•

•

How to Pay Israeli Suppliers or Employees in ILS from a UK Account

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Consult qualified professionals before making decisions.

[/aa]

A UK company receives an invoice from an Israeli software developer — denominated in Israeli shekel (ILS), not in pounds. The finance team opens their online banking, looks for a way to pay Israeli suppliers ILS UK account SWIFT, and quickly realises that ILS is not a currency their bank handles in any straightforward way. This guide covers why Israeli counterparts request ILS, how SWIFT transfers to Israel work from a UK account, how an FCA-authorised EMI compares, and how to structure recurring ILS payments. For broader context, see EQWIRE’s cross-border business payments guide.

[aa key-takeaways]

Key Takeaways

ILS payments from UK accounts travel via SWIFT — Israel is not in the SEPA zone.

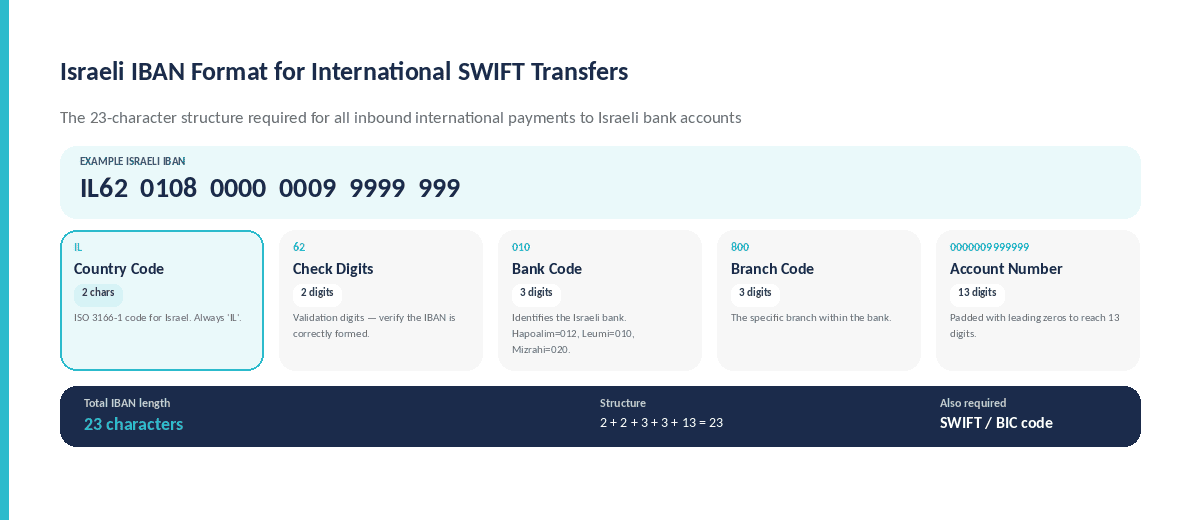

An Israeli IBAN is 23 characters long (starting IL) and is mandatory for SWIFT payments.

SWIFT correspondent charges of $10–30 per hop are deducted silently — the beneficiary receives less.

FCA-authorised EMIs offer lower FX margins (0.3–1%) vs high-street banks (1.5–3%).

UK businesses do not need a local Israeli bank account to pay in ILS.

Converting a lump sum GBP to ILS once per month reduces total FX cost.

[aa btn]Book a Call[/aa]

[/aa]

Why Israeli Suppliers and Employees Request Payment in ILS

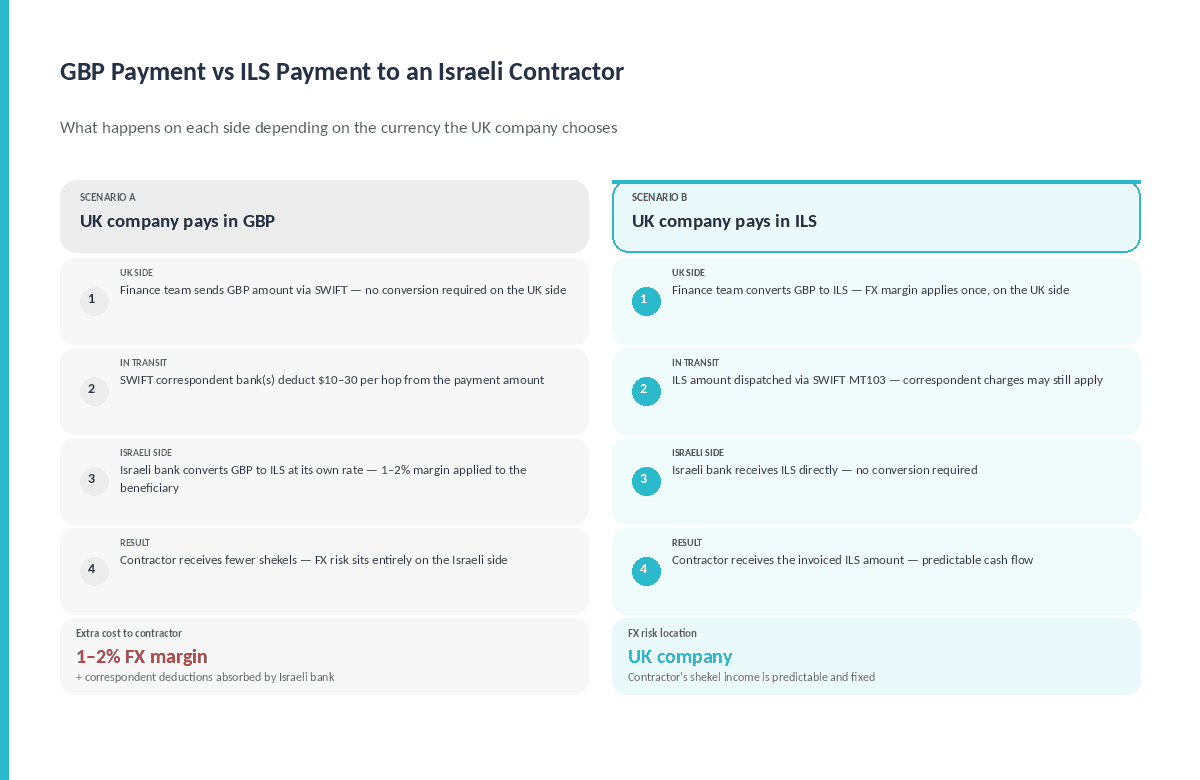

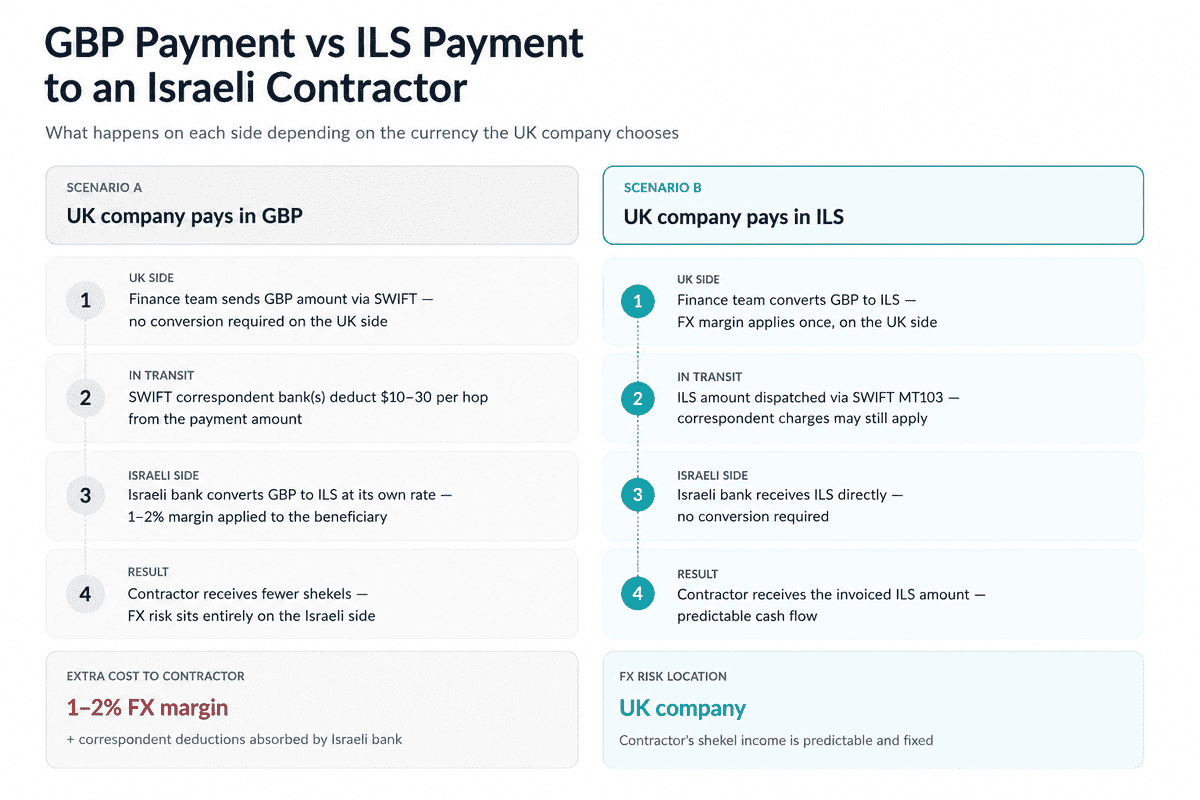

Israeli counterparts request ILS payment because their operating costs are denominated in shekel. An invoice settled in GBP shifts the FX risk entirely onto the Israeli recipient.

FX Risk and Local Cost Structures for Israeli Counterparts

The Bank of Israel maintains a managed float for the shekel. GBP/ILS has moved by 10–15% within individual 12-month windows — a meaningful margin swing for a contractor billing at a fixed GBP rate. A developer invoicing £5,000 per month who receives GBP takes on currency risk with every payment cycle.

What Happens When UK Companies Pay in GBP Instead

When a UK company pays GBP against an ILS invoice, the Israeli bank converts at its own interbank rate — typically with a 1–2% margin. The contractor raises the next invoice at a GBP premium to self-hedge. Paying in ILS removes that dynamic.

SWIFT for ILS Payments from the UK: How It Works and What It Costs

Every ILS payment from a UK account goes out as a SWIFT MT103 message, routing through a correspondent chain. Israel is not in the SEPA zone — SEPA Credit Transfer does not apply.

Payment Details Required for an Israeli Beneficiary

Israeli IBAN: Israeli IBANs are 23 characters: IL + 2 check + 3 bank + 3 branch + 13 account. Example: IL62 0108 0000 0009 9999 999. SWIFT/BIC: 8–11 chars. Bank Hapoalim = POALILITXXX, Bank Leumi = LUMIILIT, Israel Discount Bank = IDBLILITXXX, Mizrahi Tefahot = MIZBILIT. See theswiftcodes.com. Also required: beneficiary full name and bank name/branch address.

Correspondent Bank Charges and Hidden FX Margin

UK bank outgoing fee: £9.50–£25. Correspondent charges: $10–30 per hop deducted silently in transit. FX margin: 1.5–3% at high-street banks. Under the Payment Services Regulations 2017, providers must disclose rates before execution. Settlement: 1–2 days priority, 2–3 days standard.

[aa fast-fact]

Fast Fact: SWIFT correspondent charges of $10–30 per hop are deducted from the payment amount in transit — not from the sender’s account. The beneficiary receives less than instructed without clear notification.

[/aa]

[aa cta]

Pay Israeli Suppliers in ILS Without Hidden Correspondent Charges

EQWIRE’s multi-currency account supports ILS as a named balance currency. Convert GBP to ILS once, send directly via SWIFT — with transparent fees shown before execution.

[aa btn]Create Account[/aa]

[/aa]

The FCA-Authorised EMI Route: Sending ILS Without a Traditional Bank

FCA-authorised EMIs can hold ILS balances in a multi-currency account. See how an FCA-authorised EMI differs from a UK bank. ILS still travels via SWIFT — the EMI advantage is on FX margin and fee transparency.

Multi-Currency ILS Accounts for UK Businesses

EMIs apply 0.3–1% for GBP-to-ILS conversion vs 1.5–3% at a high-street bank. On £20,000 of ILS payments per month, the saving is £240–£400/month (£2,880–£4,800/year). A named IBAN account assigned directly to the business simplifies reconciliation.

What to Verify Before Opening an EMI Account for ILS

Check the firm reference number on the FCA register. Confirm ILS is available as a named outgoing currency. Confirm outgoing SWIFT is supported. Following Israel’s Regulation of Payment Services Law 2023, new nonbank institutions have entered the market — but SWIFT remains the UK-to-Israel transfer mechanism.

Step-by-Step: Initiating an ILS Payment from a UK Account

Information to Collect from the Israeli Supplier or Employee

Full legal name as it appears on the bank account

Israeli IBAN (23 chars, starting IL)

Bank SWIFT/BIC code (e.g. POALILITXXX for Bank Hapoalim)

Bank name and branch address

For recurring payments, store in a secured beneficiary register.

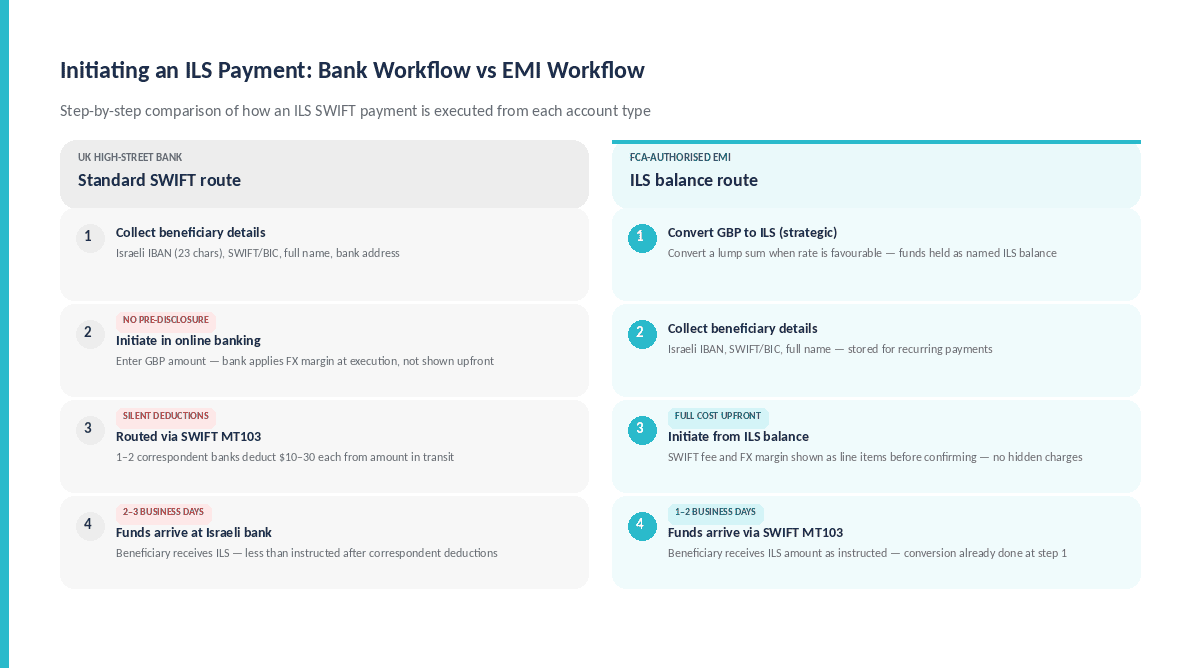

Executing the Transfer: Bank vs EMI Workflow

Via UK high-street bank: Select ILS, enter IBAN and BIC, confirm GBP amount. Rate applied at execution, not disclosed upfront. Correspondent fees deducted in transit. Settlement 2–3 business days.

Via FCA-authorised EMI: Payment instructed from ILS balance — no conversion at point of payment. Full fee breakdown shown before confirmation. Both routes deliver via SWIFT MT103.

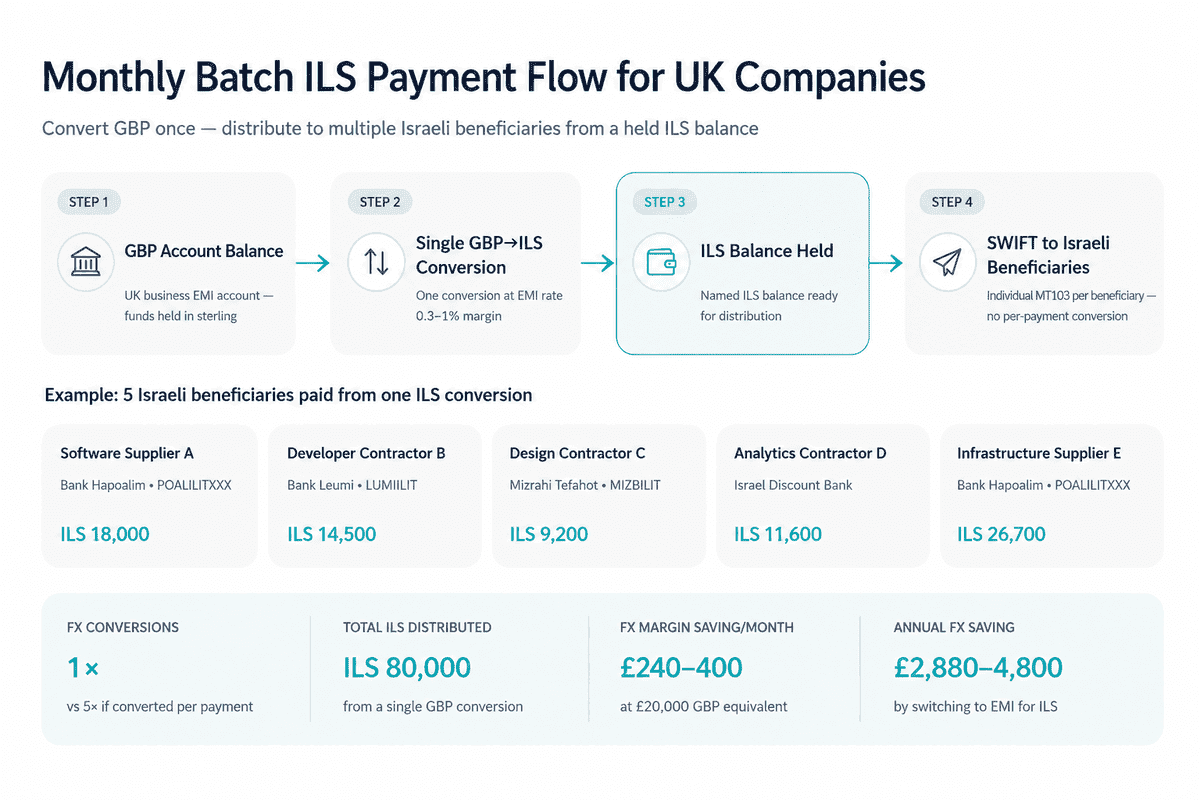

Paying Multiple Israeli Contractors in Shekel: Recurring and Batch Payments

Batch ILS Payments for Payroll and Supplier Runs

For companies managing ILS batch supplier payments to 3–10 Israeli beneficiaries: (1) Convert a single GBP amount to ILS at the start of the cycle. (2) Hold the ILS balance. (3) Initiate individual SWIFT payments to each beneficiary — no per-payment conversion.

GBP-to-ILS Conversion: Timing and Cost Management

GBP/ILS rates fluctuate daily in response to Bank of Israel policy, geopolitical news, and UK inflation data. Finance teams benefit from converting a lump GBP sum at the start of the cycle — separating the FX decision from payment execution.

[aa fast-fact]

Fast Fact: GBP/ILS has moved by 10–15% in individual 12-month windows. For a UK company paying ILS 80,000 monthly, a 5% adverse rate movement represents approximately ILS 4,000 (c.£850) in unbudgeted cost per cycle.

[/aa]

FAQ

How do I pay an Israeli supplier in ILS from a UK bank account?

Paying an Israeli supplier in ILS requires initiating a SWIFT international transfer. The sending bank needs the beneficiary’s Israeli IBAN (23 chars, starting IL), SWIFT/BIC code, and full legal name. The bank dispatches a SWIFT MT103 message routing through 1–2 correspondent banks — taking 1–3 business days. An FCA-authorised EMI with ILS balance support allows the same SWIFT route at a lower FX margin.

What IBAN format does Israel use for SWIFT transfers?

Israeli IBANs are 23 characters long and begin with IL. Structure: IL (2) + check digits (2) + bank code (3) + branch code (3) + account number (13). Example: IL62 0108 0000 0009 9999 999. The IBAN is mandatory for all incoming international SWIFT transfers.

Can a UK company pay Israeli contractors in shekel without maintaining a local bank account in Israel?

Yes. UK companies can do so entirely through SWIFT from a UK business account. The UK business needs only its own UK account, the contractor’s Israeli IBAN and BIC, and access to outgoing SWIFT transfers. No Israeli entity or local bank account is required.

How long does an ILS SWIFT transfer from the UK take?

1–2 business days for priority transfers (before 2pm GMT cut-off), or 2–3 business days for standard transfers. AML screening at the correspondent level can occasionally add 24 hours.

What are the costs of sending ILS from a UK business account to Israel?

Three layers: (1) Outgoing wire fee: £9.50–£25. (2) Correspondent charges: $10–30 per hop, deducted silently. (3) FX margin: 1.5–3% at banks, 0.3–1% at FCA-authorised EMIs. For a £3,000 payment, total costs at a high-street bank can reach £100–£150; FCA-authorised EMIs reduce this to £20–£40.

UK businesses can pay Israeli suppliers in ILS efficiently from a standard UK account. The real variable is cost. EQWIRE supports ILS as a multi-currency balance currency. Businesses can create an account and begin structuring ILS payments within the same workflow used for GBP and EUR.

[aa cta]

Open a Multi-Currency Account for ILS Payments

Send ILS to Israeli suppliers and contractors via SWIFT — with named ILS balance, transparent FX pricing, and no hidden correspondent deductions.

[aa btn]Create Account[/aa]

[/aa]

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)