•

•

AED to GBP FX Conversion: How to Convert Dirhams Without Hidden Markups

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Banks routinely fold a 2-5% markup into the exchange rate on cross-border transfers, pricing it into the rate itself instead of listing it as a separate fee. A company running a routine AED to GBP conversion business account transfer of £50,000 a month can lose more than £1,500 to that markup without seeing it itemised anywhere.

The path to AED to GBP without hidden markup starts with the account setup, not the transfer itself. Converting through a regulated electronic money institution (EMI) account that fixes the rate before the transfer executes removes the markup structurally, rather than a retail bank applying its own spread after the fact.

This guide sets out the documents an offshore or import-export business needs before opening the account, the exact sequence to follow when converting, the mistakes that cost the most money, and how to move from one-off transfers to a repeatable batch process as AED volume grows.

[aa key-takeaways]

Key Takeaways

Opening an AED to GBP conversion business account requires company incorporation documents, UBO/KYC checks, and proof of the AED-denominated funding source.

Converting without a hidden markup means fixing the rate against the mid-market benchmark before the transfer is sent, not after.

Retail banks typically embed a 2-5% markup into the exchange rate; FCA-regulated EMI accounts show the rate and fee separately.

The costliest mistakes are converting through a retail bank instead of an EMI, and accepting a quote without locking the rate.

Recurring or batch AED-GBP conversions can be scheduled once the account is set up, cutting manual work and per-transfer markup exposure.

Settlement typically takes one to five business days via SWIFT, or the same business day once converted GBP moves domestically via Faster Payments.

[aa btn]Book a Call[/aa]

[/aa]

What You Need Before Opening an AED to GBP Conversion Business Account

Opening an AED to GBP business account requires a specific set of documents before any provider accepts the application. Offshore companies face closer scrutiny than domestic UK businesses, since the account will hold and convert funds originating outside the UK.

Most FCA-regulated EMI providers request the following before approving an account:

Certificate of Incorporation and Memorandum & Articles of Association

Register of Directors and Ultimate Beneficial Owners (UBO)

Proof of business address and a description of the AED-denominated income source

Individual KYC documents for each UBO holding 25% or more of the company

A recent bank or EMI statement showing the AED balance to be converted

This applies to companies incorporated in offshore jurisdictions such as UAE free zones or the BVI. Mauritius-registered entities face the same requirement: providers expect evidence of the underlying trading activity that generates the AED balance. Standard high-street banks rarely accept offshore corporate structures at all, regardless of the exchange rate they would eventually charge.

[aa fast-fact]

Fast Fact: FCA-regulated EMIs safeguard client funds under the FCA safeguarding requirements set out in the Electronic Money Regulations 2011, holding them in a segregated account kept separate from the firm's own operating funds.

[/aa]

An AED GBP exchange rate EMI account verifies this documentation once, at onboarding, rather than re-checking it before every transfer. Once approved, the business can convert AED to GBP for business purposes on a recurring basis without repeating the compliance review each time.

Verifying a provider's status on the FCA Financial Services Register before opening an account confirms the EMI is actually authorised, not simply claiming to be.

FCA-authorised EMIs operate under the Payment Services Regulations 2017 and the Electronic Money Regulations 2011, the two frameworks that govern how payment and e-money firms handle client funds.

The safeguarding vs FSCS protection distinction matters here. EMI-held funds are ring-fenced under the Electronic Money Regulations 2011, not covered by the Financial Services Compensation Scheme the way a bank deposit would be. The segregation requirement still offers strong practical protection, even though it works through a different legal mechanism than deposit insurance.

Businesses that convert AED to GBP for offshore company banking on a recurring basis should weigh a multi-currency wallet against an FCA EMI for offshore companies specifically on document requirements, not just headline rates. Multi-currency wallets aimed at freelancers and small transfers often skip UBO-level documentation entirely, which is also why they cap transfer sizes lower than a fully verified EMI account can support.

Account approval for an offshore company typically takes longer than for a standard UK business account, since the provider has to trace the source of the AED funds rather than relying on an existing UK banking history. A trading company registered in a UAE free zone, for example, can expect the provider to request supplier or client contracts alongside the standard UBO documents, to confirm the AED balance comes from genuine trading activity rather than an unrelated source. FCA guidance on payment services and e-money firms sets out exactly this kind of source-of-funds expectation for higher-risk applicants.

Once that trading history sits on file inside the EMI, later conversions move faster, because the underlying risk profile has already been reviewed once rather than reassessed on every transfer.

Step-by-Step Checklist: Convert AED to GBP Without Hidden Markup

Converting AED to GBP without a hidden markup follows a fixed sequence, not a single transaction. AED is pegged to the US dollar at a fixed rate of 1 USD = 3.6725 AED, maintained by the Central Bank of the UAE since 1997.

The AED-GBP price is therefore a cross-rate through USD rather than a direct peg, exactly the pricing point where retail banks add their spread. The dirham to pound sterling exchange is quoted continuously throughout the trading day, so the rate available in the morning and the rate available in the afternoon on the same day can differ by a meaningful margin on a large transfer.

A mid-market exchange rate business account setup separates the exchange rate from the transfer fee, so a business can see precisely what it is paying for the conversion itself, rather than one blended number. This is the actual answer to how to convert AED to GBP for a business without guesswork: a fixed, repeatable sequence rather than a one-off negotiation each time.

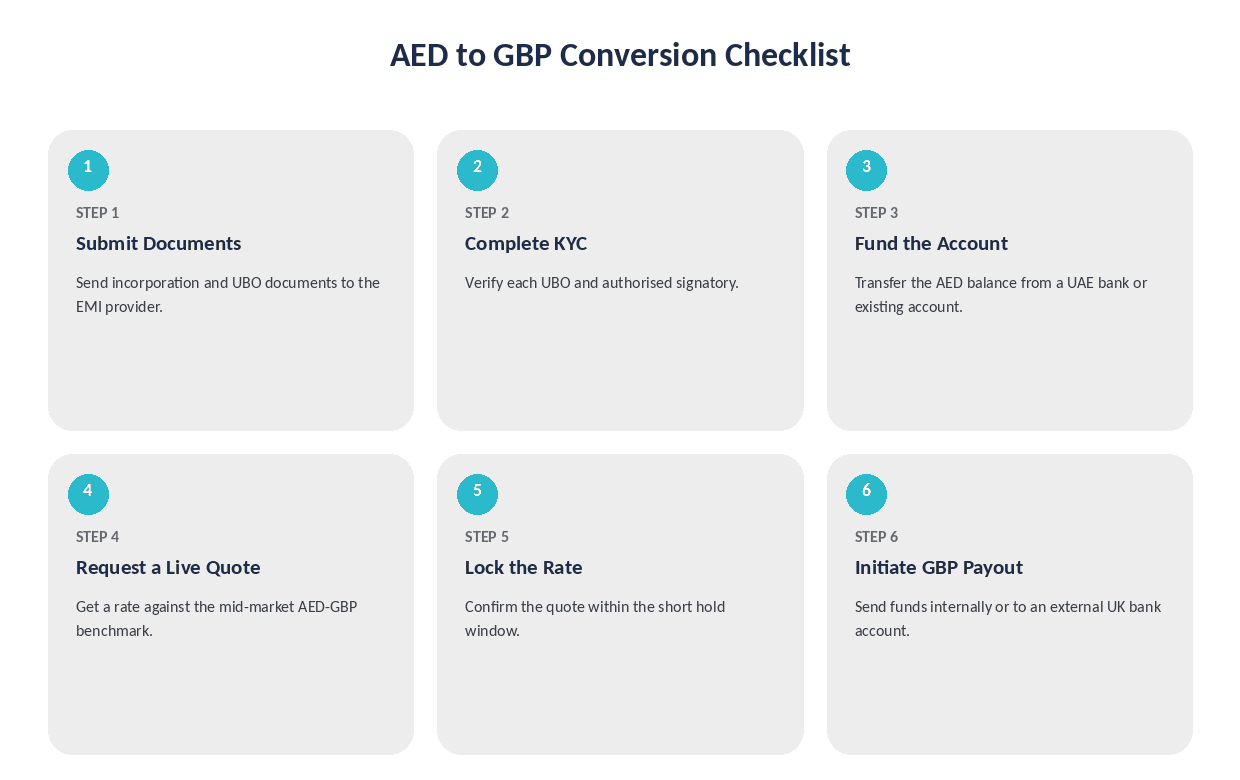

Steps 1–3: Account Setup and Verification

Submit the incorporation and UBO documents to the EMI provider.

Complete KYC verification for each UBO and authorised signatory.

Fund the account with the AED balance to be converted, either from a UAE bank or an existing AED-denominated account.

Steps 4–6: Rate Fixing and Transfer Initiation

Request a live quote against the mid-market AED-GBP rate before confirming anything.

Lock the quoted rate. Most EMI accounts hold it for a short window measured in minutes, not days.

Confirm the conversion and initiate the GBP payout, either within the same account or to an external UK bank account.

What this means in practice: once the account exists and the documents are on file, a business can convert AED to GBP for business purposes in minutes rather than days, since only steps 4 to 6 repeat on every subsequent transfer.

Skipping step 5 and accepting a quote without locking it undoes the benefit of the entire process, since the rate can move before the transfer settles. The next section covers exactly how much that costs.

Common Mistakes That Cost Businesses Money on AED-GBP Conversion

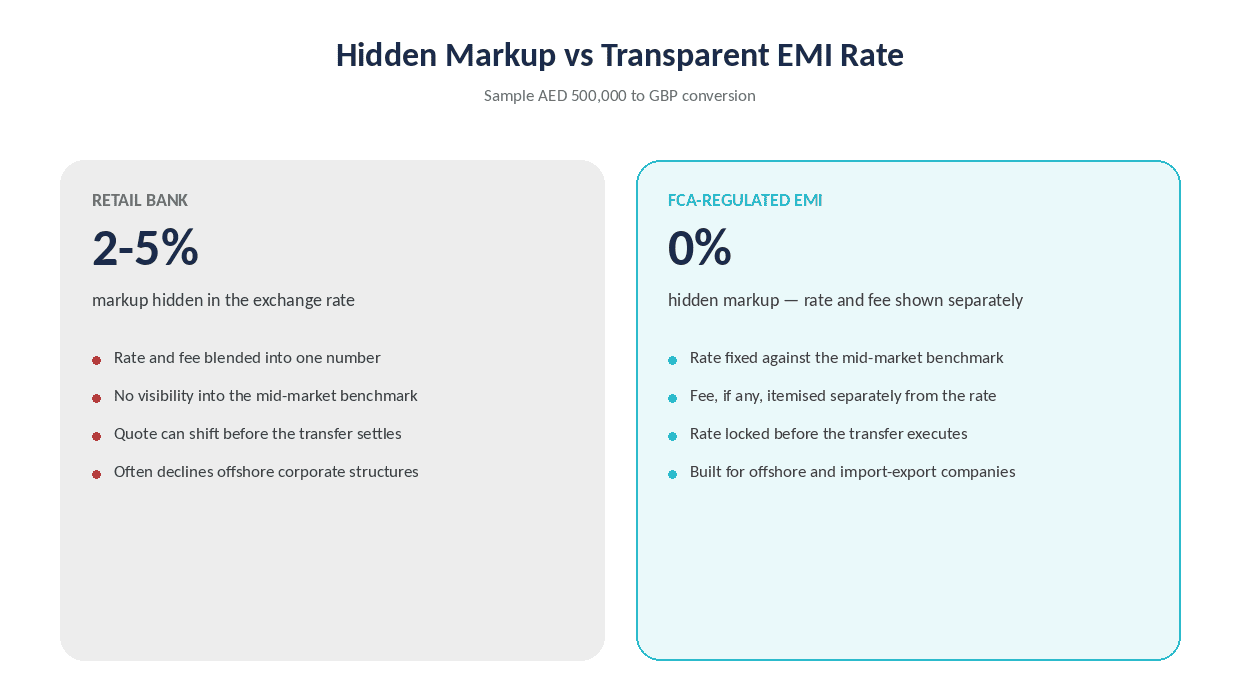

The most expensive mistake is converting through a retail bank account instead of an EMI, since banks embed a 2-5% markup directly into the AED-GBP exchange rate rather than charging a separate, visible fee. On a £100,000 conversion, that markup alone can cost between £2,000 and £5,000 before any transfer fee is added.

The most common UAE dirham to GBP business transfer mistake is treating every transfer as a one-off event, negotiated or accepted individually, rather than building a repeatable process around a single trusted provider.

Converting Through a Retail Bank Instead of an EMI Account

Retail banks often advertise a transfer with "no fee," while pricing the conversion at a rate several percentage points away from the mid-market benchmark. Checking the live GBP-AED rate before initiating a conversion makes the gap visible immediately: a business can compare the bank's quoted rate against the published mid-market rate to see the exact markup being charged.

Correspondent banking fees add a further layer of cost when a transfer routes through multiple intermediary banks rather than a direct settlement network, with each bank deducting a handling fee before the funds reach their destination.

Not Fixing the Rate Before the Transfer

A quoted rate that is not locked can move before the transfer settles, particularly on transfers that take several business days to clear through a SWIFT correspondent chain. This is what business FX conversion without markup actually requires: locking the rate at the point of conversion, not at the point of initiating a bank wire.

[aa fast-fact]

Fast Fact: A 3% hidden markup on a £1,000,000 AED-GBP conversion equals £30,000 lost to the exchange rate alone, before any transfer fee.

[/aa]

Mistake | Typical Cost Impact |

|---|---|

Converting via retail bank instead of EMI | 2–5% of transfer value |

Accepting a rate that isn't locked | Variable, rate-dependent |

Converting one-off instead of batching | Repeated fees per transfer |

[aa cta]

Convert AED to GBP Without the Guesswork

Fix the rate before sending the transfer and see the exact GBP amount landing in the account, with no hidden spread.

[aa btn]Open a Business Account[/aa]

[/aa]

Setting Up Recurring or Batch AED to GBP Conversions

Businesses converting AED to GBP for business purposes on a recurring basis can set up batch conversions rather than repeating the manual process for every transfer.

Companies receiving AED payouts from multiple sources, marketplace settlements and PSP payouts among them, often accumulate balances that can be converted together instead of converting each incoming payment individually. Businesses already receiving AED payouts from PSPs such as Adyen or Stripe typically see the clearest benefit from batching. The same applies to businesses settling through PayPal, since those payouts also arrive on a predictable schedule.

Setting a recurring UAE dirham to GBP exchange rate check, rather than reacting to each incoming payment, also makes it easier to time conversions around the rate instead of converting reflexively every time AED lands in the account. Avoiding forced conversion on incoming multi-currency payouts keeps the AED balance available in its original currency until the business actively chooses to convert it.

What this means in practice: an accountant reviewing monthly AED-GBP volume can convert once at a locked rate, instead of processing ten separate wires, each carrying its own quote and its own exposure to rate drift.

Batch conversion also simplifies reconciliation. A single monthly conversion produces one exchange rate and one line item to match against the incoming AED total, rather than several different rates applied across several separate transactions spread through the month.

Providers that support scheduled conversions typically allow a business to set a threshold, converting automatically once the AED balance crosses a set amount, which removes the need to monitor the account manually for a good moment to convert.

An import-export business receiving AED payments from several UAE buyers each month illustrates the difference clearly. Converting each payment individually as it arrives means accepting whatever rate is live at that moment, several times a month, with a fee-equivalent markup attached to each one. Consolidating those same payments into a single scheduled conversion turns several small, unpredictable costs into one negotiated transaction at a known rate.

[aa cta]

Set Up Recurring AED-GBP Conversions

Batch conversions and stop paying a markup on every single transfer.

[aa btn]Get Started[/aa]

[/aa]

How Long Does an AED to GBP Conversion Actually Take

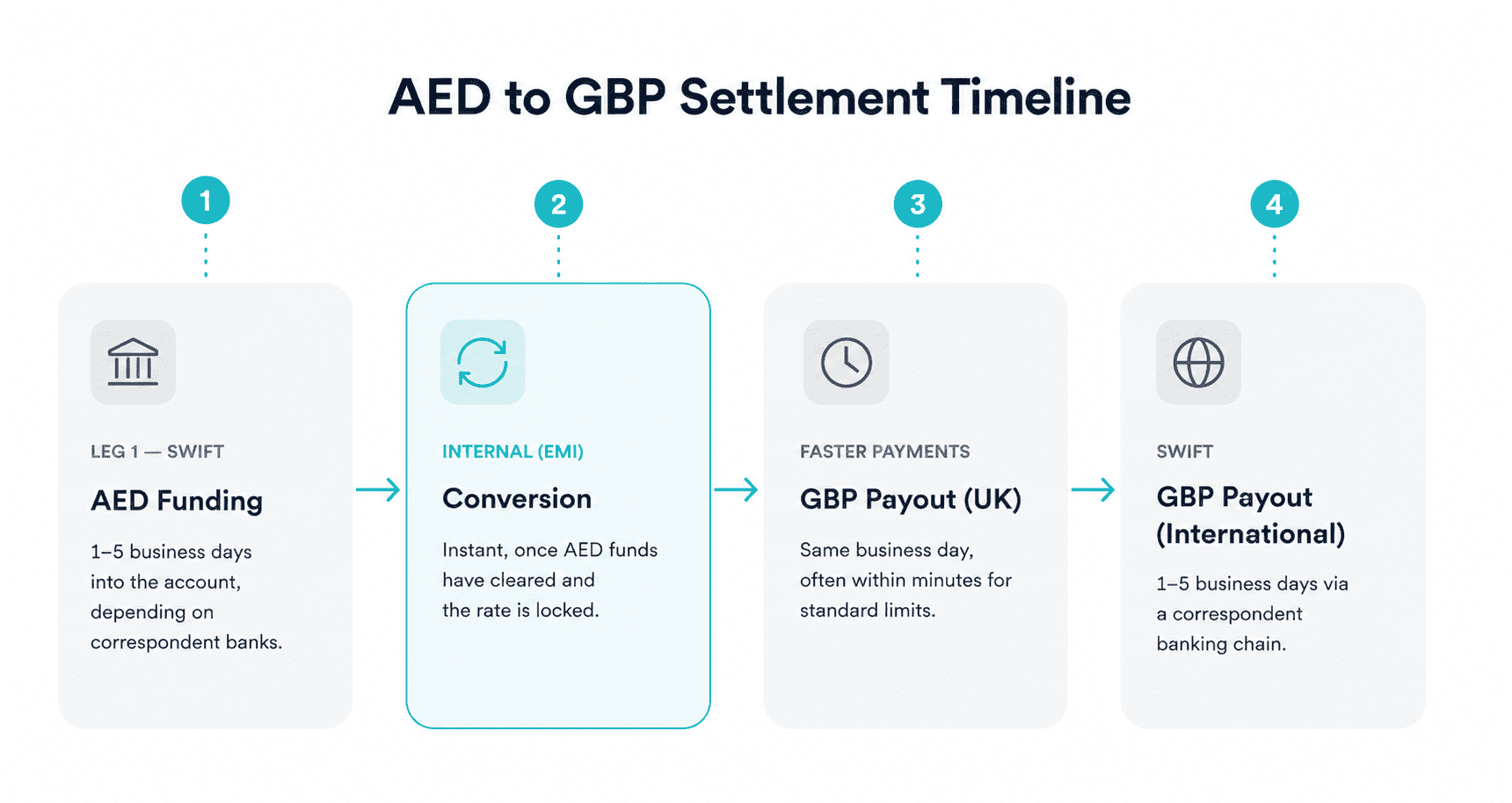

An AED to GBP conversion through a business account typically takes between the same business day and five business days, depending on which leg of the transaction is being measured.

Once AED funds clear inside the account, the conversion to GBP happens instantly at the locked rate. The time businesses actually notice comes from the transfers on either side of that conversion, not the conversion itself.

Leg | Rail | Typical Timing |

|---|---|---|

AED funding into the account | SWIFT | 1–5 business days |

AED to GBP conversion | Internal (EMI) | Instant once funds clear |

GBP payout (UK) | Faster Payments | Same business day |

GBP payout (international) | SWIFT | 1–5 business days |

Funding the account with AED from a UAE bank via SWIFT usually takes one to five business days, depending on the number of correspondent banks the payment passes through. Once converted, moving GBP to a UK bank account via Faster Payments typically settles the same business day, often within minutes for standard transfer limits.

The UK's payment and settlement infrastructure, overseen by the Bank of England, processes the sterling leg of the transaction once conversion completes. An international GBP payout routed through SWIFT again takes one to five business days, since it re-enters a correspondent banking chain.

FAQ

Best way to convert AED to GBP for offshore company with no markup?

The most reliable way to achieve AED to GBP without hidden markup for an offshore company is through an FCA-regulated electronic money institution (EMI) account that quotes a rate against the mid-market benchmark and locks it before the transfer executes. Retail banks typically embed a 2-5% markup directly into the exchange rate they offer, which stays invisible unless the rate is checked against the mid-market benchmark first. For a business asking how to avoid hidden FX markup when converting AED to GBP, the fix is structural rather than a single negotiating tactic: choose a provider that separates the exchange rate from any transfer fee, and confirm the rate before funds move rather than after. For an offshore company specifically, an EMI account also solves a structural access problem, since many UK high-street banks decline offshore corporate structures regardless of the rate they would charge.

What is the process to convert AED to GBP for offshore company accounts?

Opening an account to convert AED to GBP for offshore company banking requires standard incorporation and UBO documentation, proof of business address, and individual KYC checks for major shareholders. Offshore companies additionally need to show the underlying trading activity that generates the AED balance, since providers use this to assess the source of funds. Once approved, the EMI safeguards client funds under the Electronic Money Regulations 2011 by holding them in a segregated account, separate from the firm's own operating funds rather than pooled with its general balance sheet.

How long does an AED to GBP conversion take?

An AED to GBP conversion typically completes within the account instantly once the AED funds have cleared, but the surrounding transfers add time on either side. Funding the account with AED from a UAE bank via SWIFT usually takes one to five business days depending on the number of correspondent banks involved. Once converted, GBP moving to a UK bank account via Faster Payments typically settles the same business day, while an international GBP payout routed through SWIFT again takes one to five business days.

How can a business set up recurring or batch AED to GBP conversions?

Most EMI providers allow a business to save its verified account details after the first conversion, so subsequent AED to GBP conversions only require funding and rate confirmation rather than a full compliance review. Businesses that receive AED payouts from multiple sources, such as marketplace or PSP settlements, can accumulate a balance and convert it on a fixed weekly or monthly schedule instead of converting every incoming payment individually. This reduces the number of separate transactions, each of which carries its own quote and its own exposure to rate movement between quote and settlement.

What mistakes cause businesses to overpay when converting AED to GBP?

The most common and costly mistake is converting through a retail bank account instead of an EMI, since banks embed a 2-5% markup directly into the exchange rate rather than charging a visible fee. The second most common mistake is accepting a quoted rate without locking it, which leaves the conversion exposed to rate movement while the transfer is in transit. A third mistake is converting small amounts individually rather than batching recurring AED balances, which multiplies the number of times a markup or fee applies.

Setting up an AED to GBP conversion business account comes down to two decisions: which provider holds the account, and whether the rate is fixed before the transfer moves. An FCA-regulated EMI account addresses both by separating the exchange rate from any transfer fee and by safeguarding client funds under the Electronic Money Regulations 2011.

Businesses that set up the account correctly from the start avoid the 2-5% markup that retail banks apply by default, and can move from one-off conversions to a scheduled batch process as AED volume grows. EQWIRE's AED to GBP business account setup for offshore and UK-facing companies keeps documentation review to onboarding only, not to every transfer.

Businesses ready to convert AED to GBP without a hidden markup can open a business account at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)