered company already holding a GBP account avoids opening a new currency account if GBP is the target. A company with EU subsidiaries may find EUR simpler for internal group settlement, even where the immediate transaction is small.

VAT and tax jurisdiction deserve a closer look than they usually get. A UK-registered business reporting VAT in GBP creates an accounting mismatch every time it converts ILS receipts into EUR and then reconciles them against GBP-denominated returns. Converting directly to GBP removes that extra reconciliation step, even where the headline EUR rate looks marginally more favourable on the day of transfer.

Israeli bank accounts use the IL IBAN format, a 23-character structure and among the longest standard IBANs in use internationally. Payments sent to or from Israel route through SWIFT messages, increasingly migrating to the ISO 20022 messaging standard, and a correspondent bank chain, since Israel is not a SEPA participant. That routing detail affects settlement speed regardless of which target currency a business ultimately chooses.

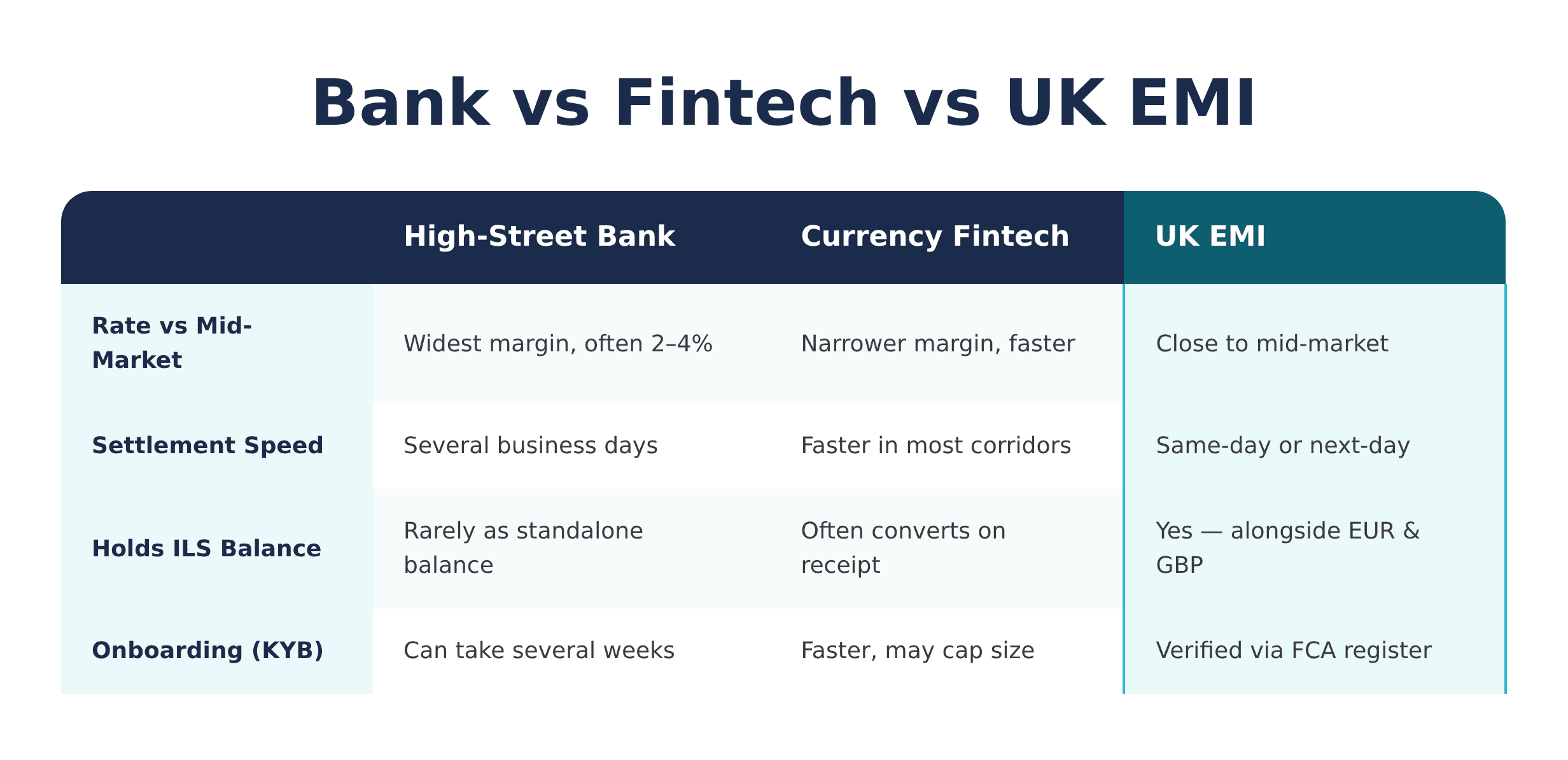

Comparing Conversion Routes: Bank vs Fintech vs UK EMI

Businesses arranging to convert Israeli shekel EUR GBP UK EMI transfers typically choose between a high-street bank, a currency fintech, or a UK electronic money institution (EMI). Each route trades off rate, speed, and compliance differently, and the trade-off rarely resolves in the same direction twice.

High-street banks apply the widest margin above the mid-market rate, often 2 to 4 percent. On a transfer of ₪100,000, that margin alone can amount to several thousand pounds compared with a rate closer to mid-market.

Settlement can take several business days once a correspondent chain is involved, and less common currency pairs such as ILS typically need more correspondent banks than a high-volume corridor like USD to GBP. Each additional bank in the chain adds its own processing window and cut-off time.

Currency fintechs narrow that margin substantially and move faster in most corridors. Many fintechs, however, do not hold ILS as a native balance, so incoming funds convert automatically on receipt rather than staying in shekels until the business chooses to convert.

That removes flexibility for a business that would rather wait for a better rate. Businesses evaluating a fintech for this corridor should confirm directly whether ILS is held as a native balance or converted automatically, since providers rarely state this clearly in marketing materials.

A similar rate-versus-speed trade-off applies when converting AED to GBP, another currency that sits outside SEPA and settles through SWIFT.

UK EMIs regulated by the Financial Conduct Authority (FCA) sit between these two options. They typically offer safeguarded client accounts, rates closer to the mid-market benchmark, and same-day or next-day settlement once documentation clears.

Their advantage grows for businesses holding recurring balances rather than making one-off transfers, since the account itself can hold ILS, EUR, and GBP simultaneously. How an EMI safeguards client funds matters as much as the rate on offer once a balance sits in an account for more than a few days.

Compliance is where the three routes diverge most sharply. A bank's Know Your Business (KYB) process for a new ILS corridor can take several weeks to complete, particularly where the business has no prior transaction history in that currency.

A fintech's onboarding moves faster but may cap transaction size until a business builds a payment history. An FCA-regulated EMI publishes its regulatory status directly on the FCA register, which shortens due diligence for a business that already banks in the UK.

[aa fast-fact]

Fast Fact: The more correspondent banks a payment passes through, the slower and more expensive it becomes, and less common currency pairs such as ILS to GBP or EUR typically need more correspondent banks than high-volume corridors.

[/aa]

[aa cta]

Compare ILS Conversion Routes Without the Guesswork

An EQWIRE multi-currency business account holds ILS EUR GBP balances side by side and settles conversions at a transparent rate.

[aa btn]Open a Business Account[/aa]

[/aa]

Case Scenarios: When Each Option Makes Sense

The right conversion route rarely stays fixed across a business's lifetime. It shifts with transaction volume, supplier count, and how predictable the ILS flow is from month to month.

Documentation requirements shift alongside volume too. A business converting occasionally can usually rely on standard KYB checks completed once at account opening. One converting frequently or in larger amounts should expect a provider to periodically request updated source-of-funds evidence for the ILS corridor specifically.

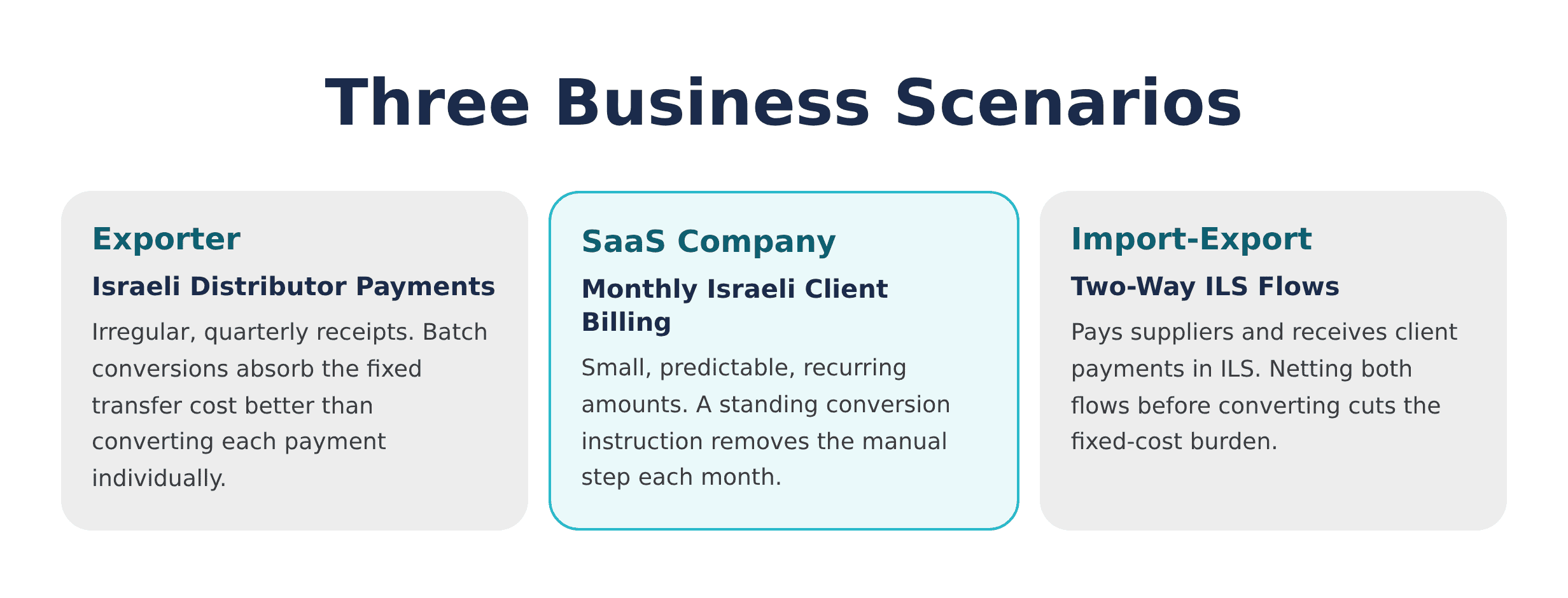

Exporter Selling Goods to Israeli Distributors

An exporter invoicing Israeli distributors in ILS receives payments on an irregular schedule tied to shipment cycles rather than a fixed monthly date. Holding the ILS balance until enough accumulates for one larger conversion often beats converting every receipt individually, since each conversion carries a fixed cost component regardless of size.

This is a case for ILS EUR conversion for UK companies timed around batch conversions rather than per-invoice conversion, particularly where shipment volumes vary quarter to quarter.

A distributor payment of ₪250,000 arriving quarterly, for example, absorbs a fixed transfer cost far better than four smaller transfers of ₪62,500 each, since the fixed cost is paid once instead of four times. The trade-off is exposure: holding a larger ILS balance for longer means more exposure to a rate move before conversion happens.

SaaS Company Invoicing Israeli Clients

A SaaS company billing Israeli clients monthly in ILS faces small, predictable, recurring amounts rather than large irregular ones. A standing conversion instruction with a UK EMI removes the manual step each month.

The predictability of the amount matters more here than rate timing, since the business already knows roughly what it will receive and convert. Automating the conversion also reduces the operational load on the finance team.

Import-Export Business With Two-Way ILS Flows

A business that both pays Israeli suppliers and receives Israeli client payments can net the two flows before converting, reducing the amount that ever touches a currency spread.

Correspondent banking fees apply to each leg of a transfer individually, so netting fewer, larger transfers reduces the fixed-cost burden meaningfully over a year. This scenario benefits most from an account that can hold an ILS balance directly, since netting is only possible if incoming and outgoing ILS do not each get force-converted on arrival.

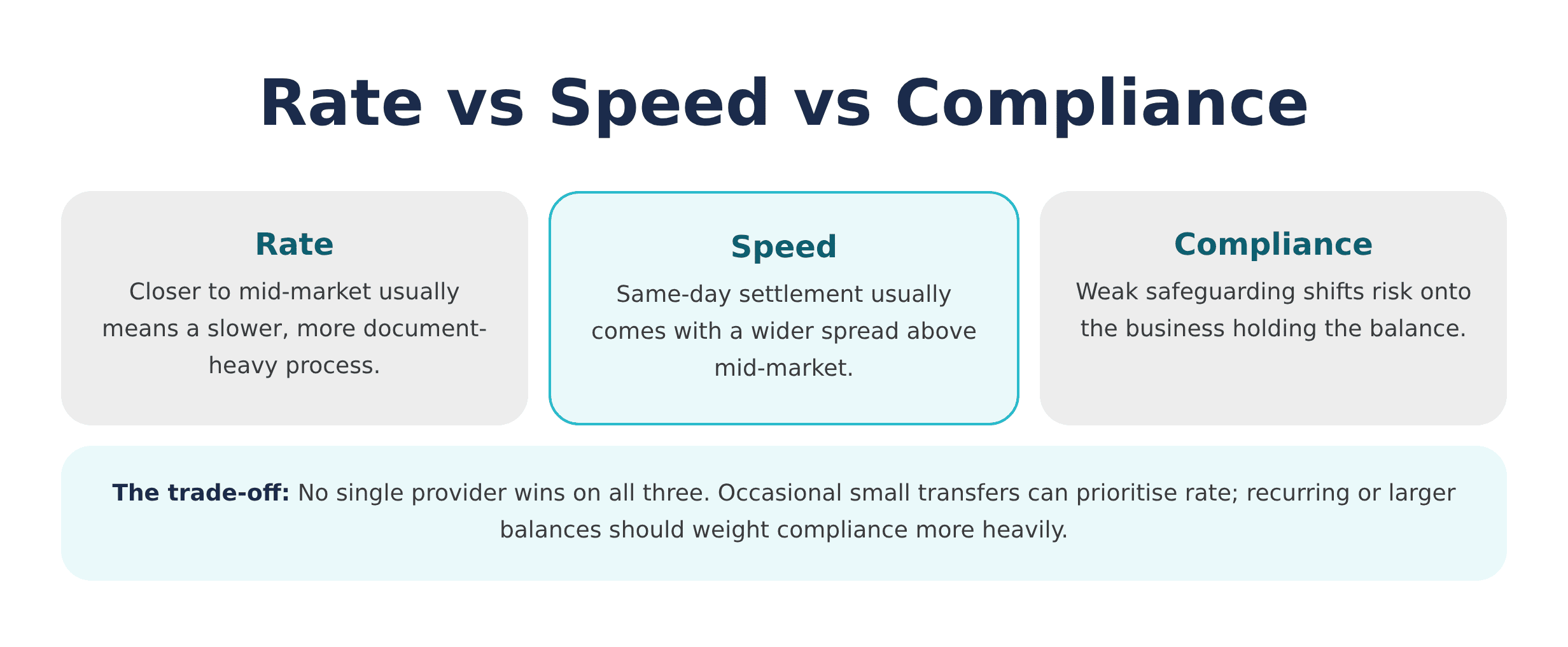

Trade-offs: Rate vs Speed vs Compliance

Rate, speed, and compliance rarely improve together when arranging an ILS to GBP or EUR conversion, much as businesses find when converting CNY to GBP or EUR through a similarly non-SEPA corridor. A same-day settlement usually comes with a wider spread above the mid-market rate. A rate close to mid-market usually comes with a slower, more document-heavy process.

The mid-market rate is the benchmark banks use between themselves. It is rarely the rate offered directly to a retail or business customer.

The gap between the mid-market rate and the quoted business rate is the real cost of a conversion, and it matters more than any advertised flat fee. A business quoted "zero fees" on an ILS transfer should still check the exchange rate against the mid-market benchmark before assuming the transfer is genuinely cheap.

A one percent hidden markup on a ₪500,000 conversion costs roughly the same as a flat fee many providers would openly disclose.

Compliance adds a third variable that is easy to underweight when comparing quotes. A provider offering the best headline rate but weak safeguarding protections shifts risk onto the business holding the balance.

An FCA-regulated UK EMI safeguards client funds in segregated accounts under the Electronic Money Regulations, a protection that matters more for a business holding an ILS EUR GBP balance for several weeks than for one converting and withdrawing immediately.

The practical implication follows directly from this. A business converting occasionally and in small amounts can reasonably prioritise rate above everything else.

One holding recurring balances or larger sums should weight compliance and safeguarding more heavily, even where that means accepting a marginally wider spread. Businesses that reassess this trade-off only once, at account opening, often carry the wrong balance for years as transaction volumes grow.

A useful habit is revisiting the rate-speed-compliance balance whenever ILS transaction volume changes materially, rather than leaving the original provider choice unexamined. A business that started converting ILS occasionally and now does so weekly is often still using a provider chosen for a very different transaction profile.

FAQ

Best way to convert ILS to GBP or EUR for businesses paid in Israeli shekel?

There is no single best way to convert ILS to GBP or EUR for businesses paid in Israeli shekel. The right route depends on transaction size, frequency, and how much compliance documentation a business already has in place. For occasional, smaller transfers, a currency fintech typically offers the fastest onboarding and a rate close to mid-market. For recurring or larger balances, an FCA-regulated UK EMI adds safeguarding protections that a fintech or high-street bank may not match at a comparable rate.

Is Israel part of SEPA?

No. Israel is not a SEPA member, so cross-border ILS payments to and from Israel settle through the SWIFT network rather than SEPA Credit Transfer or SEPA Instant. Businesses should plan for a correspondent-bank settlement timeline of several business days rather than SEPA's same-day or near-instant transfers.

How long does an ILS to GBP or EUR transfer take?

Most ILS to GBP or EUR transfers settle within a few business days, and the exact timing depends on how many correspondent banks sit in the payment chain. Same-day or next-day settlement is possible with a UK EMI or fintech once a business's documentation is verified, but a first transfer through a new provider usually takes longer while checks are completed.

Should a business convert ILS to EUR or GBP?

The decision should follow the business's own invoicing currency and supplier base rather than which rate looks better on a given day. A business invoicing EU clients or paying eurozone suppliers gains more by converting directly to EUR. One paying UK-based costs or reporting VAT in GBP should convert to GBP to avoid an unnecessary second conversion later.

Can a business hold ILS balances instead of converting immediately?

Yes. A multi-currency business account can hold an ILS balance alongside EUR and GBP balances without forcing an immediate conversion. This suits businesses with irregular ILS receipts, since it allows batching several receipts into one larger conversion instead of paying a fixed cost on every individual transfer.

[aa cta]

Hold and Convert ILS Receivables Without Forced Bank Rates

Open a multi-currency business account and choose when, and into which currency, an ILS balance gets converted.

[aa btn]Open a Business Account[/aa]

[/aa]

Converting Israeli shekel for a UK or EU-facing business is rarely a single decision made once. It is a recurring choice shaped by invoicing currency, supplier concentration, and how much rate risk a business can hold at any given time.

Because Israel sits outside SEPA, every option runs through SWIFT and correspondent banking, which puts a floor under settlement times regardless of provider. What changes between a bank, a fintech, and a UK EMI is the rate offered, how fast documentation clears, and how the balance is safeguarded while it sits in an account.

An ILS to EUR GBP conversion business account that separates the conversion decision from the receipt of funds gives a business more control than accepting whatever rate a bank applies by default. Reviewing invoicing currency and supplier concentration first makes the EUR-or-GBP choice, and the provider choice that follows it, considerably more straightforward.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)